U.S. JOLTS: Job Openings Reach Record Level During May

The Bureau of Labor Statistics reported that on the last business day of May, the level of job openings rose slightly m/m to a record 9.209 million from 9.193 million in April, revised from 9.286 million. The latest increase of 16,000 (69.1% y/y) was the smallest of five straight monthly gains.

The total job openings rate remained at the record 6.0% it reached in April. The openings rate is calculated as job openings as a percent of total employment plus jobs that have not yet been filled.

The hiring rate eased to 4.1% from 4.2%, but remained higher than 3.8% in January & December. The overall layoff & discharge rate eased to a record low of 0.9% from a downwardly revised 1.0% in April. The quits rate fell to 2.5% after surging to a record high of 2.8% in April, revised from 2.7%. The number of quits has risen by roughly two-thirds y/y.

The private-sector job openings rate held at the record 6.3% in May, revised from 6.4%. It was increased from 4.1% last May. (…)

Employers are continuing to experience trouble finding workers as hiring has lagged job openings. In May, the private sector hiring rate held at 4.6% and was below the level of 4.7% six months earlier. It remained well below the record 7.2% in May of last year. (…)

The layoff & discharge rate in the private sector held steady at the record low of 1.1% in May. (…)

As the labor market firms, workers look for new job opportunities. The 2.8% quits rate in the private sector was down modestly m/m but remained up from 1.8% twelve months earlier. It has been trending higher since the August 2009 low of 1.3%. (…)

ING:

(…) The obvious implication is that if firms can’t expand as planned, the outlook for growth will be weaker.

The general view amongst analysts and the Federal Reserve is that the labour market will be in better balance from September as childcare issues ease as schools return to in person tuition and expanded unemployment benefits cease. The latter should in theory improve the relative financial attractiveness of work and draw people back to employment.

We agree that it should become somewhat easier to find staff, but depending on how long people have been out of work could mean that there might be issues about skill sets – are the workers available what employers actually want? Moreover, evidence suggests there has been a significant increase in the number of people retiring over and above what would be expected from demographics. Some estimates suggest a figure of nearly 2 million more people. Surging equity markets have boosted the value of 401k plans and after not having to commute to work for 16 months the desire to return to the office may not be what it once was. With so many people potentially having permanently left the labour force, this could mean the struggle to find workers could be more persistent.

With companies desperate to recruit and expand to take advantage of the reopening and the stimulus-fuelled growth environment, companies are increasingly taking the decision to pay more to attract staff. This was reflected in a new all-time high for the proportion of companies raising compensation as measured by the NFIB. Today’s report shows the “quit rate” – the proportion of workers quitting their job to move to a new employer actually dipped modestly, but remains high by historical standards.

The US quit rate – proportion of workers quitting their jobs to move to a new employer

Source: Macrobond, ING

This is further bad news for US companies with the implication being that companies not only have to pay more to recruit new staff, but also perhaps raise pay more broadly in order to retain staff. If this is the case then this will be a key story that keeps inflation higher for longer and could be trigger for earlier Federal Reserve interest rate increases.

Other observations:

- The total labor pool (unemployed + not-in-labor-force-but want-job-now + marginally attached, black line above) of 11.3 million people remains 4.1M above its Feb. 2021 level but job openings have jumped by 2.2M to 9.2M. Yet, hires have stalled, suggesting a huge mismatch.

- In both 2005 and 2015, growth in private wages started to really accelerate after the ratio of the labor pool to job openings declined below 2.2. In May, that ratio was 1.2, i.e. there was 1.2 potentially available worker for each job opening. This is a very tight and mismatched labor market.

Fed Officials Saw Earlier End for Bond Buying at Meeting Minutes of the June Federal Reserve meeting show how officials have been surprised by a stronger-than-expected rise in price pressures as the economy reopens.

(…) “Various participants mentioned that they expected the conditions for beginning to reduce the pace of asset purchases to be met somewhat earlier than they had anticipated at previous meetings in light of incoming data,” the minutes said. Others saw recent reports of weaker-than-expected hiring as reason to be patient in assessing their next moves.

The minutes offer a strong sign officials will ramp up more formal deliberations at their next meeting, July 27-28, over when and how to reduce the bond buying. Officials generally judged that, “as a matter of prudent planning, it was important to be well positioned to reduce the pace of asset purchases, if appropriate, in response to unexpected economic developments, including faster-than-anticipated progress” toward the Fed’s inflation and employment goals or risks of too much inflation.

The minutes showed officials still expect recent inflation surges to be temporary, driven primarily by bottlenecks and shortages stemming from the pandemic. But some officials raised concern that consumers’ and businesses’ expectations of future inflation “might rise to inappropriate levels if elevated inflation readings persisted,” the minutes said. Central bankers believe inflation expectations can be self-fulfilling. (…)

The minutes largely reflect similar rifts, with one camp stressing risks of unwelcome inflationary pressures and another warning against drawing firm conclusions given the nature of the recent shocks. (…)

From my reading of the minutes (my emphasis):

First, the FOMC staff review:

- “The pace of increases in several measures of labor compensation had moved up in recent months. Average hourly earnings for all employees jumped at a sizable monthly rate in April and May, even though the large job gains in the leisure and hospitality sector—where wages tend to be lower than in other sectors—likely held down the increases in average hourly earnings in these months. A staff measure of the 12‑month change in the median wage derived from the ADP data had stepped up significantly in April relative to March. The employment cost index of total hourly compensation in the private sector increased at an annual rate of 4 percent in the three months ending in March, a notably faster pace than over the previous three months.”

- “key factors that influence consumer spending—including increasing job gains, the upward trend in real disposable income, high levels of household net worth, and low interest rates—pointed to strong real PCE growth over the rest of the year.”

- “The U.S. economic projection prepared by the staff for the June FOMC meeting was stronger than the April forecast. Real GDP growth was projected to increase substantially this year, with a correspondingly rapid decline in the unemployment rate. (…) with monetary policy assumed to remain highly accommodative, the staff continued to anticipate that real GDP growth would outpace that of potential over most of this period, leading to a decline in the unemployment rate to historically low levels.”

- “The staff’s near-term outlook for inflation was revised up markedly, but the staff continued to expect the rise in inflation this year to be transitory.”

- “The staff continued to see the uncertainty surrounding the economic outlook as elevated, although increasingly widespread vaccinations, along with ongoing policy support, were viewed as helping to diminish some of these uncertainties. Nevertheless, the staff judged that the risks around their strong baseline projection for economic activity were still tilted somewhat to the downside, as adverse alternative courses of the pandemic—including the possibility of the spread of more-contagious, more-vaccine-resistant COVID-19 variants—seemed more likely than outcomes that would be more favorable than in the baseline forecast. The staff continued to view the risks around the inflation projection as roughly balanced.”

Participants’ views:

- “A vast majority of participants revised up their projections for real GDP growth this year compared with the projections they had submitted in March, citing stronger consumer demand and improvements in vaccination rates as the primary reasons for these upgrades. (…) Participants’ projections of real GDP growth in 2022 and 2023 were generally little changed.

- “participants remarked that the actual rise in inflation was larger than anticipated (…). Participants attributed the upside surprise to more widespread supply constraints in product and labor markets than they had anticipated and to a larger-than-expected surge in consumer demand as the economy reopened.”

- “Several participants remarked that they anticipated that supply chain limitations and input shortages would put upward pressure on prices into next year.”

- “participants judged that uncertainty around their economic projections was elevated.”

- “a substantial majority of participants judged that the risks to their inflation projections were tilted to the upside because of concerns that supply disruptions and labor shortages might linger for longer and might have larger or more persistent effects on prices and wages than they currently assumed.”

- Several other participants cautioned that downside risks to inflation remained because temporary price pressures might unwind faster than currently anticipated and because the forces that held down inflation and inflation expectations during the previous economic expansion had not gone away or might reinforce the effect of the unwinding of temporary price pressures.”

- “a few participants mentioned that they expected the economic conditions set out in the Committee’s forward guidance for the federal funds rate to be met somewhat earlier than they had projected in March.”

- “Several participants emphasized, however, that uncertainty around the economic outlook was elevated and that it was too early to draw firm conclusions about the paths of the labor market and inflation. In their view, this heightened uncertainty regarding the evolution of the economy also implied significant uncertainty about the appropriate path of the federal funds rate. Some participants noted that communications about the appropriate path of policy would be a focus of market participants in the current environment and commented that it would be important to emphasize that the Committee’s reaction function or commitment to its monetary policy framework had not changed.”

- “several of these participants emphasized that the Committee should be patient in assessing progress toward its goals and in announcing changes to its plans for asset purchases.”

So, the staff is pretty bullish on the economy thanks to strong consumer expenditures. It expects the unemployment rate to reach historically low levels, it observes that labor compensation is rising at “notably faster” rates and that recent measures of inflation are “markedly” stronger than expected. Yet, the staff considers that economic uncertainty remains elevated and “tilted somewhat to the downside” with “the risks around the inflation projection roughly balanced”.

In other words, things are not going as expected but, no worries, everything will fall in its proper place.

Participants agree on a stronger 2021 but judge that this will have no impact on subsequent years. They also agree that recent inflation surprised on the upside on stronger than expected demand and lingering pressures on input and logistics costs. Most (“a substantial majority”) now “judged that the risks to their inflation projections were tilted to the upside”. Yet, uncertainty remains elevated and it’s better to be patient and prudent in their communications.

In other words, the facts are that everything is stronger than expected, it looks like we’re going to be wrong on growth, wages and inflation, but let’s be patient, the staff could prove right after all, and no spooking the markets.

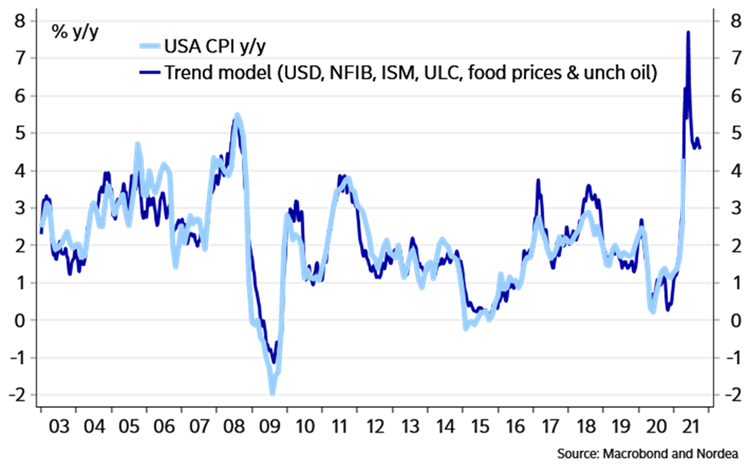

- Alan S. Blinder: Don’t Worry Too Much About the Inflation Surge We may be stuck with inflation above 2%—maybe even above 3%—for a while.

(…) One simple way to assess the importance of special factors is to consult the trimmed mean inflation series maintained by two of the Federal Reserve banks. These measures ignore the prices with the highest and lowest inflation rates and focus on the rest.

It turns out that the Dallas Fed’s trimmed mean PCE inflation rate over the past 12 months is 1.9%, and the Cleveland Fed’s trimmed mean CPI inflation rate is 2.6%. Not very scary. The high-inflation outliers—such as prices for used cars and energy—aren’t illusions, but they won’t persist.

A second inflation worry is that the U.S. economy, powered by pent-up consumer demand and huge government expenditures, will soon soar into the inflationary zone. Could be. But there are three counterarguments.

First, this worry reflects Phillips curve thinking, which hypothesizes that low unemployment rates make the inflation rate rise. But inflation wasn’t rising before the pandemic despite a 3.5% unemployment rate.

Second, the bond market isn’t buying the argument. Inflation forecasts embedded in bond yields remain consistent with the Fed’s low target.

Third, much of the extreme fiscal stimulus that has been driving spending is transitory. Most pandemic relief spending will be ending soon, and I don’t think Congress will approve much more spending this year that isn’t paid for.

The big question is how pent-up consumer demand will play out. American households socked away about $2 trillion in bank accounts as the pandemic raged. If that money gushes out, we’re likely in for some classic demand-side inflation. But if it gets spent gradually, American businesses will meet demand easily.

The third inflation worry is more subtle. Most of the supply-side bottlenecks, such as the shortage of computer chips, are global. Yet inflation is running higher in the U.S. than in other advanced economies. Is this evidence that we’ve used up the slack and are already “running hot”?

Perhaps. But on the other side, there has been a huge drop in labor-force participation in the U.S. since February 2020—1.7 percentage points, which corresponds to 2.7 million potential workers. Much of this drop stemmed from pandemic-related problems like fear of the disease, difficulty in getting child care, and generous unemployment benefits—all of which will dissipate over time, giving the labor force room to grow.

It takes time for a gigantic economy to normalize after a huge shock. The U.S. doesn’t have a 5% inflation problem. But we may be stuck with inflation above 2%—maybe even above 3%—for a while. The Fed’s latest forecast implies that inflation will tumble next year to 2.1%. I wouldn’t bet on that.

- John Authers: The Reflation Trade Has Believers in Frankfurt Just when the market appears to have lost faith, the European Central Bank arrives with a display of commitment to raise inflation.

(…) According to my colleagues who cover the ECB, the bankers agreed “to raise their inflation goal to 2% and allow room to overshoot it when needed.” For the last two decades, the target was “below, but close to, 2%,” which some policy makers felt was too vague. (…)

We are now at a point where all the world’s most powerful central banks, which are charged with maintaining the strength of their currencies, now actually want to raise inflation, and have announced that their ideal rate is higher than it used to be.

This a.m., there is no overshooting:

In a widely expected decision, foreshadowed by policymakers, the ECB set its inflation target at 2% in the medium term, ditching a previous formulation for “below but close to 2%,” which created an impression the euro zone’s central bank worried more about price growth above its target than below it.

Although the ECB said its target would be symmetric, it made no specific reference to tolerating an inflation overshoot after long periods of ultra-low price growth, a possible disappointment for investors who were looking for such a commitment that would ensure stimulus well into the recovery. (…)

“Symmetry means that the Governing Council considers negative and positive deviations from this target as equally undesirable.” (…)

J.P. Morgan Asset Management offers these long-term charts, all suggesting slower growth longer term, unless labor productivity more than doubles. What if central bankers do get the inflation they crave for?

Borrowing Is Back as Sign-Ups for Auto Loans, Credit Cards Hit Records In a sharp reversal from the depths of the pandemic, Americans are more willing to take on debt

Consumer demand for auto loans and leases, general-purpose credit cards and personal loans was up 39% in April compared with the same period last year, according to credit-reporting firm Equifax Inc. EFX 0.95% It was also up 11% compared with April 2019, according to Equifax, which measured how often lenders checked consumers’ credit reports to make loan decisions.

Equifax said lenders extended a record number of auto loans and leases in March, the latest month for which data are available. They also bumped up credit-card originations, issuing more general-purpose credit cards than any other March on record. Equifax’s data goes back to 2010. (…)

Lenders originated some three million auto loans and leases in March, up about 53% from the same month in 2020 and the highest monthly figure on record, according to Equifax. Auto balances for new originations also hit a record of $73.6 billion in March, up 59% from a year prior.

Lenders also issued nearly six million general-purpose credit cards in March, up 32% from a year earlier and the highest March figure on record. (…)

At JPMorgan Chase & Co., customer spending on credit cards increased about 17% in May from the same month in 2019. Gordon Smith, the bank’s co-president, said at a June conference that he expected the trend to continue throughout the year. (…)

Some lenders are also extending more credit to people with low credit scores. Some 1.4 million general-purpose credit cards were given to subprime borrowers in March, up 28% from last year and 25% from 2019.

Roughly 602,000 subprime auto loans and leases were originated in March, up 31% from a year before. Balances on those auto loans and leases totaled $11.7 billion, the highest on record.

China Pivots on Central Bank Easing as Fed Heads for Taper

China made a surprise shift Wednesday by signaling the economy needs additional central bank support, a warning for the rest of the world about how circuitous the exit route from the Covid-19 pandemic is proving to be.

The State Council, China’s equivalent of a cabinet, hinted the People’s Bank of China could make more liquidity available to banks to boost lending. It’s a move that puts the PBOC at odds with the U.S. Federal Reserve’s discussions around tapering its bond-buying program, suggesting that monetary policy in the world’s two biggest economies could be headed in opposite directions again. (…)

The State Council suggested the PBOC could cut the amount of money banks must keep in reserve — the so-called reserve ratio requirement, or RRR. While the shift in tone doesn’t mean the restart of broad-based easing in China, it’s an about-turn for a central bank that had been tapering its support as growth accelerated. (…)

The State Council’s shift may indicate the government expects disappointing data when it reports second-quarter gross domestic product and June activity figures next week. Economists surveyed by Bloomberg expect a slowdown in GDP growth to 8% in the second quarter from a year earlier, compared to 18.3% in the previous three months. (…)

Detailing its shift, the State Council agreed at a meeting chaired by Premier Li Keqiang to “use monetary policy tools, including a cut to the reserve requirement ratio at an appropriate timing to enhance financial support to the real economy, particularly to smaller businesses,” according to a statement Wednesday. That’s aimed at helping firms deal with the impact of rising commodity prices, it said.

(…) the mention of RRR cuts after more than a year was “notable and probably increases the chance of an actual implementation of the cut,” Goldman Sachs Group Inc. wrote in a note. The State Council’s statement had a clear “pro-growth” shift, focusing on the need to increase financial support to the real economy, the economists said. (…)

Possible impact from ING:

There are a number of impacts from a possible targeted RRR cut:

- Weaker CNY against USD as the targeted RRR cut is in contrast to Fed talk of taper and rate hike timing. This could be reflected in today’s market moves.

- This policy could be temporary when announced and possibly reported together with a timeframe or conditions.

- SMEs in China should be able to get more loans from banks at lower interest rates after the targeted RRR cut is announced. But banks’ credit policy for SMEs is not expected to be relaxed.

- Some SMEs might be less willing to go for micro-loans offered by fintech platforms, which were the usual channel SMEs got financing from due to their more relaxed credit policy compared to banks for SMEs even though they charge higher interest rates.

- A cut of targeted RRR for SMEs only lowers the cost to banks if they lend to SMEs. That means not all SMEs can get loans from banks even if there is a targeted RRR cut. Some SMEs would continue to operate in difficult conditions.

- Overall, SMEs survival rate could increase moderately, and this could help stabilise jobs and economic growth.

U.S. banks to see big jump in 2Q profits before results return to normal

Among them, Bank of America Corp (BAC.N), Citigroup Inc (C.N) and JPMorgan Chase & Co (JPM.N), the country’s three largest banks, will more than double their second-quarter profits, according to analyst estimates compiled by Refinitiv. (…)

Together, Bank of America, Citigroup, JPMorgan and Wells Fargo are expected to report $24 billion in second-quarter profits compared with $6 billion last year, the analyst estimates show. (…)

HISTORY RHIMES