U.S. Data Point to Stronger Economy Confident consumers and a stabilizing factory sector put the wind at the U.S. economy’s back as it entered the second half of the year.

(…) Sales at retail stores and restaurants rose 0.6% in June from the prior month to a seasonally adjusted $456.98 billion, the Commerce Department said Friday. Sales had climbed 0.2% in May, revised down from an earlier estimate of 0.5% growth. (…)

Excluding autos, retail sales last month rose 0.7% from May. Excluding both autos and gasoline, sales also climbed 0.7%. (…) Total retail sales rose 2.7% in June from a year earlier, up from annual growth of 2.2% in May. (…)

In the second quarter, total retail sales were up 1.4% compared with the first quarter—providing a tailwind for the overall U.S. economy. (…)

Most retail categories saw sales grow last month, led by a 3.9% jump in sales at building-supply stores. That was the largest one-month increase in the sector since April 2010 and followed a 2.5% drop the prior month and a 1.6% decline in April. (…)

Sales of motor vehicles and automotive parts were up 0.1% last month after falling 0.5% in May. (…) Sales at restaurants and bars were down 0.3% from May and clothing-store sales fell 1.0% in June. More broadly, restaurant sales were up 1% in the second quarter compared with the first three months of 2016. (…)

In the first six months of 2016, overall U.S. retail and food services sales were up 3.1% compared with a year earlier. The data weren’t adjusted for price changes, but sales growth comfortably exceeded the recent rate of inflation.

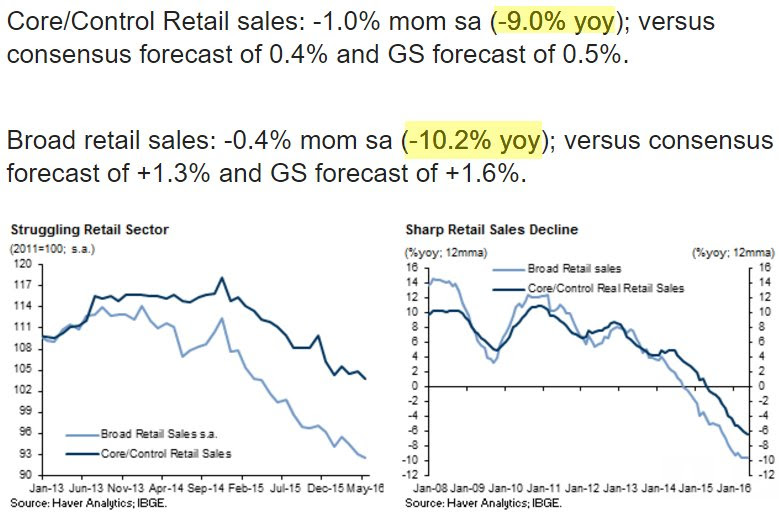

Sales in the retail control group, which excludes gasoline, building supplies and food services, rose 0.5% (4.1% YoY) and is up a huge 8.7% annualized in the last 3 months as this Haver Analytics chart shows. This figure is used in the computation of the GDP.

Hopefully, this will help that:

There is a bit of a mystery with these retail sales data. The huge +8.7% annualized growth rate in control sales during the last 3 months has received little echo from retailers and consumer surveys. As well, the most recent Beige Book contained no mention of a retail resurgence.

For example, the 9 S&P 500 Consumer Discretionary companies that have reported Q2 so far showed revenues up 3.3% YoY. Only 22% beat on revenues with a revenue surprise factor of –0.3%. The 7 Staples companies that have reported showed revenues up 0.6%, a 29% beat rate and a –0.5% revenue surprise factor.

Evercore ISI Retailers Sales Surveys did bounce back from the very weak spring but shows no meaningful upturn so far this year and is down 3.9% YoY.

Recall that April has been the big bounce month in total retail sales, +1.2% MoM after very slow sales early in the year. May was originally reported up 0.5% but that has been revised down to +0.2%. We shall see what will happen to June’s +0.6% initial release.

Consumer Prices Begin to Percolate

The consumer-price index, which measures what Americans pay for everything from shelter to sweets, increased a seasonally adjusted 0.2% in June from the prior month, the Labor Department said Friday. It had climbed 0.2% in May and 0.4% in April.

Excluding the often-volatile categories of food and energy, consumer prices also rose 0.2% in June. (…) Prices excluding food and energy climbed 2.3% from a year earlier, matching the highest level since May 2012.

While energy prices remain well below their levels from last June, costs for shelter, medical care, transportation services and clothing all have risen sharply. Shelter costs, which account for about one-third of CPI, are up 3.5% from a year earlier, the strongest rise since September 2007. (…)

In a separate report on Friday, the Labor Department said inflation-adjusted average weekly earnings fell 0.1% in June from the prior month. Average hourly earnings climbed 0.1% while prices climbed 0.2% and the average workweek was unchanged.

Good thing food-flation and goods-flation are declining fast because the consumer is getting squeezed just about everywhere else, primarily from Services (charts from Haver Analytics). The Cleveland Fed data shows core inflation rising at a sustained 2.4% rate this year:

Industrial Production Up 0.6% in June

Industrial production, a measure of everything made by factories, mines and utilities, rose a seasonally adjusted 0.6% in June, the Federal Reserve said Friday. Economists surveyed by The Wall Street Journal had forecast a 0.4% rise.

The last time it jumped at that rate was nearly a year ago, in July 2015, and the last time it increased by more was November 2014. (…)

June saw a rise in motor vehicle and parts production, a volatile category that had dipped in May. Mining, which includes energy production, registered a small increase for the second straight month, welcome news for the beleaguered sector.

The headline index was in part lifted by a 2.4% monthly rise in utilities output, as June’s warmer-than-usual weather had Americans turning up the air conditioning. (…)

Overall manufacturing output rose 0.4% in June, led by a jump in the production of motor vehicles and parts. However, other non-auto output was unchanged from May. (…)

Capacity use, a measure of how much industries are making as a share of potential output, rose 0.5-percentage point to 75.4%. The rate is 4.6 percentage points below the historical average, suggesting there is still room for the economy to ramp up, should firms feel more confidence in future demand.

Overall industrial production was down 0.7% in the 12 months through June. Manufacturing output is 0.4% above its June year-ago level, but on a quarterly basis has fallen 1% in the second quarter from the same period a year ago. Utility output is up 0.5%. Mining output is still on the path to recovery, down 10.5% from June 2015. (…)

Empire State Factory Sector Activity Index Deteriorates

The Empire State Factory Index of General Business Conditions declined during July to 0.55 and reversed much of its June improvement. Expectations had been for 5.0 in the Action Economics Forecast Survey. The data are reported by the Federal Reserve Bank of New York and reflect business conditions in New York, northern New Jersey and southern Connecticut.

Based on these figures, Haver Analytics calculates a seasonally adjusted index that is comparable to the ISM series. The adjusted figure declined to 48.9 from 50.3. Since inception in 2001, the business conditions index has had a 64% correlation with the change in real GDP.

A weaker new orders reading accounted for much of the decline in the overall index as it fell to -1.82 from 10.90. (…) employment moved lower to -4.40 from 0.00. During the last ten years there has been a 68% correlation between the index level and the m/m change in factory sector payrolls.

Major cities drive China property price gains

Property prices in large Chinese cities grew in more locations last month compared to a year earlier, with prices in higher-tier cities again leading the charge upwards – but fewer saw month-on-month prices rise compared to May.

Annualised prices for new residential homes rose in 57 out of 70 cities surveyed and fell in 12, while in monthly terms prices rose in 55 cities and fell in 10, according to data from the National Bureau of Statistics on property prices across large and mid-sized cities.

The same ten first- and second-tier cities led gains over the previous year, with Shenzhen far ahead of the pack thanks to year-on-year growth of 46 per cent. However, other first-tier cities like Shanghai (up 27.7) and Beijing (up 20.3) were pushed to fifth and sixth place, respectively by the second-tier likes of Xiamen, Nanjing and Hefei (up 33.6, 29.7 and 29, respectively).

Overall prices of new residential buildings rose 7.3 per cent year-on-year in June, according to Reuters calculations based on the official data, the highest since April 2014.

But the statistics bureau noted that annualised price growth had softened from previous months in an explanatory note published alongside the new data, indicating overall prices were up only 0.5 percentage points year-on-year by its own reckoning, compared to 1.2 percentage points the month prior.

Gains in monthly terms were notably less impressive, as five fewer cities saw prices grow in June, while six more saw them fall.

Yuan Weakens Past 6.7 Versus Dollar for First Time in Five Years

(…) China’s policy makers are trying to balance the need for a weaker yuan to help exports with efforts to avoid igniting depreciation pressures that would lead to surging capital outflows. Overseas shipments declined for the third month in a row in June, even as the yuan dropped 2.2 percent against an index of trading peers. (…)

Oil Producers Prepare for Second-Half Slump

After surviving two years of low prices, they’re gearing up for a third by buying protection against a renewed downturn. Laredo Petroleum Inc. said July 14 that it hedged more than 2 million barrels of 2017 output earlier this month. Drillers have increased bets on falling prices by 29 percent this year. (…)

“The producers have sold the hell out of this rally,” said Stephen Schork, president of Schork Group Inc., a consulting firm in Villanova, Pennsylvania. “The companies that did survive, they’ve been hedging into this rally. And they’re counting their blessings.” (…)

Producers increased bets on falling prices for a third consecutive week in the seven days ended July 12, according to data from the Commodity Futures Trading Commission. Short wagers rose by 8,566 futures and options combined, or 1.6 percent.

Drillers are also taking advantage of the rally to tap the capital markets. U.S. oil and gas producers have been selling shares at record speed, using the cash to repay debt or buy oil and gas prospects, bolstering the asset side of the balance sheet. So far this year, companies have raised more than $16 billion in equity, according to data compiled by Bloomberg. (…)

Gasoline inventories are so swollen that at least five sea tankers hauling the fuel to New York were turned away over the past few weeks, according to traders and ship-tracking data compiled by Bloomberg. U.S gasoline stockpiles rose 0.5 percent to 240.1 million barrels, an all-time seasonal high, in the week ended July 8, the Energy Information Administration reported last week.

The peak-driving season in the U.S. has so far failed to erode those stockpiles, which may send crude tumbling below $40 a barrel again, according to Schork.

“Demand is strong, but supply is even stronger,” he said. (…)

EARNINGS WATCH

Facset’s weekly summary:

Overall, 7% of the companies in the S&P 500 have reported earnings to date for the second quarter. Of these companies, 66% have reported actual EPS above the mean EPS estimate, 14% have reported actual EPS equal to the mean EPS estimate, and 20% have reported actual EPS below the mean EPS estimate. The percentage of companies reporting EPS above the mean EPS estimate is below both the 1-year (70%) average and the 5-year (67%) average.

In aggregate, companies are reporting earnings that are 3.9% above expectations. This surprise percentage is below both the 1-year (+4.2%) average and the 5-year (+4.2%) average.

If the Energy sector is excluded, the estimated earnings decline for the S&P 500 would improve to -2.0% from -5.5%.

In terms of revenues, 51% of companies have reported actual sales above estimated sales and 49% have reported actual sales below estimated sales. The percentage of companies reporting sales above estimates is above the 1- year average (49%) but below the 5-year average (55%).

In aggregate, companies are reporting sales that are 0.4% above expectations. This surprise percentage is above the 1-year (0.0%) average but below the 5-year (+0.6%) average.

If the Energy sector is excluded, the estimated revenue decline for the S&P 500 would improve to 2.3% from -0.6%.

The blended earnings decline for the second quarter is -5.5% this week, which is slightly smaller than the blended earnings decline of -5.9% last week. Upside earnings surprises reported by companies in the Financials sector were mainly responsible for the small decrease in the overall earnings decline for the index during the past week.

In the Financials sector, the upside earnings surprises reported by JPMorgan Chase ($1.55 vs. $1.42) and Citigroup ($1.24 vs. $1.10) were the largest contributors to the small decrease in the overall earnings decline for the index during the past week. As a result, the blended earnings decline for the Financials sector decreased to -4.6% from -5.8% during this period.

Five sectors have recorded a decrease in earnings growth since the end of the quarter due to downside earnings surprises and downward revisions to earnings estimates, led by the Utilities (to 2.6% from 3.5%) sector. Four sectors have recorded an increase in earnings growth during this time due to upward revisions to estimates and upside earnings surprises, led by the Materials (to -11.6% from -12.5%) sector. The Health Care sector (2.2%) has the same earnings growth rate today as it did on June 30.

RBC Capital’s tally is a little more up-to-date with Friday’s data:

- Thirty-six companies (9.9% of the S&P 500’s market cap) have reported. Earnings are beating by 3.8% while revenues are surprising by 0.4%.

- Expectations are for declines in revenue, earnings, and EPS of -1.3%, -6.4%, and -4.0%, respectively.

- EPS is on pace for -0.6%, assuming the current beat rate for the remainder of the season. This would be +3.8% excluding Energy and the Big-5 Banks.

The recent better economic data have been well received by investors as these Yaredeni Research charts illustrate:

The Bulls population has jumped materially as a result, not really because the bears have disappeared but rather because the correction camp has declined…

…Investment managers have pushed their clients (equity accounts) to be nearly fully allocated to stocks (via The Daily Shot)…

…just as the conditions for a correction are rising.

Transportation stocks have followed the crowd but keep lagging.

Q2 EPS estimates have not stabilized yet:

If Q2 EPS meet the current consensus, trailing EPS will drop a little more to the $114 range from $117.46 at the end of 2015 (per Thomson Reuters).

Meanwhile, core CPI is quietly climbing its way into the 2.0-2.5% range from 1.6% in December 2014 to 2.1% in December 2015 to 2.3% in June. Unless oil prices drop much from here, oil deflation will be behind us by the autumn months and total CPI will ramp up from its current 1.0% towards core CPI.

The S&P 500 Index is now trading at 18.9 times trailing EPS:

And 21,2 on the Rule of 20 P/E which accounts for inflation. The heat is rising. We either need better earnings and/or slower inflation, soon!

SENTIMENT WATCH

What Next for Stocks? Financial Pros Weigh In Before jumping in or cashing out of a U.S. stock market that is in record territory, investors would do well to consider whether the best of the bull market is in the past or whether there is room to run. There are cases to be made on both sides, financial advisers and fund managers say.

On one hand, stocks are richly valued by some metrics such as price-to-sales ratios. On the other, market professionals are generally cautiously optimistic that the U.S. bull market, not having shown the signs typically associated with a peak and retreat, is primed for an extended run. (…)

“Markets aren’t cheap right now; that is a fact,” Mr. Hickey said. “That being said, bull markets don’t end when markets are cheap. They usually end when markets are excessive, and in many cases, they’ve been more excessive than they are now.”

How far can this bull market go?

(…) Today’s never-say-die bull market — now the second-longest at seven years and counting — has longevity genes, too. (…)

This bull, despite expensive stocks, slowing global growth, a wobbly Chinese economy, less profitable U.S. companies and fallout from Britain’s vote to exit the European Union, continues to defy skeptics.

“I can’t say that it will, but I will say that it could,” Scott Wren, senior global equity strategist at Wells Fargo Investment Institute, said of the current bull’s chance to outlast the nearly 10-year run from Oct. 11, 1990 to March 24, 2000. (…)

But this bull, despite the naysayers, could continue to exceed expectations.

“It has a chance if it doesn’t become over-loved,” said Ann Miletti, lead portfolio manager at Wells Capital Management. She gives the current bull a “better than 60% chance” of one day becoming the longest bull ever. “It has been a slow growth market for a long time and a bumpy ride along the way. But that has also meant that expectations have remained tempered and valuations have been kept in check, which is a good setup for longevity.” (…)

The run could go another eight to 13 years, said Brian Belski, chief investment strategist at BMO Capital Markets. (…)