China Manufacturing PMI hits highest level for a decade in November

Chinese manufacturers signalled the strongest improvement in operating conditions for a decade in November, as growth of both output and new orders accelerated to 10-year highs. The sustained and strong upturn in client demand led to the fastest increase in employment since May 2011. At the same time, firms raised their purchasing activity at the steepest rate since January 2011 and increased their inventories of both pre- and post-production goods. Greater market demand contributed to stronger inflationary pressures, however, with both input costs and output charges rising at sharper rates.

The headline seasonally adjusted Purchasing Managers’ Index ™ (PMI ™ ) increased from 53.6 in October to 54.9 in November, to signal the sharpest improvement in conditions since November 2010. The health of the sector has now improved in each of the past seven months, to indicate a sustained and strong recovery from the coronavirus disease 2019 (COVID-19) outbreak earlier in the year.

Manufacturing companies in China recorded a sharp and accelerated rise in production during November, with the rate of expansion the quickest for 10 years. Firms frequently attributed the increase to greater new order volumes, as well as a further recovery from the COVID-19 related disruptions seen earlier in the year.

Overall sales likewise expanded at the quickest rate for a decade, which was often linked to a rebound in client demand. Underlying data suggested that the upturn continued to be led by firmer domestic demand, as growth in new export work was not as marked as that seen for total new orders.

Overseas demand improved substantially as the measure for

new export orders stayed in expansionary territory for the fourth

month in a row, rising from the previous month. As production overseas was subdued by uncertainties brought by the pandemic, Chinese enterprises saw an increase in export orders. But the improvement in overseas orders was slightly weaker than that of domestic demand.Increased production requirements and higher inflows of new work led companies to expand their workforce numbers again in November. Though modest, the rate of job creation was the strongest seen since May 2011. Capacity pressures persisted, however, as highlighted by a further rise in outstanding business. Furthermore, the rate of backlog accumulation was the quickest since April.

November data also revealed a substantial increase in purchasing activity, with the rate of growth the steepest since the start of 2011. However, the time taken to receive purchased inputs continued to lengthen amid reports of stock shortages at suppliers.

On the inventories front, stocks of purchases rose further in November, and at the fastest rate since February 2010. Inventories of post-production items meanwhile increased at a rate that, though marginal, was the quickest for 33 months. Panel members often attributed stock building efforts to improved sales and stronger overall market conditions.

Greater demand for inputs placed upward pressure on costs in November. Input prices rose sharply overall, with a number of monitored firms commenting on increased raw material costs, with metals mentioned in particular. Companies raised their selling prices at a quicker pace as a result, though the rate of increase remained below that seen for operating expenses.

Business confidence regarding the 12-month outlook for output remained strongly positive in November, despite easing slightly since October. Optimism was linked to planned company expansions, supportive state policies and hopes that global conditions

Eurozone Manufacturing growth remains strong in November

The seasonally adjusted IHS Markit Eurozone Manufacturing PMI® fell slightly during November but remained at a level indicative of strong growth. Although the headline index slipped to 53.8, from 54.8 in October, it was slightly better than the earlier flash reading and signalled an improvement in manufacturing operating conditions for the fifth successive month. Moreover, growth remained well above the long-run survey average.

There was some notable divergence in performance across the broad market groups data during November. On the one hand, the capital and intermediate goods sectors continued to expand at marked monthly rates. However, in contrast, consumer goods producers registered a modest deterioration in operating conditions for the first time in six months.

Except for the Netherlands and Ireland, all countries recorded a weakening of their respective PMIs during the latest survey period. Germany remained the best-performing country, followed by the Netherlands and Ireland.

Solid growth was seen in Austria and Italy, in contrast to marginal contractions recorded in both Spain and France. Greece remained by far the worst-performing in November, contracting at a steep and accelerated rate.

For the fifth successive month an increase in manufacturing production was recorded, although growth eased on October’s two-and-a-half year peak and was the slowest since July. A similar trend was seen for new orders, where growth eased to the weakest in the current five-month sequence amid a slowdown in gains across domestic and external markets.

Indeed, new export orders rose at the slowest pace since August, though growth remained solid. Germany, the Netherlands and Austria recorded the strongest gains in export trade during November.

Some pressure on capacity was signalled by a fourth successive monthly increase in backlogs of work, which continued to rise at a solid pace. Firms instead focused on productivity gains by lowering their staffing levels for a nineteenth successive month. Job losses were most prevalent in Greece, Germany and Austria.

Increased production and order requirements meant that firms continued to increase their purchasing activity, with growth amongst the best seen in the past two-and-a-half years. This served to further add pressure on suppliers, with average lead times for the delivery of inputs deteriorating to the greatest extent for seven months.

Inventories of raw materials and semi-manufactured goods were subsequently utilised wherever possible to ensure production lines could be sustained. Stocks of purchases fell markedly and for a twenty-second successive month in succession. Warehouse inventories were also depleted sharply, with latest data showing the greatest monthly fall since the end of 2009.

On the price front, input cost inflation accelerated to the sharpest recorded by the survey for nearly two years. All countries recorded stronger rises in input prices compared to the previous month.

Efforts to protect margins led to a second successive monthly rise in output prices, with the rate of inflation modest but nonetheless the strongest for a year-and-a-half.

Finally, looking ahead to the coming 12 months, business confidence improved to its highest for over two-and-a-half years. Dutch, Italian and German companies were the most confident manufacturers in November.

Japan Manufacturing PMI reaches highest level since August 2019

The Japanese manufacturing sector moved closer towards stabilisation in November, according to latest PMI® data. The higher headline PMI reading was supported by softer falls in output and new orders, which both declined at only mild rates. Despite the coronavirus disease 2019 (COVID-19) pandemic continuing to disrupt business operations and demand conditions, Japanese manufacturers remained optimistic that production will rise over the coming 12 months.

The headline au Jibun Bank Japan Manufacturing Purchasing Managers’ Index™ (PMI) rose slightly from 48.7 in October to 49.0 in November. The latest reading was the highest since August 2019, and signalled only a marginal deterioration in overall conditions, as the sector continued to take tentative steps towards more stable operating conditions.

The slight improvement in the headline index was supported by softer contractions in production and new orders. Output declined at the slowest pace since November 2019 and only modestly overall. Nonetheless, manufacturing firms continued to cite weak client demand as a result of the pandemic as the main factor weighing on production.

Similarly, new orders fell to the least marked extent since May 2019. Lower sales were often attributed to difficult trading conditions as a result of a surge in COVID-19 infections, which had dampened business and client confidence in both domestic and overseas markets. New export sales meanwhile declined after a slight increase in October, as key external markets including Europe imposed more restrictions to halt the spread of the virus.

At the same time, employment levels continued to decrease in November, although at a slightly softer pace compared to October. Firms often cited a lack of demand due to the pandemic as the main driver of job shedding, as well as the non-replacement of voluntary leavers. In line with a lack of new orders, outstanding business fell further in November. While strong overall, the pace of decline was the softest for ten months.

Japanese manufacturers signalled a rise in operating expenses for the sixth consecutive month in the latest survey period. However, the rate of input cost inflation slowed from October and was modest overall. Meanwhile, increased price competition due to the pandemic led to a renewed drop in prices charged in November, following an increase in the previous period.

Amid further falls in new orders and output, buying activity declined again in November, extending the current sequence of decline to 23 months. Manufacturing firms also noted difficulties in sourcing raw materials due to the pandemic, which led to a further deterioration in suppliers’ delivery times. As demand remained depressed, Japanese manufacturing firms indicated that stocks of both pre-production inventories and finished goods were depleted again.

Looking forward, business confidence regarding output over the year ahead remained positive, with expectations underpinned by hopes of an end to the pandemic and a recovery in both domestic and external demand.

(…) Currently, IHS Markit expects industrial production to grow 7.3% in 2021 although this is from a lower base and does not fully recover the output lost to the pandemic.

Virus vaccines offer hope for global economic recovery, OECD says Warning that rebound from pandemic’s economic damage will be patchy and fragmented

Cutting its 2021 global growth forecast to 4.2% from 5% in September, the Paris-based organization said a pattern of outbreaks and lockdowns is likely to continue for some time with rising risks of permanent damage.

There were particularly large downgrades for the euro area and the U.K., with the forecast for the latter slashed to 4.2% from 7.6%. The U.S. projection was lowered to 3.2% from 4%. (…)

Governments should continue to support their economies beyond the end of lockdown measures and avoid “fiscal cliffs,” according to the report. While public debt has soared, the OECD played down concerns, saying that borrowing costs are low.

It did, however, say some spending has been wasted, noting an “absence of correlation between the extent of fiscal aid and the resulting economic performance.” (…)

-

Germany frets about its coronavirus debt mountain Many on right seek return to fiscal rectitude, while left worries about spending cuts

-

Fed chair calls the economic recovery ‘extraordinarily uncertain’

(…) “As we have emphasized throughout the pandemic, the outlook for the economy is extraordinarily uncertain and will depend, in large part, on the success of efforts to keep the virus in check.” Powell said in prepared remarks for his testimony on Tuesday to the US Senate Committee on Banking, Housing, and Urban Affairs. “The rise in new Covid-19 cases, both here and abroad, is concerning and could prove challenging for the next few months. A full economic recovery is unlikely until people are confident that it is safe to re-engage in a broad range of activities.” (…)

Cities Dealt a Blow as Return to Office Fades U.S. employees started heading back to the office in greater numbers after Labor Day but that pace is stalling now, delivering another blow to economic-recovery hopes in many cities.

(…) About a quarter of employees had returned to work as of Nov. 18, according to Kastle Systems, a security firm that monitors access-card swipes in more than 2,500 office buildings in 10 of the largest U.S. cities.

That rate is up sharply from an April low of less than 15%, which largely consisted of building-maintenance and essential workers. The office return rate climbed steadily during the summer and early fall, but it has flattened out after reaching a high point of 27% in mid-October, Kastle said. The rate for last week was down even more sharply than in previous weeks but likely reflected the Thanksgiving Day holiday. (…)

Metro public-transportation systems in cities such as New York, San Francisco, Boston and Washington, D.C., have lost billions of dollars in revenue from months of employees favoring remote work. (…)

Office holdings have long been a cornerstone investment for major real-estate funds for their steady and reliable income. But values are falling sharply as a growing number of tenants dump sublease space on the market or demand lower rents from their landlords when their leases expire. (…)

As of the beginning of November, 2.3% of office mortgages that were converted into mortgage-backed securities were more than 30 days delinquent, up from 1.7% in February, according to data firm Trepp LLC. (…)

Home prices in cottage country jump 15 to 40 per cent across Canada amid COVID-19

Return of the Obama Economists Biden’s policy advisers were in charge during the secular stagnation years.

The WSJ Editorial Board:

(…) They’re Obama veterans who believe in more spending, more regulation, higher taxes, and easier money. Let’s hope the result is better than what became known as “secular stagnation” during the Obama years. (…)

As Federal Reserve Chair in Mr. Obama’s second term, [Janet Yellen] was slow to raise interest rates and reduce the Fed’s bond purchases. She’ll likely favor a 2009-style policy mix next year with a spending blowout while urging the Fed to monetize it.

Mr. Biden has also signed up Jared Bernstein, an architect of the Obama stimulus who famously predicted in January 2009 that spending would keep unemployment below 8% and hit 7% by autumn of 2010. Not quite. The jobless rate hit 10% in October 2009, stayed at 9.9% through April 2010, and didn’t fall below 7% until November 2013. Mr. Bernstein put his trust in the Keynesian “multiplier” that $1 of new spending yields as much as an extra $1.57 or more of additional GDP. Wrong again. (…)

The overall message of Mr. Biden’s picks is of a progressive team that views government as the leading engine of economic growth. Our guess is that they’ll use the lingering damage from the pandemic to propose a major spending and tax increase in early 2021. (…)

Eurozone inflation remains negative ahead of ECB meeting Inflation in the eurozone remains stable at -0.3% in November. Core inflation: 0.2%. But with inflation this low for quite some time and not much improvement expected ahead, the ECB will certainly take action next week

China state-owned group caught in default storm owes banks billions Revelation that Huachen borrowed $5.1bn could prompt concerns over credit system

The FT viewed a creditor document that revealed that “almost 70 Chinese and foreign banks, as well as trust companies, had Rmb33.5bn ($5.1bn) in outstanding lending to Huachen Automotive Group as of last year.” The FT says that the longstanding belief among investors that local governments in China will always bail out troubled state-backed groups has been shattered, prompting fears about the health of the broader financial system.

OPEC Defers Decision on Output Curbs Cartel to meet Thursday with Russia and its other oil producers to agree on a plan

(…) A key hurdle to a pact remains how to deal with past noncompliance by some countries. Saudi Arabia, the U.A.E. and others in OPEC insist that overproducers, including Russia, Iraq and Nigeria, cut their output more in the first quarter, to make up the difference, delegates said.

Russia pumped 430,000 more barrels a day than agreed in the five months ended Sept. 30, according to an internal OPEC assessment. Moscow doesn’t see any need to cut its output deeper and would even favor a slight increase, people familiar with the discussions said. (…)

Exxon Slashes Spending, Writes Down Assets The struggling oil giant is retreating from a plan to increase spending to boost its oil and gas production by 2025 and preparing to slash the book value of its assets by up to $20 billion.

SENTIMENT WATCH

From Axios:

- JPMorgan strategists earlier this month said they expect the S&P to reach 4,000 by early next year and raised their 2021 year-end price target to 4,500 — about 878 points, or 24%, above where it closed on Monday.

- Analysts at Goldman Sachs raised their year-end 2021 target to 4,300 and to 4,600 by the end of 2022.

- “During most of the bull market since 2009, our projections for the S&P 500 were either the most bullish or among the most bullish of Wall Street’s investment strategists. Now others are getting ahead of us,” longtime market bull Ed Yardeni wrote in a recent note to clients. “We’ll let them have the glory. We would like to see fewer bulls.”

- Bank of America on Friday doubled down on its call for a 2021 that could disappoint the market’s freshly minted super bulls, noting that its fund manager survey’s “cash rule” was closing in on a sell signal.

- Further, the bank’s contrarian Bull & Bear indicator showed increasingly thirsty stock traders and its “breadth rule,” which tracks whether global equity markets are overbought or oversold, signaled a sell call on Nov. 11.

- They expect 2021 to be “a year of vaccine not virus, a year of reopening not lockdown, a year of recovery not recession … a year of asset market rotation not asset market rally.”

(CNN)

(CNN) (Societe Generale)

(Societe Generale)

The switch:

")

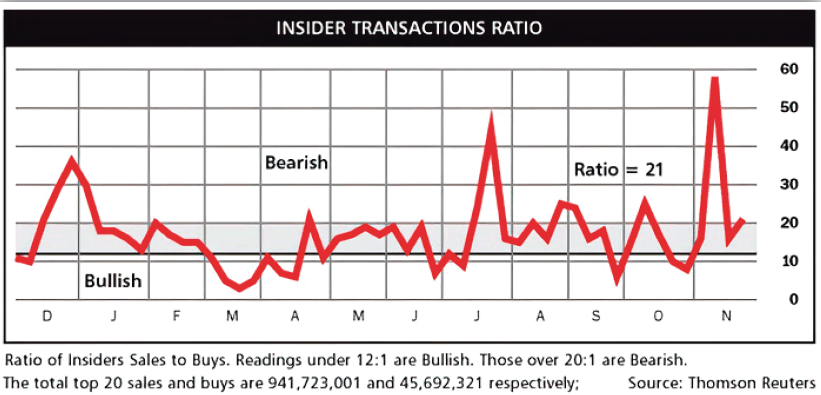

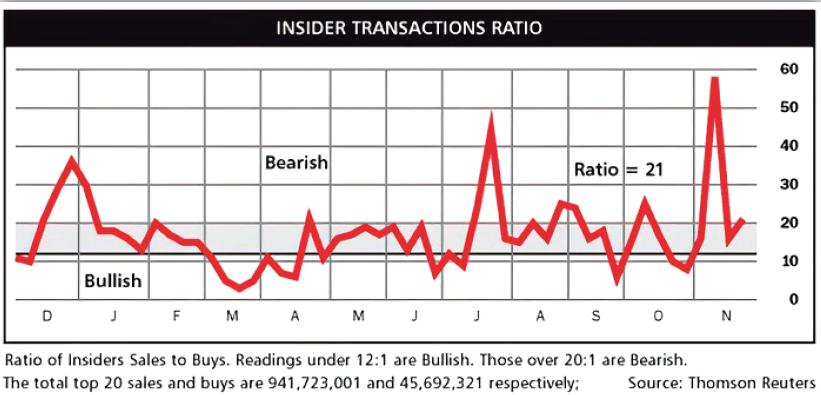

Among sectors tracked by INK, recent insider selling seemed particularly stronger in Energy, Consumer Staples, Financials, Telecom Services and Utes.

DoorDash Sets IPO Terms Pushing Valuation as High as $32 Billion DoorDash said it plans to sell 33 million shares in an initial public offering that could give the food-delivery company a valuation of as much as $32 billion.

The San Francisco company said it expects an offering price of between $75 and $85 a share, adding that a pricing at the $80 midpoint of that range would yield net proceeds of about $2.54 billion. (…)

Airbnb Inc. is expected to target a range of around $30 billion to $33 billion, using a fully diluted share count, when the home-rental startup kicks off its investor roadshow Tuesday, the Journal reported, citing people familiar with the matter.

Almost Daily Grant informs us that DASH’s $32B valuation would be double its valuation at its June private fundraising. And, if you care:

Sales through the first nine months of the year registered at $1.9 billion, more than treble the top line over the same period last year, while net losses narrowed to $149 million compared to $533 million over the first three quarters of 2019. Nevertheless, persistent red ink appears endemic to the food delivery business, as peer Uber Eats reported adjusted Ebitda of negative $183 million in the third quarter, despite seeing revenues more than double to $1.5 billion.

A tripling in sales was not quite enough to bring black ink to the bottom line…ADG adds this gossip:

For DoorDash, the revelation of extra-legal shenanigans clouds those efforts to push into the black. Last week, the company paid $2.5 million to settle a lawsuit from Washington D.C. Attorney General Karl Racine alleging that DoorDash helped itself to millions of dollars in driver tips. In addition to that restitution, the company agreed “to maintain a payment model that ensures all tips go to workers without lowering their base pay, and it will be required to provide clear and easy-to-access information about its policies and payment model to workers and consumers.”

The timing of the settlement is ironic. Founder and chief executive Tony Xu, who owns some 42% of all super voting class B shares, wrote in a founder’s letter accompanying the filing that “fighting for the underdog is part of who I am and what we stand for as a company.”

Tesla to Enter S&P 500 at Full Weight in December The electric-vehicle maker will be added to the broad stock-market gauge before the start of trading Dec. 21, meaning most index-tracking funds that follow the S&P 500 will engage in a flurry of trading the Friday before.

(…) Tesla’s market value has ballooned to about $538 billion, making it the sixth largest company in the U.S. stock market and it would have more than a 1% weighting in the S&P 500. (…) More than $100 billion will be put into motion in coming weeks as passive fund managers and some actively traded mutual funds all benchmarked to the S&P 500 adjust their portfolios to make room for it, traders and fund managers say. (…)

S&P still hasn’t announced what stock Tesla will be replacing, saying it will release that decision after the market closes Dec. 11. (…)

The stock has jumped 39% since its inclusion was announced on Nov. 16 and there has been a frenzy of options trading tied to the shares jumping higher. (…)

State Street’s Mr. Bartolini said at least five of its exchange-traded funds will have to be rebalanced as a result of Tesla’s addition, including the biggest ETF in the world, the SPDR S&P 500 Trust ETF, and its growth-focused ETF, the SPDR Portfolio S&P 500 Growth ETF. (…)

France defies U.S. and starts levying digital tax on tech giants. But will this change with a Biden presidency?

(…) The French tax has been set at 3% of revenue derived from online advertising, the sale of personal data to third parties, and marketplace activities. It is levied on companies with revenue from these activities of more than €750 million globally and €25 million in France.

France isn’t the only European Union country intent on a digital tax. The U.K. has put a national version into law. The U.K. French, Spanish and Italian finance ministers signed a joint letter in August demanding that technology giants, like Google GOOGL, -1.82%, Amazon AMZN, -0.85% and Facebook FB, -0.30%, “pay their fair share of tax.” (…)

The clear hope of European governments is that the U.S. will rejoin the OECD talks, so that an international agreement on global tax can be struck next year. This should not be too difficult: Even the companies targeted by the measure have indicated their preference for a global tax, which would spare them the compliance costs of having to deal with many different national ones. (…)

‘It will change everything’: DeepMind’s AI makes gigantic leap in solving protein structures Google’s deep-learning program for determining the 3D shapes of proteins stands to transform biology, say scientists.

(…) DeepMind’s program, called AlphaFold, outperformed around 100 other teams in a biennial protein-structure prediction challenge called CASP, short for Critical Assessment of Structure Prediction. The results were announced on 30 November, at the start of the conference — held virtually this year — that takes stock of the exercise.

“This is a big deal,” says John Moult, a computational biologist at the University of Maryland in College Park, who co-founded CASP in 1994 to improve computational methods for accurately predicting protein structures. “In some sense the problem is solved.”

The ability to accurately predict protein structures from their amino-acid sequence would be a huge boon to life sciences and medicine. It would vastly accelerate efforts to understand the building blocks of cells and enable quicker and more advanced drug discovery. (…)

“It’s a game changer,” says Andrei Lupas, an evolutionary biologist at the Max Planck Institute for Developmental Biology in Tübingen, Germany, who assessed the performance of different teams in CASP. AlphaFold has already helped him find the structure of a protein that has vexed his lab for a decade, and he expects it will alter how he works and the questions he tackles. “This will change medicine. It will change research. It will change bioengineering. It will change everything,” Lupas adds. (…)

")

")

{kind=link}

{kind=link}