FactSet StreetAccount Summary

– US Weekly Recap: Dow (1.52%), S&P (1.58%), Nasdaq (0.73%), Russell 2000 (1.29%)

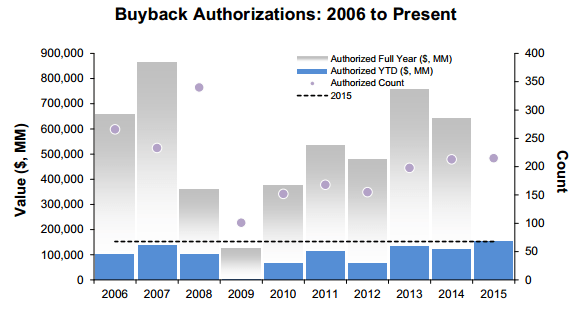

Farfetch valuation and the weekly roundup in tech and retail by Leah Grace

(…) In a follow-up to my post about self-driving cars, consulting firm McKinsey & Co. just released a study on self driving cars, claiming that self-driving cars could save thousands of lives and could boost Internet revenue by billions.

Mario Draghi’s Yield of Dreams QE has been better on the promise than it might be in execution.

The European Central Bank begins its much-anticipated purchases of sovereign bonds on Monday, and ECB President Mario Draghi says the program known as quantitative easing is working before it has even begun. He’s right about that, as strange as it sounds, and therein lies the paradox of Europe’s dive into QE: It may already have had the most effect it is going to have through Mr. Draghi’s salesmanship and Europe’s will to believe. (…)

As a result of Mr. Draghi’s open-mouth operations to talk down the euro—coupled with an expectation that interest rates might rise soon in the U.S.—the euro has declined steadily against the dollar and other currencies. On Thursday it hit an 11-year low of $1.10, compared to about $1.40 last summer. (…)

But the great unanswerable is whether QE will provide a further boost now that it is finally being implemented, especially to the smaller companies that create most of Europe’s jobs. Loan demand remains weak, and surveys of business sentiment have detected no surge in confidence. While Mr. Draghi is trying to boost lending to households and businesses with QE, banks face growing pressure from regulators—including the ECB—to reduce their risks to avoid another financial crisis.

The problem is that Europe’s companies have too-little reason to invest in growth when doing so subjects them to complex and expensive labor laws, regulations and high taxes. Mr. Draghi recognizes this and peppers his public speeches with pleas to enact supply-side economic reforms.

Europe’s political class doesn’t want to do that heavy lifting, so it relies instead on Mr. Draghi’s monetary policies to spur growth. The more aggressive he is, the more the politicians conclude they can do less. (…)

Expectations have a place in economic policy, but Mr. Draghi has spent the months since August helping markets convince themselves that the ECB is the growth engine of last resort. Perhaps everyone’s right and QE will save the day. If it doesn’t, pro-growth reform will be the only policy Europe hasn’t tried.

In reality, the Eurozone is showing signs of renewed life as shown by Markit’s PMI and recent retail sales data:

Lord Rothschild Warns Investors: “Geopolitical Situation Most Dangerous Since WWII”

Our policy has been clearly expressed over the years. Simply put, it is to deliver long-term capital growth while preserving shareholders’ capital; the realisation of this policy comes at a time of heightened risk, complexity and uncertainty. The economic and geopolitical environment therefore becomes increasingly difficult to predict.

The world economy grew at a disappointing and uneven rate in 2014 after six years of monetary stimulus and extraordinarily low interest rates.

Stock market valuations however, are near an all-time high with equities benefiting from quantitative easing.

Not surprisingly, the value of paper money has been debased as countries have sought to compete and generate growth by lowering the value of their currencies – the Euro and the Yen depreciated by over 12% against the US Dollar during the course of the year and Sterling by 5.9%.

In addition to this difficult economic background, we are confronted by a geopolitical situation perhaps as dangerous as any we have faced since World War II: chaos and extremism in the Middle East, Russian aggression and expansion, and a weakened Europe threatened by horrendous unemployment, in no small measure caused by a failure to tackle structural reforms in many of the countries which form part of the European Union.

Timely: