Home Sales Remained Sluggish in October Sales of existing homes increased 2% but some economists say the deal level is below the market’s potential because of a lack of inventory

Existing-home sales increased 2% in October from a month earlier to a seasonally adjusted annual rate of 5.48 million, the National Association of Realtors said Tuesday. But sales dipped 0.9% from the same month a year earlier, the second consecutive decline on an annual basis. (…)

Sales in the south rose 1.9% from September but remained 1.8% lower than a year ago. (…)

Housing inventory decreased 3.2% in October and is 10.4% lower than a year ago, having fallen year-over-year for 29 consecutive months, according to NAR. (…)

The supply shortage, in turn, is driving prices higher. The median price of homes sold last month rose to $247,000, up 5.5% from a year earlier. (…)

(The Daily Shot)

Weak pending sales…(Bloomberg)

Yellen Says She’s Uncertain Weak Inflation Is Transitory The Federal Reserve is monitoring inflation closely given officials’ uncertainty over whether the factors keeping it below their 2% target will prove endemic, Chairwoman Janet Yellen said.

“We expect [inflation] to move back up over the next year or two, but I will say I’m very uncertain about this,” Ms. Yellen said. (…) “this year low inflation is surprising because we’re at essentially full employment,” Ms. Yellen said. (…)

The debt time bomb that keeps growing and now equals nearly half of US GDP

Source: Informa Financial Intelligence

(…) “The only thing I would say that is concerning — there is some rhyming nature to the fact there are no covenants in deals anymore and structure doesn’t matter anymore,” he said. “That does give you some pause. I’m not worried about the leverage. It’s not going to be a 2018 dynamic. I am worried about longer term that some of the lack of covenants or collateral or structure,” he said. (…)

Source: Liscio Report

Here’s the aggregate of all the above data points, courtesy of Moody’s:

In dollars:

Are these two trends just a coincidence?

Two reminders:

- Interest rates are now on an uptrend after reaching 200-year lows. David Rosenberg estimates that “if not for the current low interest rate structure, debt-service charges and the deficit would be $250 billion higher than they are today. But under the CBO projections, net interest charges go from $269 billion in 2017 to $818 billion in 2027 (…). At that time, more than 15 cents of every revenue dollar will be diverted towards servicing the debt compared with 8 cents today.” This while so called entitlement requirements will be ballooning as the 78 million baby-boomers get to collect their pension and use and abuse the health-care system.

- The GOP’s tax reform will boost all debt and debt-servicing ratios way above current levels over the next 10 years. This, of course, assumes tax cuts don’t pay for themselves, as is always the case.

BTW:

‘Why aren’t the other hands up?’ A top Trump adviser’s startling response to CEOs not doing what he’d expect

President Trump’s top economic adviser, Gary Cohn, looked out from the stage at a sea of CEOs and top executives in the audience Tuesday for the Wall Street Journal’s CEO Council meeting. As Cohn sat comfortably onstage, a Journal editor asked the crowd to raise their hands if their company plans to invest more if the tax reform bill passes.

Very few hands went up.

Cohn looked surprised. “Why aren’t the other hands up?” he said. (…)

A Bank of America-Merrill Lynch survey this summer asked over 300 executives at major U.S. corporations what they would do after a “tax holiday” that would allow them to bring back money held overseas at a low tax rate. The No. 1 response? Pay down debt. The second most popular response was stock buybacks, where companies purchase some of their own shares to drive up the price. The third was mergers. Actual investments in new factories and more research were low on the list of plans for how to spend extra money.

The results of the Bank of America poll show a very similar pattern of corporate behavior to what happened after the 2004 tax repatriation holiday when U.S. companies spent the majority of their money coming back home from overseas on stock buybacks. It was a payday for Wall Street investors that generated little benefit to the middle class and wider economy. (…)

Corporate America has enjoyed record profits and margins and record-low interest rates. Why would a tax cut change suddenly their behavior?

The FT’s Martin Wolf:

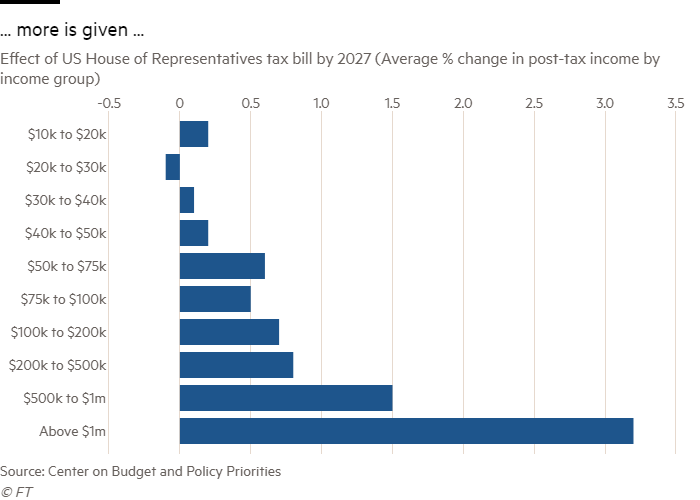

A Republican tax plan built for plutocrats

(…) The tax bills going through Congress demonstrate the party’s primary objectives. According to the Center on Budget and Policy Priorities, in the House version of the bill, about 45 per cent of the tax reductions in 2027 would go to households with incomes above $500,000 (fewer than 1 per cent of filers) and 38 per cent to households with incomes over $1m (about 0.3 per cent of filers). In the more cautious Senate version, households with incomes below $75,000 would be worse off. (…)

Is This The Real Reason Why The Treasury Curve Has Been Collapsing For A Month?

Is This The Real Reason Why The Treasury Curve Has Been Collapsing For A Month?

A ‘funny’ thing happened a month ago. The Treasury yield curve suddenly started to collapse… despite gains in stocks and positive economi data surprises… the question is, why?

Currently, the top corp tax rate in the US is 35%. It looks most likely that rate will drop to 20% when tax reform passes. If you are a corp with an underfunded pension fund, you get a tax incentive to fund the pension THIS YEAR vs in the future when the corp tax rate drops to 20%.

Why? Because contributions to the pension plan are tax deductible. You get a bigger tax deduction in 2017 then you will get in 2018 and onwards (assuming tax reform happens in something close to its current form…which it looks like it will).

Multiple primary dealers have reported pension buying in the 30yr sector over the past month, and coincidentally, 30yr bonds have rallied while the front end has sold off for the past month. (…)

This would negatively impact Q4 profits. (tks Fred)

(…) The Bank for International Settlements, the Basel-based central bank for central banks,

(…) The Bank for International Settlements, the Basel-based central bank for central banks,