FLASH PMIs

U.S. private sector businesses recorded a sharp and accelerated upturn in output led by the service sector during October, with growth the strongest for three months, albeit still much weaker than seen earlier in the year.

However, October also saw a survey-record rise in backlogs of work as firms struggled to meet demand due to supply chain bottlenecks and labour shortages, in turn driving the steepest rise in prices yet recorded by the survey.

Adjusted for seasonal factors, the IHS Markit Flash U.S. Composite PMI Output Index posted 57.3 in October, rising from 55.0 in September to signal the fastest uplift in activity for three months and one that was sharp overall. Stronger growth was driven by the services sector, which registered the quickest rate of expansion since July. Meanwhile, the latest rise in factory production was the softest since July 2020 and only mild, as goods producers continued to be severely hampered by material shortages and supply chain delays.

At the same time, inflows of new work to private sector firms rose further, extending the current sequence of improving demand to 15 months. The rate of new order growth slowed slightly since September to the weakest since December 2020, but was nonetheless solid.

Stronger sales placed further pressure on business capacity during October. The level of outstanding business rose at a series record pace, with respondents linking the latest rise with supply issues and a lack of staff. Subsequently, companies stepped up their hiring efforts in October. Employment increased at the quickest pace since June in spite of further reports of difficulties sourcing candidates and retaining staff.

October data also highlighted stronger inflationary pressures across the US economy. Average input prices rose at a survey record pace, with firms attributing higher costs to supply issues, material shortages, greater transport fees and increased wage bills. Subsequently, the rate of selling price inflation for goods and services also hit a new series peak.

Finally, the level of sentiment regarding output in the year ahead dipped to the joint-lowest in eight months (on a par with July), with many companies noting concerns surrounding ongoing supply issues, labour shortages and price pressures.

The seasonally adjusted IHS Markit Flash U.S. Services PMI™ Business Activity Index rose from 54.9 in September to 58.2 in October, to signal the most marked expansion in services activity for three months.

Driving growth in October was the quickest rise in inflows of new work since July, that was commonly attributed to stronger demand conditions as COVID-19 worries eased during the month.

Concurrently, service providers recorded more intense capacity pressures amid reports that firms were struggling to cope with growing sales due to labour issues and supplier delays. Notably, the rate of backlog accumulation was the most marked in 12 years of data collection.

Companies did, however, raise their workforce numbers at the quickest rate since June during October, although some panellists reported issues finding candidates and filling open positions.

October data also pointed to a continued spill-over of inflationary pressures. The rate of input price inflation accelerated to the second-fastest on record, and was only slightly weaker than May’s peak. Higher transportation costs, wages, supplier fees and material prices were cited by panellists as the primary drivers of inflation in October.

Subsequently, service providers upped their average charges for the seventeenth month running. The rate of increase quickened rapidly since September and was the steepest on record.

Operating conditions faced by manufacturers continued to improve in October, albeit at a weaker pace, as highlighted by the IHS Markit Flash U.S. Manufacturing Purchasing Managers’ Index™ (PMI™) falling from 60.7 in September to 59.2 in October. The latest figure pointed to the slowest improvement in the health of the sector since March, albeit one that was among the strongest on record and sharp overall.

The slower improvement in conditions reflected a weaker expansion in output and a moderation in order book growth during October. Factory production rose only modestly, with the pace of increase the slowest since July 2020 as output continued to be hampered by supply chain issues and shortages. October saw a record lengthening of suppliers’ delivery times. Supply issues and sustained sales growth prompted firms to further increase their buying activity and inventories.

The rate of increase in new orders eased to the slowest for eight months, but remained sharp overall. Survey respondents mentioned that order books were again buoyed by strong client demand. At the same time, material shortages, combined with logistical issues and greater commodity prices, were all linked to a further rise in average input costs in October. The rate of inflation surpassed August’s record to reach a fresh series high. Factory gate charges also rose at the fastest pace in the series history as firms continued to pass greater cost burdens through to clients.

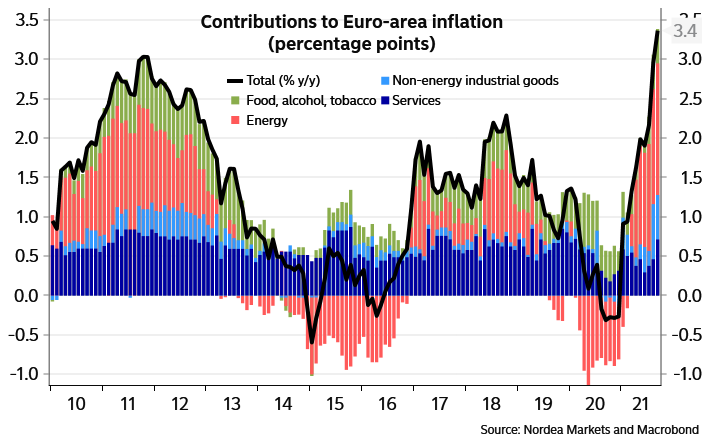

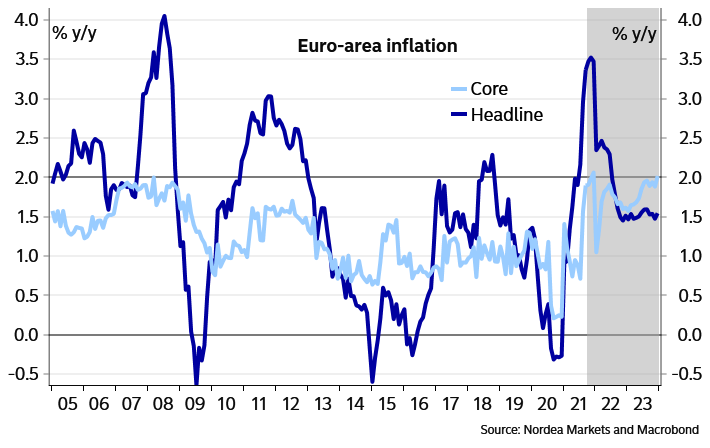

Eurozone business activity growth slowed sharply to a six-month low in October amid increasing supply bottlenecks and ongoing COVID-19 concerns, dropping most markedly in manufacturing though also cooling in services. Survey-record price increases were meanwhile reported as firms sought to pass an unprecedented rise in costs on to customers.

While job creation accelerated to the joint-highest in 21 years as firms boosted capacity to meet demand, optimism about the outlook was hit by supply concerns linked to the pandemic in manufacturing in particular. The headline IHS Markit Eurozone Composite PMI® fell for a third successive month in October, according to the ‘flash’ reading*, dropping from 56.2 in September to 54.3. The decline indicates a further cooling of the rate of expansion from July’s 15-year high. However, although the October expansion was the weakest since April, the latest reading remains above the survey’s pre-pandemic long run average of 53.0 to signal above-trend growth.

Growth slowed especially sharply in Germany, down to the lowest since February, and slipped to the weakest since April in France. The rest of the region as a whole also recorded the slowest expansion since April.

By sector, services outperformed manufacturing for a second month running, the factory sector having now reported a slowdown in growth for a fourth straight month to register the weakest increase in production seen over the past 16 months.

Similarly, while growth of new orders edged higher in services, a slower rate of demand growth was seen in manufacturing. Measured overall, the resulting rise in new orders recorded during October was the slowest since April.

Weakened factory output growth – led by a renewed decline in France and near-stalling of production in Germany – was commonly attributed to supply constraints. Suppliers’ delivery times lengthened to an extent exceeded over more than two decades of survey history only by that seen back in May, as supply shortages and transportation problems continued to worsen.

The autos and parts sector reported the worst performance, with output falling sharply again in October and at an increased rate.

While the service sector saw more robust growth than manufacturing, its rate of expansion cooled for a third month running to reach the lowest since April. Markedly weaker services growth in Germany contrasted with a slight uptick in France, though the rest of the region also saw a moderating expansion.

While some of the slowdown in services reflected a waning of the summer rebound from the fall in activity seen at the start of the year, especially weak service sector performances were recorded for travel, tourism and recreation, reflecting concerns regarding COVID-19. Conversely, strong growth was seen for healthcare, as well as media, banking and non-banking financial services.

Backlogs of work meanwhile continued to rise at an elevated pace. Although the rate of increase moderated to the lowest since April, the survey once again signalled that capacity was stretched both in manufacturing and services, with the former once again reporting an especially marked increase in uncompleted work.

Hiring was stepped up as firms sought to clear backlogs, resulting in a jobs gain that matched July’s two-decade high. Jobs growth accelerated in both Germany and France, and notably was one of the fastest in 21 years in the rest of the region.

By sector, job growth edged up in both manufacturing and services, the former running below recent peaks as material shortages obviated the need for extra workers in some cases, though the latter saw the largest gain since 2007.

Shortages were meanwhile once again seen as the key driver of higher prices for many goods and services in October, leading to a survey record increase in firms’ input costs. An unprecedented input cost increase was recorded in manufacturing while service sector costs rose at the sharpest rate since September 2000.

Selling price inflation likewise accelerated as firms passed higher costs on to customers, reaching the fastest in almost two decades of comparable survey history both in manufacturing and services.

Looking ahead, future sentiment moderated for a fourth consecutive month to the lowest since February. Although the outlook brightened slightly in services, optimism in manufacturing hit the lowest for a year, largely due to concerns over the lingering impact of the pandemic on supply chains and prices.

Activity at Japanese private sector businesses returned to expansion territory at the start of the fourth quarter of 2021, according to the latest flash PMI data. The rise was the first in six months and came as the dominant service sector registered an increase in activity for the first time since January 2020. Moreover, manufacturers reversed the slight decline seen in September to indicate growth for the eighth time in nine months. Panel members commonly associated the slight recovery to a reduction in COVID-19 cases and looser pandemic restrictions.

Private sector businesses also noted an increase in aggregate new business for the first time since April, assisted by a quicker rise in export orders. That said, firms continued to highlight sustained supply chain pressures and material shortages. As a result, input prices rose at the fastest rate in over 13 years. This contributed to the sharpest rise in output charges since July 2018.

Looking forward, companies were optimistic that business activity would improve in the year ahead. Optimism stemmed from hopes that the pandemic would end and provide a broad-based boost to demand.

Powell Says Supply-Side Constraints Have Worsened, Creating More Inflation Risk Central bank is on track to conclude asset-purchase stimulus program by mid-2022

Federal Reserve Chairman Jerome Powell indicated he is now somewhat more concerned about higher inflation and said that the central bank would watch carefully for signs that households and businesses were expecting sustained price pressures to continue.

“Supply-side constraints have gotten worse,” Mr. Powell said Friday at a virtual conference. “The risks are clearly now to longer and more-persistent bottlenecks, and thus to higher inflation.” (…)

“I do think it is time to taper,” Mr. Powell said Friday. “I don’t think it is time to raise rates.” (…)

The virus essentially removed a piece of potential economic output—concentrated in high-contact service sectors, such as leisure, hospitality and entertainment industries. Officials “want to give full time for that to come back” before deliberately cooling demand for goods and services more broadly by raising rates, he said.

On the other hand, inflation is running well above the Fed’s 2% goal. “We see that. We know how painful that is” for consumers, Mr. Powell said.

“We think we can be patient and allow the labor market to heal,” he said. But at the same time, “no one should doubt that we will use our tools to guide inflation back down to 2%” if it looked like more persistent inflationary pressures were taking root, Mr. Powell added.

About the “no one should doubt”, Bloomberg’s account of Powell’s comments could actually raise some doubts about that:

“If we were to see a serious risk of inflation moving persistently to higher levels, we would certainly use our tools to preserve price stability while also taking into account the implications for our maximum employment goal,” he said. “We think we can be patient and allow the labor market to heal,” he said.

From the FOMC’s August 2020 revised Monetary Policy Strategy statement (my emphasis):

On maximum employment, the FOMC emphasized that maximum employment is a broad-based and inclusive goal and reports that its policy decision will be informed by its “assessments of the shortfalls of employment from its maximum level.” The original document referred to “deviations from its maximum level.”

The Brookings Institute:

As Fed Chair Jerome Powell said in unveiling the new strategy, “Our revised statement emphasizes that maximum employment is a broad-based and inclusive goal.” He specifically cited the benefits that a strong economy brings to “low- and moderate- income communities.” Moreover, Powell articulated a new strategy for achieving this goal, saying that the FOMC would base policy on the extent to which employment fell short of its maximum level, rather than focusing on whether employment was deviating from its maximum level, as it had in the past. (…)

This revised statement acknowledges that the FOMC should take into account the substantial differences in labor market outcomes across communities when thinking about full employment and provides a specific strategy for achieving this.

Recall that the Fed’s new policy was framed in mid-2020 after the FOMC concluded that “the historically strong labor market did not trigger a significant rise in inflation” because “the flattening of the Phillips curve” caused a “muted responsiveness of inflation to labor market tightness”.

The new “broad-based and inclusive” strategy put more emphasis on the employment mandate than on the now more vague, floating, “long-run” 2% average inflation mandate. Powell said that “This change may appear subtle, but it reflects our view that a robust job market can be sustained without causing an outbreak of inflation.”

Today’s Fed finds itself confronted with an upside down world where inflation is rising without “maximum employment” triggering the outbreak.

Only one year after the new strategy, wages, quiet when unemployment ran below 4% in 2018-19, are rising in spite of a 5% unemployment rate (6.3% for Hispanic/Latinos and 7.9% for African Americans).

At Friday’s virtual conference, Powell, for the first time and generally unnoticed, incorporated wages into the inflation risk, per Reuters’ account :

Powell noted, “supply constraints and elevated inflation are likely to last longer than previously expected and well into next year, and the same is true for pressure on wages. (…) For now, the Fed will watch and wait”, Powell said.

When Powell warns that “we will use our tools to guide inflation back down to 2%”, he is trying to mute inflation expectations. This supposedly data-dependent Fed is now boxed inside its new policy and has no other choice than to “watch and wait” and hope that the 5 million pandemic-unemployed Americans will soon disappear along with all these transitory shortages.

The market risk is that investors remain more focused on inflation than on “maximum employment”.

- Mohamed A. El Erian: Mystical Hold of ‘Transitory’ Tempts Huge Fed Error Failure to respond quickly and fully to persistent inflation would constitute the biggest monetary policy mistake in more than 40 years.

(…) the cognitive transition at the core of the Federal Reserve — regional Fed banks have shown greater awareness — has been remarkably slow and partial, falling ever further behind what the vast majority of companies have been saying and doing as they cope with input shortages, soaring transportation costs and a lack of sufficient workers.

Labor has also received the message. Quit rates have risen to record highs as more workers switch jobs to secure higher compensation elsewhere. In turn, this has been forcing companies to raise wages and salaries for their existing staff as they seek to strengthen labor retention. To compound matters, strike activity is on the increase. (…)

The cognitive inertia has been amplified by the ill-timed adoption of a “new monetary framework,” which is built for the macro world of yesterday (that is, deficient aggregate demand) and not that of today (deficient supply). Political factors and posturing may also be playing a role. (…)

I strongly suspect that the coming evolution in the Fed’s inflation narrative will come with a doubling down on talk seeking to separate, substantially in time and scale, the tapering of large-scale asset purchases from interest rate increases. The longer and harder the Fed forces this distinction, the more likely it will face market resistance as fixed-income investors realize that, rather than deliver a timely and orderly recalibration of monetary policy, the Fed faces an increasing probability of having to slam on the monetary policy brakes down the road — the “handbrake turn,” to borrow a phrase from Andrew Haldane, the former chief economist of the Bank of England. (…)

It is a risk that still can— and must — be avoided, though the window for doing so is closing fast on the Fed.

- Investors Bet Inflation Pressures Will Linger A key measure of investors’ inflation expectations has climbed in recent weeks, adding fuel to concerns about lasting pressures on consumer prices.

As of Thursday, the gauge known as the 10-year break-even rate suggested that the consumer-price index will rise by an annual average of 2.64% over the next decade, according to Federal Reserve Economic Data, or FRED. That is up from a recent low of 2.28% in late September and the highest level since 2012.

The break-even rate is found by looking at the difference in yields between nominal Treasury bonds and Treasury inflation-protected securities, or TIPS. The rate is so called because TIPS holders can earn the same return as holders of nominal Treasurys if average annual CPI inflation matches that gap over the life of the bonds. (…)

- Hey, Inflation Might Be Good for Us, Says Paulsen Price boosts of 3% or so would spur the economy and stocks, the Leuthold strategist argues.

(…) In his eyes, a modest price increase of 3% to 3.5% on the Consumer Price Index (CPI) should strengthen the gross domestic product (GDP) and the stock market. (…)

“We’ve been fighting inflation for four decades in this country—always being quick to tighten, slow to ease. And the result is we’ve created some of the most sluggish growth over the last 15 years we’ve had in the entire postwar history.”

For Paulsen, a slight inflation jump, above the Fed target, would spur consumers and companies to take more risk, which in turn would pump up earnings and investment returns. He said he concluded this by examining inflation expectations, as compiled by the Cleveland Fed, going back to 1982, at the end of the double-digit era (the CPI’s rise that year was 6.1%, versus 10.3% the year before). (…)

Inflation “stokes animal spirits,” he said. “If people think prices are going to go up over time, that means you might feel better about getting higher wage hikes, for example. And it might cause businesses to expand more operations because they know they can grow into it with pricing flexibility.” (…)

Paulsen added, “There are some good things from a little higher inflation. Not runaway, but from a little higher inflation. Maybe we’re headed to that environment. And if we are, maybe we’re going to get a little better economic outcome.”

I can’t say about the economic outcome but as far as equity returns, it does not verify:

While we’re doing scatter plots, 4% core inflation seems like a trigger for lower P/Es:

Here’s the Rule of 20 P/E against Core CPI: dispersion really narrows after 6% core inflation:

The majority of positive returns happen below 23 on the R20 P/E. Current: 27.3.

INFLATION WATCH

- Shoppers Find Discounts Are in Short Supply This Holiday Season Consumers should expect to pay closer to full price on products this holiday season, including on Nike sneakers, Coach handbags and Ralph Lauren Polo shirts, industry executives and analysts say.

-

U.S. Companies Bet Shoppers Will Keep Paying Higher Prices P&G, Nestlé, Chipotle say price increases haven’t turned customers away, and they expect that to continue even as inflationary pressures mount

(…) P&G, maker of Tide detergent and Pampers diapers, last week announced a third round of price increases, which will go into effect over the next few months, and told investors to expect profitability to accelerate as the year progresses. (…)

Chipotle Mexican Grill Inc. CMG -2.80% said price increases haven’t turned people off its burritos. Higher menu prices helped net income more than double in the most recent quarter, compared with a year before, despite higher labor and commodity costs. (…)

“We’re seeing price increases that are quite shocking, yet consumers have absorbed these prices without a dip in demand,” said Ben Reich, chief executive of Datasembly, which amasses granular pricing data on a range of consumer goods.

Price increases at U.S. grocers rose 1.18% on average in September compared with a year ago, nearly three times the average increase at the start of 2021, according to the firm, which this week plans to launch a publicly available pricing index for U.S. groceries. (…)

The biggest U.S. grocers say they have been insulating consumers from price increases, but that is starting to change. Kroger Co. KR 2.37% and Albertsons ACI 4.44% Cos. both said they would begin passing more costs along to shoppers to protect their own profitability.

“We’ve been very comfortable with our ability to pass on the increases that we’ve seen at this point,” Kroger finance chief Gary Millerchip said in a recent call with analysts. “And we would expect that to continue to be the case.”

- Unilever jacked up prices by more than 4% on average last quarter and signaled that trend will continue into next year. Nestle, P&G and Danone made similar comments.

- Prepare for Propane Sticker Shock Exports have drained domestic supply ahead of heating season and prices have surged.

- What to Do About the Rising Cost of Home Insurance

- La Nina Threatens to Worsen Energy Crisis With Colder Winter

- Goldman sees upside risks to $90/bbl Brent price forecast

So far since the start of the pandemic, nominal aggregate payrolls (employment x hours x wages) have increased 6.0% and headline CPI 5.9%. Recently, employment growth has slowed while weekly hours are near their cyclical peak. Wages? Real wages? Last 6 months inflation annualized: Food: +7.1%, Energy: +12.8%, Rent: +3.2% (+4.1% in the last 3 months, +4.9% in the last 2 months). Don’t be so comfortable…

Citi last week: “…while the US has a bigger ‘flation’ problem than a ‘stag’ problem, we continue to underline the risks to global activity coming from China, where ‘stag’ seems to be the dominant risk, since there is a chance of a deeper and longer Chinese slowdown than the market is braced for”.

But the “stag” part is not so distant in the U.S. given the increasing “flation” problem.

BTW: The Fiscal Boost Is About To Fade…

Some relief coming?

- Natural Gas Prices Drop From Recent Peak Natural-gas prices have shed 19% since hitting a 13-year high earlier this month, reversing some of a run-up that has prompted fears of exorbitant heating bills and higher manufacturing costs at a time of already high prices.

A warm start to autumn is behind the decline. With most of the country yet to turn the heat on, gas has accumulated in storage facilities faster than expected and shrunk a deficit that prompted worries over winter price surges and even potential shortages.

The forecasts that steer commodity traders call for temperatures to remain unseasonably high into November. Meanwhile, federal weather scientists said Thursday that their climate models predict a second straight winter of above-average temperatures, particularly in the South and East. (…)

The U.S. Energy Information Administration said Thursday that about one-third more gas than normal was added to domestic stockpiles last week, the latest in a stretch of above-average weekly builds. Inventories that ended August 7.7% below the recent average are now just 4.2% short, according to EIA data. (…)

(…) At Chinese ports, importers have been able to unload Australian coal—signaling a potential end to a yearlong ban on the trade—though the cargoes haven’t yet cleared customs, analysts and shipping brokers said. (…) “We estimate around five million metric tons of coking coal and three million metric tons of Australian thermal coal stockpiled in Chinese ports could be cleared into China’s domestic market,” said Rory Simington, principal analyst at energy consulting firm Wood Mackenzie. (…)

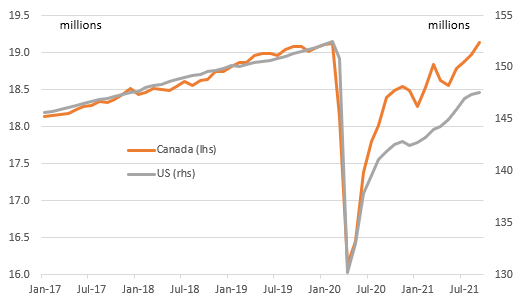

Canadian Retail Sales Slipped in September Amid Supply Constraints Receipts likely fell 1.9%, a preliminary estimate released Friday by Statistics Canada indicated, after a gain of 2.1% in August — slightly ahead of a 2% consensus estimate in a Bloomberg survey of economists. The statistics agency also revised it July data upward to show receipts fell 0.1% instead of the 0.6% contraction previously reported.

U.S. Home Sales Jumped 7% in September Increase in existing-home sales last month followed late-summer drop in mortgage rates

(…) About 23% of September existing-home sales were purchased in cash, up from 18% a year earlier, NAR said.

Many homes are selling above listing price. The typical home sold in September was on the market for 17 days, unchanged from the prior month, NAR said. (…)

The share of first-time buyers in the market fell to 28%, its lowest level since July 2015. Fierce competition has pushed home prices sharply higher and priced a number of people out of the market. While sales rose for homes priced above $250,000 in September, the number of transactions declined below that price point, NAR said. (…)

The median existing-home price rose 13.3% in September from a year earlier, NAR said, to $352,800. That compares to a 15.2% increase the prior month. Price cuts are becoming more common, too. Nearly 15% of listings lowered their prices in September, up from 7.9% in April, according to Zillow Group Inc. (…)

EARNINGS WATCH

From Refinitiv/IBES:

Through Oct. 22, 117 companies in the S&P 500 Index have reported earnings for Q3 2021. Of these companies, 83.8% reported earnings above analyst expectations and 12.0% reported earnings below analyst expectations. In a typical quarter (since 1994), 66% of companies beat estimates and 20% miss estimates. Over the past four quarters, 85% of companies beat the estimates and 12% missed estimates.

In aggregate, companies are reporting earnings that are 13.9% above estimates, which compares to a long-term (since 1994) average surprise factor of 4.0% and the average surprise factor over the prior four quarters of 18.3%.

Of these companies, 77.8% reported revenue above analyst expectations and 22.2% reported revenue below analyst expectations. In a typical quarter (since 2002), 61% of companies beat estimates and 39% miss estimates. Over the past four quarters, 79% of companies beat the estimates and 21% missed estimates.

In aggregate, companies are reporting revenues that are 2.6% above estimates, which compares to a long-term (since 2002) average surprise factor of 1.2% and the average surprise factor over the prior four quarters of 4.1%.

The estimated earnings growth rate for the S&P 500 for 21Q3 is 34.8%. If the energy sector is excluded, the growth rate declines to 27.5%.

The estimated revenue growth rate for the S&P 500 for 21Q3 is 14.5%. If the energy sector is excluded, the growth rate declines to 11.7%.

The estimated earnings growth rate for the S&P 500 for 21Q4 is 22.8%. If the energy sector is excluded, the growth rate declines to 16.1%.

Trailing EPS are now $194.85. Full year 2021: $201.35e. 2022: $220.76e.

- With corporate tax off table, U.S. Democrats turn to billionaires to fund spending bill Democrats were forced to shift to the unorthodox plan in the face of opposition from one of their own senators, Kyrsten Sinema, to raising the corporate tax rate and the top personal income tax rate to pay for the hefty spending plan, which is a pillar of Democratic President Joe Biden’s domestic agenda.

TECHNICALS WATCH

My favorite technical analysis firm notes the improvement in overall market breadth but many important indicators remain in a downtrend. Trading volume has fallen and traditional leaders such as Tech and Consumer Discretionary are not showing much enthusiasm. Small caps continue to seriously lag with declining breadth. Prudence and selectivity remain advisable.

Macrobond, ING

Macrobond, ING