Household Income Jumps, Spending Slows Economists think the Covid-19 Delta variant held back spending growth; expanded child tax credit boosted households as savings remains high

The 1.1% gain in household income marked the biggest jump since March, the Commerce Department said Friday. Families started receiving tax credits worth up to an additional $1,600 per child this year as part of a $1.9 trillion pandemic-relief package passed by Congress this spring.

Many families stashed the extra money, boosting their already high savings.

Growth in consumer spending slowed last month to 0.3%—less than a third June’s spending increase of 1.1%. Economists believe the Delta variant, a highly contagious strain of Covid-19, is partly to blame for the slower growth. Consumer fears of infection, new business restrictions and mask mandates are likely leading households to pull back in some areas, economists said.

Spending on services, such as restaurant outings and sporting events, grew sharply last month but was partly offset by a decline in spending on goods, such as cars and refrigerators.

(…) households now have $1.7 trillion in savings—up from about $1.3 trillion in January 2020, just before the pandemic walloped the economy, Mr. Brusuelas said. (…)

Consumption expenditures (red) keep exceeding labor income (black) since March, indicating that Americans are still willing to dissave. Spending on services (yellow) is slowly recovering and is now slightly above (+1.3%) pre-pandemic levels. Spending on goods (retail sales, blue) has flattened but at a very high level, still 17.5% higher than in February 2020. That’s in spite of low autos purchases due to inventory shortages.

The savings rate has averaged 9.4% in the last 3 months, getting closer to its 7.5% level of the 3 months prior to the pandemic. Will Americans keep extra precautionary savings or spend it all during the holiday season? Important question for growth and inflation forecasters. Yet, Mr. Powell did not address the demand side when discussing inflation during his Jackson Hole speech last Friday.

Powell Says Fed May Start Scaling Back Stimulus This Year Federal Reserve Chairman Jerome Powell reaffirmed the central bank’s emerging plan to begin reversing easy-money policies and detailed why he expects a recent rise in inflation to fade.

(…) Mr. Powell’s remarks didn’t provide a strong signal of when the process is likely to begin, suggesting any tapering isn’t likely to occur before the meeting that follows in early November. (…)

Mr. Powell used the bulk of his speech to explain why he is still confident that this year’s inflation surge would prove temporary and why it is so important for the Fed to get this call right. (…)

Fed officials have set a “different and substantially more stringent test” for raising rates than they have for the “coming reduction in asset purchases,” Mr. Powell said. (…)

By arguing that inflationary pressures still appear likely to largely reverse on their own, Mr. Powell staked out a position that calls for more patience around when to raise rates. He cited a record dating to the 1950s that “taught monetary policy makers not to attempt to offset what are likely to be temporary fluctuations in inflation,” he said. “Indeed, responding may do more harm than good, particularly in an era” when interest rates are more likely to be pinned near zero.

Because it can take a year for monetary-policy decisions to ripple through the economy, tightening policy due to temporary factors raises the risk of an ill-timed move to unnecessarily slow the economy, leading to less hiring and inflation that remains too low, Mr. Powell said. “Today, with substantial slack remaining in the labor market and the pandemic continuing, such a mistake could be particularly harmful,” he said.

At the same time, Mr. Powell pointed to the painful experience of the 1970s, in which the Fed believed large increases in food and energy prices would ease but core inflation continued to run high. Because economists have since concluded that consumers’ and businesses’ expectations of higher inflation in the future were driving actual prices higher, Mr. Powell underscored the Fed’s commitment to monitor these inflation expectations very carefully. The Fed would raise rates “if sustained higher inflation were to become a serious concern,” he said.

In his review of recent inflation developments, Mr. Powell suggested inflation was likely to moderate in the coming months because prices of certain items, such as used cars, that contributed strongly to the recent price surges have begun to decline. So far, there is little evidence that inflation is rising beyond a “relatively narrow group of goods and services that have been directly affected by the pandemic and the reopening of the economy,” he said. Mr. Powell said he saw little evidence of wage increases that might lead to excessive inflation, for example.

Mr. Powell also suggested that long-running forces such as globalization and technology that have held down prices, especially of consumer goods, over the past 30 years are likely to continue once the pandemic subsides. “There is little reason to think” that global disinflationary forces “have suddenly reversed or abated,” he said. (…)

Some participants at Friday’s symposium said they thought, given an outlook that Mr. Powell has said remains highly uncertain, the Fed chairman didn’t pay enough attention to the risks that inflation remains elevated, even if it falls from recent highs.

The speech made a solid case for why inflation pressures will fade away but failed “to take seriously any arguments on the other side,” said Jason Furman, a former chief economist to President Barack Obama. That allowed Mr. Powell to skirt questions of how the Fed would respond to a more difficult scenario where inflation stays high while unemployment is elevated, he said.

“It’s not doing a lot to prepare markets for the harder case, which is completely plausible,” he said.

Also last Friday:

The Office of Management and Budget said it expected consumer prices would rise 4.8% in the fourth quarter from a year earlier, up sharply from the 2% rise that the Biden administration forecast in May. Officials see those price pressures quickly abating next year, with the consumer-price index rising 2.5% in the fourth quarter of 2022, more than the 2.1% they expected in May, and reaching 2.3% in 2023. (…)

The White House also lifted its projections for growth this year to 7.2%, from 5% projected in May, which officials attributed in large part to the faster than expected economic recovery as more Americans became vaccinated and resumed normal activity this summer. (…)

Officials also dialed back their projections for budget deficits this year, projecting an annual shortfall of $3.1 trillion, down from $3.7 trillion forecast in May, as strong economic growth this year bolstered federal revenues. Deficits as a share of gross domestic product are now expected to total 13.9%, down from an earlier projection of 16.7%. (…) (WSJ)

(…) While Powell on Friday noted that job openings, along with the number of people quitting their jobs, are both at record highs, he maintained a “serene” interpretation of the implications, according to Summers, a paid contributor to Bloomberg and a professor at Harvard University. Summers said his own take was that this was a signal of “much more rapid wage increases” over a period of time. (…)

“With all that structural change, you’re likely to see some substantial increase in the level of unemployment that the economy can sustain without excessive inflation,” Summers said. “We’re kind of making a bit of a paradigm error” in terms of the read on inflation dynamics, according to Summers, who’s also a former head of the White House National Economic Council under President Barack Obama.

He also highlighted that Powell in his remarks didn’t mention housing costs, which have been rising rapidly. (…)

I found interesting that the bulk of Powell’s remarks sought to explain why inflation, which has turned out much higher than he expected (a “sharp” run up in inflation), was not a threat and would soon start fading. He also explained how the Fed was monitoring it. Not really reassuring to me…

1. The absence so far of broad-based inflation pressures

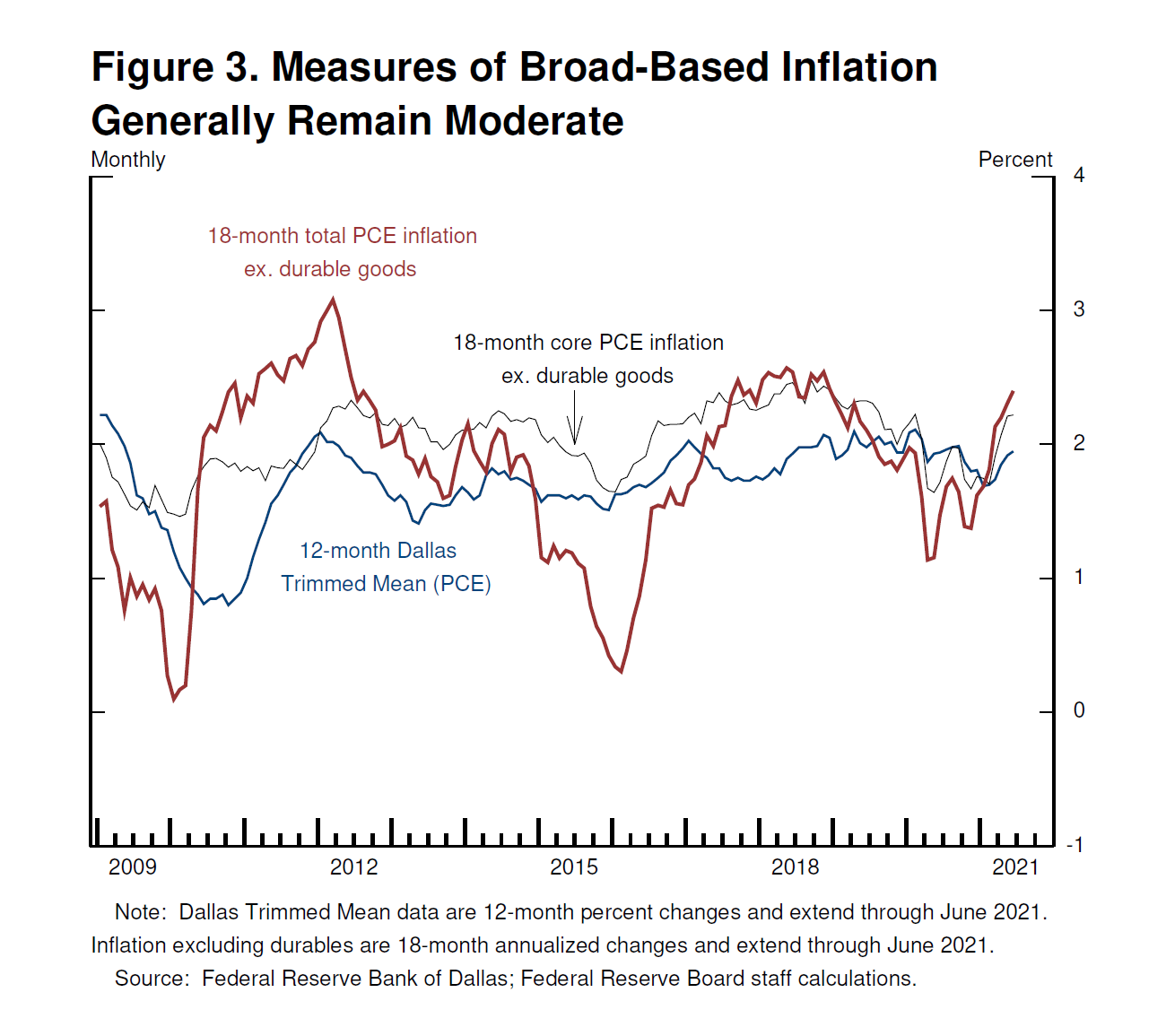

We consult a range of measures meant to capture whether price increases for particular items are spilling over into broad-based inflation. These include trimmed mean measures and measures excluding durables and computed from just before the pandemic. These measures generally show inflation at or close to our 2 percent longer-run objective (figure 3). We would be concerned at signs that inflationary pressures were spreading more broadly through the economy.

Mr. Powell has often mentioned his preference for trimmed mean PCE inflation. His chart plots the 12-month trend at 2.0% but does not show the 6-month trend at 2.6%, up from 1.5% in March, nor the 1-month trend at 3.2% in July, in sharp acceleration from March’s 2.1%.

The Cleveland Fed’s trimmed-mean CPI is at 3.0% YoY in July, up from 2.1% in March. It is up at a 5.3% annualized rate in the last 3 months, from +3.2% in the previous 3-month period.

This Fed claims it is now totally fact-based, but does it consider facts the survey results from its own constituents?

Philly Fed: The firms continued to report increases in prices for inputs and their own goods. (…) Nearly 74% of the firms reported increases in input prices, while 3% reported decreases. The current prices received index reached its highest reading since May 1974. Over 56% of the firms reported increases in prices of their own manufactured goods, up from 50% in July and 36% in April.

And 75.2% currently expect to raise prices again during the next six months, seeing no let down in their own cost inflation. Actually, regarding their own prices, the firms’ median forecast was for an increase of 5.0% over the next 12 months. The firms’ actual price change over the past year was 3.0%.

The firms expect their employee compensation costs (wages plus benefits on a per employee basis) to rise 4.0% over the next four quarters, the same as in May. When asked about the rate of inflation for U.S. consumers over the next year, the firms’ median forecast was 5.0%, an increase from 4.0% in May.

K.C. Fed: On the inflation front, the prices received index for finished products strengthened to a new record 61 in August from 52 in July.

N.Y. Fed: Wages and prices were expected to continue to rise significantly.

More broadly, the even more recent Markit’s August flash PMI surveys revealed that

Services input costs rose markedly and at one of the fastest paces on record amid significant hikes in supplier prices and greater wage bills. Subsequently, service providers raised their selling prices at a sharper rate.

The rate of manufacturing input price inflation was the fastest on record (since May 2007) as suppliers hiked their charges again. Meanwhile, firms increased their own selling prices at the steepest rate in the series history in the hope of partially passing on higher costs to clients.

And from recent corporate conf. calls:

- “We’re seeing general inflation price increases. We were seeing general inflation everywhere. It is very real because there’s underlying cost increases around labor and materials. And one of the things I’ve always said is, this is affecting this entire industry. It’s not only affecting Samsonite and so we will be adjusting prices and the whole industry will be adjusting prices.” – Samsonite International CEO Kyle Gendreau

- “…we’re seeing a less promotional environment and rising inflation, as well as stronger sales in our apparel categories.” – TJX CFO Scott Goldenberg

- Historically, the typical spike above $900 has lasted two to six months. We’re now seven months into the current cycle. We were somewhat insulated from higher steel prices in the first half of 2021 due to advanced contracts, which were negotiated late last year. However, in the second half of the year, we are experiencing significant headwinds from higher steel prices.” – Lear SVP & CFO Jason Cardew.

Goldman Sachs’ index of company price announcements is at the highest level since 2011, and mentions of the word “inflation” in this season’s Russell 3000 earnings calls were the most frequent since their series began in 2010.

Taiwan Semiconductor Manufacturing Co., the world’s largest chip manufacturer, plans to increase the prices of its most advanced chips by roughly 10%, while less advanced chips used by customers like auto makers will cost about 20% more. The higher prices will generally take effect late this year or next year.

Non-fuel import prices are up 6.3% YoY in July, 6.5% annualized in the last 3 months.

2. Moderating inflation in higher-inflation items

Mr. Powell discussed at length fading inflation on goods (but he only specifically mentioned cars which, btw, have only deflated 5% from their peak!) that flared up this year but never discussed rising pressure on items that have not contributed much to inflation so far but are likely to bite soon such as rent and housing costs.

Incidentally, the same Dallas Fed that provides Powell with the trimmed mean PCE data also has this chart which seems to disprove his assertion that there is no “broad-based inflation pressures”. You can trim only up to a point. Nearly 60% of PCE components prices are rising by more than 3% in July, 42% by more than 5% and 24% by more than 10%.

BTW: The number of ships waiting to enter the biggest U.S. gateway for trade with Asia reached the highest since the pandemic began, exacerbating delays for companies trying to replenish inventories during one of the busiest times of the year for seaborne freight. (Bloomberg)

3. Wages

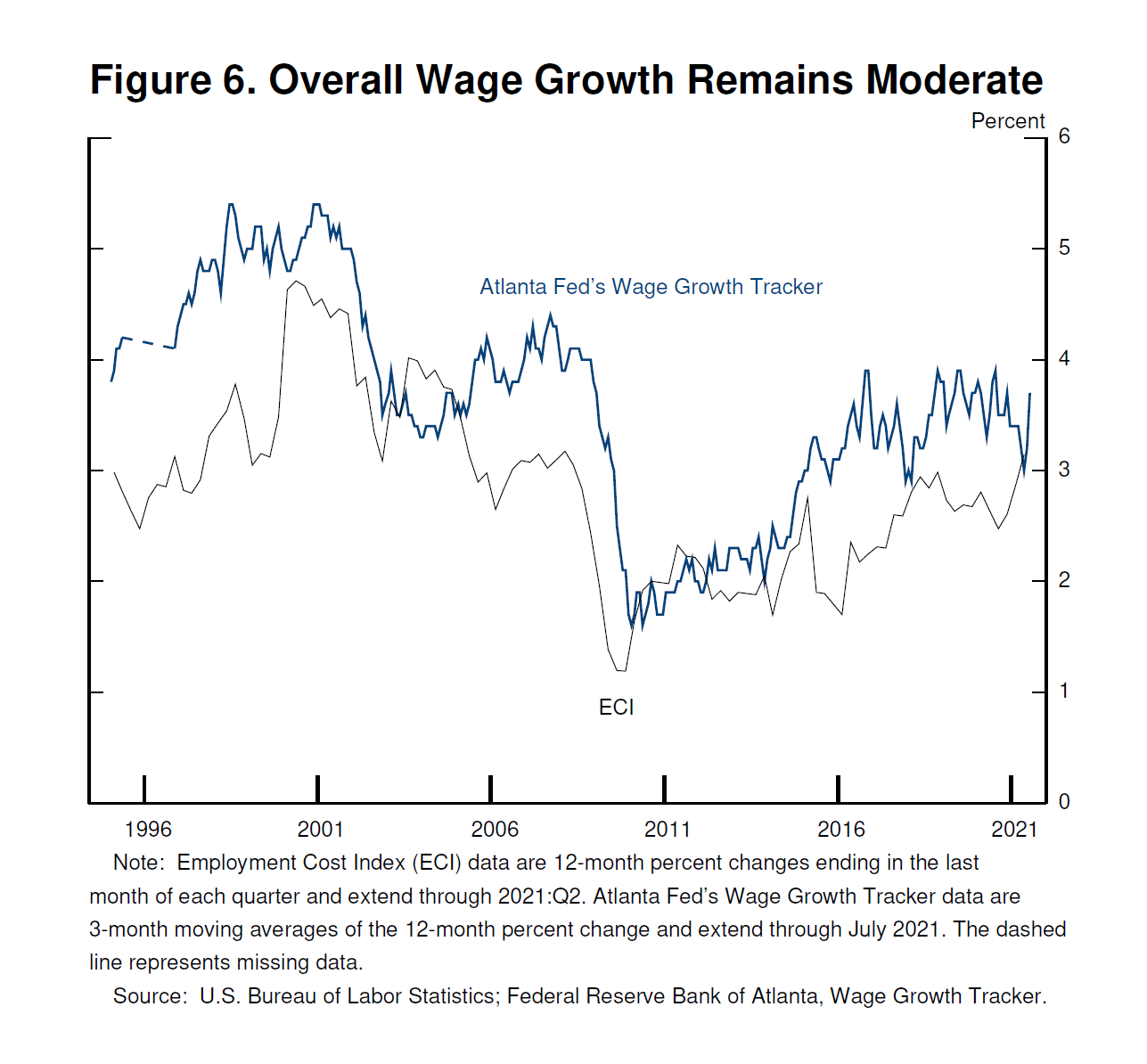

(…) if wage increases were to move materially and persistently above the levels of productivity gains and inflation, businesses would likely pass those increases on to customers, a process that could become the sort of “wage–price spiral” seen at times in the past. Today we see little evidence of wage increases that might threaten excessive inflation (figure 6). Broad-based measures of wages that adjust for compositional changes in the labor force, such as the employment cost index and the Atlanta Wage Growth Tracker, show wages moving up at a pace that appears consistent with our longer-term inflation objective. We will continue to monitor this carefully.

The Atlanta Fed’s Wage Tracker is a 3-m moving average of median wage growth so it may be lagging a little at its July 3.7% level. The ECI’s Total Comp. index is up “only” 3.1% YoY in Q2 but its Wages and Salaries component is up 3.6% YoY and 4.0% annualized in Q2 from 3.0% pre-pandemic. The trend is certainly not comfortable, particularly with so many companies raising prices allegedly to try to offset their rising input costs. More and more companies are specifically mentioning higher wages in recent months.

The Richmond Fed’s August survey said that “Survey results suggested that many firms increased employment and wages in August, as the wage index hit a record high.”

From recent conf. calls:

- “As we look ahead, wage inflation is expected to remain at headwinds. The employment market remains very tight.” – Kohl’s CFO Jill Timm

- “…labor is our number one challenge. (…) labor is our single biggest issue we face (…). We’ve increased wages and created flexible shifts and childcare onsite clinics.” –Tyson Foods CEO Donnie King

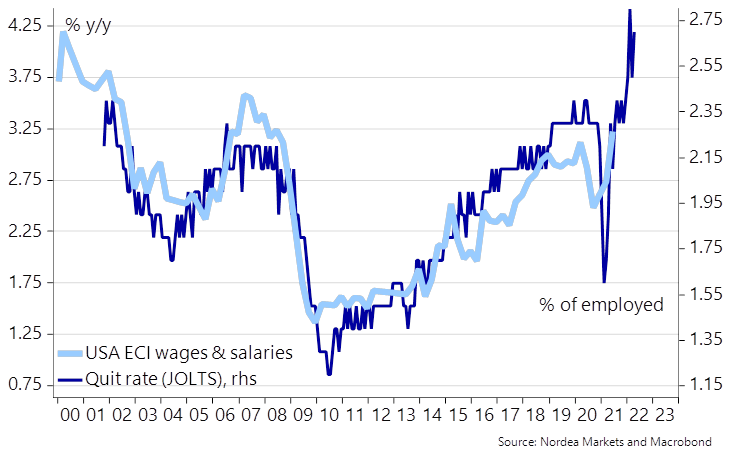

And this chart from Nordea suggests higher wage inflation coming:

GS’ composition-corrected wage tracker increased to +3.5% YoY — its highest level since 2007 — and GS’ wage survey leading indicator has rebounded to +3.9% — its highest level since 2001.

4. Longer-term inflation expectations

Policymakers and analysts generally believe that, as long as longer-term inflation expectations remain anchored, policy can and should look through temporary swings in inflation. Our monetary policy framework emphasizes that anchoring longer-term expectations at 2 percent is important for both maximum employment and price stability.

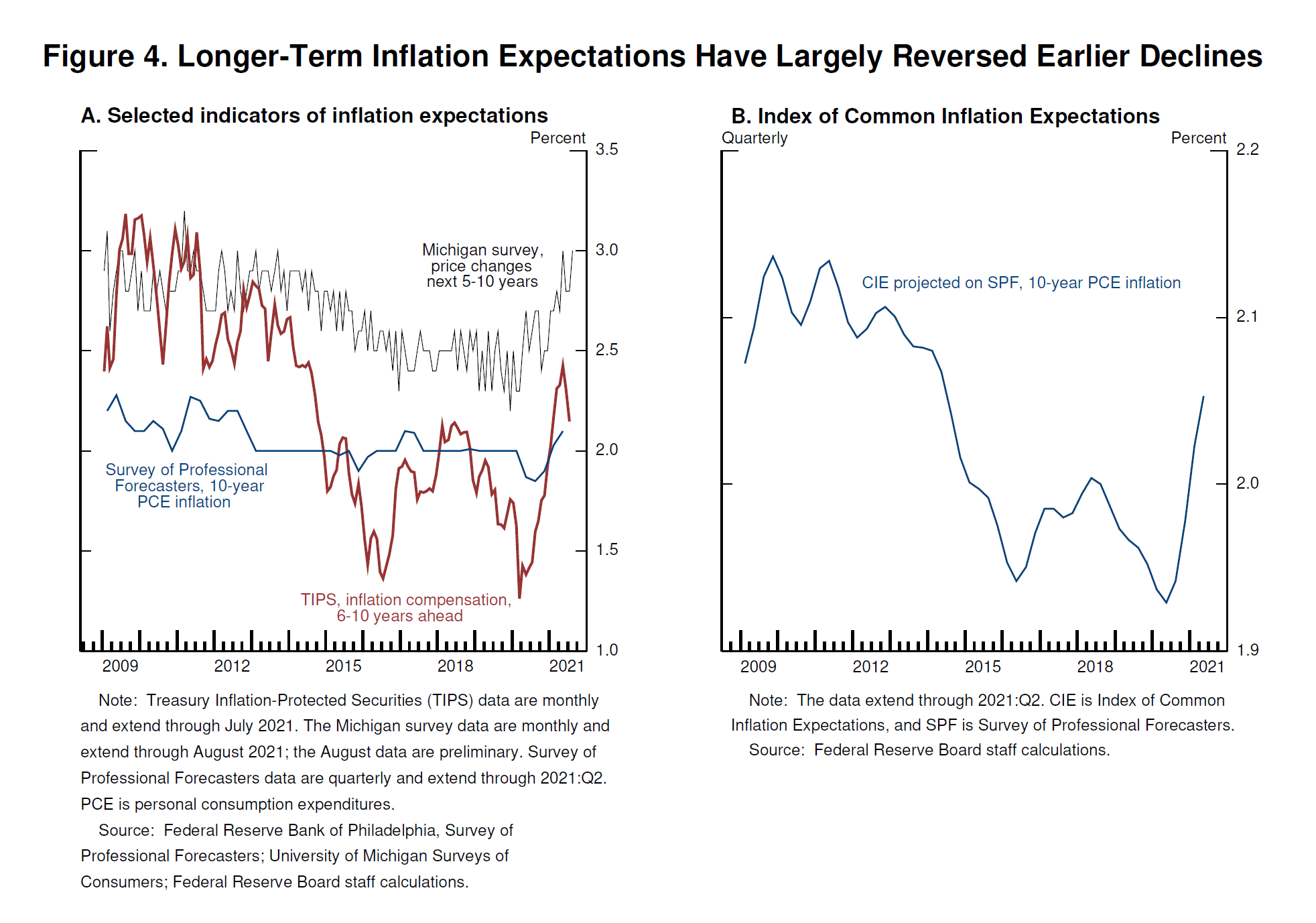

We carefully monitor a wide range of indicators of longer-term inflation expectations. These measures today are at levels broadly consistent with our 2 percent objective (figure 4). (…)

Longer-term inflation expectations have moved much less than actual inflation or near-term expectations, suggesting that households, businesses, and market participants also believe that current high inflation readings are likely to prove transitory and that, in any case, the Fed will keep inflation close to our 2 percent objective over time.

Some other surveys differ.

The NY Fed survey adds that

Consumers polled by the New York Fed said they expected rents to increase 9.8% in the coming year, the highest reading since the survey began in 2013. Expected changes in medical care costs over the next 12 months ticked up to 9.5%, while the expected change in gas prices moderated to 8.1%.

Goldman’s composite of seven business inflation expectations rose to the highest level in its two decade history. Businesses are on inflation’s front line.

5. The prevalence of global disinflationary forces over the past quarter century

(…) While the underlying global disinflationary factors are likely to evolve over time, there is little reason to think that they have suddenly reversed or abated. It seems more likely that they will continue to weigh on inflation as the pandemic passes into history.

Mr. Powell, who seems to have forgotten part of the Trump presidency, displays a 25-year chart of inflation for Canada, the Euro area, Sweden, Switzerland and Japan. Let’s say that

- I personally would not have chose these particular countries to prove that particular point;

- I would not wish to base my judgement and policy decisions on 36-month moving averages.

Some charts FYI from Ed Yardeni:

From Markit: “In the Eurozone, the rate of input price inflation accelerated to the second-fastest on record (since October 2009), with both manufacturing and service sectors registering a quicker rise in costs. At the same time, the rate of selling price inflation ticked higher as firms sought to pass higher input prices on to clients.

From Robert Brusca at Haver Analytics who seems to read my mind:

The German PPI rose by a brisk 1.9% in July as the PPI excluding energy gained 1.2%. June also saw a better-than one percentage point gain in both the PPI and the ex-energy PPI as did May. In fact, March and April both come close to these marks with month-to-month gains of 0.8% and 0.9% for the headline and ex-energy measures, both. Inflation pressures have become intense and are lasting. (…)

What is clear is that German PPI inflation really is too high and it is accelerating from 12-months to six-months to three-months. The same is true for the CPI and the CPI excluding energy also is too high and it is accelerating from 12-months to six-months to three-months. There is a whole lot of uncomfortable inflation news here. And Germany is not alone in this. It is, more or less, a global phenomenon.

(…) central bankers imbue their view with a sense of certainty that I think is simply unfounded. Perhaps they think that if we believe what that they know is true we will shift our beliefs… (…)

For now, what we can see is that inflation pressures are cooking across timelines and across inflation measures. (…)

So I wonder exactly how central bankers are coming to support views that I do not seem to be able to identify on my own. Pardon me If I remain suspicious of the Fed’s constant denial of inflation reality and if I focus on its ‘forecasts’ from 2015-2018 when it led us astray. By thinking – AGAIN- that current inflation reality is wrong and its forecast is right, the Fed is once again substituting a view of reality for reality. It is once again doing the same thing, finding a distraction from current reality to dismiss what is a perfectly valid and entrenched inflation trend in order to ignore it.

For European and German conditions, things are not as distorted as in the U.S. But the denial is still there. (…)

“Reports that say that something hasn’t happened are always interesting to me, because as we know, there are known knowns; there are things we know we know. We also know there are known unknowns; that is to say we know there are some things we do not know. But there are also unknown unknowns—the ones we don’t know we don’t know. And if one looks throughout the history of our country and other free countries, it is the latter category that tends to be the difficult ones.” (Donald Rumsfeld)

![]() Maybe there are also unknown knowns, facts that we just refuse to see or pretend they don’t exist.

Maybe there are also unknown knowns, facts that we just refuse to see or pretend they don’t exist.

Mark Twain to Jay Powell: “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

- Mohamed A. El-Erian: Fed’s Powell Cheers Markets But Risks a Mistake Investors will happily continue to give the Federal Reserve chair the benefit of the doubt, but there’s good reason to question his characterization of policy being “well positioned.”

(…) By refraining from breaking new ground or providing operational details of any evolution in policy, both of which would have inevitably tilted more hawkish at this point, Powell gave investors more reason to take stocks and bonds higher.

(…) there’s good reason to question the characterization of Fed policy being “well positioned.” For example:

- The five reasons that Powell set out to support his oft-repeated argument that the recent spike in prices is likely transitory do little to alleviate current concerns about an inflation dynamic that is already proven and, judging from Friday’s data, continues to be hotter and more persistent than the Fed expects.

- His failure to mention housing and rental inflation missed an important part of the evolving inflation story, and one that has consequential economic, social and political implications.

- Powell’s outlook for the economy doesn’t seem to reflect sufficient appreciation of the bottom-up, cost-push pressures that the majority of companies are experiencing and that several regional Fed presidents have cited in their own assessments of the economic outlook and their associated call for an early taper.

- After a balanced historical reading of policy reactions to higher inflation, Powell’s characterization of the current risk of a potential policy mistake appears overly biased in favor of an overreaction to inflation. If anything, the Fed is quite far from this given that it is still maintaining the uber-stimulative policy stance that it adopted well over a year ago at the height of the Covid disruptions to the economy and markets.

- Finally, while rightly pointing to the uncertainties associated with the delta variant, Powell shied away from discussing the considerable and increasing decoupling of finance from the real economy.

Investors will happily continue to give Powell the benefit of the doubt; after all, his policy approach has paved the way for increasing financial wealth. Economists, though, are more divided. The beneficial impact on the economy of the Fed’s massive asset purchases are limited, if any, while the risks to economy and the financial system continue to mount.

I continue to believe there is just cause for concern about a monetary policy mistake that could undermine future economic wellbeing and financial stability, with adverse social, institutional and political spillovers. I am hoping that my worries are misplaced but unfortunately, both the numbers and the analysis suggest otherwise.

Covid-19 in Malaysia Threatens to Prolong Chip Shortage The country in Southeast Asia is cited as auto makers cut production, highlighting a little-known but critical link in the semiconductor supply chain.

The Southeast Asia nation is one of the world’s top destinations for assembly and testing of the devices that control smartphones, car engines and medical equipment. Disruptions in Malaysia threaten to prolong uncertainty over chip supply well into next year, dashing hopes of relief in the second half of 2021. (…)

Mr. Vijayaraghavan said chip manufacturing relies on a precarious model designed to keep costs low by holding minimal inventory and spreading assembly across several markets specializing in processes that are hard to relocate in a pinch. “There’s very little room for error, so whenever there’s any disruption you see it all the way through to the end product because there’s just no slack in the system,” he said.

Malaysia is a major hub for packaging, a labor-intensive process of combining basic elements into functioning components and testing them for quality before they are shipped abroad and made into end-use products. About 7% of the global supply of semiconductors goes through the country at some point, according to the U.S.-based Semiconductor Industry Association. The U.S. imports more chips directly from Malaysia than from any other country in the world, the group said. (…)

In practice, factory output could be uneven for the next two or three quarters, until the entire country reaches a higher vaccination rate and transmission slows. Malaysia has fully vaccinated almost 45% of its population, according to Our World in Data. (…)

High-Frequency Charts Show U.S. Economy Softening From Delta

- The number of travelers moving through airport checkpoints has started to drop again. (…) The seven-day average has declined to around 1.76 million passengers a day in late August from around 2.05 million a month earlier. (…) There’s been a “deceleration in leisure booking and an increase in cancellations,” said Helane Becker, senior reseach analyst with Cowen Inc. As companies have delayed a return to offices, the return of business air travel is also likely delayed, she said.

- Seated dining at U.S. restaurants has been running at about 10-11% below 2019 levels in recent weeks, after narrowing the gap to just 5-6% below in late July, according to OpenTable, which processes reservations online.

- (…) hotel occupancy has now declined for four consecutive weeks, according to STR, a lodging data tracker. Average room rates have declined for three weeks.

- “Labor demand might drop if people cut back on travel, eating out, and other services spending.” And potential workers might be reluctant to look for work, (…).

McDonald’s, others consider closing indoor seating amid Delta surge in U.S.

Delta-driven Covid surge puts renewed strain on US hospitals Hospitalisations top 100,000 and seven-day tally of infections surpasses 1m for first time since January

EU Seeks to Block Nonessential Travel From the U.S. The EU action is in response to the increase in Covid-19 cases in the U.S. European officials have been considering the move for much of the last month.

(…) CBA’s downgraded outlook comes as data shows retail sales collapsed in Sydney in July as lockdowns were extended and cases of the Delta variant rose swiftly, spreading to regional areas of New South Wales soon after.

Based on current estimates, the lockdown of activity in Sydney, which accounts for about one-third of national output, could extend into November as the state government races to boost vaccination levels.

With Victoria also in lockdown, more than half of Australia’s population is affected by mobility constraints. (…)

No recession scare in the USA at this time…but credit markets are sniffing something:

(@B2Investor)

EARNINGS WATCH

From Refinitiv/IBES

Through Aug. 27, 489 companies in the S&P 500 Index have reported earnings for Q2 2021. Of these companies, 87.7% reported earnings above analyst expectations and 9.4% reported earnings below analyst expectations. In a typical quarter (since 1994), 66% of companies beat estimates and 20% miss estimates. Over the past four quarters, 83% of companies beat the estimates and 14% missed estimates.

In aggregate, companies are reporting earnings that are 15.9% above estimates, which compares to a long-term (since 1994) average surprise factor of 3.9% and the average surprise factor over the prior four quarters of 20.1%.

Of these companies, 87.1% reported revenue above analyst expectations and 12.9% reported revenue below analyst expectations. In a typical quarter (since 2002), 61% of companies beat estimates and 39% miss estimates. Over the past four quarters, 74% of companies beat the estimates and 26% missed estimates.

In aggregate, companies are reporting revenues that are 5.3% above estimates, which compares to a long-term (since 2002) average surprise factor of 1.1% and the average surprise factor over the prior four quarters of 3.5%.

The estimated earnings growth rate for the S&P 500 for 21Q2 is 95.4%. If the energy sector is excluded, the growth rate declines to 79.9%. The estimated revenue growth rate for the S&P 500 for 21Q2 is 24.9%. If the energy sector is excluded, the growth rate declines to 20.8%.

The estimated earnings growth rate for the S&P 500 for 21Q3 is 29.8%. If the energy sector is excluded, the growth rate declines to 23.2%.

No change in positive trends for revisions nor guidance.

Trailing EPS are now $183.10.

Full year 2021: $201.84. Full years 2022: $220.39.

TECHNICALS WATCH

Market tops are supposedly not events but processes. Looking at the S&P 500 Index, the event is another new high, I think the 52nd this year! But if one looks at the market internals, the topping process seems to be continuing. Selectivity is still in force as fewer stocks are making new highs while the large cap index is. Momentum is also waning with only fewer and fewer stocks above their moving average. (Charts below courtesy of CMG Wealth)

And we are defying gravity: is this time so different?

As said, the large cap index is not showing much weakness, is it?

-

13/34–Week EMA Trend Chart:

But small caps are going nowhere this year:

Billionaire Paulson Who Shorted Subprime Calls Crypto ‘Worthless’ Bubble

(…) Now though, more than 14 years after CDOs and credit-default swaps dominated everyone’s attention, Paulson is again seeing signs of excessive speculation.

Paulson, 65, is increasingly concerned about rising prices, he said in an episode of “Bloomberg Wealth with David Rubenstein.” The rapidly expanding money supply could push inflation rates well above current expectations, he said, and gold, which he’s backed for years, is primed for its moment.

His harshest words are for the hottest investments of this era. SPACs, on average, will be a losing proposition, while cryptocurrencies are a bubble that will “eventually prove to be worthless.” (…)

But the area that’s most mispriced today is credit. You have current inflation that’s well in excess of long-term yields and there’s a perception in the market that this is transitory. I think they bought the federal line that it’s just temporary, due to the restart of the economy and that it’s eventually going to subside. However, if it doesn’t subside, or it subsides at a level that’s above the 2% that the Fed is targeting, then ultimately interest rates will catch up and bonds will fall. In that scenario, there are various option strategies related to bonds and interest rates that could offer very high returns. (…)

We thought in 2009 with the Fed doing quantitative easing, which is essentially printing money, it would lead to inflation. But what happened was while the Fed printed money, at the same time they raised the capital and reserve requirements in banks.

So the money sort of recycled. The Fed bought Treasuries, created money, which wound up in the banks and then was redeposited at the Fed. And the money never really entered the money supply. So it wasn’t inflationary. However, this time it has entered the money supply. The money supply was up about 25% last year and the best indicator of inflation is money supply. So I think we have inflation coming well in excess of what the current expectations are. (…)

")

{kind=link}

{kind=link}

{kind=link}