FLASH PMIs

US private sector businesses indicated a strong upturn in output at the end of 2021, despite the rate of expansion easing to the slowest for three months. Service sector business activity growth remained especially sharp, with manufacturers registering a slight uptick in the pace of expansion in production.

Adjusted for seasonal factors, the IHS Markit Flash US Composite PMI Output Index posted 56.9 in December, down slightly from 57.2 in November, but still signalling a strong rise in private sector business activity. Although slower than rates seen earlier in the year, the pace of output growth was faster than the historic trend.

Supporting the upturn in activity was a quicker increase in new orders during December. The pace of expansion was the sharpest for five months, and largely driven by a faster rise in service sector new business. New order inflows to the manufacturing sector eased to the slowest since October 2020, however. Meanwhile, new export orders increased at the strongest pace since September.

At the same time, inflationary pressures continued to mount, with firms facing ever increasing input prices. The pace of cost inflation accelerated again to reach a fresh series record. Companies reported broad-based upticks in cost burdens, with a range of key materials noted higher in price, alongside soaring transportation and distribution fees.

Despite the increase in costs, the pace of inflation of prices charged for goods and services softened for the second month running in December, with some firms mentioning efforts to boost sales amid stronger competition. With the exception of rates seen in October and November, the latest uptick in selling prices was nevertheless the fastest on record (since October 2009).

Ongoing disruptions to supply chains and labor shortages hampered firms’ ability to work through outstanding business at the end of 2021. The expansion in backlogs of work was among the fastest in the series’ history. Challenges securing suitable candidates and retaining staff led to only a marginal rise in employment, which served to exacerbate pressures on capacity. Staffing difficulties were especially acute in the service sector, which drove the slowdown in job creation.

Private sector firms recorded the strongest degree of confidence regarding the 12-month outlook for output for just over a year in December. Optimism stemmed from hopes of further upticks in client demand and that the impact of the Omicron variant is less severe than prior virus waves.

The seasonally adjusted IHS Markit Flash US Services PMI™ Business Activity Index fell to 57.5 in December, down slightly from 58.0 in November. The upturn in business activity remained sharp despite slowing to a three-month low as demand conditions strengthened at the end of the year. The pace of new business growth accelerated to the fastest for five months. Foreign client demand also rose.

Employment growth slowed to the softest for three months in December, as pressure on capacity remained substantial. Subsequently, backlogs of work rose at the third-fastest pace on record.

Labor and input shortages, alongside greater distribution costs, led to the steepest increase in input prices on record in December. Output charges rose at the second-sharpest pace in the series history despite some reports of greater competition for clients.

Meanwhile, business expectations for the year ahead improved to the strongest since November 2020. Hopes of new client acquisitions and greater inflows of new orders reportedly drove optimism.

Operating conditions improved in December, as highlighted by the IHS Markit Flash US Manufacturing Purchasing Managers’ Index™ (PMI™) posting at 57.8 in December, down from 58.3 in November. That said, the health of the sector improved at the slowest pace for a year as output growth remained subdued. The headline index is also continuing to reflect a severe deterioration in input delivery times, with longer supplier lead times ordinarily signalling a stronger sector performance.

Although the pace of output growth quickened to the fastest for three months in December, the rate of expansion was muted compared to those seen earlier in the year as material shortages – although easing to the lowest since May, as measured by suppliers’ delivery times – hampered production again. An inability to source components also weighed on demand as clients reportedly worked through their existing stocks of goods.

Despite supply chain delays moderating markedly during the month, a further overall deterioration in vendor performance led to another substantial increase in backlogs of work in December. The rate of job creation quickened to the fastest since June, but numerous panellists stated that problems finding and retaining staff persisted.

At the same time, the rate of cost inflation softened to the slowest for seven months at the end of 2021. That said, input prices continued to rise at a marked pace, offering firms little respite from inflationary pressure. Greater transportation, distribution and material costs were commonly mentioned. Output charges also rose sharply, albeit at the softest rate since April. Firms continued to note the partial pass-through of costs to clients.

Finally, output expectations for the year ahead were the greatest for four months in December, amid hopes of smoother supply flows in 2022.

The pace of eurozone economic growth slowed in December as rising COVID-19 infection rates hit service sector activity, offsetting improved manufacturing growth amid alleviating supply delays. Firms’ costs and average selling prices continued to rise sharply, though rates of increased cooled from November’s record highs.

Business optimism meanwhile remained resilient despite rising virus case numbers, helping to sustain a solid, albeit weakened, rate of jobs growth across the region. Companies looked to pandemic-related disruptions easing over the course of 2022, most notably in relation to supply chains.

The headline IHS Markit Eurozone Composite PMI® dropped two points from 55.4 in November to 53.4 in December, according to the ‘flash’ reading*, indicating an easing in the rate of output growth to the lowest since March. The decline takes the average reading for the fourth quarter to 54.3, substantially lower than the 58.4 average seen in the third quarter. As such the PMI data point to a marked weakening of economic growth in the closing quarter of 2021, albeit with the rate of growth remaining above the survey’s pre-pandemic long-run average of 53.0.

The December slowdown was led by the service sector, where business activity grew at the weakest rate since April. Slower service sector activity growth was in turn led by a steep fall in tourism and recreation activity of a similar magnitude to the declines seen at the start of the year amid rising COVID-19 infection rates and associated restrictions across the region. Inflows of new business into the service sector also slowed, dropping to the lowest since the recovery from early-2021 lockdowns began in May.

Manufacturing output growth meanwhile picked up, the factory sector outpacing services for the first time in five months, yet remaining well below rates of expansion seen earlier in the year. Despite manufacturers reporting a weakening of new order growth, December saw the largest expansion of production since September thanks to an easing of supply constraints.

Although supply chain delays continued to run far higher than anything seen prior to the pandemic, the lengthening of delivery times in December was the least marked since January. Input buying consequently rose at the fastest pace since August and pre-production inventories grew at a rate unprecedented in more than two decades of survey history, facilitating higher output in many firms.

By country, growth stalled in Germany due to the first drop in new orders for goods and services since June 2020, ending a 17-month recovery. A renewed fall in service sector activity outweighed a pick-up in manufacturing production growth.

France meanwhile continued to grow at a solid pace, albeit down on November, as a relatively resilient service sector helped offset a decline in manufacturing output for the second time in the past three months.

The rest of the region recorded the slowest expansion since April, with growth moderating in both manufacturing and services, though rates of increase remained well above long-run averages.

Inflationary pressures meanwhile cooled, attributable in part to the easing of supply constraints recorded during December. However, although input costs and average selling prices measured across both manufacturing and services both grew less steeply than in November, both series still showed the second-fastest rates of increase recorded in the history of the survey. Companies reported that higher shipping costs, rising energy prices and increases in staff costs again added to the upward pressure on prices.

Employment growth remained solid but slowed to a three-month low amid the easing of new business growth seen during the month. Hiring trends varied by sector and country: the strongest manufacturing jobs gain for four months helped to counteract the weakest rate of service sector job creation since May, with the latter hit harder by the resurgent COVID-19 worries. The strongest pace of hiring was meanwhile seen in Germany followed by France and then the rest of the region as a whole.

Finally, future output expectations improved marginally, in part due to hopes of further supply improvements, though remained the second-lowest since January due to worries about the lingering detrimental impact of COVID-19. Optimism about the year ahead picked up in Germany but worsened in France and on average in the rest of the region.

Japan: Softer increase in private sector output in December

The headline au Jibun Bank Flash Japan Manufacturing Purchasing Managers’ Index™ (PMI)® posted 54.2 in December, down slightly from 54.5 in November, to signal a

further solid improvement in business conditions. Manufacturers registered softer, but still solid, increases in output and new work. Concurrently, the rate of job creation hit a 32-month high amid a steeper increase in backlogs. Shortages of inputs contributed to a further rapid rise in costs, however, and business confidence softened.

At 51.1 in December, the au Jibun Bank Flash Japan Services Business Activity Index slipped from a 27-month high of 53.0 in November and pointed to a marginal increase in services output. New business inflows also expanded at a softer pace. Staffing levels meanwhile fell for the second month in a row, as sentiment around the year ahead eased to the lowest since August. Cost pressures continued to build, with the rate of input price inflation accelerating for the fourth month running to its highest since August 2008. Prices charged rose at the quickest pace since October 2019.

“Really Strong”, Really?

Traders bet Fed will not raise rates as aggressively as forecast Markets dismiss central bank guidance amid investor uncertainty over US economic prospects

The NY Fed’s Business Leaders Survey

Covering service firms in New York, northern New Jersey, and southwestern Connecticut

Survey responses were collected between December 2 and December 9

(…) Business activity in the region’s service sector grew modestly for a fourth consecutive month, according to the December survey. (…) The business climate index

remained negative at -16.3, indicating that on net, firms continued to view the business climate as worse than normal for this time of year.(…) the employment index was little changed at 18.4, pointing to ongoing moderate increases in employment levels, and the wages index came in at 52.3, signaling

another month of strong wage growth. (…)

Not “really strong”, at least in the NY area, Mr. Powell.

To a supplemental survey question:

Businesses Report Sharp Acceleration in Most Costs

(…) In the current survey, far more businesses reported that supply disruptions had worsened over the past month than reported improvement: specifically, 40 percent of service firms and 60 percent of manufactures reported that the availability of supplies had worsened over the past month, while fewer than 5 percent in both groups said it had improved. Still, these results were somewhat less negative than in November.

Looking ahead to the next month, a majority of service-sector firms predicted that the availability of supplies would not change, while nearly twice as many projected that availability would worsen (25 percent) as said it would improve (13 percent). Among manufacturers, 46 percent of businesses said they expect conditions to worsen, while just 9 percent predicted improvement.

On the issue of input prices, the average service firm reported that the prices they paid in 2021 for labor, materials, and other inputs combined rose by 7 percent, and the average manufacturer indicated a corresponding hike of just over 10 percent.

This result contrasts dramatically with the respective average price hikes of 1.8 and 3.0 percent in 2020 indicated in last December’s survey. It also far exceeds the increases that businesses had expected to see in 2021—3.8 percent and 3.3 percent, respectively—based on that earlier survey.

Looking ahead to 2022, service-sector respondents foresee their input prices rising by nearly 8 percent, while manufacturers expect prices to rise by nearly 10 percent, on average.

For wages, both service firms and manufacturers reported an average increase of nearly 6 percent during 2021—roughly double what had been expected in last December’s survey. Looking ahead to 2022, both groups projected that wages would increase by the same percentage. Employee benefits were reported to have risen by just under 5 percent, on average, but were expected to rise by 6-7 percent in 2022.

(…) The one expense category where prices barely increased was rent, where the average hike was just 1 percent; modest increases are also expected for 2022. Businesses reported significantly steeper price increases for almost all of the expense categories than in last December’s survey. ■

U.S. Industrial Production Increases Moderately in November

Industrial production increased 0.5% (5.3% y/y) during November following a 1.7% October rise, revised from 1.6%. Motor vehicle parts shortages and recovery from Hurricane Ida affected production last month. A 0.7% rise had been expected in the Action Economics Forecast Survey. Manufacturing output rose 0.7% last month (4.6% y/y) following a 1.4% increase during October, revised from 1.2%.

Durable goods production rose 0.8% (4.9% y/y) last month after a 1.4% October gain. Motor vehicle production rose 2.2% (-5.4% y/y) following a 10.1% rise. Excluding the motor vehicle sector, factory output rose 0.6% (5.5% y/y) after a 0.8% gain. Elsewhere in the durable goods sector, high-tech product production rose 0.7% (6.3% y/y) after a 0.3% rise in October. (…)

U.S. Housing Starts Improve Sharply in November

Housing starts rose 11.8% (8.3% y/y) during November to 1.679 million units (SAAR) from 1.502 million in October, revised from 1.520 million. It was the highest level of housing starts since March. A November level of 1.570 million starts had been expected in the Action Economics Forecast Survey.

The rise in starts overall in November reflected an 11.3% gain (-0.8% y/y) in single-family starts to 1.173 million. The increase was to the highest level since March and followed four consecutive months of decline. Starts of multi-family homes improved 12.9% (37.1% y/y) to 506,000, the highest level since February 2020.

Building permits increased 3.6% (0.9% y/y) to 1.712 million from 1.653 million in October, revised from 1.650 million. It was the highest level of permits in three months. Permits to build single-family homes gained 2.7% (-4.5% y/y) to 1.103 million. Permits to build multi-family homes rose 5.2% (12.6% y/y) in November to 609,000.

The Great Central Bank Divide As inflation goes global, monetary maestros go their separate ways.

(…) One question: Don’t these people talk to each other? This week has seen a widening gap in monetary management in the world’s largest economies, with the potential for trouble down the road. (…)

Investors had thought (or hoped) the omicron Covid variant might derail the BoE’s plans, but Governor Andrew Bailey thinks inflation is the bigger worry.

Not so in Frankfurt, where the European Central Bank is the most dovish. (…) The ECB’s negative policy rate, of minus-0.5%, will linger until QE ends (if it ever does).

Compared to these two, Fed Chairman Jerome Powell is trying to split the baby. He announced Wednesday an accelerated taper of pandemic QE while talking up future rate increases that may or may not ever happen.

The message is that each major monetary area is on its own, though a conspicuous feature of the current inflation is that it’s everywhere. (…)

The lack of a coordinated response to a common problem will make it harder to control mounting economic risks. One worry is exchange rates. (…) Expect more currency instability if central banks diverge further. (…)

Diverging monetary policies may also have unpredictable effects on capital flows. While a stronger British pound will reduce import prices, bigger capital inflows may swell asset prices or create inflationary pressure. These complex factors increase the risk of policy mistakes and financial instability. (…)

Their [central banks’] gamble this week is that each can chart and travel its own path. That’s a new economic risk on top of inflation and the pandemic.

Bank of Mexico Accelerates Interest-Rate Increases The Bank of Mexico stepped up the pace of interest-rate increases Thursday after inflation reached a more than 20-year high, prompting the bank to raise its inflation forecasts for this year and next.

Japan’s Central Bank Shuns Tightening Trend, Citing Lack of Inflation Japanese consumers have seen little of the price pressures hitting Americans, with overall consumer prices rising just 0.1% in October compared with the same month a year earlier.

Energy Crisis in Europe Intensifies With Russian Troops on Ukraine Border Cold weather and fear of a Russian invasion of Ukraine send natural-gas prices into overdrive

(…) Cold-weather forecasts launched natural-gas prices to record highs this week and propelled electricity markets to levels rarely experienced in Germany, France and the U.K.

The chances of a gusher of Russian gas arriving to swell depleted supplies by spring, meanwhile, are fading, after Moscow massed troops on its western flank. U.S. officials say the deployment could pave the way for an invasion of Ukraine in early 2022.

Benchmark European gas prices are more than seven times as high as a year ago at 127.77 euros ($144) a megawatt-hour, having jumped by more than a quarter over the past week. In a sign that traders expect the shortfall to last for months, prices for contracts that expire deep into 2022 have shot up alongside those that require imminent delivery of gas.

A prolonged spell of higher energy prices will further complicate the picture on inflation and cloud prospects for economic growth. (…)

The shortfall in Europe contrasts with the U.S., where mild weather sent gas prices down by a third this quarter. (…)

Early winter storms have covered central and Eastern Europe with snow and forecasts project frigid temperatures ahead. Yet the prospects of additional fuel coming from Russia, the continent’s main gas supplier, are dim. Nord Stream 2, a controversial pipeline that circumvents U.S. allies Ukraine and Poland by sending gas straight to Germany, is complete but can’t be used before it gets approval from German and European regulators.

German regulators paused the certification process on the roughly 750-mile pipeline that runs under the Baltic Sea in November. U.S. Secretary of State Antony Blinken this week described Nord Stream 2 as a “source of leverage” for the U.S. in efforts to deter Russia from invading Ukraine. (…)

- Fertilizer Costs Push Farms to Raise Prices Higher prices for commodities like corn would further inflate prices cereal, cooking oil, beef and other meat

(…) The price of phosphorus-based fertilizers ranges between roughly $830 to $920 a ton, up from between $450 and $500 a ton at this time last year, according to agricultural research firm DTN. Anhydrous ammonia, which helps convert nitrogen into a form usable for plants, is assessed at more than $1,300 a ton, up 18% in the past month and an all-time high, DTN said. Other popular forms of fertilizer, such as potash and urea, are more than double what they cost last year, according to DTN. (…)

The potential for higher fertilizer costs to cut into production of corn and other crops could fuel continued food-price inflation. Food costs have already climbed this year as companies have passed along higher labor, transport and packaging costs. (…)

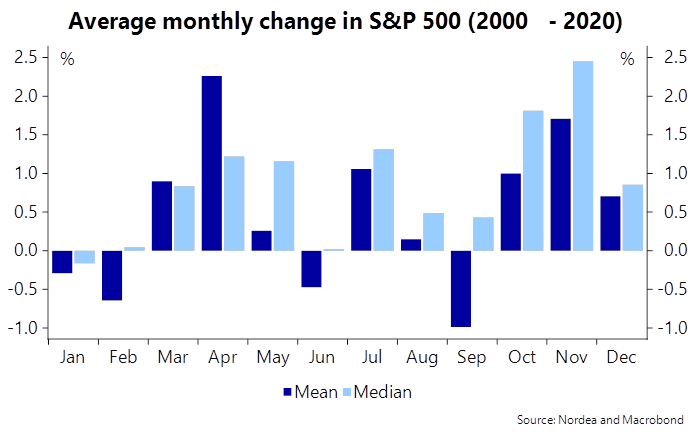

FYI:

Equities have often retreated in January

Omicron Update: Dec 17 Katelyn Jetelina

Well, Omicron cases are growing really fast. Like explosive, skyrocketing, vertical growth fast. If we continue this rate of spread, I would venture to say that there is no modern day virus that has spread this fast and this far ever before.

We continue to see case growth in South Africa, although I’m convinced they’ll hit their peak soon due to several indicators (like test positivity rate and acceleration slowing). While previous waves have averaged 2 months, Omicron will hopefully result in a shorter wave due to high transmissibility and change of behavior.

Omicron in Europe is well on its way. The UK continues to breaks case records. On Wednesday, the UK reported 78,610 new cases—their biggest one-day increase on record. Then, on Thursday they broke that record again and reported 88,376 new cases. France also recorded their biggest one-day increase on record with 65,713 cases. Denmark has the highest case load they’ve ever had. In all of these places, Omicron is largely driving explosive spread, but Delta is still around too. (…)

In the United States, the latest (Dec 14) projection is displayed below. Given CDC estimated 2.9% Omicron cases on Dec 11, which was up from 0.4% on Dec 4, models suggest that Omicron will start spiking case rates between Christmas and New Years. On a national level, we will probably peak in the second week of January. (…)

But Omicron in areas like New York is well on its way. New York/New Jersey has the highest proportion of Omicron cases in the United States (13%). We are starting to see the impact of this already. Yesterday New York reported 18,276 cases- their biggest one-day increase since January 2021. 8,318 are in New York City alone.

(…) even the vaccinated (especially those with only two doses) will get infected and spread the virus. (…)

It’s essential that we remain out of the hospital. Immunity has positively and drastically impacted hospitalizations prior to Omicron. Below is a graph from the UK showing the fanning effect: cases differentiated from hospitalizations and deaths after vaccines were rolled out.

For those without a booster, the first line of defense is down: neutralizing antibodies aren’t going prevent infection nor transmission of Omicron. However, T-cells should still keep a lot of people out of the hospital.

Those with boosters will be most protected. That’s because boosters restimulate the immune system and increase the number of antibodies. The more antibodies we have, the more they can find the the limited landing spots on Omicron. This will decrease breakthrough cases and decrease transmission.

Boosters also generate a much broader level of immunity. In other words, boosters develop antibodies against more parts of the virus than the primary series. (…)

We are seeing hospitalizations and deaths increase in South Africa, but they are at lower rates than before. In Gauteng— South Africa’s epicenter— hospitalizations are about 45% than what they were for Delta. Excess deaths are now gaining speed, but still much lower than before. On a national or global scale, a small percentage can add up quickly when we are talking about an incredibly fast moving virus.

I am increasingly concerned about older adults. Earlier this week, the Kaiser Family Foundation released a report describing severe breakthrough cases in the United States. They found that more than two-thirds (69%) of breakthrough COVID-19 hospitalizations occurred among people ages 65 and older. Given that only 52% of Americans 65+ have a booster, this population is going to have a lot of breakthrough cases. And I really hope they don’t also end up at the hospital.

South Africa continues to report a higher rate of hospitalizations among the 0-4 year old group. A few days ago we got an update from a hospital— kids have a 20% higher rate of hospitalizations with Omicron compared to Delta.

The hospital gave important context though: “Incidental COVID19 diagnoses among children exceeded COVID19 specific admissions.” In other words, more children are hospitalized “with COVID19” (e.g. injury and test positive) than “for COVID19” (i.e. SARS-CoV-2 taking over the body). So the increase in admissions is likely reflective of high community transmission. I don’t know if this is necessarily good news, but it’s not bad news either.

Case counts are going to get very high. As high as our testing capacity can take. While the severity of disease is reduced (due to immunity or intrinsic changes, we don’t know), the mere number of infections will increase hospitalizations.

Please use a layered approach this holiday season. There are still 75 million Americans relying on the “herd” to protect them through no choice of their own. While your individual risk may be low, Omicron presents significant societal risk.

- Americans rush for vaccine boosters ahead of Omicron wave Pharmacy chains struggle with record demand as waiting times for jabs stretch to two weeks

South Africa Hospitalization Rate Plunges in Omicron Wave

South Africa delivered some positive news on the omicron coronavirus variant on Friday, reporting a much lower rate of hospital admissions and signs that the wave of infections may be peaking.

Only 1.7% of identified Covid-19 cases were admitted to hospital in the second week of infections in the fourth wave, compared with 19% in the same week of the third delta-driven wave, South African Health Minister Joe Phaahla said at a press conference.

Health officials presented evidence that the strain may be milder, and that infections may already be peaking in the country’s most populous province, Gauteng.

Still, new cases in that week of the current wave were more than 20,000 a day, compared with 4,400 in the same week of the third wave. That’s further evidence of omicron’s rapid transmissibility, which a number of other countries, such as the U.K., are also now experiencing.

Scientists have cautioned that other nations may have a different experience to South Africa as the country’s population is young compared with developed nations. Between 70% and 80% of citizens may also have had a prior Covid-19 infection, according to antibody surveys, meaning they could have some level of protection.

Currently there are about 7,600 people with Covid-19 in South African hospitals, about 40% of the peak in the second and third waves. Excess deaths, a measure of the number of deaths against a historical average, are just below 2,000 a week, an eighth of their previous peak. )…)

“We have seen a decrease in a proportion of people who need to be on oxygen. They are at very low levels,” said Waasila Jassat, a researcher with the NICD. “For the first time there are more non-severe than severe patients in hospital.”

![]() A Bloomberg News investigation has found a key piece of evidence underpinning U.S. suspicions of Chinese spying using Huawei Technologies Co. as a conduit — a previously unreported breach that occurred halfway around the world nearly a decade ago. The news could harden resolve in Washington as it considers tougher sanctions on Semiconductor Manufacturing International Corp., China’s largest chipmaker.

A Bloomberg News investigation has found a key piece of evidence underpinning U.S. suspicions of Chinese spying using Huawei Technologies Co. as a conduit — a previously unreported breach that occurred halfway around the world nearly a decade ago. The news could harden resolve in Washington as it considers tougher sanctions on Semiconductor Manufacturing International Corp., China’s largest chipmaker.

")

")

")

")