U.S. Jobless Claims Fall to Five-Month Low Applications for unemployment benefits have fallen below the prepandemic average as employers hold on to workers in a tight labor market

This chart shows unemployment claims with the scale set to reflect levels between 2014 and 2019. The horizontal line is the average for that period. The low in claims was in March.

- Why Are Companies Still Hiring When GDP Is Shrinking? A persistent economic puzzle is why the labor market is still strong amid slowing growth and high inflation. Many employers say they continue to struggle with staffing shortages and are reluctant to cut head count.

(…) Layoffs and other involuntary discharges, at 1.4 million in July, were about 20% below their average monthly level in 2019, when GDP was growing more quickly. (…)

“Inflation is a challenge, but we can measure it. We can work to overcome it. Not having enough people in the supply chain—that has proven to be much more difficult,” [Raytheon] chief executive Greg Hayes told analysts this summer. “The only thing that’s going to solve labor availability, I hate to say this, is a slowdown in the economy because right now, there just simply aren’t enough people in the workforce for all of our suppliers.” (…)

But even employers not seeking to raise head count have to keep hiring to fill vacancies caused by historically high rates of turnover. In July, 2.7% of workers quit their jobs, up from 2.3% in February 2020, when the jobless rate matched a half-century low. (…)

“We just keep hiring and replacing, hiring and replacing—wash, rinse, repeat,” said Ms. Henry. “Efficiency goes to hell when you continuously hire since the person who is training them isn’t going at their normal pace because they’re stopping to explain things,” she said. Many new hires leave before that training yields return, she added. (…)

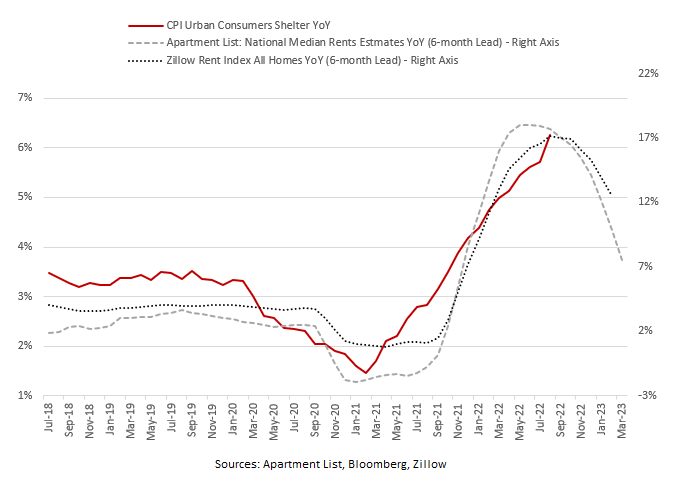

Construction industry layoffs are still below prepandemic levels, though new home sales have fallen sharply this year and housing starts have dropped because of higher mortgage rates. Residential builders are struggling with the legacy of job cuts undertaken during the housing crisis of 2007-09, with employment in residential construction 12% below its 2006 peak. (…)

The Fed’s concern on employment is about wages so it wants to reduce job openings to ease the pressure. According to the Atlanta Fed’s wage tracker, wage growth in the last 12 months was highest in Leisure and Hospitality (6.3%), Trade & Transportation (6.2%) and Manufacturing 5.9%) vs the U.S. average of 5.5%. These sectors have not shown much slowdown in their respective openings compared with their pre-pandemic levels.

On the other hand, the unemployment rate in Leisure and Hospitality is 6.1% while it is 4.3% in Trade & Transportation. Manufacturing is at 3.3%, below the national average of 3.8%.

U.S. GDP Growth is Unrevised in Q2’22, Posting Second Straight Quarterly Decline

Real GDP growth during Q2’22 was unrevised at -0.6% (+1.8% y/y) after declining an unrevised 1.6% in Q1. The latest figure matched expectations in the Action Economics Forecast Survey. GDP increased at a 2.1% annual rate from 2016 to 2021, up 0.2 percentage points from the earlier estimate.

The Q2 gain in corporate profits after-tax was revised up to 7.4% (7.7% y/y) from 6.1%. Domestic nonfinancial profits rose 7.9% (9.8% y/y). Financial sector earnings declined 9.0% (-10.2% y/y) while foreign sector profits rose 5.8% (21.8% y/y).

Real personal consumption expenditure growth last quarter was revised up to 2.0% (2.4% y/y) from 1.5%. Durable goods outlays fell 2.8% (-3.7% y/y) while nondurable spending declined 2.4% (-1.1% y/y). Services outlays rose 4.6% (4.8% y/y). Business fixed investment growth was revised lower to 0.1% (2.4% y/y). Residential investment declined 17.8% (-7.2% y/y), revised from -16.2%.

Government spending fell 1.6% (-1.3% y/y) last quarter, revised from -1.8%. Federal government spending declined 3.4% (-4.0% y/y), revised from -1.9%. Defense spending rose 1.5% (-3.9% y/y). State & local government spending weakened 0.6% (+0.5% y/y).

The contribution of inventory investment was revised minimally to a 1.9 percentage point subtraction from GDP growth. (…)

The GDP price index was revised higher to 9.0% (7.6% y/y) from 8.9%. This remained the fastest pace of GDP price inflation since Q1’81. The rise in the PCE price Index was revised to 7.3% (6.6% y/y) from 7.1%. The PCE price index less food & energy increased 4.7% (5.0% y/y), revised from 4.4%, and has risen at about that rate for roughly a year. (…)

The WSJ has this important info :

The report, which included five years of benchmark revisions, also revised downward gross domestic income—a measure of corporate profits, wages and benefits, self-employment income, interest and rent—to a 0.1% increase in the second quarter. That largely closed a gap between output and income that had pointed to a stalling economy rather than a recession.

But Axios did the digging to explain:

One driver behind the downward GDI revision was slower labor compensation than initially reported. In other words, worker wage growth wasn’t as hot as we thought.

In Q1, inflation-adjusted GDI increased by 0.8%, lower than the initial estimate of 1.8%. The latest estimate of Q2 GDI shows it increased 0.1%, not the 1.4% the government first reported.

For 2021, the change in GDI was revised down, while GDP was revised up slightly. That brings the gap between the measures to -0.6% last year. That’s a much more normal discrepancy than the -2.3% gap previously reported.

Nike warns of inventory glut, price cuts (CNBC)

Mortgage Rates Rise to 6.7%, Highest Since 2007 Mortgage rates are more than double where they were a year ago, adding pressure to the already cooling U.S. housing market.

(Haver Analytics)

(Haver Analytics)

Homes in Canada Have Never Been So Unaffordable, RBC Says

- CMHC Cuts Home-Price Outlook, Projecting Drop as Deep as 15%

- “Our G10 home price model suggests sizable nominal home prices declines from the peak of around 15% in Canada, 5-10% in the US, and under 5% in the UK. The declines are larger for real home prices at just over 20% in Canada, just over 10% in the US, and 10% in the UK.” We view the risks to these estimates as tilted to the downside because of a sharp deterioration in our descriptive home price outlook scores and evidence of strong mean reversion in regional data. (Goldman Sachs)

China’s Service Sector Slows in Latest Economic Warning Sign Chinese economic activity remained feeble, with the services sector slipping into contraction, offering fresh evidence of the damage that Beijing’s Covid-prevention measures and a real estate slide are inflicting on the economy.

(…) A subindex measuring the services sector fell to 48.9 in September from 51.9 the previous month, China’s National Bureau of Statistics reported Friday. The poor performance in the services sector dragged the broader official nonmanufacturing purchasing managers index down to 50.6 in September, from 52.6. A reading below 50 indicates contraction. (…)

As of Friday, cities under some form of Covid restrictions accounted for 25% of gross domestic product, down from 28% a week earlier, according to Goldman Sachs. (…)

The official manufacturing purchasing managers index ticked up to 50.1 in September from 49.4 the previous month, according to official data. The reading followed two consecutive months of contraction. (…)

A subindex of the official manufacturing PMI tracking new export orders showed overseas demand continuing to weaken in September. The subindex slipped to 47, the lowest level in four months, the data showed.

Separate data released on Friday by Caixin Media Co. and S&P Global, focused on smaller-scale and private-sector manufacturers, pointed to weaker factory activity as new orders contracted for a second straight month. The China Caixin manufacturing purchasing managers index fell to 48.1 in September from 49.5 a month earlier. (…)

On Thursday, China’s central bank said it would allow some cities that are suffering from falling home prices to further slash mortgage rates for first-time home buyers, adding to previous administrative measures aimed at stabilizing the faltering market. (…)

Business conditions across China’s manufacturing sector deteriorated modestly in September, as efforts to contain the COVID-19 virus weighed on performance. Total new business dropped for the second month in a row, which led to a renewed fall in output, while firms also trimmed their purchasing activity and inventories. Reduced demand for inputs placed further downward pressure on prices, with input costs falling at the quickest rate since the start of 2016. Companies often looked to pass on any cost savings to clients to help improve sales, which led to the quickest fall in selling prices since December 2015.

The headline seasonally adjusted Purchasing Managers’ Index™ (PMI™) declined from 49.5 in August to 48.1 in September, to signal a back-to-back deterioration in the overall health of the sector. The reading was consistent with only a mild rate of contraction, however.

A key factor driving the headline index lower was a faster fall in new orders during September. New business fell for the second month in a row, and at the quickest rate since April, with panel members often commenting that restrictions around travel and operations had dampened customer demand. Foreign sales also fell again, and at a solid rate that was the fastest for four months. (…)

Eurozone Inflation Hits 10% as Power Suppliers Scramble for Reserves Consumer prices in the currency area are now rising at a much faster pace than in the U.S., with the ECB set for a series of interest rate rises

(…) According to Eurostat, household energy prices were 40.8% higher in September than a year earlier.

The higher energy costs facing most businesses are percolating through the economy. Prices of services were 4.3% higher than a year earlier, driving a pickup in core inflation to 4.8% from 4.3%. (…)

The Organization for Economic Cooperation and Development on Monday said it now expects the average rate of inflation in the eurozone to be 8.1% this year, up from 7% when it last released forecasts in June. In the U.S., it expects average inflation to be 6.2%, up from 5.9% in June. In 2023, it expects eurozone inflation to average 6.2% and U.S. inflation to average 3.4%. (…)

Taiwan Warns Exports to Struggle in Rest of 2022 as Demand Slows

(…) Growth in overseas shipments might slump to single-digits in the fourth quarter of 2022, Su said in an interview in Manila on Friday. (…)

August export growth slowed to just 2%, the slowest pace in more than two years, prompting Ministry of Finance chief statistician Beatrice Tsai to warn at the time that “winter is coming” earlier than expected. She also cautioned that September exports could even shrink by as much as 3% from a year earlier.

Export orders have also slowed. While orders gained 2% in August, reversing a decline in July, purchases from China and Hong Kong fell more than 25% last month. Almost 40% of Taiwan’s exports went to Hong Kong and China for the first eight months of the year, data from the finance ministry showed. (…)

![]() According to Garry Evans, Chief Strategist, Global Asset Allocation at BCA Research, the current trend in the business cycle indicates that global earnings growth will slow into negative territory by January 2023, and continue further into May 2023.

According to Garry Evans, Chief Strategist, Global Asset Allocation at BCA Research, the current trend in the business cycle indicates that global earnings growth will slow into negative territory by January 2023, and continue further into May 2023.

SENTIMENT WATCH

Investors dump global bond and equity funds on recession risks

Global bond and equity funds witnessed massive outflows in the week ended Sept. 28 as worries about a recession grew, with the U.S. Federal Reserve determined to keep interest rates higher to tame inflation pressure. (…)

Investors offloaded a net $22.07 billion worth of global bond funds, in their biggest such weekly net sales since June. 22, data from Refinitiv Lipper showed.

John Authers: Gatsby, the Dollar, and Staring Blankly at the World Falling Apart

(…) The dollar has never regained its pre-Plaza highs from early 1985. But now, wishful thoughts are returning to the Plaza Accord once more. As the chart shows, the dollar is still far below its 1985 high in nominal terms. On a real effective basis, taking account of inflation, Citibank’s index show that it is almost back to its high since inception in 1989, after the accord was reached. (…)

Interventions by three of the four largest economies outside the US in the space of a week show that the dollar’s strength is beginning to cause real stress. But there are at least two sides to any currency trade, and no meaningful limit to the dollar is possible without willing participation by the US. (…)

According to the IIF’s estimates of fair value, the euro and the pound are still overvalued and have further to fall, despite the damage they have already sustained. That might vitiate any Plaza-style attempt to limit the dollar. And it also confirms that this dollar surge is likely to create more pain in western Europe than in the emerging world. (…)

While US inflation is elevated, it seems difficult to countenance why the US would proactively participate in an inflationary dollar policy, and without US participation, we see little chance of success. (…)

We think that policymakers are aware of a hard truth: They don’t have enough FX reserves to make a sustained difference. Back in 1985-87, the last time we had a coordinated intervention to weaken USD, daily FX turnover was near US$200 billion per day (on a net-gross basis) but, as of the last reported BIS figure in 2019, daily turnover is over 40 times higher at US$8.3 trillion per day. The G10 collectively has US$2.8 trillion in FX reserve assets (deposits and securities, so excluding gold). (Morgan Stanley) (…)

China’s Rival Aircraft to Boeing, Airbus Jets Wins Certification China is angling to disrupt the dominance of Boeing and Airbus in commercial jetliner manufacturing. However, it’s not clear when, if ever, the C919 will be a competitive threat to the duopoly. Comac hasn’t attracted much interest for its products overseas, and the nation’s airlines still favor Airbus and Boeing as the workhorses of their fleets.

(…) Comac has said it already has 815 orders from 28 Chinese customers for the C919, though the majority aren’t confirmed and many are from aircraft lessors yet to place the jet with an airline. China’s so-called big three — China Eastern, Air China Ltd. and China Southern Airlines Co. — and Hainan Airlines have 2,241 Boeing and Airbus narrowbody aircraft between them, and at least 546 on order. (…)

For now, the plane will only be allowed to fly within China until it is certified by foreign regulators. (…)

(

(