“Getting into the Zone”

St. Louis Fed President Jim Bullard addressed the question of what is a “sufficiently restrictive” policy rate for the current macroeconomic environment. His approach is based on generous assumptions that tend to favor a more dovish policy. Still, the policy rate isn’t yet in a zone that may be considered sufficiently restrictive, he said.

- Francois Trahan, analyst at Macro Specialist Designation and former Institutional Investor’s all-star strategist:

A pivot would NOT mark the beginning of a new bull market. Surely, a real pivot would give us a nice bounce in equities, but the beginning of a new bull market will have to first start with enduring and pricing in a proper recession. This chart shows that Growth P/Es fell during the Fed tightening cycle of 2004/06, had brief rebound once tightening was done, and then melted even more once EPS began to collapse … and all that fun stuff is ahead of us.

Bear talk

Say what you want about David Rosenberg, he’s a one-handed economist with strong convictions.

Link here.

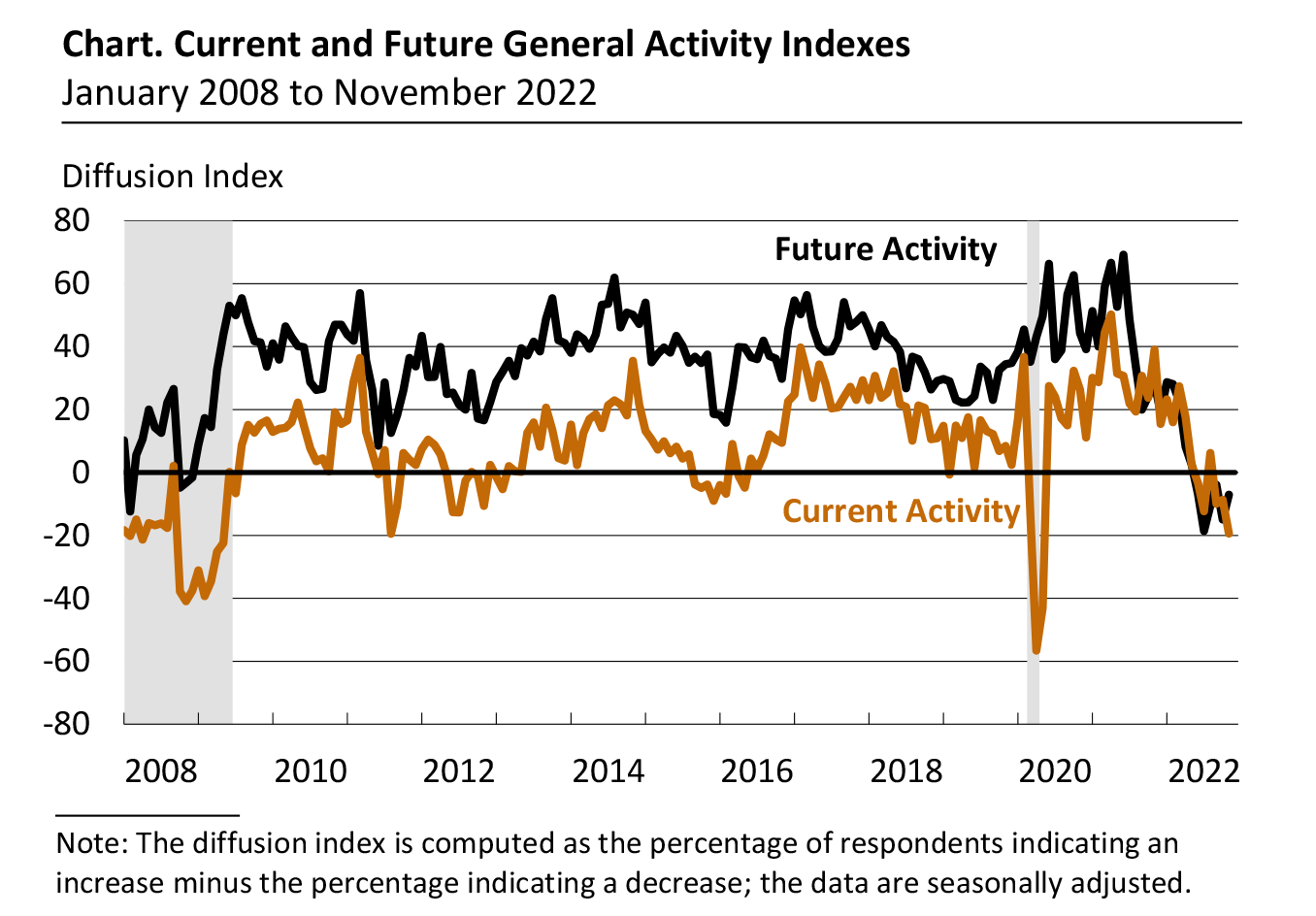

Philly Fed Manufacturing Business Outlook Survey

Manufacturing activity in the region continued to decline, according to the firms responding to the November Manufacturing Business Outlook Survey. The general activity index declined further, the new orders index remained negative, and the shipments index remained positive but low. The employment index declined but continued to suggest overall hiring, and the price indexes continued to suggest overall increases. Although the survey’s future indexes rose slightly, they continued to suggest that the firms expect overall declines in activity and new orders six months from now.

The indexes for prices paid and prices received continue to indicate overall price increases for inputs and the firms’ own goods. The prices paid diffusion index ticked down 1 point to 35.3. Nearly 47 percent of the firms reported increases in input prices, and 12 percent reported decreases; 41 percent reported no change. The current prices received index moved up 4 points to 34.6, its highest reading since June. Almost 38 percent of the firms reported increases in the prices of their own goods, 3 percent reported decreases, and 59 percent reported no change.

In this month’s special questions, the firms were asked to forecast the changes in prices of their own products and for U.S. consumers over the next four quarters. Regarding their own prices over the next year, the firms’ median forecast was for an expected increase of 4.8 percent, down slightly from 5.0 percent when this question was last asked in August. The firms reported a median increase of 7.5 percent in their own prices over the past year, down from 10.0 percent in August. The firms’ median forecast for the rate of inflation for U.S. consumers over the next year was 5.0 percent, down from 6.0 percent in August. Over the long run, the firms’ median forecast for the 10-year average inflation rate was 4.0 percent, up from 3.0 percent in August.

- Kansa City Fed Manufacturing Activity Declined at a Steady Pace

- Gap warned that sales in the fourth quarter might decline in the mid-single digits as economic headwinds persist. (WSJ)

Jobless Claims Fell Slightly Last Week Filings for U.S. unemployment insurance, a proxy for layoffs, remained near historically low levels amid a still-tight labor market.

U.S. Housing Starts Fall Sharply in October

Total housing starts fell 4.2% (-8.8% y/y) during October to 1.425 million (SAAR) from 1.488 million in September, revised from 1.439 million. Starts in August were revised to 1.508 million from 1.566 million. Starts in October were 21.1% lower last month than the April 2022 peak. The Action Economics Forecast Survey expected 1.41 million starts in October.

Single-family starts weakened 6.1% (-20.8% y/y) in October to 855,000 after falling 1.3% to 911,000 in September. Single-family starts were 34.6% below their December 2020 peak. Multi-family starts declined 1.2% (+17.8% y/y) to 570,000 after falling 1.4% in September. They were 9.8% below the April 2022 peak. (…)

Building permits declined 2.4% (-10.1% y/y) during October to 1.526 million after rising 1.4% in September. Single-family permits weakened 3.6% (-22.1% y/y) to 839,000. It was the eighth straight consecutive monthly decline. Multi-family permits eased 1.0% (+10.6% y/y) to 687,000 after rising 8.1% in September.

![]() Housing units under construction are still at an all-time high, as are construction jobs, both at significant risks when these units are completed.

Housing units under construction are still at an all-time high, as are construction jobs, both at significant risks when these units are completed.

Companies Still Boost Capital Spending Despite Higher Rates Capital spending among companies in the S&P 500 in the third quarter is set to top $200 billion even as a potential recession looms.

Capital spending among companies in the S&P 500 in the third quarter is set to top $200 billion, according to S&P Dow Jones Indices, which analyzed data through Monday from roughly 90% of index components. That is on pace for a jump of about 20% from a year earlier, roughly in line with the first and second quarter’s growth rates. (…)

Stock repurchases are on pace for 11% decline in the third quarter from a year earlier at roughly $180 billion, S&P Dow Jones Indices data through Monday show. Dividend payments, which are committed before the quarter begins, rose about 8% to $140 billion. (…)

Total new orders for nondefense capital goods, a proxy for economy-wide capex, is up 8.3% YoY in Q3 while PPI-Industrial commodities is +15.8%.

U.K. Unveils Largest Tax Increases and Spending Cuts in a Decade The U.K. is the first major Western economy to start sharply limiting spending growth after years of fiscal stimulus.

(…) The measures mark a second major shift in U.K. economic policy in just a matter of months, after previous British Prime Minister Liz Truss spooked financial markets by pledging to jump-start growth with tax cuts funded by more borrowing. Her successor, Rishi Sunak, is now taking economic policy in the other direction, trying to convince investors the U.K. is serious about eventually taming rising government debt. His challenge will be to regain market confidence without causing major damage to an economy widely expected to enter a recession.

Chancellor Jeremy Hunt announced £55 billion, equivalent to around $66 billion, of spending cuts and tax increases over the next five years, an attempt to begin lowering the size of government debt relative to the economy from the fiscal year ending March 2028. The bulk of the spending cuts, however, are due to take effect starting in 2025, after the next U.K. general election. (…)

Oaktree’s Marks Sees ‘Great Bargains’ Coming as Recession Looms

(…) Marks predicts US inflation has likely peaked, and expects rates to stay near the 5% mark in the next 5 to 10 years. An accompanying shift in consumer appetite alongside higher borrowing costs will lead to “significant distress” at many companies, he said.

“A year ago the outlook was considered flawless and I think we’re going to reach a point where they consider it hopeless,” he said of investors. “And that’s when you get the big buys. That’s when you get to be a buyer of assets cheap and a maker of loans at high yields with safety.” (…)

Marks said losses for banks on hung bridge loan deals has damaged credit markets. One example was the acquisition of Twitter Inc. Elon Musk saddled the firm with almost $13 billion of debt that’s now in the hands of Wall Street banks struggling to offload it to investors.

After poorly-timed debt sales, the banks have resorted to selling the loans at discounts of as low as 70 cents on the dollar, Bloomberg previously reported.

“Just imagine the magnitude of those losses,” Marks said.

And while corporate America as a whole is not highly levered, the distress is piling up, he said. (…)

“We’ll be looking among the ruins for great bargains.”

German wage settlement points to dampened second-round effects A regional wage agreement in Baden-Wuerttemberg yesterday will pave the way for broader wage developments and shows the European Central Bank that second-round effects will kick in next year but should be dampened

Last night, employers and unions in the metal and electronics industry in Baden-Wuerttemberg reached a new wage agreement. Wages will be increased by 5.2% in June 2023 and by 3.3% in May 2024. There will also be a one-off payment of €3,000, exactly the amount the German government had offered to exempt from tax and social security contributions. While this is “only” a regional wage agreement, it will have knock-on effects on other regional and sectoral wage negotiations. Almost four million people in Germany work in the metal and electronics industry.

Traditionally, there has been a lot of attention on German wage settlements across the eurozone. The takeaway for German wage developments and the risk of second-round effects is that last night’s deal shows what a compromise can look like. It won’t be enough to fully offset the drop in purchasing power caused by higher inflation, but it softens the damage. For the ECB, it signals that second-round effects remain dampened and that a lower, subdued inflationary pressure can last for longer than markets currently think.

China’s New Daily Covid Cases Jump Above 24,000 Guangzhou, the provincial capital of China’s manufacturing powerhouse Guangdong, had the highest tally, with more than 9,000 new cases among its 19 million residents.

China’s central government has laid out preparations to deal with surging Covid-19 infections, while warning local authorities against “irresponsible loosening” of pandemic-control measures.

China would continue to “rectify the practice of excessive measures such as lockdowns, while also opposing irresponsible attitudes and prevent a loosening up,” said Mi Feng, spokesman for China’s National Health Commission during a briefing on Thursday. (…)

Guangzhou, the provincial capital of China’s manufacturing powerhouse Guangdong, had the highest tally, with more than 9,000 new cases among its 19 million residents. (…)

Before stopping the lockdowns, China needs to vaccinate a larger percentage of its population. China has yet to produce a strong and effective vaccine. Senior health officials seemed to be opening the door to BNTX vaccine distributed by Fosun.

China’s top health officials on Thursday stressed enhancing medical resources to upgrade the country’s ability to fight COVID-19 flare-ups, and vowed to push forward the vaccination campaign, two steps epidemiologists believe are needed for further adjustment of anti-epidemic policies. (…)

When asked when BioNTech’s COVID-19 vaccines will be available for the Chinese public, Shen Hongbing, deputy director of the National Administration of Disease Prevention and Control, said that safety, effectiveness, availability and affordability should be considered during vaccination, and China is making plans to speed up its vaccination campaign. (…)

The expert also emphasized strengthening hospital networks and speeding vaccination, especially among vulnerable groups, as local governments’ priorities in addition to virus control. The Chinese mainland should strive to avoid what happened in Hong Kong this year, when the fifth wave took roughly 10,000 lives, so major policy adjustments will not happen until the country is fully prepared, according to the CDC expert. (…)

- ‘We’re not ready’: threat of Covid exit wave stymies China’s reopening Beijing has failed to prepare for an inevitable mass outbreak by focusing on containment, experts say

China, Japan reach consensus on stabilizing, developing bilateral ties, stressing the two sides should ‘be partners, not threats’

HISTORY RHYMES

FTX Didn’t Name Names in Related-Party Transactions The lack of detail in financial statements echoes past scandals including Enron.