The U.S. Consumer Is Starting to Freak Out The flush savings accounts and cheap credit that helped keep Americans spending at high rates since 2020 are disappearing, while inflation remains elevated.

The engine of the U.S. economy—consumer spending—is starting to sputter.

Retail purchases have fallen in three of the past four months. Spending on services, including rent, haircuts and the bulk of bills, was flat in December, after adjusting for inflation, the worst monthly reading in nearly a year. Sales of existing homes in the U.S. fell last year to their lowest level since 2014 as mortgage rates rose. The auto industry posted its worst sales year in more than a decade. (…)

A downshifting consumer is a key reason that business and academic economists polled by The Wall Street Journal, on average, put the probability of a recession in the next 12 months at 61%. However, many economists say, the U.S. might avoid a recession entirely if spending patterns stabilize. (…)

Still, there are signs of labor-market weakness. Employers are shedding temporary workers at a fast rate, and people who lose their jobs are taking longer to find new ones. Meanwhile, the number of hours worked a week has declined for two straight months, according to the Labor Department, resulting in a slowdown in workers’ take-home pay. (…)

Credit-card balances were up 15% on the year in the third quarter, according to the Federal Reserve Bank of New York, the largest increase in more than two decades.

Additionally, tens of millions of Americans are set to start or resume making payments on student loans later this year, after the Supreme Court rules on President Biden’s student-debt cancellation plan. Payments have been frozen since March 2020, and are scheduled to begin again 60 days after litigation is resolved or the program is implemented.

Many taxpayers will get smaller refunds when they file their returns in the coming months because Congress didn’t extend the breaks put in place at the height of the pandemic.

Most Americans who lose their jobs can expect unemployment payments for six months or less, at a fraction of their former paychecks, the same as before pandemic programs kicked in. Pandemic programs allowed Americans to receive unemployment payments for as long as 18 months, and in some cases paid workers more than their paychecks. (…)

The large stock-market declines over the past year also alarmed consumers (…).

- The share of Americans who say they live paycheck-to-paycheck climbed 3% last year, a likely reflection of the growing strain on household budgets. But it’s not just the lowest earners feeling the squeeze. Most of the newcomers were people earning more than $100,000 a year, according to a Pymnts.com and LendingClub survey. It all points to weaker consumer spending in the months ahead. (Bloomberg)

- Important to monitor:

U.S. Gasoline Prices

U.S. Natural Gas Prices

- Banks Brace for More Consumers to Fall Behind on Their Loans Delinquencies are rising, in some cases surpassing prepandemic levels, prompting banks to add to their rainy-day funds.

- U.S. lender Citizens stepping back from auto loans – CEO

(…) “Spreads are tight, so you’re not making a good return on that capital,” he said, adding that there are limited cross-selling opportunities. (…)

“We are being very selective on where we are extending credit given the potential for recession in 2023,” Van Saun said.

Moody’s analyst Warren Kornfeld told Reuters that banks’ auto loan charge-offs now are approaching pre-pandemic levels (…). “We believe that most banks recognize the growing risks in auto lending outside of the super prime segment,” he said. (…)

Fed Debates Whether Wages or Low Unemployment Will Drive Inflation

- U.S. : Demand-driven inflation has vanished (NBF)

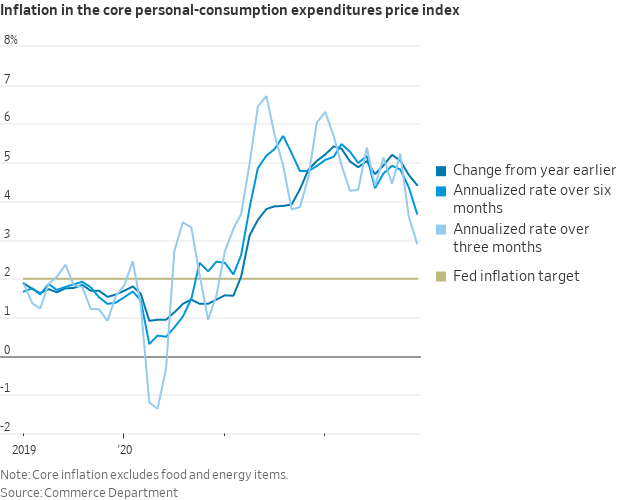

While we eagerly await the Federal Reserve’s interest rate decision this Wednesday, we got crucial developments on the inflation front Friday with December’s reading of Personal Consumption Expenditure (PCE) inflation, the indicator the U.S. central bank targets according to its official mandate.

The San Francisco Fed has developed a methodology to decompose PCE inflation into supply and demand components a few months ago, and the December decomposition has plenty to raise eyebrows.

As today’s Hot Chart shows, demand has been a negative contributor to U.S. inflation for two consecutive months now, a first since the initial pandemic shock. This development is consistent with volume consumption, which also recorded a second consecutive monthly decline in December, a first during this expansion.

China’s recent announcement to end its zero-covid policy and reopen its economy argues for a fading contribution from supply-driven inflation in the months ahead. With a resurgence in deflationary forces, we are confident that inflation will continue to come down faster than what is currently assumed by the Fed.

What about the situation in Canada? In a report published last week, we used the methodology developed by the San Francisco Fed to evaluate the situation in our country and we noted the absence of demand-driven inflationary pressures in headline PCE in the third quarter, and a fading contribution of demand on the core figure.

Despite 2022’s slew of interest-rate hikes from Chair Powell and colleagues, financial conditions are the loosest since last February as investors bet fading inflation will allow the central bank to soon cease raising borrowing costs and then cut them later this year.

That’s likely wishful thinking as far as Powell is concerned and he has a clear incentive to push back against the trade given rising stocks and bonds could fan the very price pressures he wants to restrain.

Such a backdrop means Powell is expected to balance this week’s likely 25 basis-point increase in rates with a stern message that the step down in size from the past six hikes doesn’t diminish his commitment to reducing inflation to 2%. It stood at 5% in December. He may even be willing to roil the upbeat markets if that’s what it takes to make his point.

(…) financial conditions are now looser than in March when policymakers began to raise rates, and minutes of their December meeting show that this was already on their minds. Officials noted that an “unwarranted” easing in conditions would complicate their task of restoring price stability.

Dallas Fed President Lorie Logan, speaking on Jan. 18, cautioned that policy could respond if financial conditions ease further in response to a slower pace of rate increases.

“If that happens, we can offset the effect by gradually raising rates to a higher level than previously expected,” she said. (…)

Euro zone banks tighten credit by most since debt crisis, ECB says

(…) But demand for loans from enterprises and households also fell for the same reasons, with the drop in demand for mortgages the biggest on record, the ECB’s quarterly Bank Lending Survey showed. (…)

A net 26% of banks polled by the ECB said they made their standards stricter for approving loans to companies in the final quarter of last year, the biggest tightening since 2011.

Banks also restricted access to consumer credit and mortgages, a trend that banks expect to continue this quarter. (…)

IMF Upgrades Outlook for Global Economy Easing inflation and China’s reopening should allow the global economy to grow a bit faster than previously expected, the international lender said.

In its latest World Economic Outlook, released Monday Washington time, the IMF sees the global economy growing 2.9% this year, up from its October projection of 2.7%. The IMF expects growth to accelerate to 3.1.% in 2024, still less than last year’s 3.4%. (…)

“With a global growth rate at 2.9%, we are well away from any sort of global recession marker,” Mr. Gourinchas said during a press briefing. Nonetheless, he warned of downside risks to the outlook, such as rebounding inflation and the war in Ukraine.

Several developments in the past few months contributed to the shift in the IMF’s views, its economists explained. Economic growth proved surprisingly resilient in the third quarter of last year, helped by tight labor markets, stronger-than-expected spending by households and businesses, and Europe’s swift adaptation to the energy crisis caused by the war in Ukraine. (…)

China’s economy is projected to expand 5.2% this year, up from 3% in 2022, and significantly faster than the 4.4% expansion the IMF had projected in October. (…)

Emerging market and developing economies are leading the improved global outlook. Their growth is projected at 4% this year and 4.2% in 2024, compared with 3.9% in 2022. (…)

U.S. growth is expected to slow from 2% in 2022 to 1.4% this year and 1% next year. Euro-area growth is expected to decelerate from 3.5% last year to 0.7% this year, before rebounding to 1.6% in 2024. The U.K., after putting in solid 4.1% growth last year, will see its economy contract 0.6% this year. It is the only major advanced economy the IMF expects to experience negative growth. (…)

The World Bank, the IMF’s sister organization, is more cautious. Earlier this month, the bank had sharply lowered its global growth forecast for this year to 1.7%, from an estimated 3% in June. It cited elevated risks of a worldwide recession due to persistently high inflation.

Thanks to lower fuel and commodity prices and tighter monetary policy, global inflation is set to fall to 6.6% this year and 4.3% in 2024, after peaking at 8.8% in 2022, the IMF said. About 84% of countries are expected to see lower consumer price inflation this year. (…)

![]() China Top 100 Developers See Jan Sales -32.5% Year on Year and -48.6% MoM: CRIC (@Sino_Market)

China Top 100 Developers See Jan Sales -32.5% Year on Year and -48.6% MoM: CRIC (@Sino_Market)

Ford Cuts Prices of EV Mustang Mach-E Move comes after Tesla slashed prices on a number of its models in the U.S.

Ford Motor Co. said it is boosting production and cutting prices of its electric Mustang Mach-E crossover up to 8.8% on some versions. (…)

“We are not going to cede ground to anyone,” said Marin Gjaja, chief customer officer of Ford’s electric-vehicle business. He added that the company is keeping its pricing competitive and reducing customer wait times.

Ford’s Mach-E price cuts range from 1.2% to 8.8%, depending on the configuration. In dollar terms, that is about $600 to $5,900 less than the previous sticker price on the sporty SUV, a model that hit the market in late 2020 and is a direct competitor to Tesla’s Model Y.

The Mach-E has a starting price tag of about $46,000. But some fully loaded versions can sell for over $60,000. (…)

John Murphy, an auto analyst for Bank of America Merrill Lynch, said Tesla’s markdowns create the risk of triggering a broader EV price war in the auto industry. Mr. Murphy, in a research note earlier this month, said many car companies are losing money on EVs and will have to seek ways to build these models even more efficiently. (…)

Ford became the No. 2 EV seller in the U.S. last year, although it still trails Tesla by a wide margin. Tesla accounted for about 65% of all electric vehicles sold in the country last year, according to market research firm Motor Intelligence. Ford’s EV market share in the U.S. was about 7.6% last year.

- Chinese upstarts Xpeng and Seres Group announced price cuts earlier this month on the heels of Tesla’s multiple reductions in China. Electric vehicle prices shot up 54% in July last year from the same month in 2021, compared to 10% for gas-powered cars. (Axios)

- Tesla uses its profits as a weapon in an EV price war

Tesla, once one of the auto industry’s biggest money losers, has over the past year built a commanding lead over most major rivals in profit per vehicle, a Reuters analysis of industry data shows.

Tesla earned $15,653 in gross profit per vehicle in the third quarter of 2022 – more than twice as much as Volkswagen AG (VOWG_p.DE), four times the comparable figure at Toyota Motor Corp (7203.T) and five times more than Ford Motor Co (F.N), according to a Reuters analysis.

For most of this year, Tesla joined rivals in aggressively raising prices on its most popular vehicles, such as the Model Y SUV. Shortages of semiconductors and other materials kept auto industry production down, allowing companies across the industry to focus on higher-margin models and book strong profits, even as sales volumes fell.

Reuters Graphics

I would not take these numbers to the bank. Corporate accounting varies significantly and TSLA is not the most transparent company. For example, a Nikkei-Asia analysis recently put Tesla’s profits per vehicles at $9,570 and Toyota’s at $1,200.

FYI: BP Energy Outlook, 2023 edition

Samsung Expects Sluggish Demand to Drag On as Profit Slides The South Korean tech company saw operating profit drop 69%, hit by falling sales of chips and smartphones as demand for gadgets languishes.

Economic uncertainties are weakening momentum for any short-term rebound in demand for memory chips, Samsung’s main cash cow, said Kim Jae-june, executive vice president for global sales and marketing at the company’s memory business, in an earnings call on Tuesday. (…)

Samsung is the world’s largest producer of two major types of memory chips called DRAM, which enables devices to multitask, and NAND flash that provides storage on devices.

Industry analysts expect average contract prices of both types of memory to keep falling through the first half of the year, as demand remains sluggish and inventory levels high amid continued macroeconomic challenges and widening recessionary fears.

Samsung’s semiconductor business led by memory-chip sales saw operating profit for the October-December quarter drop by 96.9% from the prior year to 270 billion won, the company said. Semiconductor revenue for the three-month period declined 23.6% from last year to 20.07 trillion won.

Despite the current downturn, Samsung said it would keep its capital expenditure plans for 2023 similar to last year’s as it looks to prepare for mid- to long-term demand. The move contrasts with that of rivals that have already pulled back their capacity expansion plans or lowered output for this year to ease the supply glut.

Samsung, however, signaled a near-term reduction in production through line maintenance and other adjustments. The firm also plans to increase the research and development portion of its capital expenditure compared with prior years. (…)

Worldwide smartphone shipments during the fourth quarter—typically a strong quarter aligned with the holiday season—declined 18.3% from the prior year to 300.3 million units in the largest-ever decline in a single quarter, according to International Data Corp., a tech-market researcher. (…)

Wilson doubling down on bearish bets (The Market Ear)

Wilson thinks we will soon have the final leg of this bear market. “…Bottom line, we double down on our thesis, which is now out of consensus again, based on sentiment and positioning. With month end this week taking some pressure off active managers to keep chasing this rally that is based on a narrative that started in October from much lower valuations, it’s time to fade it…A pause is very different this time given the fact the Fed is still doing QT and remains unlikely to cut rates in the absence of a recession. In short, we think the Fed meeting this week will be a reminder of that fact.” (Wilson, Morgan Stanley)

U.S. Considers Cutting Off Huawei From Exports The Biden administration is considering entirely cutting off the Chinese telecommunications giant from U.S. suppliers over national-security concerns by tightening export controls targeting the firm.

The Trump administration in 2019 added Huawei to the Department of Commerce’s “Entity List,” a roster of foreign companies deemed to be national-security threats. However, the Commerce Department later agreed to grant licenses to U.S. companies allowing them to sell technology to Huawei as long as it wouldn’t put national security at risk.

The Biden administration is now considering no longer granting such licenses, although no decision has been made, the people familiar said. The deliberations were previously reported by Bloomberg and the Financial Times. (…)

Officials have signaled to Qualcomm Inc. and Intel Corp., which continue to supply Huawei, that this is a good time to wind down their sales to the Chinese company, said one of the people familiar with the matter. (…)

One of the ideas under consideration is to use more stringent controls that not only ban direct dealings with the company, but that also prohibit exports to other companies and intermediaries who then supply Huawei, according to this person. That policy has the potential to suppress Huawei’s dealings outside the U.S. given the extent U.S. components are used internationally.

(…) Huawei didn’t feature among the top five providers of handsets in China last year, according to research firm International Data Corp. Those five vendors, including Apple Inc. and Chinese manufacturers, accounted for about 84% of smartphone shipments in the country in 2022, according to IDC. (…)

-

Three-Way U.S. Chip Alliance Should Spook Beijing Deal with Japan, Netherlands sends strong signal on allied unity and possibly complicates China’s expansion plans

Japan and the Netherlands agreed on Friday to join the U.S. in limiting exports of advanced chip-manufacturing equipment to China. The three countries dominate the manufacturing of equipment for advanced semiconductors, so the plan could make it even harder for China to develop its own chip industry.

Japan and the Netherlands are particularly dominant in a manufacturing process called lithography: using light to print tiny circuits on silicon wafers. Dutch manufacturer ASML essentially monopolizes the production of equipment needed for the process called extreme ultraviolet lithography, or EUV, used to make the most cutting-edge chips. It has already stopped shipping EUV machines to China.

But since the Biden administration expanded its chip-related curbs on China in October, some older Dutch and Japanese technologies also might need to be restricted to make the U.S. measures effective—and avoid forcing U.S. companies to absorb the impact alone. Japan’s Nikon competes with ASML in supplying parts for a technological process called deep ultraviolet lithography, or DUV, which is one step less advanced than EUV. Friday’s agreement likely will restrict Japanese and Dutch companies from shipping at least some models of DUV machines. (…)

These latest restrictions won’t completely hamstring China’s chip industry, but they send a strong signal of allied unity, and could even presage further measures to come. For Beijing and China’s chip aspirants, that might be the most worrying aspect of this latest salvo.

-

Why China Will Never Lead on Tech Communism is incapable of nurturing the curiosity that leads to innovation.

(…) But there is a bigger reason that China’s ambitious technology endeavors are failing: Its communist system stifles innovation. In China, all major funding is controlled and distributed by the Communist Party. Top scientists must be in the party system to advance their careers and get funding. The higher they rank within the party, the more funding they can receive. They can also make fortunes steering projects and government funds to companies owned by their associates and earning huge kickbacks. The recent corruption investigations have implicated key Big Fund officials and executives of companies that have received the most funding, raising speculation that the fund’s leaders may have taken kickbacks from these companies.

Before the investment pause, chip startups that were linked to the local government officials tasked with recommending and verifying candidates were capturing subsidies. According to an analysis by the South China Morning Post, 15,700 new Chinese semiconductor companies were registered from January to May 2021. A Chinese media outlet, Sing Tao Global, reported that many companies in industries ranging from construction and cement to garments and pharmaceuticals had switched, at least on paper, to chip manufacturing, resulting in unfinished projects and frequent shutdowns. But even without this poor resource allocation, China’s chip development still would be hindered by the country’s lack of long-term vision.

In 2019 I interviewed a data and AI scientist at Huawei, China’s largest and most powerful telecommunications company, which at the time was poised to take over the global rollout of 5G. He told me that despite Huawei’s achievements, a hunger for quick success pervaded the company. While Ren Zhengfei, the company’s founder and CEO, would publicly encourage new research, he was likely to cut off funding if there were no notable achievements within a project’s first two years. This pattern has led to the most consistent innovation at Huawei taking place only at the application level. The company rewards innovations that can make money immediately, but long-term research that might lead to world-changing innovation isn’t being done.

This isn’t unique to Huawei. It is the norm of Chinese society under communist control. Great innovation comes from free and curious minds. Such minds need nurturing, and, despite all its dazzling skyscrapers and smart cities, China today is incapable of doing so.

China’s test-oriented education discourages creativity and independent thinking. The Communist Party uses propaganda to instill a sense of loyalty and gratitude in the people, to the detriment of faith, which encourages broader inquiry. All this, combined with a sense of achievement derived from China’s recent economic successes, has caused the Chinese to become entirely focused on attainment. The goal is always to achieve the greatest benefit at the least cost. Dreams and passions are impractical and expensive, even silly. They must be discarded.

If China can’t cultivate free thinkers, it will always be a follower and never a leader as the West imagines and invents the future.

Life is Good, Especially for Older Americans

Life is Good, Especially for Older Americans

Overall self-reported happiness grows with age, with a striking spike among those age 70-plus, an AARP Research, in collaboration with National Geographic Partners, study reveals. Thirty-four percent of adults 80-plus and 27% of those in their 70s report they are “very happy,” compared to 21% of those 60 to 69, 18% of those 50 to 59 and 16% of those 40 to 49.

The research shows this increased happiness is bolstered by a focus on quality of life over quantity of years, and the importance of relationships and independence. Fielded in January 2022, the 15-minute survey of 2,580 US adults ages 18-plus found that older adults recognize the challenges of growing older but worry about them less as the years pass. Middle age by comparison is the time where life’s burdens take on the greatest prominence.

Stress, anxiety, and fear diminish with age. Even fear of death wanes as older adults focus on planning to minimize the burden and pain of others and finding peace.

Friends, family, and community are the hallmarks of finding happiness, the study revealed. Relationships become a central feature and a source of purpose and joy as people age, particularly in retirement.

Relationships become most important as people reach their 70s and continue to strengthen on into their 80s, while concerns over finances, health, and purpose diminish. Still, people of various ages seem to understand that relationships are not made overnight, with many saying they take time to build and improve relationships in younger years to ensure they are in place as they age. (…)

Despite medicine’s obsession with prolonging life, people are not overly concerned with how long they will live. As they age, this concern continues to diminish.

Instead, individuals are more in tune with the quality of their lives. A long life should be gratifying, not simply a march through time, they feel.

That doesn’t mean people aren’t taking steps for good health. In seeking quality of life, the focus on taking care of oneself increases over the decades in the second half of life. Caring for relationships, going to wellness and screening appointments, monitoring vitamin intake, eating fresh produce and engaging in exercise are all part of ensuring quality years to come. (…)

On a cruise ship last week, we did not notice much emphasis on good health…