Home Prices Rose in March for Second Straight Month Case-Shiller index climbs 0.4% as shortage of homes for sale spurs competition among home buyers

On a year-over-year basis, the index rose 0.7% in March, down from a 2.1% annual rate in the prior month. The annual increase was the smallest since May 2012. (…)

The median existing-home price fell 1.7% in April from a year earlier to $388,800, according to the National Association of Realtors.

The Case-Shiller 10-city index fell 0.8% over the year ended in March, following a 0.5% increase in February. The 20-city index dropped 1.1%, after an annual gain of 0.4% in February. For both indexes, it was the first annual decline since May 2012. (…)

- Consumers saw labor-market conditions cooling more markedly in May as waning demand for workers helps right the supply-demand imbalance – Bloomberg

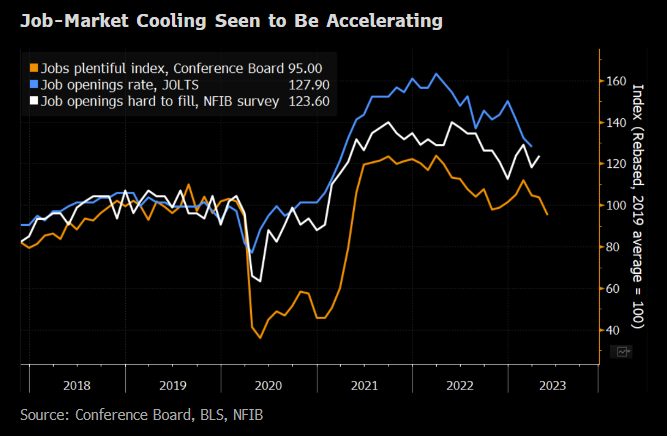

The “Job Plentiful” index is back to its 2019 level. But there’s nothing wrong with that:

Restart of Student Loan Payments Included in Debt-Ceiling Deal Monthly bills will resume 60 days after June 30

(…) McCarthy said Sunday that forbearance is costing the government about $5 billion a month. The average monthly bill before the pandemic was $393 per borrower, and more than 40 million Americans currently have student loan debt.

The debt-ceiling deal doesn’t address Biden’s one-time forgiveness program, which would wipe out up to $20,000 in federal loans per borrower and is currently being weighed by the Supreme Court. That decision is likely to come before the end of June. Biden had said that monthly payments would restart 60 days after the ruling was issued, or no later than the end of August.

Jefferies has said the return of monthly loan payments presents risks similar to the effects of the 2013 fiscal cliff, when tax increases led to reduced consumer spending. And in a note released Monday, JPMorgan’s chief US economist Michael Feroli said that the end of the payment moratorium will reduce annual disposable personal income by $38 billion, which will reduce consumer spending.

That would be about 2% of DPI.

- There’s no “compelling reason” to pause rate hikes, Cleveland Fed chief Loretta Mester said, according to the FT. Rates will head higher in the short run on inflation, Lawrence Summers said.

- There’s a slew of Fed speakers today. We have Collins and Bowman at 8:50 a.m., then Collins speaks again at 12:20 p.m. followed by Harker at 12:30 p.m., and Jefferson at 1:30 p.m. At 2 p.m. the Fed releases the Beige Book.

- US interest rates could push higher in the short-run, and taxes rise in the long run, says former Treasury Secretary Lawrence Summers, who sees risks from inflation and government debt. In a speech Tuesday at the Peterson Institute, he said the US seemed stuck with underlying inflation around double that of the Fed’s target, meaning the central bank may have to raise rates further. “My guess is that Fed funds are going to have to get to a point 50 basis points or more ahead of where they are,” he said, adding the US would be “likely to require substantial increases in revenue.”

The 2-year Ts rate suggests a pause:

China Tensions Rattle American Manufacturers Makers of watercraft and ventilators reconsider Chinese supply chains, balancing potential risks against the lower costs.

Executives are plotting alternate supply chains or devising products that can be made elsewhere should China’s hundreds of thousands of factories become inaccessible. That prospect became more conceivable, they said, after the 2022 invasion of Ukraine prompted companies to sever ties with Russia, sometimes taking huge write-downs.

U.S. companies were further rattled after Chinese authorities recently questioned workers at Boston-based consulting firm Bain & Co. and raided the Beijing offices of Mintz Group, a due-diligence firm based in New York. The government has also barred major Chinese firms from buying products made by U.S. semiconductor company Micron Technology, citing national-security risks. (…)

China’s access to raw materials and ability to produce components for finished goods remains unmatched, and its dense supplier networks have yet to be replicated elsewhere.

China accounts for 31% of global manufacturing, according to the United Nations Industrial Development Organization, nearly twice the 17% share of the U.S. It is also an important market for many U.S. companies. (…

Harris sees other bad omens, such as a court system that he said has become increasingly unfriendly to U.S. companies. Some businesses are plotting a departure, he said, but are finding no easy equivalent to their setups in China. Vietnam, for example, has become so popular that manufacturing space is now hard to find, he said. (…)

U.S. manufacturing production stalled after the GFC but employment has picked up a little though still 5.5% below pre-GFC numbers. Manufacturing unit labor costs, stable for 20 years, jumped by 25% between 2014 an 2019 and another 13.4% since.

According to China’s NBS, manufacturing wages jumped 52% between 2014 and 2019 and another 25% since.

A recent study by the Reshoring Institute concluded “that China can no longer be considered a low-cost country, as its labor rates have significantly increased.”

With labor rates in China doubling over the past few years, companies are now considering moving back to America or to alternate low-cost countries. The research study shows that wages in China are now nearly comparable with those in some European countries leaving the lowest-cost manufacturing to India, Mexico and Vietnam.

Salaries: production Salaries: managers/supervisors

Source: The Reshoring Institute

But there are other issues:

In many world locations there simply aren’t enough workers to fill the jobs at mega-assembly operations. In the United States and Western European countries, worker shortages to fill existing positions have become a major problem, while in countries such as India, China, and Mexico labor is relatively plentiful.

Productivity rates are also important to compare. If a worker in China is paid $300 per month and one in Vietnam is paid $200 per month, it seems reasonable to consider moving to Vietnam until you compare productivity rates. Chinese workers with more experience and often better skills may work faster and with a low error rate as compared with Vietnamese workers. When all of these comparisons are taken into consideration, the decision to move may not be so attractive. (…)

Despite significantly higher labor rates in the United States, manufacturers are coming back to America. To be competitive in world markets and at home, U.S. manufacturers must automate production, reengineer processes to extract labor costs, and make manufacturing more efficient.

When comparing manufacturing in America versus other countries, you must consider the total cost of ownership and include all costs such as logistics, quality, proximity to markets, import duties and penalties, inventory carrying costs, and geopolitical risks. Clients at the Reshoring Institute are often surprised to find that when all costs are considered, American manufacturing can be very competitive.

China’s Recovery Slows Further as Factory, Services Activity Pulls Back An official reading of manufacturing activity slipped deeper into contraction in May

An official gauge of the country’s manufacturing activity slipped unexpectedly to 48.8 in May, falling deeper into contractionary territory even as the broader economy has been unshackled from three years of strict zero-Covid restrictions.

The purchasing managers index remained below the 50 line that separates expansion from contraction for a second straight month, falling short of April’s 49.2 result and the 49.7 forecast by economists surveyed by The Wall Street Journal. (…)

The official gauge of nonmanufacturing purchasing managers index, which covers both service and construction sectors, remained in expansion territory, but pulled back to 54.5 in May from 56.4 the previous month, China’s National Bureau of Statistics said Wednesday. (…)

Subindexes of the manufacturing PMI tracking new orders and new export orders contracted further in May compared with a month earlier. (…)

While the services sector has been leading the recovery this year, the subindex tracking services activity declined to 53.8 in May from 55.1 in April, China’s statistics bureau said. The construction subindex also fell to 58.2 in May from 63.9 in April. (…)

Americans are flying

The Transportation Security Administration reported that it screened nearly 9.8 million airport travelers during the four-day Memorial Day weekend, up about 300,000 from the same weekend in 2019. On Friday, TSA screened 2.74 million people, the highest for a single day since before the pandemic. (Axios)

Data: TSA; Chart: Axios Visuals

We Asked Workers Why They’re Not Coming Back to the Office Terrible commutes. Expensive child care. Employees explain why they will keep working from home.

(…) A battle of wills could be ahead. The gap between what employees and bosses want remains wide, with bosses expecting in-person collaboration and workers loath to forgo flexibility, according to monthly surveys of worker sentiment maintained by Nicholas Bloom, a Stanford University economist who studies remote work.

One reason workers say they’re reluctant to return is money. Some who have lost remote-work privileges said they are spending hundreds, or in some cases thousands, of dollars each month on meals, commutes and child care. (…)

(Bloomberg)

BBB Advised

Tremors in investment grade: the triple-B-rated portion of the Bloomberg U.S. Corporate Bond Index sports a 53-basis point yield premium to single-A’s as of this afternoon, up from 45-basis points in March and representing the largest such pickup in six months.

That gradual creep wider comes as some $11.4 billion worth of formerly high-grade issuers were downgraded to junk by Barclays’ count in the first quarter. The investment bank predicts the full-year tally of so-called fallen angels will reach as much as $80 billion, a figure exceeded on only three occasions (2009, 2016 and 2020) over the past two decades. (Almost Daily Grant)

U.S. Mood Remains Glum; 18% Satisfied With State of Nation

The 18% of Americans who are satisfied with the state of the nation today is about half of the 35% historical average. Gallup has measured national satisfaction since 1979. The lowest reading was 7% in October 2008 during the height of the financial crisis. The high point was 71% in February 1999 during the dot-com boom and after the Senate acquitted President Bill Clinton in his impeachment trial.

Americans’ confidence in the U.S. economy also remains depressed, with Gallup’s Economic Confidence Index essentially unchanged at -43 in May after dropping in April. However, like the national satisfaction measure, it is not as low as last summer, when it fell to -58 in June 2022, the lowest Gallup had recorded since the Great Recession.

And yet, Americans want more stock in their companies:

Some 61% of U.S. adults are invested in the stock market, an April poll from Gallup found. That’s the highest share since 2008, up from 58% last year and 52% as recently as 2016.

A paucity of income-generating opportunities during the post-crisis E-Z money epoch (witness the sub-1% average interest rates on offer for five-year certificates of deposit from 2012 to 2017 and 2020 to mid-2022, per data from Bankrate.com) can explain the growing popularity, some believe. “My overarching conclusion about why equity ownership is relatively high is that the ‘there is no alternative’ principle was alive and well, until very recently,” Christine Benz, direct of personal finance and retirement at Morningstar, told Yahoo! Finance Thursday. (ADG)