CONSUMER WATCH

Walmart Sinks on Cautious Consumer Outlook, Late-October Dip Retail giant modestly raises forecast but sees rising pressure

There was a “sharper falloff” in sales during the last two weeks of the fiscal third quarter, which ended Oct. 31, said Chief Financial Officer John David Rainey. While the exact cause is hard to identify, higher interest rates, dwindling savings and student-loan repayments are weighing on demand, he said. November is off to a good start so far, thanks in part to promotions and holiday shopping.

“We are more cautious on the consumer than we were 90 days ago at this time,” Rainey said in an interview as Walmart reported financial results Thursday. “The takeaway for us is that we’re seeing strength, we’re seeing share gains versus others, but there still is pressure on the consumer.” (…)

Excluding fuel, comparable sales at Walmart’s US unit rose 4.9% during the three months ending in late October. Target Corp. and Home Depot Inc. reported declines in that metric this week, as consumers continued to pull back from discretionary purchases. (…)

“We think we may see dry groceries and consumables start to deflate in the coming weeks and months,” McMillon said on an earnings call.

In the US, McMillon said, the price of beef is up versus a year earlier but dairy, eggs, chicken and seafood are down. General merchandise prices, meanwhile, “came down a little more aggressively in the last few weeks or months.”

- US Continuing Jobless Claims Rise to Highest in Almost Two Years Recurring applications rise for eighth week, to 1.87 million

Recurring jobless claims, a proxy for the number of people continuously receiving unemployment benefits, jumped to 1.87 million in the week ended Nov. 4, according to Labor Department data out Thursday. That marked an eighth straight week of increases.

Initial jobless claims also rose, to 231,000 in the week ending Nov. 11. That was the highest since August. (…)

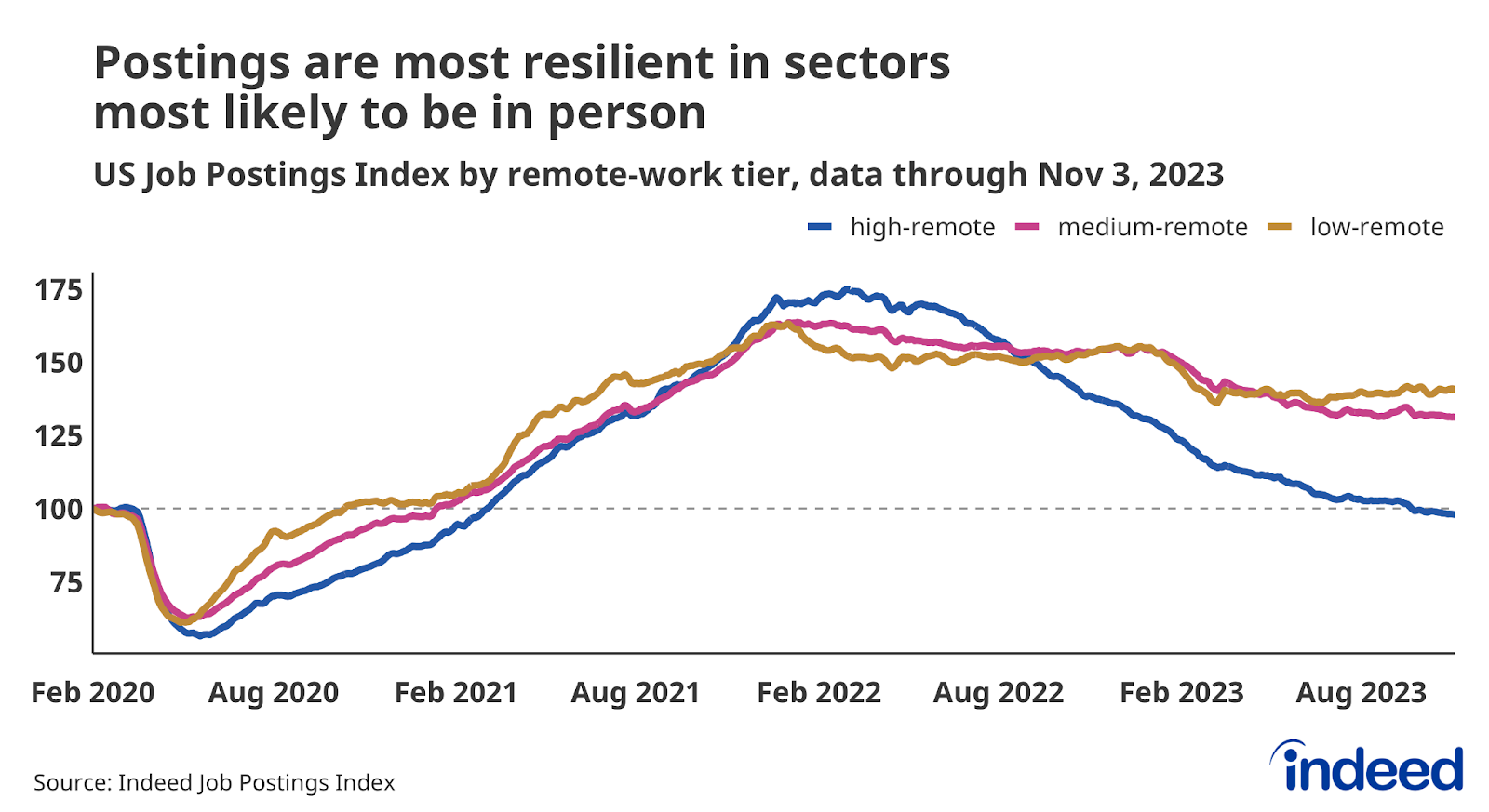

It may be just short-term noise but the sharp drop in Indeed Job Postings so far in November (through Nov.10) is worrisome.

Indeed’s breakdown confirms the shift in leadership, not really healthy in my view:

The pullback in job postings has been most stark in sectors tied to previously high-flying industries, including tech, where stock valuations have fallen and hiring plans have returned to earth. Sectors connected to companies that provide in-person services, including restaurants, hotels, and hospitals, represent a continued source of robust hiring demand.

The Conference Board’s ETI keeps declining:

“While changes have been minimal month to month and the index remains elevated, there are signs of cooling as recent job gains have been mostly concentrated in industries facing major labor shortages including in-person services and government. If labor markets continue cooling and wage growth slows further, the Federal Reserve may be done with interest rate hikes for the current tightening cycle.”

Eric Basmajian (@EPBResearch) observes that both the leading and coincident ETI “are nearing the historical “brink” of the waterfall.”

The eight leading indicators of employment aggregated into the Employment Trends Index include:

- Percentage of Respondents Who Say They Find “Jobs Hard to Get” (The Conference Board Consumer Confidence Survey)

- Initial Claims for Unemployment Insurance (U.S. Department of Labor)

- Percentage of Firms with Positions Not Able to Fill Right Now (© National Federation of Independent Business Research Foundation)

- Number of Employees Hired by the Temporary-Help Industry (U.S. Bureau of Labor Statistics)

- Ratio of Involuntarily Part-time to All Part-time Workers (BLS)

- Job Openings (BLS)

- Industrial Production (Federal Reserve Board)

- Real Manufacturing and Trade Sales (U.S. Bureau of Economic Analysis)

Speaking of manufacturing, recently released regional indexes show no upturn just yet.

NAHB Housing Market Index: Builder Confidence Down Again

INFLATION WATCH

Oil Collapses Into Bear Market as Robust Supply Pressures OPEC+ Rising US inventories spur selloff with WTI near $73 a barrel.

(…) The latest slump has been driven by a myriad of factors. Prices for real-world barrels have been steadily softening over the last few weeks, in part as supply exceeds expectations. Shipments from Guyana and the North Sea are set to rise next month, while US exports have been surging.

Those higher volumes muddy the outlook ahead of a meeting of the Organization of Petroleum Exporting Countries and its allies at the end of next week. Saudi Arabia and Russia — the group’s biggest producers — have pledged to keep additional output curbs in place until the end of the year, though Russia’s crude exports have risen in recent weeks. (…)

“All eyes are now back at OPEC+ after the recent fall in oil prices, along with weakening crude curve structures and weakening economic statistics,” said Bjarne Schieldrop, chief commodities analyst at SEB AB.

Inventory data from the US earlier in the week pointed to a sharp increase in stockpiles recently, particularly at the key storage hub of Cushing, Oklahoma. Those builds come as refineries undergo seasonal maintenance, reducing their demand for crude. Overseas shipments have also been leaping as US production rises, adding supply to the market.

The International Energy Agency said earlier this week that production growth means the global market won’t be as tight as had been expected this quarter. (…)

“We believe that OPEC will ensure that Brent oil prices end up in a $80-to-$100 range in 2024 by ensuring a moderate deficit and leveraging its pricing power,” Goldman Sachs Group Inc. analysts including Daan Struyven said in a note. The latest selloff was driven by non-OPEC supply topping expectations, they said.

The demand outlook has also been cloudy. Figures from China, the world’s largest importer of crude, show that refiners cut daily processing rates in October as apparent oil demand fell from a month earlier. Meanwhile, US unemployment benefits rose to the highest level in almost two years, signaling a slowdown in the world’s biggest crude consumer.

- Iran told US it did not want Israel-Hamas war to escalate Hossein Amirabdollahian says Tehran has used back channels to convey fears of conflict in Gaza spreading across region

More from Indeed:

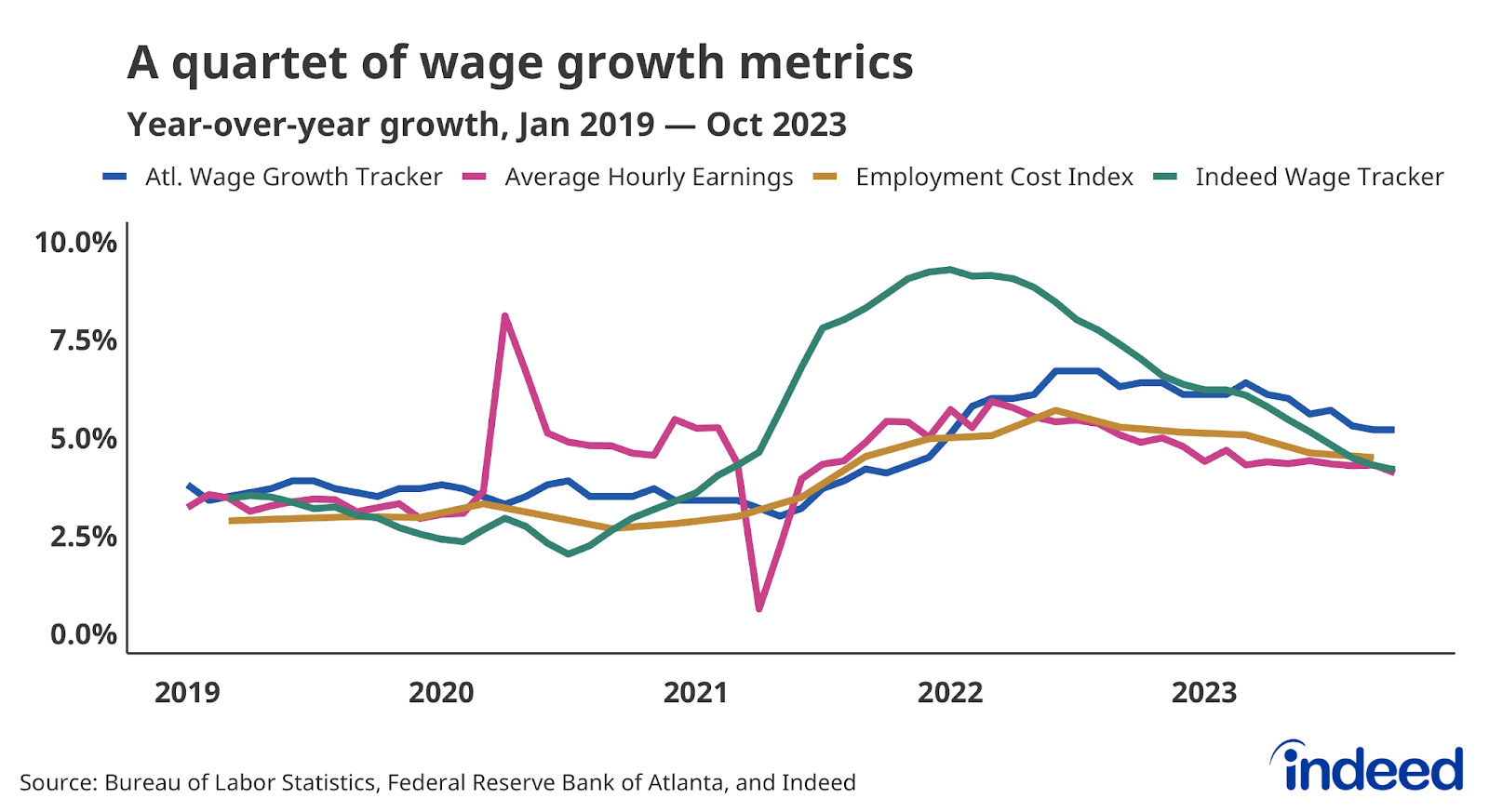

One of the most apparent signs of the ongoing US labor market cooldown is that wages are no longer growing as quickly as they recently were. Falling employer demand, increasing labor supply, and diminished quitting has resulted in employers handing out smaller raises.

This slowdown in wage growth can be seen in a variety of measures of wage growth, including the Indeed Wage Tracker and those from the federal government. The Indeed Wage Tracker peaked first, in January 2022, and the Atlanta Fed’s Wage Growth Tracker peaked last, in early 2023.

While wage growth has slowed, by several measures, it hasn’t yet returned to its pre-pandemic growth pace. But there are indications it may fall to that level relatively soon. According to the latest data from the Indeed Wage Tracker, posted wages in October were up 4.2% from a year prior, down from 4.8% in July and well below the January 2022 peak of 9.3%.

If posted wages continue to slow down at roughly the rate they have for the past three months, the Indeed Wage Tracker will return to its pre-pandemic pace before the middle of next year.

Wage growth seems on a track back to the healthy and sustainable rate seen before the pandemic. Wage growth between 3.5% to 4% would be consistent with 2% inflation, assuming labor productivity grows between 1.5% and 2% annually. Labor productivity is up 2.2% over the past year, but the underlying pace might be lower than that moving forward.

Where Have All the Foreign Buyers Gone for U.S. Treasury Debt? Overseas private investors and central banks now own about 30% of all outstanding U.S. government debt—down from roughly 43% a decade ago.

The U.S. Treasury market is in the midst of major supply and demand changes. The Federal Reserve is shedding its portfolio at a rate of about $60 billion a month. Overseas buyers who were once important sources of demand—China and Japan in particular—have become less reliable lately.

Meanwhile, supply has exploded. The U.S. Treasury has issued a net $2 trillion in new debt this year, a record when excluding the pandemic borrowing spree of 2020. (…)

A group of Wall Street executives that advise the U.S. Treasury, known as the Treasury Borrowing Advisory Committee, recently flagged waning demand from two big-time buyers: banks and foreigners.

Over the medium term, the committee said it expects “demand from banks and foreign investors to be more limited.” (…)

Overseas investors sold a net $2.4 billion in long-term Treasurys in September, bringing their holdings to $6.5 trillion, according to data from the U.S. Treasury released Thursday. On a rolling 12-month basis, which helps to smooth out volatility in monthly data, the pace of foreign buying has eased to around $300 billion in recent months from levels above $400 billion for much of last year, according to data from the Council on Foreign Relations that also adjusts for changes in valuation.

The makeup of overseas demand has shifted. European investors bought $214 billion in Treasurys over the past 12 months, according to Goldman Sachs data. Latin America and the Middle East, flush with oil profits, also added to holdings. That has helped offset a $182 billion decline in holdings from Japan and China. (…)

“In the U.S. it might look a bit bleak, but from our perspective over here [UK], you look in a much better shape than we are,” he said. “You’ve got some real value at these levels.” (…)

Ramjee said he remained concerned about the U.S. government’s widening deficits. But few other developed-market government bonds offer real yields—or interest rates exceeding expected inflation—comparable to those offered by U.S. bonds.

Demand from private investors in Europe, however, isn’t enough to offset the longer-term structural changes that are weighing on foreign demand for Treasurys, said Praveen Korapaty, chief interest rates strategist at Goldman Sachs.

“Are they actually swinging the needle here? Not really,” he said. “The foreign ownership of Treasurys continues to decline and we expect that will remain the case for the foreseeable future.” (…)

Central banks, voracious buyers of U.S. Treasurys in the 2000s and early 2010s, remain a weak spot for overseas Treasury demand. The strength of the dollar has spurred many central banks, including those in China and Japan, to stop adding to their stockpiles of U.S. Treasurys or even to sell them down, analysts say. They use the dollars they get from selling U.S. bonds to buy their own currencies, boosting the value.

At the same time, China has diversified reserves away from Treasurys and has been investing in bonds backed by U.S. government agencies such as Freddie Mac that offer higher yields than Treasurys. China has bought a net $32 billion of those in the year through August, according to data from the Council on Foreign Relations.

Japanese private investors—including banks, pensions and insurers—are a source of worry. Many have invested heavily in U.S. Treasurys as a way to escape ultralow, and at times negative, interest rates at home. Between those investors and the Bank of Japan, the country is the largest foreign holder of U.S. Treasurys with a stockpile worth more than $1 trillion.

The Bank of Japan has allowed government bond yields to rise as the country finally looks set to escape its deflationary spiral, which should encourage investors to invest more in the domestic government bond market. (…)

Masatoshi Yamauchi, an executive officer at All Nippon Asset Management, whose main clients include regional banks, said Japanese banks have continued to invest in U.S. Treasurys, but with shorter durations, and without hedging currency risk, which is currently very costly for Japanese investors. But they, too, might soon lose interest in the U.S., he warned.

“They are getting full,” he said. “Interest rates are becoming more attractive in their mother market.”

@YuanTalks:

- #China cut holdings of #US #Treasuries for 6th straight month in Sept to $778.1 bn, lowest since May 2009, falling below $800 bn for first time in 14 years, showed data from US Department of Treasury

- #China‘s new #home prices fell for 4th straight month in Oct, fewest cities saw 2nd-hand home price rise since Oct 2014