Business Inflation Expectations Unchanged at 3.0 Percent

")

- How do your current sales levels compare with sales levels during what you consider to be “normal” times?

- How do your current profit margins compare with “normal” times?

")

- How do your unit costs compare with this time last year?

")

Short-Term Inflation Expectations Decline, Household Spending Expectations Fall Sharply

Median one-year-ahead inflation expectations declined to 5.0 percent, its lowest reading since July 2021, according to the [NY Fed] December Survey of Consumer Expectations. Medium-term expectations remained at 3.0 percent, while the five-year-ahead measure increased to 2.4 percent.

Household spending expectations fell sharply to 5.9 percent from 6.9 percent in November, while income growth expectations rose to a new series high of 4.6 percent.

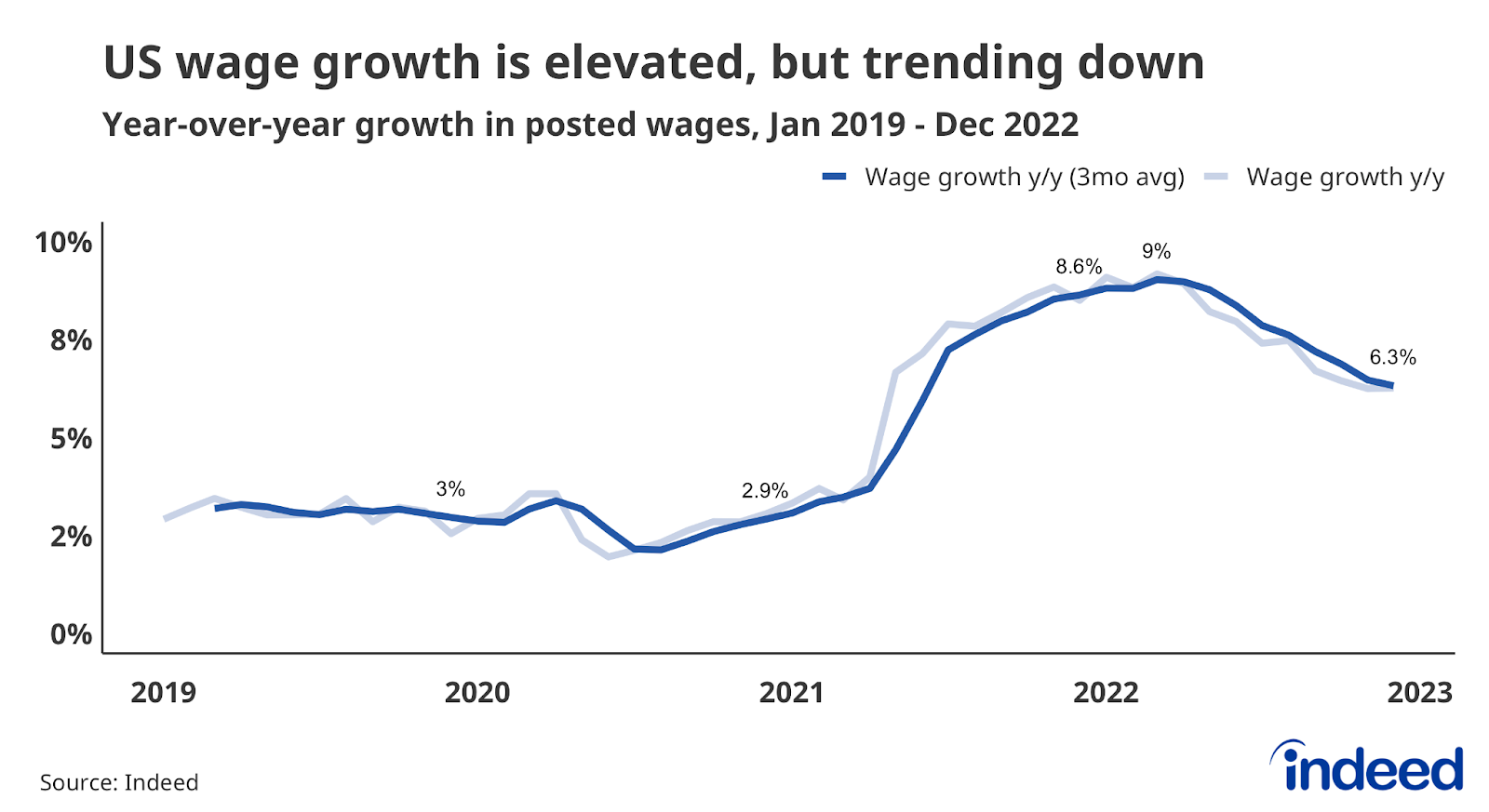

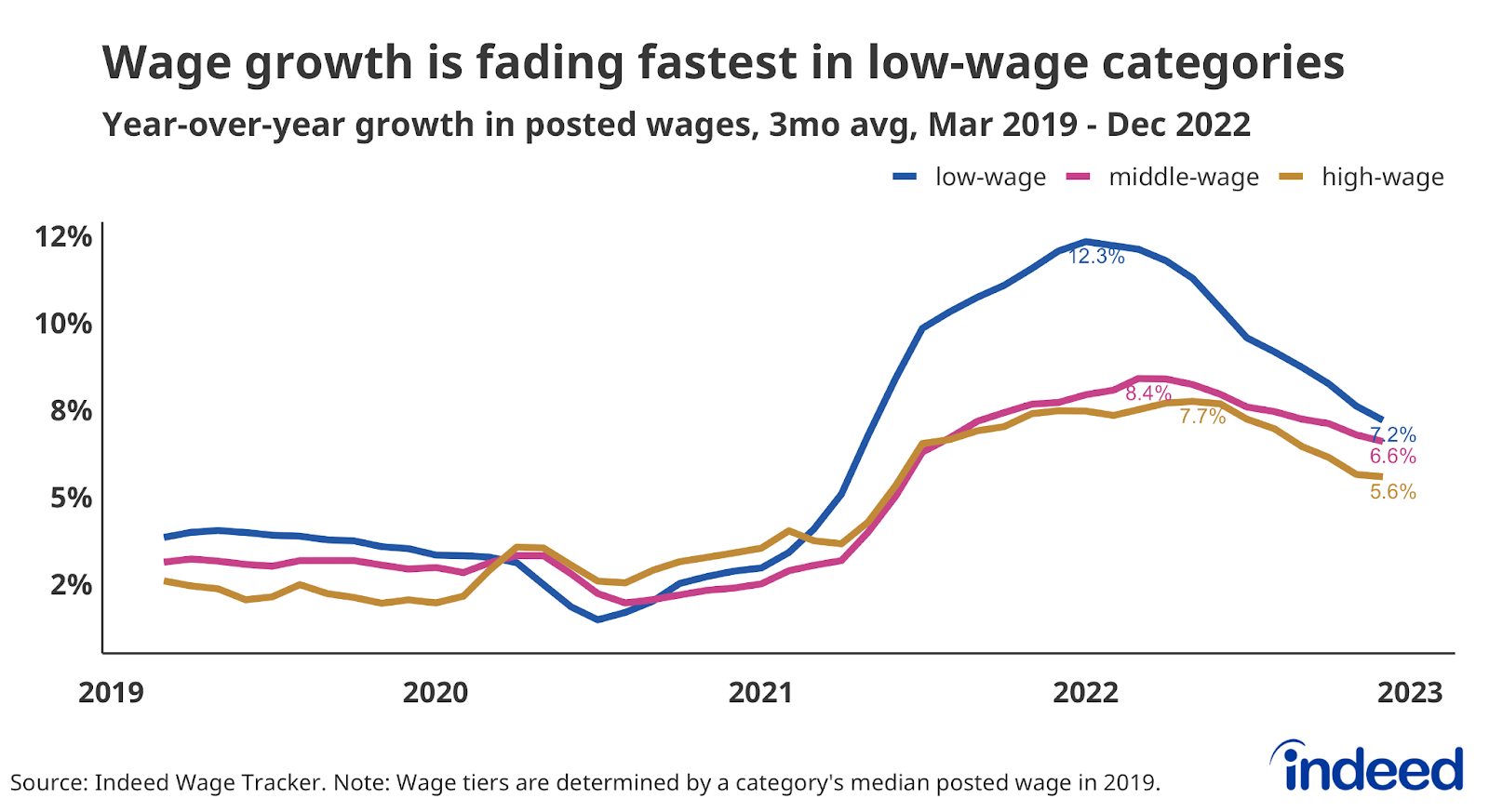

US Posted Wages Continued to Slow In December Though wages and salaries advertised in job postings on Indeed grew at a quick pace in December, they continued to decelerate from their rapid pace earlier in the year.

The latest data from the Indeed Wage Tracker shows that wages and salaries advertised in Indeed job postings continue to grow quickly, but the slowdown that started last spring continues. Posted wages grew 6.3% year-over-year in December 2022, a pace more than twice December 2019’s measurement of 3%.

Fewer than one in five occupational categories had faster posted wage growth in December than six months prior. That represents a tremendous decline from December 2021, when advertised wages were accelerating in almost nine out of every 10 categories.

Lower-wage sectors continue to show a sharper wage growth decline than other sectors. Overall posted wage growth declined by 0.2 percentage points from November to December, but fell by 0.4 for lower-wage categories. Compare that to a 0.2 point decline for middle-wage categories and a flatlining for the high-wage group.

PC Shipments Drop Sharply, With Slump Expected to Last Until 2024 Worldwide shipments dropped nearly 29% in the fourth quarter from a year earlier, the largest quarterly decline since the mid-1990s, as the end of pandemic-era demand mars the industry’s outlook.

(…) “Enterprise buyers are extending PC life cycles and delaying purchases, meaning the business market will likely not return to growth until 2024,” Mr. Kitagawa said. (…)

PC makers shipped between 65.3 million and 67.2 million PCs in the fourth quarter of 2022. Worldwide PC shipments totaled 286.2 million units in 2022, a 16% decline from the prior year, according to Gartner. (…)

Average selling prices have fallen over the past few months as discounts were offered to reduce overstocked inventories, IDC said. Falling sales have caused many sellers to cut prices for devices. (…)

Amazon Union’s Win in New York Is Upheld Amazon contested election results after workers formed first U.S. union at the company in April last year

(…) Amazon can contest Mr. Overstreet’s ruling to the NLRB governing board in Washington, D.C. The company could eventually bring the case to court, labor attorneys say. Andy Jassy, Amazon’s chief executive officer, last year said he believed the case is “going to take a long time to play out.” (…)

The Amazon Labor Union lost in two other elections in New York state. A majority of workers at a company site in Bessemer, Ala., also voted against unionizing. (…)

- Coinbase’s CEO, Brian Armstrong, announced yesterday that the crypto-exchange would be cutting 20% of its workforce. As a bellwether for the sector, Coinbase’s second round of cuts — following an 18% reduction in headcount back in June 2022 — suggests the “crypto winter” is yet to show any signs of thawing.

Inflation, ‘uncertain economy’ are making home buyers more cautious, KB Home says

(…) KB Home still has a “large” backlog of more than 7,600 homes, equal to about $3.7 billion in future revenue, supporting its projections for 2023, Mezger said. (…)

“Depending on market dynamics and backlog levels in each community, we are getting more aggressive with our pricing ahead of the spring selling season, in order to generate new orders,” Mezger said.

KB Home is also looking for cuts in costs and in building time, which would help to offset any impact of lower prices, he said.

The number of homes delivered rose 3% to 3,786, while the average selling price rose 13% to $510,400, KB Home said.

Reflecting a “sharply lower demand stemming from higher mortgage interest rates, inflation and other macroeconomic and geopolitical concerns,” gross orders for the quarter hit 2,169 units, down 47% on-year.

Cancellation rates as a percentage of gross orders jumped 68%, compared to 13% a year ago.

KB Home guided for first-quarter 2023 housing revenue in a range between $1.25 billion and $1.40 billion, average selling price between $490,000 and $500,000, and profit margins between 20% and 21%.

KB Home shied away from a larger set of full-year guidance “due to significant uncertainty and limited forward visibility regarding 2023 housing market, macroeconomic and geopolitical conditions,” guiding only for housing revenue in a range of $5 billion to $6 billion for the year.

- Wholesale used vehicle prices are down almost 15% from a year ago.

Source: Daily Shot

Source: Daily Shot

China Inflation Picks Up as Covid-19 Restrictions Fall Rising Chinese demand for global commodities could offset easing inflationary pressures.

Consumer prices rose 1.8% in December compared with a year earlier, faster than the 1.6% annual rate recorded in November, China’s national statistics bureau said Thursday. (…)

The acceleration in inflation was driven by gains in food prices, data shows. Food prices rose 4.8% on year in December, compared with November’s 3.7% increase. Nonfood prices increased 1.1 % on year, matching November’s gain. (…)

In the first five days of the traditional peak-travel period, which began on Jan. 7, nearly 38 million passengers were traveling over national railways, highways, waterways and airways—a 41% increase from the same period a year earlier though still 49% lower than the level in the same period in 2019, according to official data released Thursday. (…)

Prices charged by companies at the factory gate fell 0.7% in December on the year, albeit at a slower pace than a month earlier. (…)

Core CPI inflation was +0.7% YoY in December (+0.6% in November).

Where Will the Chinese Splash Their Extra $827 Billion? Investors are waiting to see if consumers engage in a spending frenzy, or keep their cash for a rainy day.

Forced to stay home because of the government’s Covid-Zero policy, Chinese consumers saved one-third of their income last year, depositing 17.8 trillion yuan ($2.6 trillion) into banks. That’s extreme, even for the famously thrifty nation. Before the pandemic, households put away roughly 17% of their earnings. (…)

Over the last three years, excess savings reached 5.6 trillion yuan ($827 billion), according to JPMorgan Chase & Co estimates. (…)

A big chunk of the extra savings during the Covid era could have been made out of precaution. With consumer confidence at a record low, people might be saving for a rainy day. According to the latest central bank survey, over 60% of urban depositors preferred risk-free deposits, while only 15.5% braved investment products. (…)

- This is the U.S. experience per JP Morgan (via The Daily Shot)

Chip Giant TSMC Plans to Cut Spending to Offset Falling Near-Term Sales

(…) “Demand is softer than we thought three months ago,” Chief Executive Officer C.C. Wei said on a conference call. TSMC and its customers will be “more prudent” about their expectations for demand and supply over the coming months, he said. (…)

TSMC said its capital expenditure is set to decrease to $32 billion to $36 billion this year from $36.3 billion in 2022. (…)

- Biden plans new China controls

President Biden plans a new escalation in the U.S.-China relationship, with an executive order imposing new controls on China projects by U.S. companies and investors, Axios’ Hans Nichols reports.

Final language hasn’t been approved. But it appears the executive order will focus on quantum computing, artificial intelligence and semiconductors — and not include biotechnology or batteries.

Officials are unlikely to unveil the order before Secretary of State Tony Blinken makes his first visit to China, currently penciled in for February.

The Biden administration has taken several steps to check Chinese ambitions in AI and quantum computing, with the aim of slowing the development of China’s military capabilities.

Last October, Biden imposed expansive restrictions on semiconductor technology and equipment that can be shared with China.

An analyst with the Center for Strategic Studies described the new policy as “strangling with an intent to kill.”

- COVID-19 brought the number of patents issued in the U.S. down, but only slightly. While the number of patents issued is strong, less than half go to U.S. residents.

- Chinese innovators apply for roughly two-thirds of all patents. The U.S. and Japan have almost all the rest of the applications. (U.S. Chamber of Commerce)

USMCA Panel Rules Against U.S. in Auto Dispute With Mexico, Canada The U.S.’s neighbors had challenged the way it calculates regional content required for tariff-free access under the trade pact.

(…) The minimum regional content requirement was raised to 75% under USMCA from about 62% under Nafta.

Canadian Trade Minister Mary Ng said the ruling reaffirms “our understanding of the negotiated outcome on the rules of origin for automotive products.” Canada joined Mexico’s initial complaint, warning the U.S. interpretation could inhibit the ability of domestic manufacturers from qualifying for duty-free trade in North America. (…

The ruling means that the U.S. must use Mexico’s and Canada’s methods to calculate regional content, or face retaliatory tariffs. (…)

The U.S. Chamber of Commerce said the ruling could provide certainty for the North American motor-vehicle industry, and called on the Biden administration to implement the report’s findings.

John Authers: Is 2% Inflation in View? Be Careful What You Wish For

(…) The question certainly seems to have moved on from whether inflation will cool — to how fast the rate will come down. The path to that is more nuanced, as many may expect. Domestically, there are the US labor and housing markets to consider, pockets of the economy that will likely be key. Internationally, there are global supply chains and China’s big reopening. But economists polled by Bloomberg remain confident that inflation will be down around target by the end of this year. That’s encouraging — although it’s important to point out that they were equally confident that inflation would be under control by the end of last year:

(…) Equally, there are calls that inflation will not stabilize obediently at 2%, but will likely overshoot back into the familiar territory of deflation. Just look at the bold call by Jeffrey Gundlach of DoubleLine Capital, who in his annual “Just Markets” webcast this week said it was “absurd” to believe that inflation would drop from 9.1% to 2% and “magically stop there.” If, in fact, inflation goes to 2% over the course of 2023, it will turn negative, he added. So, if we do have an encouragingly low inflation number in our immediate future, we should remember that it’s possible to have too much of a good thing.

Energy, Industrials and Consumer Discretionary are all expected to show revenue growth exceeding inflation. A few sectors do have a valid explanation for showing less revenue growth than inflation. This is due to their currency exposure, since the dollar was up 8.8% in Q4 versus a year ago. Technology and Materials are the only 2 S&P sectors with more than 50% non-US revenues (55 and 58% respectively). It therefore makes sense that they would have trouble matching US inflation rates.

Data Trek

2022 Q3 saw the lowest percentage of companies beat earnings expectations since 2020 Q2. 70.7% of constituents posted a earnings beat which is a nine-quarter low and below the prior-four quarter average beat rate of 75.5%.

Similarly, the aggregate earnings surprise factor last quarter was also at a nine-quarter low (3.4%) and below the prior-four quarter average surprise factor of 5.3% and below the long-term average of 4.1%.

While Energy is contributing the lion share of earnings growth from a year-over-year perspective, the sector is expected to post a quarter-over-quarter decline in earnings growth (-17.0%), which would mark the second consecutive quarterly decline and put further pressure on the breadth of earnings growth.

Net profit margins peaked in 2021 Q2 (12.9%) and have declined for five consecutive quarters to 11.6% last quarter.

Based on analyst expectations, net margin is expected to decline again this quarter to 11.1%. The forward four-quarter (23Q1-23Q4) net margin is currently 11.7%.

World Bank warns global economy could tip into recession in 2023

The development lender said it expected global GDP growth of 1.7% in 2023, the slowest pace outside the 2009 and 2020 recessions since 1993. In its previous Global Economic Prospects report in June 2022, the bank had forecast 2023 global growth at 3.0%. (…)

The bank said major slowdowns in advanced economies, including sharp cuts to its forecast to 0.5% for the United States and flat GDP for the euro zone, could foreshadow a new global recession less than three years after the last one. (…)

The bleak outlook will be especially hard on emerging market and developing economies, the World Bank said, as they struggle with heavy debt burdens, weak currencies and income growth, and slowing business investment that is now forecast at a 3.5% annual growth rate over the next two years — less than half the pace of the past two decades. (…)

It predicted a [China] rebound to 4.3% for 2023, but that is 0.9 percentage-point below the June forecast due to the severity of COVID disruptions and weakening external demand. (…)

The European Central Bank expects to continue raising interest rates “significantly” at future meetings, at a sustained pace, to ensure that inflation returns to the 2% target over the medium term, ECB policymaker Pablo Hernandez de Cos said on Wednesday.

“Keeping interest rates at tight levels will reduce inflation by dampening demand and will also protect against the risk of a persistent upward shift in inflation expectations”, De Cos told a financial event in the evening.

His stance was in line with the ECB’s guidance and comes after ECB policymaker Mario Centeno said on Tuesday the current process of interest rate increases was approaching its end. (…)

In any case, he said it was crucial to continue to stress the importance of taking into account the “extraordinary uncertainty we are experiencing,” adding that the institution’s future interest rate decisions would continue to be data-driven.