U.S. Nonfarm Productivity Falls Below Consensus Expectations

- Nonfarm productivity declined in Q1 (-2.7% QoQ a.r.), -0.9% YoY.

- Unit labor costs—compensation divided by output—increased in Q1 (+6.3%, QoQ a.r.), +5.8% YoY.

- Compensation per hour rose 4.8% YoY in Q1 but was +3.4% QoQ annualized in Q1, the slowest pace since 2022Q2.

The measure of productivity (always debatable) jumped during the pandemic but is trending back to its long term pace of 1.0-1.5%. But corporate labor costs per unit of production has skyrocketed 13.4% in 3 years, twice its 2.0% longer term pace.

There is a rather close relationship between UCL and core inflation. But which one leads?

Well, corporate profit margins (pretax) have jumped 50% from their pre-pandemic level, in spite of accelerating ULC. The power of pricing power!

- A case in point:

Bank of Canada’s Macklem Warns Inflation Could Get ‘Stuck Materially Above’ Target

Bank of Canada Gov. Tiff Macklem said there is a risk that robust wage growth, elevated inflation expectations and frequent price increases from businesses could impede central bank efforts to slow inflation toward its 2% target.

Such a scenario, he said in prepared remarks Thursday to a Toronto business audience, could prompt the central bank to resume rate increases, after deciding to pause following its January decision. (…)

Mr. Macklem reiterated that the central bank believes its aggressive rate-rising campaign is beginning to bear fruit, as inflation has slowed from a peak of 8.1% in June of last year to 4.3% as of this March. The central bank expects inflation to decelerate to 3% this summer.

The road to 2% inflation is more complicated, Mr. Macklem said. At present, the central bank anticipates inflation slowing to 2% by the end of 2024. Obstacles remain, he said, citing a tight labor market that is pushing annual wages upward, in the 4% to 5% range; corporate price-setting [remember the charts above?], which has yet to return to prepandemic conditions; and elevated inflation expectations, based on the results of central-bank surveys.

“There is a risk that these adjustments will take longer or stall, and inflation will get stuck materially above the 2% target,” Mr. Macklem said. “The projected decline from 3% to 2% is both slower and more uncertain.”

He added: “If we start to see signs that inflation is likely to get stuck materially above our 2% target, we are prepared to raise rates further.”

In a question-and-answer session following his speech, Mr. Macklem said rate cuts were unlikely, given the inflation outlook. “The lesson from history is you certainly don’t want to loosen prematurely because if inflation gets stuck, it’s really hard to get it back down.”

Economic activity is slowing, Mr. Macklem added, but “is still in excess demand,” citing a 5.1% annual increase in the cost of services in March. (…)

In Canada, economists said a tentative labor deal reached this week between the Canadian government and about 120,000 employees could maintain upward pressure on wage growth. Canada agreed to a 12% wage increase over four years for workers, after a 12-day strike. The minutes of Bank of Canada rate-policy deliberations said officials “revisited their concern that the current pace of wage growth, if sustained, would not be consistent with getting inflation back to 2% without a substantial increase in productivity.”

ECB Slows Pace of Rate Increases The European Central Bank indicated it isn’t ready to pause its campaign against high inflation, diverging from the Fed.

(…) In a statement, the ECB said it would increase its key rate by a quarter percentage point, to 3.25%, a near 15-year high. It was the smallest move since the bank started raising rates last July. The bank also said it would reduce its bondholdings at a faster pace starting in July, a move that is likely to weigh further on economic growth and inflation. (…)

The shift to a slower pace of rate increases was “based on the understanding that we have more ground to cover and we are not pausing,” ECB President Christine Lagarde said at a news conference.

“We all concluded that the inflation outlook is too high and has been so for too long,” Ms. Lagarde said of Thursday’s policy meeting. Some officials advocated a larger half-point rate increase, she said. (…)

Investors responded to the decision by lowering their expectations for future ECB interest rate increases. The euro fell 0.5% to $1.1003, signaling that investors see more limited divergence between the ECB and the Fed. European government borrowing costs also declined, with the yield on the 10-year German bund down to 2.192% from 2.282% before the announcement. (…)]

Ms. Lagarde warned on Thursday that underlying price pressures remained strong and that wages were rising sharply.

Investors bet after Ms. Lagarde’s news conference that the ECB would raise rates by only another quarter point, to 3.5%, down about 0.1 points from their prediction earlier in the day, according to data from Refinitiv. They expect the Fed to reduce interest rates by about 0.8 points later this year, to about 4.2%, the data show. (…)

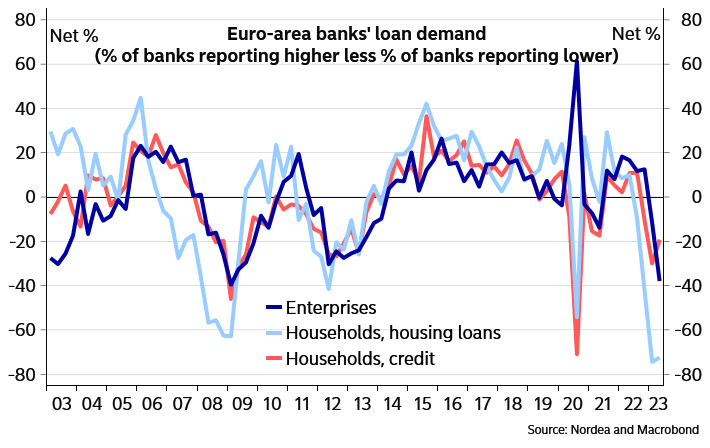

Tighter monetary policy already clearly visible in the credit environment in the Euro Area

- The market is anticipating approximately 180 bps of rate reductions from the Federal Reserve in the second half of this year and the first half of next year. (The Daily Shot)

Source: The Daily Shot

Source: The Daily Shot

- Companies increasingly mention weak demand on earnings calls. (The Daily Shot)

Source: BofA Global Research

Source: BofA Global Research

Eurozone retail sales fell more than expected in March

Retail sales in the eurozone fell by -1.2% in March, which means that retail once again contributed negatively to GDP growth in the first quarter. This adds to other weak eurozone March data, indicating that the bloc ended the first three months of the year on a weak note

Retail continues to struggle with the loss of consumer purchasing power and a shift in preference away from goods and towards services, now that the Covid-19 pandemic has ended.

The volume of sales has been on a declining trend since late 2021 and the March 2023 data are consistent with a continuation of the downward trend. Declines in March were particularly large in Germany, France and the Netherlands at -2.4%, -1.4% and -1.3% respectively, while Spain saw an increase in sales of 0.7%.

With inflation falling, wage growth picking up and unemployment remaining low, the outlook for sales should show some bottoming out in the months ahead, particularly once the catch-up demand for services weakens again.

For the second quarter, though, it looks like the correction in sales could continue as real wages are still falling in the eurozone. This disappointing March figure adds to some individual countries posting weak industrial data this morning and indicates that the first quarter ended on a weak note despite some upbeat survey data.

While it looks like the second quarter was off to a better start, it is important to keep in mind that the eurozone is starting to feel the effect of tight monetary policy and still faces high inflation. We, therefore, expect a modest bounce-back in economic activity for the current quarter.

The US regional bank crisis

John Authers:

This is not like the GFC in the sense that it doesn’t hinge on distrust in the valuations of assets on banks’ books. It isn’t that investors fear that many of their loans are toxic. Rather, the issue now concerns profits. With interest rates where they are, the logic is that banks can only hold on to their deposits, a vital source of cheap funding, by offering rates to customers that obliterate their profits.

This doesn’t directly threaten a bank, in the way that the bad loans did in 2008. But if a bank looks less likely to make profits, that will mean a lower share price, which in turn will make it harder for it to raise equity funding, and not just debt finance. Allowing consolidation in the banking sector would be painful for regulators, and for consumers who would likely get worse service and value for money from monopolistic monoliths. But it’s getting harder to resist.

Why does it matter? First, banks that are in trouble will tighten credit, and companies are now very worried that this is happening and could worsen. Remarkably, Bloomberg colleagues show that credit tightening has come up more often in earnings calls over the last few weeks even than during the horrors of 2008:

Second, it could force changes in both monetary and fiscal policy. Yields have fallen again this week on the belief that the bank crisis will compel the Fed to ease monetary policy. Possibly even more important, the most obvious solution could involve a big fiscal outlay. Insuring all deposits, advocated by many as the measure that could end the crisis, would be mighty costly, even on an interim basis. To do it on a permanent basis would require legislation, which in turn would require America’s polarized politicians to agree on something.

This is very different in concept from what happened in 2008. And as the problem is one of liquidity, or banks’ ability to raise money in a hurry, rather than solvency, it should be far less serious. Bank crises do happen from time to time. That doesn’t mean that this crisis can be ignored, or that it won’t be painful.

- A Debt Deal Could Help Solve the Country’s Inflation Problem Spending cuts could prompt the Fed to cut interest rates sooner, easing some of the pressure on banks.

The Federal Reserve has a problem with stubborn inflation and fragile banks. Congress and President Biden have a problem with a looming deadline to raise the debt ceiling.

There might be a way to address all these problems at once.

Here’s why. Banks are in trouble because of rising interest rates. Rates have climbed because inflation is high. And inflation is too high because demand is hot. One way to cool demand would be for the federal government to cut spending—which happens to be what Republicans, who control the House, are demanding in return for raising the federal government’s $31.4 trillion borrowing limit. (…)

On the substance, Mr. Biden doesn’t want to reduce spending. His team looks with regret back at 2011, when President Obama and then-Vice President Biden acceded to Republican demands for cuts in return for raising the debt ceiling. Besides setting a bad precedent, that austerity took a toll on an economy struggling to recover from the financial crisis. (…)

To be sure, fiscal policy is no longer pushing inflation higher; it is a drag on economic growth, according to the Hutchins Center on Fiscal and Monetary Policy. However, that is because of expiring temporary measures rather than concrete steps to reduce spending or raise taxes.

In fact, the combined effect of bills Mr. Biden has signed on infrastructure, veterans benefits, semiconductors and energy subsidies is to raise, not lower, budget deficits. Even his so-called Inflation Reduction Act might end up reducing the deficit by far less than advertised, if at all. The Congressional Budget Office projects federal spending will equal 23.7% of gross domestic product this fiscal year, well above the prepandemic 21% in 2019.

The CBO says the Republican debt-ceiling bill would reduce discretionary federal spending by $129 billion in the fiscal year ended Sept. 30, 2024, relative to current law. (Discretionary spending must be reauthorized regularly, unlike mandatory programs such as Social Security and Medicare.) That would lower federal spending to 23.1% of GDP, enough to knock about half a percentage point off economic growth. Lower growth is normally a bad thing, but not when demand is too hot. (…

The Fed will likely solve its inflation problem long before Congress solves its debt problem.

Dam! No Water, No Electricity, No Aluminum

Bloomberg’s David Fickling:

(…) Yunnan province, which contains the headwaters of the Yangtze River that feeds many of the vast dams China has constructed over the past few decades, has been gripped by severe drought in recent months, according to the official China Daily. The provincial capital of Kunming has had the driest start to the year since 1985, with rainfall at about 10% of typical levels, the paper reported. Conditions are even worse than they were last year, when the nation experienced its second-driest summer on record. (…)

Economic planners in Yunnan have told local aluminum smelters, one of the most power-hungry sectors of the economy, to cap output and purchase more coal and coal-fired power, the South China Morning Post reported.

Electricity production is already suffering. Nationwide hydro generation in the first quarter of the year came to 204 terawatt-hours, a drop of nearly 8% from the same period last year. That’s particularly worrying because China has more dams now than ever. In the first quarter, they were producing power at no more than about 26% of full capacity, the worst performance since 2014. Water levels at the Three Gorges Dam, the world’s biggest power station, peaked about 15 meters below their normal levels last winter. (…)

China isn’t alone. India has a similar mix of hydroelectricity and coal on the grid, combined with a huge population and blistering hot months. Summer sales of air conditioners will be as much as 20% higher this year, Business Insider India quoted a local appliance manufacturers association as saying in March. Parts of Southeast Asia, facing parched conditions over coming months, are in the same boat.

THERE’S LOTS… AND LOTS

Axios posts this chart and says “New vehicle inventories are jumping from the pandemic-era’s historic lows — and it could lead automakers to ease off the gas”.

New for dealer lots… “vehicles”

Data: U.S. Bureau of Economic Analysis; Chart: Axios Visuals

Really? That’s lots in lots!

Yes, but no. Here’s a longer term chart to put current inventories in the proper perspective.