SERVICES PMIs

Note that data for these PMIs were collected 12-27 March, before “liberation day”, when tariff uncertainty was near its highest.

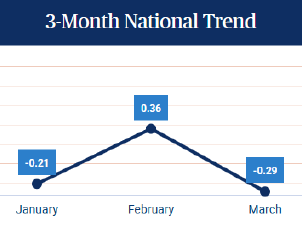

Growth picks up in March, but confidence in outlook remains subdued

The S&P Global US Services PMI Business Activity Index improved noticeably in March having slumped to a 15-month low during February. After accounting for seasonal factors, the index rose to 54.4, from 51.0 and the highest reading of 2025 so far. By remaining above the crucial 50.0 no-change mark in March, the index has signaled continuous monthly growth since February 2023.

Higher activity was principally linked to increased volumes of new work amid evidence of strengthened customer demand. Unseasonably warm weather was also noted to have supported an upturn in activity and sales. New business overall rose solidly and to a greater degree than in February, though growth remained slightly below trend and mainly domestic focused. Latest data showed that foreign sales rose only slightly in March (although this was an improvement on the declines seen at the start of the year).

Confidence in the outlook remained positive overall in March, linked to an expected improvement in economic conditions over the next year. Some firms pointed to the new administration’s economic policies as likely being supportive to growth. However, reflective of the uncertainty in the outlook, concerns persisted over the effects of federal cost cutting initiatives, and in particular, the role of tariffs in raising prices and dampening overall demand. Subsequently, confidence edged lower in March and was, with the exception of last September when sentiment was impacted by uncertainty ahead of the Presidential election, the weakest since December 2022.

With some growth forecast, and new business volumes increasing, a net rise in employment was recorded during March. It was the third time in the past four months that staffing levels have risen, although the net increase was again only modest and below trend. Service providers signaled only mild capacity pressures as work outstanding was up only marginally following a solid reduction during February.

Labor expenses were reported as a factor driving up operating expenses during March. Vendors were also reported to have raised their charges, which was linked by panelists to tariffs. The net result was a third successive monthly acceleration of input price inflation to its highest in a year-and-a-half.

Service providers sought to pass on higher costs to clients via an increase in their own charges. But output price inflation, despite picking up since February, remained below trend in March. Competitive pressures and efforts to sustain demand served to limit output price inflation.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence

(…) the rate of expansion remains below that seen throughout the second half of last year. Combined with a weak manufacturing reading for March, the survey data point to GDP having risen at an annualized rate of just 1.5% in the first quarter, down sharply from the 2.4% rate seen at the end of last year.

The focus turns to whether growth will also trend lower in the second quarter. In this respect, we note that some of the improvement in March reflected better weather, after adverse conditions dampened services activity in the first two months of the year at many companies. There’s a suggestion, therefore, that the expansion in March may exaggerate the true underlying growth momentum in the economy.

This gloomier picture is supported by the PMI’s future activity index, which showed optimism edging lower again in March. Business sentiment is now the lowest since the end of 2022 barring only the heightened uncertainty seen ahead of last year’s Presidential election.

Companies report heightened concerns and uncertainty around the impact of political change, ranging from DOGE-related budget cutting to tariffs and the degree to which foreign demand may be affected by recent policy initiatives. Concerns have also risen in relation to costs, which rose in March at the fastest rate in nearly two years as firms across both services and manufacturing reported intensifying supplier-driven price hikes, fueled by tariffs.

The ISM services report tells us that activity is holding up, but firms are no longer hiring, orders have slowed to a crawl, backlogged orders are falling and businesses are having trouble getting their hands on supplies.

At 50.8 the services ISM index hit a nine-month low and sits only marginally above the 50-line designating expansion from contraction. The measure for business activity was higher, a modestly positive development even if it was somewhat out of synch with an otherwise downbeat take on the current state of the service sector.

While tariffs are targeted at goods imports, service-providers are not immune to uncertainly and tariff-related price pressure. (…) even as the prices paid metric fell in March for services, at 60.9 prices paid is still running at a rate consistent with a broad expansion input prices. It matches precisely the six-month moving average for prices paid, a period during which service price inflation has been particularly difficult for policymakers to get under wraps.

Orders and order backlogs both fell in March, for backlogs, the 4.3 point move takes that measure of pipeline business back into contraction territory. A purchasing manager in the wholesale trade industry spoke to how tariffs are certainly influencing behavior: “Tariff confusion and the variety of ways that suppliers are responding have had a strong effect on our purchasing decisions this month, causing us to shift spend and in some cases buy in advance of reported tariffs.” This is precisely the sort of Catch-22 that we envisioned months ago in our report Purchasing Manager’s Dilemma.

Ultimately just about everyone is trying to game out the impact of the litany of new tariff policies President Trump announced. In theory, it’s simple. If you shock any macroeconomic model with tariffs, you will get a stagflationary effect. The more tariffs, the larger the likely stagflation impulse.

In plain English the idea centers around the fact that tariffs raise costs for domestic importers and in an effort to mitigate those costs, businesses cut expenses elsewhere, with labor potentially on the chopping block. Inflation up, unemployment up, stagnant growth.

The labor market has shown signs of stabilizing after the slowdown in the late summer months of last year, which had encouraged the Fed to kick off its easing cycle. But we wouldn’t classify the labor market as overly strong or sturdy at the moment. The services ISM employment component fell 7.7 points in March, or the most of any underlying component, to a contraction reading of 46.2.

The labor data remain mixed but are softening. Data on job cuts have increased in recent months, but initial and continuing claims for unemployment insurance remain within what are considered normal ranges. We find some comfort in the fact that labor is in short supply.We continue to hear anecdotally that businesses are struggling to find ‘qualified’ talent today, but small business hiring plans have come down in recent months.

Source: Institute for Supply Management and Wells Fargo Economics

(…) Ultimately, while we still look for a few factors to have been supportive of employment last month, such as a rebound in leisure & hospitality hiring and the conclusion of a couple strikes, the March ISM readings point to payroll employment slowing below 100K as soon as the April jobs report.

The data may be different in some respects but the narrative is similar:

- Cold and then warm weather makes demand readings iffy but S&P’s “only mild capacity pressures” and ISM’s “pipeline business back into contraction territory” are not suggestive of strong demand.

- The ISM services employment component cratered 7.7 points into contraction territory indicating that larger firms are de-risking.

- Pipeline costs are surging across the economy but “competitive pressures and efforts to sustain demand served to limit output price inflation”. Good news (contained inflation), bad news (margin pressures). One certainty, demand is softening.

Canada: Severe drops in activity and new business recorded in March

Canada’s service sector economy endured in March its steepest cuts to activity and new business since the height of the COVID-19 pandemic. Tariff concerns, which led to a retrenchment of client spending, weighed on market demand and subsequently sector performance. With the outlook also extremely uncertain, confidence about the next 12 months fell to a near five-year low. Modest job losses were also registered.

Cost inflation meanwhile accelerated noticeably, but a challenging market environment meant service providers chose to broadly not pass on higher operating expenses to clients.

Euro area economy expands modestly in March

The eurozone private sector economy eked out another expansion in March, rounding off the first quarter of 2025 with a third successive monthly increase in business activity. Albeit the strongest since August 2024, the upturn was only modest overall and weaker than the long-run trend of the survey. Greater output volumes came despite a further contraction in new work intakes, although employment rose for the first time since last July.

Price pressures faded slightly during the latest survey period, with both input costs and output prices rising at their softest rates in 2025 so far.The seasonally adjusted HCOB Eurozone Composite PMI® Output Index – a weighted average of the HCOB Manufacturing PMI Output Index and the HCOB Services PMI Business Activity Index – ticked up to 50.9 in March, from 50.2 in February, marking a third successive month in which the headline figure has posted in expansion territory (a reading above 50.0). Additionally, the index hit its highest level since August last year, signalling the quickest rate of growth in seven months. That said, the expansion was only modest overall and was weaker than the long-run trend of the survey (52.4). (…)

The HCOB Eurozone Services PMI Business Activity Index ticked higher in March to 51.0, from 50.6 in February, to signal a slightly faster pace of expansion in output.

New business volumes were down marginally again March, as was the case in February. Non-domestic markets were an area of weakness, with export sales falling at a quicker pace. Higher output and lower new orders meant that services companies cleared backlogs at a faster rate. The rate of depletion was the quickest in just over four years.

China: Services activity growth accelerates to three-month high

The headline Caixin China General Services Business Activity Index posted 51.9 in March, up from 51.4 in February. Scoring above the crucial 50.0 no-change mark for the twenty-seventh month in arow, the latest reading signalled another expansion of services activity in China. While modest, the rate of growth was the most marked since last December.

Higher new business inflows underpinned the latest improvement in services activity growth. The pace at which new orders rose was the quickest in three months, aided by supportive policies, marketing efforts and a broad improvement in demand conditions, according to panellists. The latest data indicated that the expansion of total new business stemmed mainly from firmer domestic demand, as the volume of new export business was unchanged in March.

Panellists also mentioned improvements in business efficiency at the end of the first quarter, which supported a third monthly reduction in the volume of backlogged work. That said, the rate of depletion remained marginal overall. Signs of spare capacity contributed to a renewed drop in employment in March. The pace of job shedding was the quickest in nearly a year, albeit modest.Some service providers also reported reducing their headcounts amid cost concerns.

Indeed, average input prices rose in March after falling fractionally in the prior month. Panellists often mentioned higher staff expenses and greater supplier charges as key factors driving inflation. That said, the rate of input price inflation was only marginal. Services firms generally opted to absorb any cost increases and lowered their charges for a second straight month.While only slight, the rate of discounting was the most pronounced in six months. Heightened market competition placed pressure on services firms to lower their selling prices to support sales, according to anecdotal evidence.

Overall, business sentiment in the Chinese service sector remained upbeat in March. Panellists often hoped that supportive domestic policies and business development efforts will boost sales and output in the next 12 months. Although still above the average recorded over 2024, the level of business confidence moderated from February, with some firms expressing concerns over theg lobal economic and geopolitical outlooks.

DEAL OR NO DEAL?

Ed Yardeni:

The worst-case scenario is a recession if high tariff rates stick, leading to a slowdown in business and consumer spending that cause layoffs. We raised our odds of a stagflation/recession scenario from 35% to 45% on Monday.

I hope these reciprocal tariffs get negotiated down and don’t trigger a 1930s-style tit-for-tat trade war. We’re hoping the art of the deal is still what motivates the president.

Art of the deal? ![]()

Resistance Is Futile, Make a Deal: Trump’s Tariff Message to the World Administration is trying to head off painful retaliatory measures, forcing big trading partners to decide whether fighting is worth it

Leaders from Canada, Europe and China are threatening stiff countermeasures against the U.S. in response to President Trump’s surprisingly steep tariffs on nearly all imports. The administration’s response is, don’t even think about it.

Trump is trying to short-circuit the trade war’s cycle of retaliation by threatening massive new tariffs on any country that responds, and by dangling the prospect of a better deal for those who hold their fire and negotiate. The highest tariffs—the so-called reciprocal duties for many countries with goods-trade imbalances with the U.S.—don’t go into effect until Wednesday, giving world leaders time to plead their cases with a president who considers himself a master dealmaker.

“Every country’s called us,” Trump told reporters Thursday. “That’s the beauty of what we do. We’re in the driver’s seat.”

Will he make deals to lower tariffs? “It depends,” Trump said. “As long as they are giving us something good.” (…)

Administration officials have indicated that Trump isn’t willing to budge on the broad outlines of his trade policies. Almost every import will now be subject to at least a 10% tariff, a level that officials described as a floor. But there is negotiating room regarding the higher tariffs on select countries that have large trade surpluses with the U.S. (…)

So far, much of the world is holding out hope for a deal. Anthony Albanese, the prime minister of Australia, which has a free-trade agreement with the U.S. but now faces 10% tariffs, said his government wouldn’t join a “race to the bottom” by retaliating. Japan, which will be subject to 24% tariffs, didn’t immediately announce plans to retaliate. India, facing a 26% tariff, according to Trump’s executive order, indicated it had no plans to retaliate.

(…)

Late yesterday: “I think that maybe China will call and say, ‘well, we’re upset with the tariffs,’ and maybe they want to get something a little bit in order to get TikTok approved,” Trump said, while cautioning he had “no knowledge” that Beijing would seek that approach.

Today:

China Hits Back at Trump Tariffs with 34% Duties on All US Goods

China retaliated against new US tariffs with a slew of measures — including levies on all American imports and export controls on rare earths — delivering on a promise to strike back after President Donald Trump imposed duties and escalating a trade fight.

Beijing will impose a 34% tariff on all imports from the US starting April 10, matching the level of Trump’s so-called reciprocal tariffs on the world’s second-largest economy.

Chinese authorities also said they will immediately restrict exports of seven types of rare earths, start an anti-dumping probe into medical CT X-ray tubes from the US and India, and halt imports of poultry products from two American companies. Additionally, it’s adding 11 American defense companies to an unreliable entity list, and imposing export controls on 16 US firms.

The Rest of the World Is Bracing for a Flood of Cheap Chinese Goods President Trump’s ‘Liberation Day’ tariffs risk domino effect across the globe as Chinese goods look for new markets

President Trump’s jumbo tariffs on China threaten to create a new problem for a global economy already stressed over trade: a $400 billion deluge of Chinese goods looking for new markets.

U.S. consumers and businesses learned Wednesday that, from April 9, Chinese imports will face tariffs of around 70% on average, after Trump walloped China with stiff new duties as part of his “Liberation Day” trade broadside. The new tariffs will likely push up prices in the U.S. for products ranging from consumer electronics and toys to machinery and essential components for manufacturing.

That towering tariff wall also risks diverting some U.S.-bound Chinese exports into a global market already swimming in China-made goods, worsening a so-called China shock that is facing pushback from countries around the world, according to economists. Other major exporters, such as Vietnam, South Korea and Japan, could also see barriers to their exports proliferate as U.S. spending on imports falls and their exports get shunted to new destinations. (…)

Chinese imports will be slapped with a 34% duty. That new tariff rate was stacked on top of a 10% tariff levied in February, another 10% added in March and a range of other tariffs imposed during Joe Biden’s presidency and Trump’s first term in office. That lifts the average rate on Chinese imports to around 70%, according to economists.

It will be hard for other countries to absorb Chinese exports that normally went to the huge U.S. market. The U.S. in 2024 imported around $440 billion of goods from China, according to Census Bureau data. China in 2023 was the source of a fifth of iron and steel products imported into the U.S., more than a quarter of its imported electronics, a third of its imported footwear and three-quarters of its imported toys, according to data from the International Trade Centre, an agency of the United Nations and the World Trade Organization. Ninety-one percent of U.S. umbrella imports came from China. (…)

Here and there:

- The discordant result is that U.S. adversaries like Iran (10%) and Venezuela (15%) will pay lower rates than friends in Europe (20%), Japan (24%) and Taiwan (32%). BTW, Russia = 0.

- Mr. Trump hits Vietnam with a 46% tariff, which means Nike will have to rethink where to make low-margin shoes. Mr. Trump seems to think they should be made in America. Mr. Trump’s tariffs may have the U.S. investing to create jobs in shoe-making when it should invest in AI. This misallocation of capital will not make the U.S. more competitive against China.

- “He’ll be in a negotiation with every country,” said Steve Bannon, a former senior White House strategist who remains close with Trump and his aides. “Every day will be like Christmas. At the end of the day, what really excites him is talking about a deal with Canada, having Witkoff update him on Russia—the deals.”

- “The chips are starting very soon,” Trump said. “The pharma is going to start coming in, I think, at a level that we haven’t really seen before. We are looking at pharma right now. Pharmaceuticals. It’s a separate category. We’ll be announcing that sometime in the near future. It’s under review right now.”

- Trump’s justification hinges on a naive belief that treats trade imbalances as if they were the profit and loss account of a business, and not the culmination of highly specialised supply chains. He also considers factory work to be the fount of economic development, ignoring how decades of free trade has enabled America to rise up the industrial value chain and become a global leader in services and innovation. (FT)

- America’s now shut-out trade partners ought to focus on expediting free trade initiatives among themselves. After all, the US accounts for just 13 per cent of global goods imports, and with the exception of those in the White House, the economic imperative of comparative advantage continues to be widely understood. (FT)

- He’s gambling that generations of politicians, economists, CEOs, small-business owners, academics and even some of his own staffers are wrong — and that he’s right. Trump feels wholly confident he’ll be vindicated — if not instantly, then soon. Officials tell us he’s never felt more confident and happy than in pushing maximal tariffs, a lifelong aspiration.

- The president feels like a real estate mogul with a full inventory of mansions under his sole control, insiders tell us. Despite public comments, Trump sees this as maximal leverage to work the phones for weeks or months — cutting deals to force better terms for the U.S.

- Everyone around him — from top staff to top Republicans in Congress — fear disagreeing with him. Even if they had the stones to confront him, they seem convinced it’d be futile. They’re as all-in on Trump as Trump is on tariffs.

The greatest issue concerns the dollar. Relative to the rest of the world, US assets have boomed ever since the Global Financial Crisis and went into overdrive after the pandemic stimulus programs in 2020. At that point, America let the liquidity flow, and attracted massive flows from other countries into its stock market. Following Julian Brigden of MI2 Partners, you could call this “vendor financing.”

The growth in European holdings of US stocks has been breathtaking:

This has been helped by a virtuous circle. The flows push up the dollar, which increases the returns for foreign investors and fosters confidence that the US is unstoppable, thus drawing in more funds. It’s a classic example of what the hedge fund manager George Soros, mentor of US Treasury Secretary Scott Bessent, calls reflexivity, or the ability of the market to create its own reality.

The problem arises when something obtrudes. (…)

The profits European investors are still sitting on are considerable, and they’ll now have an incentive to take those profits, which could be needed for investing in a much more difficult trade war environment at home. US stocks, particularly Big Tech, have been a kind of piggy bank for the world. The risk now is that foreign investors will smash the piggy bank. For an idea of what’s at stake, look at Apple Inc., which stands to be grievously hurt by the new tariff regime. Its market cap almost touched $4 trillion three months ago. Now it’s nearly back to $3 trillion. (…)

If trade flows are going to fall, as is more or less inevitable if these tariffs are imposed for any period of time, the risk is that capital flows will have to follow. That’s bad for the US, which attracts masses of capital, but the danger is evident in this chart from London’s Absolute Strategy Research:

Capital can move much more quickly than goods can. The risk is that the virtuous circle will turn vicious and upend the US financial system.

BUY NOW, PAY LATER:

Americans Rush to Buy TVs, Soy Sauce, Lululemon Workout Gear Trump’s new tariffs spur some shoppers to stock up. ‘Now is the time to buy.’

(…) On the Bluesky social-media platform on Wednesday afternoon, Mark Cuban, the billionaire businessman and TV personality, suggested to his followers that they might want to start stockpiling. “From toothpaste to soap, anything you can find storage space for, buy before they have to replenish inventory,” Cuban said in a post. “Even if it’s made in the USA, they will jack up the price and blame it on tariffs.” (…)

“My dad used to call this going broke saving money,” (…)

Most Canadians Support Building an Oil Pipeline That Would Sidestep US Market

(…) Nearly all of Canada’s crude exports go to the US because of a lack of pipelines running to Canadian ocean ports. Even the pipelines that carry oil from Alberta to eastern Canadian refineries cross through the US on their routes, a potential vulnerability in a trade war.

The poll showed strong support for a new pipeline that would flow across Canada. Some 77% support or somewhat support the idea of the national government funding a pipeline’s construction, according to the survey. Just 15% are opposed or somewhat opposed, and the rest were unsure. (…)

{kind=link}