Note: I am currently travelling. Hence the more limited postings.

Note: I am currently travelling. Hence the more limited postings.

Trump Dismisses Affordability Concerns, Insists Prices Are Coming Down President says notion that GOP performed poorly in recent elections because of cost of living is Democratic ‘con job’

(…) Most prices are on the downswing, he argued.

“Our energy costs are way down. Our groceries are way down. Everything is way down. And the press doesn’t report it,” Trump said. “So, I don’t want to hear about the affordability. Because right now, we’re much less.”

Trump’s optimistic perspective on the economy is at odds with government statistics and the views of many voters, according to pollsters and analysts. The Labor Department reported last month that consumer prices rose 3% in September from a year earlier, marking the fastest pace since January. In recent surveys, voters said the cost of housing, groceries and utility bills is unmanageable. Democratic candidates who focused their messages on affordability came out on top in Tuesday’s elections, handily beating their Republican challengers. (…)

Rep. Marjorie Taylor Greene (R., Ga.) said in a recent interview with CNN, “Affordability is a problem.”

“I go to the grocery store myself. Grocery prices remain high. Energy prices are high,” she said. “My electricity bills are higher here in Washington, D.C., at my apartment, and they’re also higher at my house in Rome, Ga.—higher than they were a year ago.” (…)

The Federal Reserve’s anecdotal survey of the economy from October found that manufacturing activity varied across the country and that “most reports noted challenging conditions due to higher tariffs and waning overall demand.” (…)

This is not something Trump can hope to keep lying about to turn it into his reality.

Most Americans’ reality is that they are squeezed and worried about their jobs. They are also likely to see shortages of several Chinese goods in coming weeks, and more price increases.

![]() Bessent Says Trump’s $2,000 ‘Dividend’ May Come Via Tax Cuts

Bessent Says Trump’s $2,000 ‘Dividend’ May Come Via Tax Cuts

(…) Bessent said he hadn’t spoken to the president about this idea but “the $2,000 dividend could come in lots of forms, in lots of ways. It could be just the tax decreases that we are seeing on the president’s agenda — no tax on tips, no tax on overtime, no tax on Social Security – deductibility on auto loans.”

Hmmm…

Canada’s Second Monthly Job Surprise Reverses Recent Decline

The Canadian economy added 66,600 jobs in October, marking a second consecutive month of surprise employment gains as tariffs otherwise slow down economic activity.

The gains were driven by part-time positions, with growth in wholesale and retail trade, transportation and warehousing and information, culture and recreation. The employment increase helped bring down the jobless rate to 6.9%, Statistics Canada’s labor force survey showed on Friday.

Economists surveyed by Bloomberg were expecting the unemployment rate to hold steady at 7.1%, and for the economy to shed a modest 5,000 jobs.

The Canadian labor market also surprised to the upside in September, adding a healthy 60,400 positions. Taken together, the last two months reversed losses in July and August, and curbed some of this year’s labor market softness brought on by the US trade war.

With the jobs added in September and October, Canada overall gained a net 164,500 positions since January. The three-month moving average of job growth was 20,500.

The fact that the October employment gains were concentrated in industries that recently experienced job losses suggests the strong report may be a correction of past weakness, said Charles St-Arnaud, chief economist at Alberta Central.

“As a result, it seems unlikely that this trend will continue,” he said in an email. (…)

The labor force survey data is notoriously volatile, arguing against reading too much into any one report, Nathan Janzen, assistant chief economist at Royal Bank of Canada, told investors in a note.

“But details were also broadly positive with job growth concentrated in the private sector, improvement in the most trade-exposed manufacturing and transportation sectors, wage growth accelerating and the labor force participation rate rising,” he said, adding the report aligns with his bank’s expectation of no further rate cuts.

The increase in employment was concentrated in the manufacturing heartland of Ontario, where employment rose by 55,000, marking the first increase since June.

Annual wage growth for permanent employees rose to 4%, compared to economist expectations for a deceleration to 3.5%. (…)

China Consumer Prices Unexpectedly Rise on Holiday Demand

The consumer price index rose 0.2% from a year earlier, after a 0.3% decline in September, according to data released by the National Bureau of Statistics on Sunday. The median forecast of economists surveyed by Bloomberg was for a 0.1% drop. China’s core CPI, which excludes volatile items such as food and energy, climbed 1.2%.

Service costs also edged up 0.2% last month and contributed to the rise in inflation, according to the statistics bureau. Factory-gate deflation eased, despite persisting for a 37th straight month.

“The broad-based price increases likely reflect seasonal demand around the Golden Week,” Goldman Sachs Group Inc. economists wrote in a note. “Its durability remains to be seen.” (…)

A Bloomberg News analysis of almost 70 everyday products and services from multiple sources showed prices dropped more sharply than the headline Consumer Price Index indicates, especially for goods that ordinary consumers buy. (…)

The government has reduced its official target for consumer inflation to around 2% for this year, the lowest level in over two decades. Even so, price growth has been around zero or negative for much of 2025.

BTW, “China’s October import and export value growth declined and missed market expectations. In USD terms, export value dropped 1.1% yoy in October vs. +8.3% yoy in September, and import value grew 1.0% yoy in October vs. +7.4% yoy in September. We think the weakness was largely driven by fewer working days (18 in this October vs. 19 in last October) and a higher base last October.”

China Resumes Nexperia Chip Export, Urges EU to Make Progress

China on Sunday confirmed that it has taken steps to exempt compliant exports of Nexperia chips intended for civilian use, while urging the European side to make progress in resolving the clash that threatens to disrupt global auto production. (…)

A resumption of exports could set the stage for the Netherlands to lift government controls imposed on Dutch-based Nexperia, which is owned by Zhejiang-based communications equipment manufacturer Wingtech Technology Co. China had retaliated by restricting exports over components from Nexperia’s Chinese facility, which accounted for about half of its pre-crisis volumes.

Pressure has been mounting on the Netherlands to resolve the crisis, as automakers such as Volkswagen AG warned the impact of a global chip shortage. Honda Motor Co. recently slashed its annual profit forecast after halting production at several plants. (…)

Can the US break China’s grip on rare earths? Experts question Washington’s suggestion that it can end Beijing’s dominance of sector within two years

The US has claimed China’s dominance over rare earths is coming to an end, with Treasury secretary Scott Bessent telling the Financial Times in October that Beijing’s leverage over the metals would last no more than 24 months. (…)

But some observers have questioned Bessent’s two-year timeline, given the extent of China’s grip on the sector and the complexity and expense of building the mines and processing that will be needed to replace Chinese suppliers.

“Promises of a year or two are either naivety or spin,” said Tim Puko, director of commodities at the Eurasia Group consultancy. “There is no realistic way for the US to hit that target now.”

After half a century of under-investment and tighter environmental and permitting regulations, Washington is injecting funding into rare earths and critical mineral companies in the hope of catalysing the sector domestically. It has also sought to corral allies including Australia and Japan into rare earths deals.

“There’s a much greater understanding that this is a real issue geopolitically and also from a national security perspective and that this needs to be solved irrespective of temporary reprieves,” said Thras Moraitis, chief executive of Serra Verde, which is developing a Brazilian rare earths mine with US government funding. (…)

After signing the deal with Australia’s Prime Minister Anthony Albanese, Trump declared that “about a year from now we’ll have so much critical mineral and rare earth that you won’t know what to do with them”. (…)

Building a major new rare earths supply chain that cuts out China will take many years, experts say, making Bessent’s two-year timeline to build self-sufficiency highly optimistic.

The ratcheting up of Chinese export controls has, however, helped galvanise the US and its allies, which could accelerate the pace of development. Bringing a new mine to life is lengthy, risky and capital-intensive. Newly discovered deposits are studied for years before a final decision to build a mine, while projects are often slowed by long permitting processes. Raising the money to finance a mine is also challenging, meaning initial timelines frequently slip.

“Twenty-four months for a full detachment from the supply of Chinese rare earths and magnet materials is ambitious, and would require vast amounts of finance, permitting and education of the workforce to accomplish,” said David Merriman, research director at Project Blue.

Australia’s Lynas, the largest rare earths producer outside China, has warned that there is “significant uncertainty” about its planned processing facility in Texas, after wastewater management and permitting challenges added to costs.

Another question is how a new supply chain would survive financially. Even if mines, plants and factories are built, operators will need to compete with low-cost Chinese rivals.

Belgian chemicals group Solvay plans to start producing heavy rare earths in small quantities from 2026. But to “kick-start the value chain in Europe”, the group would need buyers and governments to “make sure that this investment makes sense and is profitable”, said CEO Philippe Kehren.

Meanwhile, German magnet maker VAC’s chief executive Erik Eschen told the FT he was concerned that China’s restrictions had led to a magnet stockpile that could “flood the market” and drive down prices should there be a US-China détente.

The US has few of the miners or refiners the administration wants, with only two players producing at scale, Energy Fuels and MP Materials. They have both pledged to materially increase their production of neodymium-praseodymium (NdPr), a light and commonly used rare earth compound that goes into magnets.

Last year the US imported about 7,000 tonnes of permanent magnets, according to import data. However, US consumption far exceeds that — with the motor industry alone requiring 42,000 tonnes a year. Two magnet makers in the US, Vulcan Elements and Noveon Magnetics, have said they plan to reach capacity of at least 10,000 tonnes a year. Vulcan said it would reach “significant volumes” by 2027, while Noveon’s current capacity is 2,000 tonnes.

A unit of Germany’s VAC, eVAC, expects to start shipping products this month from its new rare earth permanent magnet factory in South Carolina. “I want to ramp up before Christmas,” Eschen said, noting that carmaker General Motors was a customer.

Other projects are waiting in the wings. Among rare earth processors, Ucore Rare Metals broke ground on its separation plant in Louisiana this year and said in August it expected to be producing small quantities of material in 2026.

While a swath of companies in the US or with ties to the country have pledged to develop rare earth projects across mining, processing and magnet manufacturing, industry insiders say most remain speculative or uneconomic without stronger price signals.

“I do think that there’s room for a lot of other players and a lot of other supply, but to get to that in five or 10 years, you’re going to need materially higher prices,” said MP Materials chief executive James Litinsky.

EARNINGS WATCH

Corporate Earnings Were Great This Quarter. Wall Street Is Still Not Impressed. Four of five S&P 500 companies are beating estimates, but investors aren’t rewarding them for their performance

Of the 446 S&P 500 companies to report third-quarter results so far, more than 80% of them beat analysts’ estimates, according to LSEG I/B/E/S data. That is the biggest crop of outperformers since the spring of 2021. But no matter how many times those analysts might have uttered the words, “great quarter, guys,” in recent weeks, the message hasn’t reached stock investors.

The S&P 500 is only up 1.3% since Oct. 14, when JPMorgan Chase and other big banks kicked off the season with strong results. Furthermore, the median stock among S&P 500 companies that beat its earnings estimates bested the broader benchmark by only 0.3% in the day after it reported, according to an Oct. 31 report from Goldman Sachs analysts. The historical average, Goldman said: about 1%. (…)

“Investors were coming into earnings season more concerned that they might have overvalued stocks,” said Ed Yardeni, president of Yardeni Research. That meant good reports were more likely to be met with “a sigh of relief, more than a surprise,” he said. (…)

There are still some 54 S&P 500 companies on deck to share their results, including major retailer Walmart and AI poster child Nvidia. (…)

Well, there were actually not big, but huge surprises:

In aggregate, companies are reporting earnings that are 10.3% above estimates, which compares to a long-term (since 994) average surprise factor of 4.3% and the average surprise factor over the prior four quarters of 7.1%.

In aggregate, companies are reporting revenues that are 2.3% above estimates, which compares to a long-term (since 2002) average surprise factor of 1.3% and the average surprise factor over the prior four quarters of 1.5%.

The estimated earnings growth rate for the S&P 500 for 25Q3 is 16.8%. If the energy sector is excluded, the growth rate improves to 17.8%.

The estimated revenue growth rate for the S&P 500 for 25Q3 is 8.1%. If the energy sector is excluded, the growth rate improves to 8.7%.

The estimated earnings growth rate for the S&P 500 for 25Q4 is 8.0%. If the energy sector is excluded, the growth rate improves to 8.4%.

Not only tech:

Hence, upward revisions:

Encouraged by positive guidance:

Amazing earnings performances supporting expensive valuations on trailing EPS…

… but not quite as expensive using forward EPS:

Interestingly, since June, trailing EPS rose 5.1% and forward EPS 5.7%. Analysts are not getting carried away, are they?

Fast rising earnings amid stable inflation = rising Rule of 20 Fair Value (yellow line):

Tech earnings are up 28.5% so far in Q3, better than the previous 4 quarters:

“It seems like we have finally reached the point of maximum optimism around artificial intelligence,” said Sameer Samana, head of global equities and real assets at Wells Fargo Investment Institute. “We think it would be fair to describe the flurry of deal announcements, some of which at least seem both circular and lofty, have led to investor fatigue and some wariness.”

Have we?

NVDA comes Nov. 19. “Chief Executive Officer Jensen Huang of Nvidia, which is the primary AI chip supplier to major companies, said on Saturday his business is “growing month by month, stronger and stronger.” (Bloomberg)

FYI:

On Thursday, Tesla CEO Elon Musk suggested Tesla will need so many chips for its robots and self-driving cars that it might build its own chip factory. He also said Tesla would have to spend “tens of billions” to train the AI in its robot.

Musk told investors during Tesla’s annual meeting that he’s unsure how Tesla will get enough chips to power its self-driving and robot ambitions.

“Even when we extrapolate the best-case scenario for chip production from our suppliers, it’s still not enough,” he said.

Bitcoin (no earnings, no real world value) vs Nasdaq:

Sam Altman says OpenAI will top $20 billion in annualized revenue this year, hundreds of billions by 2030

(…) In September, OpenAI CFO Sarah Friar told CNBC that OpenAI was on track to generate $13 billion in revenue this year. (…)

Nice growth rate, but he’s on the hook for $1.4T. That is more than the combined annual EBITDA generated by the 10 biggest tech firms.

Venture capitalist David Sacks, who is serving as President Donald Trump’s AI and crypto czar, said Thursday that there will be “no federal bailout for AI.” He wrote in a post on X that if one frontier model company in the U.S. fails, another will take its place.

What about domino collateral damages? It can be argued that OpenAi is becoming too big to fail.

Altman said Thursday that OpenAI does “not have or want government guarantees for OpenAI datacenters.” He said taxpayers should not bail out companies that make poor decisions, and that “if we get it wrong, that’s on us.”

“This is the bet we are making, and given our vantage point, we feel good about it,” Altman wrote. “But we of course could be wrong, and the market—not the government—will deal with it if we are.”

Mark his words.

From Mexico to Ireland, Fury Mounts Over a Global A.I. Frenzy

Nearly 60 percent of the 1,244 largest data centers in the world were outside the United States as of the end of June, according to an analysis by Synergy Research Group, which studies the industry. More are coming, with at least 575 data center projects in development globally from companies including Tencent, Meta and Alibaba.

As data centers rise, the sites — which need vast amounts of power for computing and water to cool the computers — have contributed to or exacerbated disruptions not only in Mexico, but in more than a dozen other countries, according to a New York Times examination.

In Ireland, data centers consume more than 20 percent of the country’s electricity. In Chile, precious aquifers are in danger of depletion. In South Africa, where blackouts have long been routine, data centers are further taxing the national grid. Similar concerns have surfaced in Brazil, Britain, India, Malaysia, the Netherlands, Singapore and Spain. (…)

Many governments are eager for an A.I. foothold, too. They have provided cheap land, tax breaks and access to resources and are taking a hands-off approach to regulation and disclosures. (…)

In country after country, activists, residents and environmental organizations have banded together to oppose data centers. Some have tried blocking the projects, while others have pushed for more oversight and transparency.

In Ireland, authorities have limited new data centers in the Dublin area because of “significant risk” to power supplies. After activists protested in Chile, Google withdrew plans to build a center that could have depleted water reserves. In the Netherlands, construction was halted on some data centers over environmental concerns.

“Data centers are where environmental and social issues meet,” said Rosi Leonard, an environmentalist with Friends of the Earth Ireland. “You have this narrative that data centers are needed and will make us rich and thriving, but this is a real crisis.”

There are few signs of a slowdown. Companies are expected to spend $375 billion on data centers globally this year and $500 billion in 2026, according to the investment bank UBS. (…)

For two decades, Ireland rolled out the red carpet for tech. Apple, Google, Microsoft and TikTok made the country their European base, and about 120 data centers are clustered around Dublin and dot the countryside beyond. A third of the country’s electricity is expected to go to data centers in the next few years, up from 5 percent in 2015. (…)

In January, storms caused power outages across western Ireland, fueling debates over whether the grid was at a breaking point.

“There’s a reason why the grid is under strain, and it’s because of the disproportionate number of data centers,” said Sinéad Sheehan, an activist who organized a petition against the Ennis project that was signed by more than 1,000 people.

Ireland’s experience is a warning. By 2035, data centers globally are projected to use about as much electricity as India, the world’s most populous country, according to the International Energy Agency. A single data center can also use more than 500,000 gallons of water a day, nearly as much as an Olympic-size swimming pool.

Environmental groups worldwide are sharing information, tactics and resources to push back. (…)

Darragh O’Brien, Ireland’s minister for climate, energy and the environment, said construction was migrating to countries with the most welcoming policies. (…)

Government support worldwide has helped tech firms build with little accountability, said Ana Valdivia, an Oxford University lecturer studying data center development. Few environmental regulations were designed for data centers, and the companies often demand some level of secrecy from governments.

In Mexico, Mr. Sterling described an ambitious growth plan that would quadruple total electricity use from data centers to 1.5 gigawatts over the next five years, roughly the amount used by 1.25 million American homes. Nondisclosure agreements with tech companies were needed to win the deals, he said, and he was required to keep information from communities and Mexico’s electricity utility.

“I signed that NDA as a public service,” he said.

Project operators are often camouflaged through subsidiaries or outside contractors. In Mexico, at least one Microsoft data center is owned and operated by Ascenty, a Latin American data center company. In Ireland, the would-be Amazon data center was developed by a firm called Art Data Centres. (…)

Company representatives and government officials said new technology, including cooling systems that recycle water, was helping to solve the resource strains.

Data centers “use a lot of water, they don’t waste a lot of water,” Mr. Sterling said. (…)

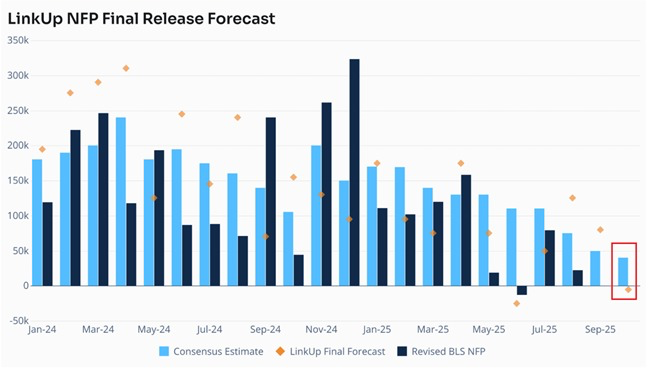

Data:

Data: