The Conference Board Leading Economic Index® (LEI) for the U.S. Increased in May

The Conference Board Leading Economic Index® for the U.S. increased 0.3 percent in May to 127.0 (2010 = 100), following a 0.2 percent increase in April, and a 0.4 percent increase in March.

“The U.S. LEI continued on its upward trend in May, suggesting the economy is likely to remain on, or perhaps even moderately above, its long-term trend of about 2 percent growth for the remainder of the year,” said Ataman Ozyildirim, Director of Business Cycles and Growth Research at The Conference Board. “The improvement was widespread among the majority of the leading indicators except for housing permits, which declined again. And, the average workweek in manufacturing has recently shown no sign of improvement.”

The Conference Board LEI for the U.S. continued to increase in May with positive contributions from all of its components except for building permits, which dropped sharply, and weekly manufacturing hours. In the six-month period ending May 2017, the LEI increased 2.3 percent (about a 4.7 percent annual rate), faster than the growth of 1.1 percent (about a 2.3 percent annual rate) during the previous six months. Also, the strengths among the leading indicators have remained more widespread than weaknesses.

The Conference Board CEI for the U.S., a measure of current economic activity, edged up in May. The coincident economic index rose 1.1 percent (about a 2.1 percent annual rate) between November 2016 and May 2017, the same pace of growth as over the previous six months. The strengths among the coincident indicators remain very widespread, with all components advancing over the past six months. The lagging economic index continued to increase at nearly the same pace as the CEI over the past few months, and as a result the coincident-to-lagging ratio is unchanged.

No recession in sight as per this chart from Doug Short. In fact, recession risks are diminishing.

So far in 2017, the consumer has kept the economic engine humming at slow speed, even if his real disposable income growth declined.

Real labor income growth is now being helped by rising wages and slowing inflation.

The decline in the unemployment rate coupled with rising wages, including minimum wage rates, has brought median household income above its 2000 level. Finally, the middle class could start to contribute.

See how the middle class household has been squeezed since 2000. While real income stayed essentially flat during 17 years, shelter cost rose 8% faster than total inflation, healthcare costs 28% faster and education costs 58% faster.

Add that energy costs had grown 57% faster than total CPI by December 2013 (currently +22%) and you can easily understand why Trump is in the White House and why the economy has been near stall speed throughout this recovery: the average American family simply has precious little money left for discretionary spending.

-

For Consumers, Less Debt but Lots of Bills As a group, U.S. households’ debt-to-income and debt-to-asset ratios in the first quarter fell to their lowest levels since the early 2000s. But financial obligations beyond debt payments, such as rents and auto leases, are taking a bigger bite out of pay.

(…) The Federal Reserve this week reported that households’ overall debt-service ratio—the share of after-tax income going toward debt payments—are near historic lows.

But Americans face financial obligations beyond debt payments, such as rents and auto leases, and these are taking a bigger bite out of pay. Indeed, the Fed report shows the share of income going toward non-debt financial obligations is sitting near its highest level since the 1980s. It is a development that particularly for households at lower income levels may be crimping spending.

Fed Up?

-

Fed’s Bullard Calls Officials’ Projected Rate Path ‘Unnecessarily Aggressive’ St. Louis Fed President James Bullard said he doesn’t see any need for further interest-rate increases but the central bank should begin shrinking its $4.5 trillion portfolio of assets “sooner rather than later.”

-

Fed’s Evans Says Rate Rise Could Wait Until December

-

Jobless Rate Falls to Record Low in California, Six Other States

-

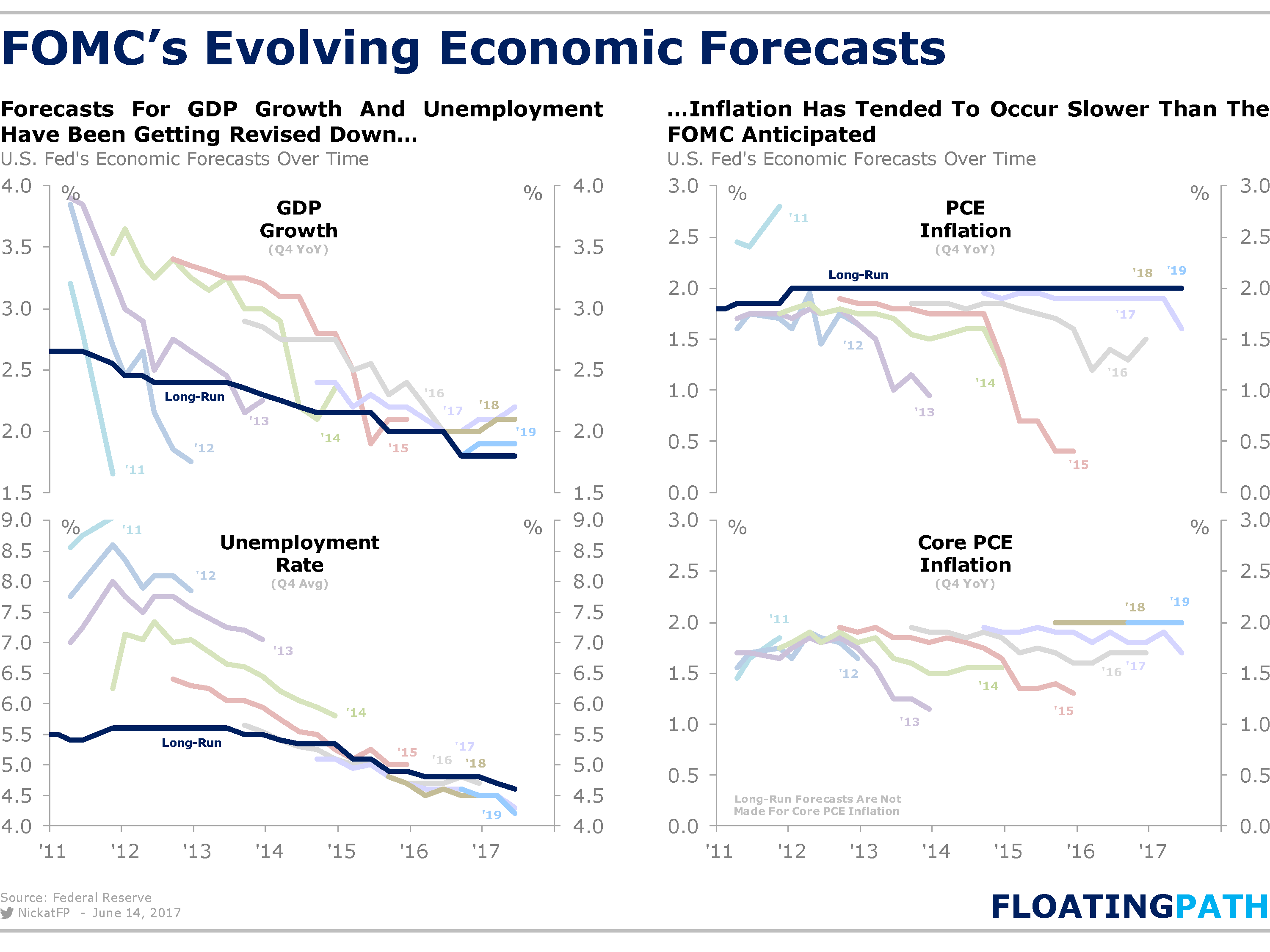

Hawks to More Than Just Talk on FOMC in 2018

(…) There are no names on the dot plot, but Bloomberg Intelligence Economics infers which projections correspond to each FOMC member based on a careful analysis of their public comments. (…)

The clustering of dots for 2017 shows a narrow range of potential fed funds outcomes at year-end, spanning a low end of 1-1.25 percent (the current level) and a high end of 1.50-1.75 percent. The median outcome, consistent with one additional 25-basis-point rate increase, is broadly supported by eight participants with even tail risks (by four participants each) favoring outcomes either 25 basis points higher or lower. (…)

There is some modest bias to the downside, but it appears to be a 6-3 voter split in favor of one versus no additional hikes.

(…) upon consideration of the dots likely corresponding to voting members of the FOMC in 2018, the potential range of outcomes is narrower than what a cursory glance would otherwise suggest. Importantly, contrary to the past few years, the bias is tilted in a more hawkish direction in 2018. While the overall median and median among voting members overlap at 2-2.25 percent, there are more outliers favoring faster normalization. (…)

It is instructive to match policy makers to dots in this way because the signals from voting members of the committee occasionally diverge materially from the overall results. Such is the case in 2018 — while the overall and voting medians overlap, the distribution of dots among voters is skewed to the upside.

This “hawkish skew” in 2018 is particularly noteworthy because Janet Yellen’s term as Chair and Stanley Fischer’s term as Vice Chair expire on February 3 and June 12, respectively. While their terms as Governors do not end until 2024 and 2020, they will likely choose to leave the Fed if not reappointed to their leadership positions. As such, two stalwart moderates could be removed from the dot plot, thereby tilting the bias in a significantly more hawkish direction. (Bloomberg Briefs)

Canadian Retail sales jump; signal best start to year since 1991

Consumers continued their free-spending ways in April, pushing retail sales to a 0.8 per cent gain from the prior month and bringing the total increase since the beginning of the year to 3.6 per cent, Statistics Canada reported Thursday. (…)

The gain in retail sales in April was powered by the country’s two biggest provinces: Quebec (1.6 per cent) and Ontario (1 per cent).

Excluding car and parts dealers, retail sales were up 1.5 per cent in April and has gained 4 per cent since the start of the year. That’s the best start on record.

The gains so far this year have been driven by actual new sales rather than price increases. Volume sales were up 0.3 per cent in April and the 3.3 per cent year-to-date gain is also a record start.

![]() Rolling 3-month annualized retail sales are up 8.1% in April!

Rolling 3-month annualized retail sales are up 8.1% in April!

Taiwan’s Foxconn Eyes Seven States for $10 Billion Investment Taiwan’s Foxconn Technology Group, which assembles Apple’s iPhones in China, is looking at seven states in the American heartland where it would invest $10 billion or more in factories to build flat-panel screens.

(…) Terry Gou, chairman of the company formally known as Hon Hai Precision Industry Co. , says the company will build out supply chains, a big boost for transportation and logistics providers in an industrial economy that’s lost some of its might in recent decades. Manufacturing reached a low of 11.6% of the U.S. economy in the last quarter of 2016, and the electronics industry has taken a growing share of the factory output. (…)

SamsungElectronics Co. is in late-stage discussions to invest about $300 million to expand its U.S. production at a South Carolina factory, the WSJ’s Timothy W. Martin reports, and would take over a site that Caterpillar Inc. is leaving. The decision is a boost for the Port of Charleston, which is about 150 miles away, and would draw in parts distribution as well as potential exports from the home appliances Samsung plans to produce. Samsung rival LG Electronics also plans to build a washing machine factory in Tennessee, its first major U.S. plant. Both companies are making a calculation that reining back logistics and shipping costs by producing appliances close to U.S. customers will more than offset potentially higher labor costs. More manufacturers may come to that conclusion if the new investments from Asia pay off.

Tesla Inc. says it is exploring with government officials in Shanghai opening a facility to build electric vehicles, and the WSJ’s Tim Higgins and Trefor Moss report the auto maker would make its signature cars there for the Chinese market while most of Tesla’s production would remain in the U.S. Tesla Chief Executive Elon Musk has said that making its vehicles in China would help cut prices for the vehicles by a third by reducing shipping costs and avoiding import duties. China production would bring new complications for Tesla’s supply chain, however, adding tough questions for a business that has struggled at times to ramp up production in line with sales. China’s regulations require vehicle components be sourced locally, pushing batteries from Tesla’s big Nevada “gigafactory” out of the picture.

IHS Markit Flash Eurozone PMI: Eurozone enjoys best quarter for six years despite growth slowing in June

- Flash Eurozone PMI Composite Output Index at 55.7 (56.8 in May). 5-month low.

- Flash Eurozone Services PMI Activity Index at 54.7 (56.3 in May). 5-month low.

- Flash Eurozone Manufacturing PMI Output Index at 58.5 (58.3 in May). 74-month high.

- Flash Eurozone Manufacturing PMI at 57.3 (57.0 in May). 74-month high.

Although the rate of growth waned to a five-month low, high order book inflows and elevated levels of business confidence meant job creation remained one of the strongest recorded over the past decade as firms continued to expand capacity to meet rising demand. Price pressures eased, however, largely reflecting lower global commodity prices.

At 56.4, the average PMI reading for the second quarter was above the reading of 55.6 seen in the first three months of the year and was the highest since the first quarter of 2011.

While the June survey showed manufacturing output rising at the steepest rate since April 2011, service sector growth waned to a five-month low, albeit still remaining robust to indicate a broadbased upturn.

Overall new order growth eased to the slowest in four months, reflecting weaker inflows of new business into the service sector. In contrast, factories reported the highest influx of new orders since February 2011, in part due to strong export sales. Overall exports (including intra-regional trade) continued to rise at one of the fastest rates seen over the past six years, buoyed by strengthening demand in key sales markets and recent euro weakness.

(…) Input cost inflation dipped to a seven-month low, easing especially markedly in the manufacturing sector due to lower prices for many commodities, notably oil. However, with supplier delivery delays worsening to the greatest extent for just over six years, the survey suggests that inflationary pressures persist in supply chains.

Slower growth was recorded in both France and Germany, down to five- and four-month lows respectively, largely reflecting weaker rates of service sector expansion. Headline PMI readings for manufacturing were the second-highest since April 2011 in both countries. Both nations nevertheless continued to record strong overall rates of expansion, with second quarter composite PMI averages above those seen in the opening quarter of 2017. There was greater variation in labour market trends: while jobs growth in Germany

slipped to a six-month low, employment rose in France at the steepest pace since July 2007.Growth eased across the rest of the single currency area for a second successive month, but the performances in terms of both business activity and hiring remained among the best seen over the past ten years.

Despite the June dip, the average expansion in the second quarter has been the strongest for over six years and is historically consistent with GDP growth accelerating from 0.6% in the first quarter to 0.7%.

Slower Eurozone Wage Growth Is Setback for ECB

The European Union’s statistics agency Friday said wages in the first quarter of 2017 were 1.4% higher than a year earlier, a smaller increase than the 1.6% recorded in the final three months of last year.

In Germany, where the calls for an end to ECB stimulus are loudest, wages rose by 1.9%, a slowdown from 2.8% at the end of last year.

The modest nature of the rise means wages lagged behind consumer prices over the same period, resulting in a drop in real incomes. (…)

The ECB’s economists expect wage rises to pick up over coming years. In new forecasts released last week, they see wages rising by 2.4% in 2019 from 1.7% this year.

China Passenger-Car Market Pulls Back Again

Passenger-car sales in the world’s biggest auto market dropped 2.6% to 1.75 million last month, the government-backed China Association of Automobile Manufacturers said Monday.

That performance followed a 3.7% decline in April, the sharpest since a mid-2015 slump, which prompted the government to slash its auto-sales tax to 5% from 10% to stoke demand. (…)

Passenger-car sales surged 16% in 2016, thanks in part to the government’s tax cut. But Beijing raised the tax back to 7.5% at the start of this year, sapping buyer interest in the early months of 2017.

Tighter liquidity controls are also making some Chinese banks reluctant to finance auto purchases, said Robin Zhu, an auto analyst with Sanford C. Bernstein, a research and brokerage firm. (…)

Sales of commercial vehicles in China increased 15% year-over-year in May to 345,000. The commercial vehicle market grew 18% in the first five months of 2017.

While total vehicle sales declined marginally in May by 0.1% year-over-year, they increased 3.7% in the first five months overall. (…)

But car dealers and auto makers are hoping for a year-end sales boost, as buyers try to make purchases before an expected tax increase to 10% takes effect.

-

Local auto brands in China are rapidly increasing market share but are still only 35% of the nation’s car market.

Source: Credit Suisse (via The Daily Shot)

-

Slowing credit growth in China should result in moderating economic activity.

-

-

Source: Capital Economics (via The Daily Shot)

Flash Japan Manufacturing PMI: Slower growth signalled in June

- Flash Japan Manufacturing PMI® down to seven-month low of 52.0 in June (53.1 in May).

- Flash Manufacturing Output Index at 52.1 (54.0 in May). Slowest growth for nine months.

- Exports rise further and job creation sustained.

Slower growth was signalled in June, with both orders and output rising at the weakest rates since late last year amid reports of a slight softening in market conditions.

That said, external demand is holding up well, and the sector continues to operate within a solid growth range. This is helping support employment gains, whilst also

enabling firms to pass costs on to clients to the greatest degree in over two-and-a-half years.

M&A’s widening lead over profits reflects an aging upturn

M&A’s latest surge comes with a warning. When M&A previously soared above pretax operating profits in 2007 and 1999-2000, a business cycle downturn was fast approaching. Thus, concerns about the adequacy of organic revenue that currently drive M&A also suggest that the upturn’s momentum may be waning. (Moody’s)

From the FT:

(…) “The economy is doing very well, is showing resilience,” said Fed Chairwoman Janet Yellen at a news conference following the Fed’s two-day policy meeting.

(…) “The economy is doing very well, is showing resilience,” said Fed Chairwoman Janet Yellen at a news conference following the Fed’s two-day policy meeting.

{kind=link}