SMALL BUSINESS “OPTIMISM” CHARTED

These are the big job creators and they are not in good shape nor in good mood.

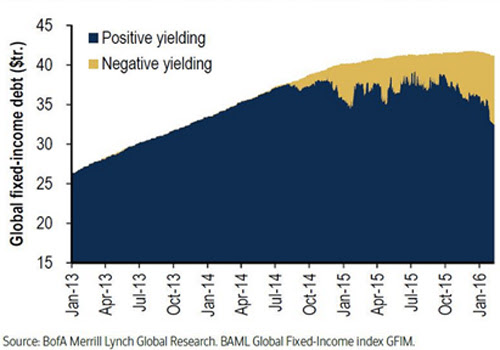

THE BIG SQUEEZE!

THE BIG SQUEEZE!

This is the biggest margin squeeze in 30 years:

Something’s got to happen soon: either prices go up or employment comes down.

Deflation Is Coming To The Auto Industry As Used Car Prices Drop, Off-Lease Deluge Looms

Last week, we learned that vehicle leasing as a percentage of monthly light-vehicle sales hit a record in February at 32.3%.

In other words, a third of the over 1 million cars and light trucks “sold” during the month were leases, according to J.D. Power. (…)

Of course the thing about leased vehicles is that they come back, and as WSJ wrote last week, “about 3.1 million vehicles will return to dealer lots off leases this year, up 20% from 2015 [and] the number will climb to 3.6 million in 2017 and 4 million in 2018.”

So what does that mean for dealers? Deflation.

And what does that mean for the automakers? Hefty losses.

Nothing about this is hard to understand. You get a supply glut causing pricing assumptions for your existing inventory to prove wildly optimistic and you end up with giant writedowns.

This has happened before. “The auto industry expanded the use of leasing in the mid-1990s, helping to fuel retail sales of new vehicles,” WSJ recounts. “Eventually, a glut of off-lease cars sent resale values down and auto lenders who had bet residuals would remain high ended up racking up billions of dollars in losses, having to sell the cars for much less than they anticipated.” (…)

The Manheim Used Vehicle Value Index posted its largest Y/Y decline in over two years last month, falling -1.4% and -1.5% M/M. We’re now 3.5% below the peak. (…)

And of course falling used car prices means pressure on new car prices as well, which would be a shock to America’s booming auto market. (…)

Bonus chart: largest used car price decline for any February since 2008

Foreign Buyers Are Pulling Back, Realtors Say Demand from foreign buyers is weakening, the National Association of Realtors said Monday, undermined by a strong U.S. dollar and rising home prices.

(…) In fact, there is growing evidence that many foreign buyers have been pulling back, in part because prices in many of the cities they favor, such as New York and San Francisco, have risen sharply. The affordability of those properties is weakened further by a stronger U.S. dollar.

In January, the median price of existing U.S. homes had increased 67% for a buyer from Brazil, factoring in the exchange rate, compared with a year earlier, according to NAR. For a buyer from Canada, it increased 27% and for a Chinese buyer, 14%. (…)

Foreign buyers remain a small sliver of the U.S. housing market. But any pullback could have a disproportionate effect on demand for high-end condos in places like Miami and Manhattan and luxury homes in Southern California. (…)

Fed Likely to Stand Pat on Rates, Keep Options Open for April or June Amid uncertainties about inflation and global growth, Federal Reserve officials are likely to hold short-term interest rates steady at their policy meeting next week but keep open options to move in April or June.

The IMF Is Sounding the Alarm. Is Anyone Listening? Few major economies seem to be hearing the International Monetary Fund urging action.

“The IMF’s latest reading of the global economy shows once again a weakening baseline,” the fund’s No. 2 official, David Lipton, warned Tuesday in a speech to the National Association for Business Economics.

While the world economy is still expanding, he said, “we are clearly at a delicate juncture, where risk of economic derailment has grown.” (…)

IMF Managing Director Christine Lagarde said a coordinated effort was needed, urging governments with room in their budgets to ramp up spending and all countries to accelerate delivery of long-promised economic overhauls.

Unlike the G-20’s massive joint-stimulus effort in 2009 to combat the financial meltdown wreaking havoc across the globe, IMF members are at odds about the severity of the problem and how to fix it.

“We are strictly against announcing publicly that the G-20 is preparing a stimulus program,” German officials privately told other countries as the group drafted its joint communiqué.

The IMF fears such an attitude risks jeopardizing the global economic expansion. (…)

RECESSION WATCH

The outlook points to easing growth in the United Kingdom, the United States, Canada and Japan. Similar signs are also emerging in Germany. Stable growth momentum is anticipated in Italy and in the Euro area as a whole. In France, and India, CLIs point to stabilising growth momentum. The outlook for China remains unchanged from last month’s assessment, pointing to tentative signs of stabilisation, while in Russia and Brazil the CLIs point to a loss in growth momentum.

Forward-looking indicators for the global economy fell sharply for the month of February. The JPMorgan Global Manufacturing PMI (in blue) is now resting at 50, which is the key threshold separating expansion from contraction. At the end of last year, the services measure (in red), which increasingly comprises a larger share of global GDP, was sitting comfortably above contractionary territory near 53 and was as high as 55 toward the first half of last year. It has now fallen steeply to 50.7 and shows the global economy is on a much weaker footing compared to last year (all charts below courtesy of Bloomberg).

In the next chart we take a look at the recent bounce in commodities and oil. As you can see, it’s all about the dollar. Here we’ve plotted the trade-weighted broad dollar index (inverted, in green) next to oil (in black) and commodities (in red). The correlation between the three is quite striking. If you are betting on oil and commodities to move higher, then you are betting on the dollar to weaken from here.

Do credit card delinquency rates help predict the onset of recession? See for yourself. Here are three measures we are watching that have a fairly high correlation over time, which also help to signal economic downturns. Credit card delinquency rates appear to be forming a bottom similar to 2005-2006, but the most troubling are delinquency rates on commercial and industrial loans (in blue), which are now clearly trending higher. In terms of the last economic cycle, this appears more similar to where we were in 2007.

Financial conditions in the US turned decidedly positive in the third quarter of 2012 and remained so until turning decidedly negative in the third quarter of 2015. The recent market rally off the February lows was unable to lift financial conditions back into favorable territory.

An area that strategists are closely watching for signs of improving or worsening financial conditions is the high yield market. High yield corporate bonds for each of the 10 major sectors have traded flat to negative since last year, with energy seeing the greatest damage. All 10 sectors of the high yield market are now rallying from their lows. Can this be sustained? Time will tell.

Here’s another look at corporate spreads, both high yield and investment grade, compared to the S&P 500. Credit spreads were narrowing from 2012 until around 2014-2015 when they started to widen and signal greater pressure on the market. Echoing the chart above, they’ve since backed off their highs though it’s unclear whether this is a change in trend or simply a pause before heading higher.

On a more positive note, initial jobless claims are not yet raising a recessionary red flag for the US. This agrees with the overall message coming from broad US leading economic indicators like the Conference Board’s LEI (see here). We continue to watch the LEIs closely for signs of further deterioration or, conversely, a turnaround, however unlikely that may seem.

Citigroup warns of fall in revenues Forecast sets scene for lacklustre results in banking sector

John Gerspach, chief financial officer, forecast that revenues at Citi’s investment banking operation would drop about a quarter in the first three months of the year compared with 2015.

Fixed income and equities trading revenues would be down about 15 per cent, he added.

His forecasts come a month before bank results season gets under way. Shares in Citi, the fourth-largest US bank by assets, fell 3.7 per cent to $41.04 on Tuesday. Losses for the year so far stand at 21 per cent. (…)

Seasonal factors — investors tend to place more orders in January as they set their annual investment strategies — traditionally makes the first quarter a strong period for securities businesses. (…)

Investment banking — which includes debt and equity underwriting — had a “tough first quarter”, the Citi finance chief said. Mergers and acquisitions had a “tough comparison” with the same period a year ago.

“There’s probably some hope that we would recapture some of that in the last three quarters,” he said. “But it’s been a tough first quarter.”

Last month Edward Pick, Morgan Stanley’s head of trading, said the year “started out OK” but “it’s been a lot choppier since then”.

Daniel Pinto, head of JPMorgan’s corporate and investment bank, forecast first-quarter investment banking revenues would be down by about 25 per cent from last year. Trading would be down about a fifth, he said.

The latest downbeat forecast will raise concerns about further job cuts and pay levels at investment banks. (…)

What Doesn’t Kill Bull Market in S&P 500 May Make It Stronger

“How low can stocks go,” the Wall Street Journal wondered on March 9, 2009, as the financial crisis was wiping away trillions of dollars from American equities, the deepest rout since the Great Depression.

That day, of course, marked the bottom. The bull market that celebrates its seventh anniversary today has restored $14 trillion to stock values, pushing up the Standard & Poor’s 500 Index by almost 200 percent. (…)

Now, investors are awash in angst, showing little faith the run can continue. They worry about contracting corporate earnings, slowing Chinese growth and uncertainty over interest rates. And they’re walking the talk by pulling cash from stocks at almost the fastest rate on record. (…)

Investors took out almost $140 billion from equity mutual and exchange-traded funds in the last 12 months, more than double the peak outflows experienced over any comparable periods during the global financial crisis.

Yet when people withdraw money, stocks inversely tend to rise later, according to data since 1984. In the 12 instances when funds experienced monthly outflows that were at least 2 standard deviations from the historic mean, the S&P 500 rose an average 7.1 percent six months later, compared with a normal return of 3.9 percent, data compiled by Bloomberg and Investment Company Institute show. (…)

What happens next? Wall Street strategists see the bull market lasting at least through December, with the S&P 500 rising to 2,158, or an 9 percent increase from yesterday’s close, according to the average of 21 estimates compiled by Bloomberg. If the run lasts until the end of April, this bull will become the second oldest on record. Coincidentally or not, the last two ended near the eighth year of an election cycle. (…)

![]() May I humbly submit this post I wrote on March 2, 2009, S&P 500 Valuation Analysis: Near Bottom to be followed on March 3, 2009 with S&P 500 P/E Ratio at Troughs: A Detailed Analysis of the Past 80 Years, precisely to answer that question: “How low can stocks go”. To conclude that

May I humbly submit this post I wrote on March 2, 2009, S&P 500 Valuation Analysis: Near Bottom to be followed on March 3, 2009 with S&P 500 P/E Ratio at Troughs: A Detailed Analysis of the Past 80 Years, precisely to answer that question: “How low can stocks go”. To conclude that

- Trough valuation analysis shows trough S&P 500 Index levels at 720 using 2009 estimates, with a low probability downside risk to between 516 and 602.

- Valuation using the Rule of 20 method gives “trough” valuation of 791-923 for the S&P Index using current trailing earnings.

- Using 2009 operating earnings estimates, “trough” valuation would be 720-840.

- The worst case scenario, using the $43 estimate would bring trough valuation of 516-602.

The actual low was 666 on March 6, 2009.

(Note on the links: these posts under the old New$-to-Use site are more difficult to access and most if not all the charts have vanished into the blosgosphere ![]() .)

.)