U.S. Light Vehicle Sales Set New Record in 2015

Rising to 17.42 million units, they just beat the old record of 17.40 million reached in 2000, as gasoline prices and interest rates fell. The feat occurred despite a 4.6% m/m decline in December sales to 17.34 million (SAAR) from 18.19 million during November. It was the lowest level in six months. Nevertheless, sales rose 2.5% versus December 2014, pulling the full-year average up 5.4% against 2014. These gains were, however, the smallest of the economic expansion.

Sales of light trucks set the pace in 2015 with a 12.7% full-year increase to a record 9.69 million units. Their 55.7% share of total vehicle purchases also was a new record. The gain was led by a 25.3% surge in imported light truck sales to 1.37 million units, just off the 2007 record of 1.47 million. Not to be outdone, the 10.8% increase in sales of domestically produced light trucks pulled them to a record 8.33 million. During December, sales of imported light trucks fell 3.2% to 1.59 million. Nevertheless, they were 45.9% higher than December 2014. Sales of domestically produced light trucks fell 4.4% last month to 8.34 million (+8.1% y/y).

Passenger car sales during all of 2015 declined 2.5% to 7.72 million units, leaving them well below the 1990 high of 9.30 million. Sales of U.S. made cars eased 0.8% to 5.63 million while sales of imports fell 6.7% to 2.09 million. For December, passenger car sales declined 5.2% from November to 7.40 million (-8.7% y/y). Sales of domestically made cars fell 3.4% to 5.51 million (-5.5% y/y) while sales of imported cars were off 10.1% to 1.89 million (-17.0% y/y).

-

Younger Buyers Help Keep U.S. Car Sales Humming Auto makers reported highest annual sales volume in industry’s 125-year history

(…) In 2010, as the industry was rebounding from one of the worst years in the postwar era, J.D. Power estimates those born between 1977 and 1994 (the firm considers them Gen Y) made up only 17% of sales, or 1.6 million vehicles. Five years later, that number has grown to 28% of sales, or 3.3 million vehicles. The impact of baby boomers and Gen Xers on industry volume has flat lined or fallen back during that same period.

The average age of a new car owner fell in 2015, J.D. Power said, to 48 years old from 49. (…)

![]() But December sales were not great:

But December sales were not great:

And the cyclical breakout remains elusive (charts from CalculatedRisk):

But per capita sales are back in the 30-year channel as Doug Short illustrates:

We like to track sales of pickup trucks as they are often a sign of strength or weakness in the small business and construction sectors. Based on this idea, both appear to be doing well. In the latest release for December, Ford announced that sales of F-Series trucks totaled 85.2K, which represented an increase of 14.6% from last December’s total and the largest December y/y increase since 2011. This month’s sales total also makes this December the best month for Ford truck sales since 2005 and the third best December on record. To put this into perspective, sales in December 2015 were more than double the total of December 2008.

For all of 2015, sales of Ford F-Series totaled 780K, which is the strongest year for sales since 2005. In the year, sales of F-series trucks grew 3.5%, rebounding from 2014’s decline of 1.3% when sales were hampered by delays due to the redesign of the new F-150.

-

Big SUVs Fuel U.S. Production Boom The tables have turned for the U.S. auto industry and Arlington, Texas, is among the biggest winners, straining to meet demand for its hulking sport-utility vehicles despite running three production shifts a day.

-

U.S. Gasoline Prices Near Seven-Year Low

U.S. Apartment Vacancies Climb as New Buildings Crowd the Market

The national vacancy rate averaged 4.4 percent in the three months through December, up from 4.3 percent a year earlier and in the third quarter, the New York-based research company said Tuesday. Vacancies rose from the previous three months for a second straight quarter — the first time that’s happened since 2009.

Vacancies remain close to their lowest in more than a decade, with rising demand for older apartments in suburban locations keeping the national rate down. The surge in apartment construction since the recession has been largely confined to Class A properties, typically buildings close to city centers aimed at high-income professionals.

“It’s taking a lot longer for new projects to lease up,” Ryan Severino, a senior economist at Reis, said in a phone interview. “Vacancies are rising predominantly because a lot of shiny, sexy new Class A projects are having a harder time leasing up relative to a few years ago.”

Reis has recorded zero completions of new Class B and C apartments since 2012, following the addition of about 44,000 units from 2007 to 2011. Developers have delivered almost 1 million new Class A units since the beginning of 2007, according to the firm. (…)

The share of U.S. households that rent rose to 37 percent, the highest level since the mid-1960s, from 31 percent a decade ago.

Apartment rents rose 0.8 percent in the fourth quarter from the third, with asking rents averaging $1,229 a month, and effective rents — payments after any discounts, such as a free month — averaging $1,179, Reis said. While the increase “was a bit slower than the scorching performance during the last two quarters,” it “still represents an annualized rate in excess of 3 percent, well ahead of even core inflation,” Severino said in the report.

OIL

For almost 30 years, the kingdom has held the riyal at a fixed exchange rate and that has brought stability to government finances. Ninety percent of the government’s revenue comes from oil, which is priced in dollars.

But fewer dollars are coming in now, straining a budget that is committed to generous subsidies and public-sector wages. Abandoning the peg would make those dollars stretch further when converted to a local riyal, because without the peg, the riyal would weaken.

What’s more, to hold the peg, Saudi Arabia spends billions of its dollars buying riyals in foreign-exchange markets. (…)

Those reserves fell to $635.2 billion at the end of November, down 15% from a peak of $746 billion in August last year, according to the latest central bank data. (…)

Many economists said the Saudi government will keep spending dollars to avoid devaluation, which would come with uncomfortable long-term consequences. Households and businesses have debt in foreign currencies, and payments costs would rise if the local currency falls. Consumers also would have to pay more for imports, from cars to luxury goods.

That could be a tough path for the government, local analysts said. Saudis already are angered by cuts to subsidies in the state budget. (…)

In recent months, two oil-rich nations also have abandoned their dollar pegs.

Azerbaijan scrapped its peg to the greenback in December and its currency quickly lost half its value. Kazakhstan, another economy dependent on natural resources, let its currency float freely in August and saw it lose more than a quarter of its value in one day.

China has also moved to devalue the yuan since the summer as it grapples with slowing economic growth.

“The last year has shown us that when economic fundamentals change, pegs break,” saidPeter Kinsella, an emerging-market strategist at Commerzbank in London.

Let’s also say that the current Saudi leadership has not demonstrated much judgement in some of its key decisions, be it on its oil strategy or on its relationships with its neighbours and allies.

-

Sliding scale: fallout in the Gulf

Senior figures in Riyadh are unrepentant about their breach of relations with Iran following the ransacking of the Saudi embassy in Tehran; it has fallen to them, they argue, to forestall imperialist Persian mischief-making. The row, prompted by the Saudi execution of a Shia cleric, does not appear to be escalating: Kuwait, the latest country to follow the Saudi lead, has merely withdrawn its ambassador from Tehran, not broken off ties. As for other Arab powers, the Omanis and Qataris will do nothing. The real price will be paid elsewhere: chiefly in efforts to end the Syrian conflict. Last year’s big breakthrough was getting Iranians and Saudis to sit at the same table. At talks expected next month, that looks unlikely. Enmeshed in tension and conflict (notably with a costly military campaign in Yemen) the Saudis argue that things could hardly be worse. But outsiders see plenty of scope. (The Economist)

OPEC oil output fell in December, a Reuters survey found on Tuesday, led by lower supply from Iraq following a record-breaking month in November and smaller declines elsewhere in the producer group. (…)

OPEC supply fell in December to 31.62 million barrels per day (bpd) from a revised 31.79 million in November, according to the survey, based on shipping data and information from sources at oil companies, OPEC and consultants. (…)

OPEC has boosted production by almost 1.40 million bpd since its November 2014 refusal to cut supply and prop up prices. Output is not far below July’s 31.88 million bpd, the highest since Reuters records began in 1997.

The biggest monthly decline in output came from Iraq, the world’s fastest growing source of supply growth last year.

Exports from Iraq’s main outlet, its southern terminals, have slipped from November’s record level which had been boosted by delayed October cargoes, but are likely to reach new highs in the coming months, industry sources said. (…)

Top exporter Saudi Arabia has kept output steady to slightly lower, sources in the survey said, due to less demand from outside the country and largely steady domestic use. (…)

CHINA

-

Renminbi rates gap widens to record Speculation rises that Beijing intends to allow currency to depreciate faster

-

The Chinese devaluation threat — again (Gavin Davies)

(…) Some bears in the currency markets believe that China could soon be suffering from a genuine exchange rate crisis, in which its enormous foreign exchange reserves could be quickly drained.

That would indeed be a severe shock to global markets, since it would effectively export the deflationary forces that are overpowering the Chinese manufacturing sector to the rest of the world, and would probably require direct measures to restore the health of the Chinese financial system. But it still seems unlikely to happen, for now at least.

(…)

Admittedly, the PBoC did not give any formal commitment to keep the currency stable as part of the SDR talks and the IMF has explicitly argued that some flexibility in the medium term is desirable as the currency is increasingly determined by free market pressures.

However, many observers suspect that there was an informal “understanding” with the US (which, remember, still argues that the renminbi is undervalued) to eschew a sharp devaluation. China’s already strained economic relationship with the US would be ruined if it deliberately devalued so soon after its longstanding desire for SDR entry had been achieved.

What it does suggest, however, is that private sector capital outflows have been very large recently. Market sources reckon that private capital outflows may be running at $10bn a day, slightly more than occurred during the crisis last August. Official foreign exchange reserves have declined by $213bn, from $3,651bn last July to $3,438bn at the end of November, and will probably have dropped further when the December figures appear on Thursday.

In addition, China bears point out that the “errors and omissions” category in the official balance of payments data has risen by around $200bn since 2013, possibly indicating that the private capital outflow has been much larger than shown in the official data. These bears are beginning to convince themselves that the PBoC could soon run out of liquid foreign exchange reserves, making it impossible for them to continue supporting the currency.

But that seems rather fanciful. China’s foreign balance sheet remains extremely strong, and the central bank continues to have a huge foreign exchange war chest, should it choose to use it.

The big question, therefore, is whether the PBoC will in fact choose to keep the renminbi in its fairly stable band against the official basket. (…)

My expectation is that the Chinese authorities will seek to maintain their objective of broad stability against the basket. Recent Chinese activity data have been fairly encouraging (see the “nowcast” graph below), the current account of the balance of payments is in large and rising surplus, and a devaluation would undermine the key objective of rebalancing the economy away from moribund manufacturing sectors. It would also require a recapitalisation of the Chinese financial system, which has direct and indirect exposure to China’s $900bn foreign debt mountain. Finally, it would certainly inflame the Republicans, as well as some Democrats, in a US election year.

If this expectation is correct, then the PBoC will soon need to intervene on a large scale to reverse part of the recent depreciation — not to defend a particular exchange rate floor, but to prevent extrapolative expectations of devaluation from becoming self-fulfilling. If the central bank passively permits the renminbi to continue its downward drift, the situation could rapidly get out of its control.

This chart seems to confirm CEBM Research survey I mentioned yesterday:

Apple Suppliers Drop in Asia After IPhone Output Cut Report

Apple Suppliers Drop in Asia After IPhone Output Cut Report

Apple Inc. suppliers led by Sharp Corp. and Pegatron Corp. fell after Nikkei Asian Review reported the U.S. company would reduce the first quarter output of its latest iPhones by about 30 percent. (…)

Inventories of the new iPhones, which debuted in September, have piled up at retailers in China and Europe amid lackluster sales as an increase in the dollar against emerging markets currencies makes the device more expensive in those countries, Nikkei reported. Apple had initially told suppliers to keep production of the iPhone 6s and 6s Plus models for the January-March period at the same level as for their predecessors, the publication said. (…)

“With poor end demand for iPhone 6s in developed markets, we estimate that the supply chain has accumulated 20 million units of iPhone inventory including finished goods and components,” Ken Hui, an analyst at Jefferies Group LLC in Hong Kong, wrote in a report.

SENTIMENT WATCH

-

No End to the S&P 500 Slide In Sight: Analysis

-

S&P 500 May Enter Bear Market in 2016 as Swings Grow, UBS Says

After a weak start to 2016, the Standard & Poor’s 500 Index will reach a top in the second quarter, before falling as much as 30 percent later in the year or early in 2017, according to UBS technical strategists led by Michael Riesner. The Dow Jones Transportation Average has already entered a bear market, and the Russell 2000 Index of smaller companies has fallen 14 percent from its high last year.

“We are definitely more in the late stages of a bull market instead of being at the beginning of a new major breakout,” the strategists wrote in a note dated Jan. 5. “Our key message for 2016 is that even if we were to see another extension in price and time, we see the 2009 bull cycle in a mature stage, which suggests the risk of seeing a significant bear cycle event in one to two years.” (…)

The strategists note that the S&P 500 and Dow Jones Industrial Average are in the advanced stage of a so-called Elliott Wave pattern, indicating that after a final rally driven by mega-caps that could send the S&P 500 to 2,300, equities will fall. However, they forecast that the underlying bull market will then resume and last until the end of the decade.

![]() David Rosenberg:

David Rosenberg:

- At no time in the post-WWII era did the S&P 500 and the TSE decline in back-to-back years absent a U.S. recession – and a U.S. recession is still a very low-odds scenario (10% max).

- (…) the most important development in 2015 was that Consumer Discretionary stocks were the S&P 500 leader. This is a group after all that represents 70% of GDP. There have only been three times in the past where consumer cyclicals led the stock market – 1975, 1988 and 2001. In the subsequent year, real GDP growth nearly doubled to 3.6% from 1.7% on average.

EARNINGS WATCH

The Q4 earnings season officially launches next week but we already have 17 S&P 500 companies having reported: 76% beat with a +3.6% surprise factor. Six Consumer Discretionary companies have reported and 83# beat with a +7.0% surprise factor.

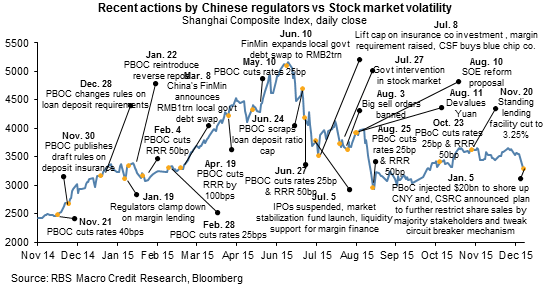

CHINESE LAISSEZ-FAIRE

From Alberto Gallo at RBS (via FT Alphaville):

(…) The real question is: will Gallo have to change the scales on that chart soon to generate more space?

You’d bet yes. As Balding said earlier today, “As with virtually all Beijing economic and financial policy, they are content to let the market play the dominant role if, and this is a big if, if the market does what Beijing wants it to do.”

El Nino Is So Last Year, Here Comes La Nina to Wreak More Havoc

As the effects of the most severe El Nino in almost 20 years still reverberate around the world, preparations are already under way for La Nina. (…)

El Nino is a warming in the equatorial Pacific Ocean, while La Nina is a cooling of the waters. Each can impact agricultural markets as farmers contend with too much or too little rain. A large part of the agricultural U.S. tends to dry out during La Nina events, while parts of Australia can be wetter than normal.

The previous La Nina began in 2010 and endured into 2012. Conditions typically last between 9 months and 12 months, while some episodes may persist for as long as two years, according to the National Oceanic and Atmospheric Administration. Both La Nina and El Nino tend to peak during the Northern Hemisphere winter.

North Korea’s Hydrogen Bomb Claim Disputed by Weapons Experts

South Korea’s spy agency said the test may not have been of a hydrogen device, according to Lim Dae Sung, an aide to lawmaker Lee Cheol Woo who was briefed by the National Intelligence Service. The yield and the seismic wave from the earthquake triggered by the explosion Wednesday were lower than in the reclusive nation’s previous test in 2013, Lim said. (…)

The test likely had a yield of between 1,000 and 30,000 tons of TNT — a similar level to its last test in 2013, according to Li Bin, a senior associate focused on nuclear policy at the Carnegie Endowment for International Peace. The yield — comparable to that of the atomic bomb dropped on Hiroshima — fell well short of the destructive power of a hydrogen bomb, which would equal at least a 50,000 tons of TNT, Li said.

“It’s more like an ordinary atomic bomb test, not a hydrogen bomb,” he said. (…)

Guns and glory: Oregon’s stand-off

Guns and glory: Oregon’s stand-off

The hoverboard-riding, craft-beer-sipping urbanites of the Beaver State’s largest city, Portland, have shaped its public image. But 300 miles (480km) to the south-east, something still more exotic is on display. An armed band, calling itself Citizens for Constitutional Freedom, has occupied the local headquarters of the Malheur National Wildlife Refuge, demanding clemency for two people convicted of arson on federal land, and an end to government control of the area. The ringleader, Ammon Bundy, is the son of Cliven Bundy, a Nevada rancher who rallied hundreds of armed supporters in 2014 in a dispute about payment for grazing rights. In 2015 a group of Oath Keepers (retired law-enforcement officials claiming to defend the constitution) took on the federal authorities over an Oregon mining claim. The feds usually wait for heavy rain to disperse such folk. Under a stout roof paid for by federal taxes, the Citizens may take longer to dislodge. (The Economist)