Inflation Pickup Makes Fed More Likely to Raise Rates Next Year Consumer prices are rising at their strongest 12-month pace in three decades

The Labor Department reported Wednesday that consumer prices rose strongly in October, up 0.9% on a seasonally adjusted basis from the prior month. Over the last 12 months, inflation is up 6.2%. So-called core prices, which exclude food and energy items, rose 4.6% over the past year. Both are the largest annual increases in more than 30 years. (…)

The rise in core prices over the past year is in line with unit labor costs, a key measure of compensation for U.S. workers, which rose 4.8% in the third quarter from a year earlier.

(…) data suggest price pressures are broadening to a wider range of goods and services as rising shipping and commodities costs feed through the economy. (…)

U.S. bond market expectations for inflation ticked up after Wednesday’s report, as did prices in futures markets indicating the Fed would raise rates at its meeting next June.

St. Louis Fed President Jim Bullard said on Tuesday he was worried an “inflationary process” had started over the last six months. “There’s a case to be made that inflation is going to be mostly transitory and dissipate, but you can only put so much probability on that scenario,” he said. (…)

More data:

- October’s core CPI was up 0.6% MoM, +7.3% a.r.. Coming after +0.10% and +0.24%, the slowdown thesis has been put aside.

- Core Goods inflation jumped 1.0% last month after +0.3% and +0.2%. Last 3 months: +6.1% a.r..

- Core Services: +0.4% after +0.0% and +0.2%. Last 3 months: 2.4% a.r. but a disturbing trend. Rising wages being passed on?

- Shelter: +0.5% after +0.2% and +0.4%. Last 3 months: 4.5% a.r..

Now look at the essentials of life:

- Food-at-Home: +5.4% YoY but +10.8% a.r. in the last 3 months. Energy: +30.0% YoY. Rent of primary residence: +2.7% YoY but +4.9% a.r. in the last 3 months.

Now, forget these essentials:

- All items less food, shelter, and energy: +5.3% YoY, +3.6% a.r. in the last 3 months.

- All items less food, shelter, energy, and used

cars and trucks: +4.0% YoY, +4.0% a.r. in the last 3 months. - Goods less food, energy, and used

cars and trucks: +5.5% YoY, +7.8% a.r. in the last 3 months.

Inflation is now here, there and everywhere. Deflating average hourly earnings, workers’ real take-home-pay still looks on trends…

…but that is because of the statistical compositional quirks during the pandemic. Using a composition-adjusted series, the average worker is now starting to feel the inflation pinch:

So far, there is no visible impact on nominal spending as the Chase spending tracker shows through Nov. 5.

US inflation again exceeded expectations by a wide margin. Headline and core rates are now at 30-year highs with near-term momentum suggesting 7% is possible. Pipeline price pressures show little sign of abating and inflation expectations are climbing as well, leading us to conclude QE tapering will be accelerated and rate hikes will come sooner. (…)

With the economy set to grow 6%+ annualised in this quarter and inflation set to persist at 6%+ through 1Q why does the Fed need to keep stimulating? The November FOMC statement said the committee “is prepared to adjust the pace of purchases if warranted by changes in the economic outlook” and if this backdrop doesn’t justify QE taper concluding early we are not sure what will. (…)

The Federal Reserve continues to assert that “longer term inflation expectations remain well anchored at 2 percent”, but consumer surveys suggest this is looking increasingly tenuous. The Federal Reserve’s own survey (conducted nationally by the NY Fed), shows 1Y ahead inflation consumer expectations rising to 5.7% – not really surprising as it tends to track actual inflation. However, the 3Y ahead inflation expectations rose to a new all-time high of 4.2%. We wouldn’t be surprised to see the University of Michigan 5-10Y ahead expectations break-up toward 3.5% in the next few months.

It is a similar story for market inflation expectations using Treasury index protected securities. They are now show 3%+ inflation out to 7 years maturity with even the 10Y up at 2.7%.

")

")

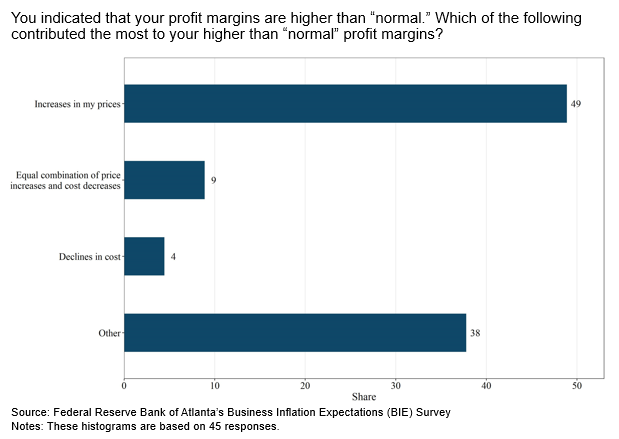

- 58% of surveyed firms say their unit costs are “up significantly” or “up very significantly”, from 45% last July. The percentage “up very significantly” is 32%, from 17% last July.

- “Projecting ahead over the next 12 months, how do you think the following five common influences will affect the prices of your products and/or services?”

")

")

- Most companies are protecting their margins raising prices. Higher productivity not specifically mentioned yet.

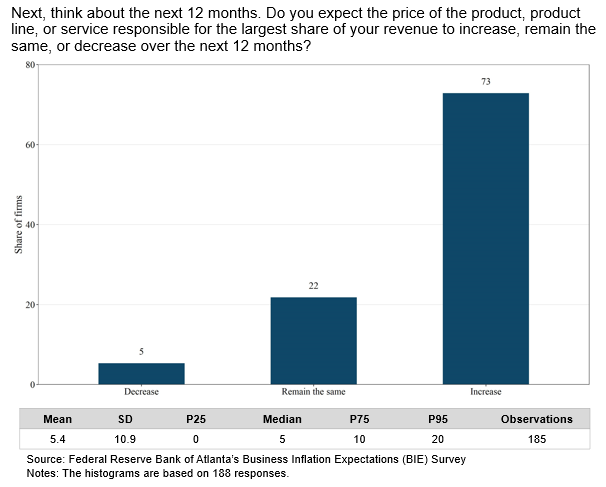

- Companies anticipate being able to keep raising prices in 2022:

According to the Bureau of Labor Statistics, private industry wages and salaries increased 6.5% annualized in Q3. That’s the fastest increase recorded in this wage series in nearly 30 years. The surge in labor costs should not be a surprise.

Big and small companies have been talking publicly for many months about labor shortages and the need to raise wages to keep staff and attract new workers. The pressure on labor costs is widespread but is most severe in services, the segment of the private sector workforce that accounts for 84% of all jobs. (…)

Even after boosting wages by the most significant amount in three decades, firms are telegraphing the need to do more to maintain and recruit staff. In other words, the labor shortage is not going away anytime soon. (…)

Powell is using the pre-pandemic jobless rate and employment levels as gauges to its full employment mandate. Yet, history shows that no two labor markets are alike. And, the precise moment when the sweet spot for the demand for labor and the supply of workers is met is not based on any arbitrary metric, but when a broad range of companies start increasing wages and offering even more to new workers in order to compete. At that point, it’s the view of companies, not policymakers or economists, that the labor markets have passed the point of balance.

Companies have declared that the country is at full employment. The Fed should declare victory and start to normalize official rates at the same time as it plans to scale back its asset purchase program. However, the Fed is not listening, and the continuation of the easy money will only add to labor market pressures and more inflation.

John Authers: It’s Official. The Inflation Numbers Are a Hot Sticky Mess The debate over whether this is transitory is over, and the question now is what to do.

(…) The current “patient” approach is beginning to look totally inappropriate. My colleague Cameron Crise offered this dramatic chart, which calculated a “real” fed funds rate by subtracting the headline increase in CPI. On this basis, we have the lowest real fed funds rate in history, at a time when inflation is its highest in 30 years.

Whoever is running the Fed next year will be aware of the hapless chairmen of the 1970s who presided over the last episode of steeply negative real rates. This is as true for possible Chairwoman Lael Brainard as it is for incumbent Jerome Powell. Tuesday saw long bond yields tumble after news that Brainard had been interviewed, on the assumption that she would be significantly more dovish. That led to an epic switchback after the inflation numbers. Apparently Mr. Market has worked out that no Fed chairman can lie back and do nothing about inflation like this.

Meanwhile, the exceptional turbulence in fixed-income markets, a fact of life for a month now, continued in full force. (…)

In a nutshell, the market has swung strongly against the notion that the Fed can stay patient, and is betting that it has already left it too late. (…)

- Inflation Is Now Global, But the Traps Are Local Why it’s tough to take the inflation fight to where it truly matters: The big powers like the U.S., China and Europe are hemmed in by domestic policies they can’t exit. Expect prices to keep rising.

(…) Most central banks know how to deal with this, right? They simply raise interest rates. Even critics of prolonged easy money say that when it comes down to it, officials have a tried and true formula. Central banks dare not chance truly runaway levels of inflation and risk a return to the bad old days of the 1970s, at least in the U.S. and Europe. Or, in China’s case, squander a big part of the prosperity and economic stability engineered by Deng Xiaoping’s opening of the economy. For all the talk about cold war between Washington and Beijing, China’s inflation experience has largely tracked the West’s, according to a Reserve Bank of Australia paper published on the eve of the pandemic.

The current hand-wringing isn’t happening in a vacuum, however. China is worried about growth, which is already slacker than the fourth quarter of 2019, before Covid-19 crashed over the world. (…)

For its part, the Federal Reserve will find it tough to accelerate tightening. Chair Jerome Powell has emphasized that quantitative easing should be finished before considering hikes in the benchmark rate. The tapering of QE has only just been announced and is scheduled to wrap up mid-2022. That makes a meaningful withdrawal of stimulus, as opposed to slowing the pace of easing, unlikely before the third quarter. Sure, the Fed can always hasten the taper, but the institution has bent over backwards to avoid a tantrum like the market gyrations of 2013. (…)

ECB President Christine Lagarde is unlikely to find Germany’s broadside helpful. Since the euro’s inception, ECB bosses have grown used to German officials warning about the sins of loose money. (…)

The market for monetary nostalgia is on a bull run. Inflation is globalized, but don’t look for a Plaza Accord-type global response echoing the 1985 pact inked in a swank New York hotel that re-aligned the trajectories of major currencies. Domestic conditions aren’t sufficiently sympathetic.

Within less than 24 hours, the world’s three largest economies — the U.S., China and Japan — each released inflation data that shattered consensus forecasts and showed prices rising at the fastest pace since at least the early 1990s. Actually the highest print in more than 40 years in Japan.

The fourth-largest economy, Germany, also confirmed inflation at the fastest pace since the early ‘90s, but that release didn’t surprise economists as it was the final print and the beat had come with the preliminary estimate. Germany isn’t letting the side down though — it recently confirmed the highest producer price inflation on records that go back to 1977. This from the country where policy makers famously fear inflation more than most. (…)

What’s bizarre is that we listen to economists on this issue. Today marked the 11th month in a row of Japan PPI beating consensus forecasts! It was the ninth in a row for China PPI. They’ve underestimated seven of the last eight U.S. CPI prints, although NONE of the 70 economists surveyed by Bloomberg anticipated the 0.9% m/m increase in CPI Wednesday — the highest prediction was 0.7%. And yet their “expertise” is still guiding too many people in markets. You almost couldn’t make it up. It’s like the frogs trusting the chef who put them in the pot on whether they will be OK. (…)

Bonds will suffer, but we’ll swing from bouts of curve flattening to steepening. The risk-reward ratio of overpriced momentum stocks now has negative appeal, but some other equity sectors can still perform. Currency markets will see some extraordinary dislocations as FX will be a key outlet for economic imbalances. (…)

The inflation genie is out of the bottle. The immediate path for markets is difficult because the shifting reaction function of big central banks is still in play. It’s not suddenly going to get easier: the year ahead will see immense asset-price dislocations.

(…) The 6.2% increase in the consumer price index in October “would have been enough in any market since 1925 — and for all I know long before that — it would have been enough to have crashed the market,” said the value-investing giant and co-founder of Boston-based asset manager GMO. “But this time the faith in the Fed is so complete that when they say it is temporary we believe it.” (…)

Grantham, 83, said the U.S. central bank has overstimulated the economy repeatedly, inflating the tech bubble in 2000, the housing bubble before the 2008 financial crisis and creating “craziness” in today’s stock market with wild moves in meme stocks.

“Have they learned? Absolutely not,” said Grantham. “The Fed in my opinion, hasn’t done a thing right since Paul Volcker.”

In order to explain today’s “market you have to assume 100% ignoring of rising inflation, which is quite remarkable.” (…)

Manhattan Rents Jump by Most on Record as Tenants Seek Upgrades The median rent rose 18% in October from a year earlier to $3,382, appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate said in a report Thursday. It was the biggest annual increase in data going back a decade.

Jobless Claims Closing in on Pre-Pandemic Lows

With the Veteran’s Day holiday tomorrow, the weekly release of jobless claims was pushed up to today. Initial claims missed expectations falling to only 267K rather than the anticipated drop to 260K. Last week’s number was also revised higher by 2K to 271K. The decline this week marked the sixth week in a row of declines as claims are once again at the lowest levels since March 2020. In fact, this week’s level is only 11K above the March 14, 2020, pre-COVID surge level. (…)

Delayed an extra week, the inclusion of all other programs showed yet another drop in continuing claims on an unadjusted basis. Total claims across all programs fell to 2.57 million, down roughly 100K from the previous week. Essentially that entire decline was on account of regular state claims with the moves in PUA and PEUC claims basically netting out. There continue to be some residual claims from pandemic era programs, but they now account for a significantly smaller share of claims than was the case only a few months ago, and generally, those claim counts have declined. (…)