A Higher Peak for Shelter Inflation (Goldman Sachs)

(…) Our best guess is that our tracker will peak around 6% year-over-year in Q1, which suggests that the already strong sequential increases in the official measure will likely increase further over the next few months. But fortunately, the preliminary data we have for Q4 show that asking rent growth has slowed on a sequential basis, albeit remaining at high levels. For example, Apartment List’s rent index has slowed from a month-over-month peak of +2.6% (sa by GS) to +0.8% in November.

We now expect PCE shelter inflation to peak next year around 5½% year-over-year (vs. 5% previously), which raises our end-2022 core PCE forecast by 0.1pp to 2.4% year-over-year. Thereafter, we expect the massive gap that has grown between asking rents and effective rents to continue to put upward pressure on shelter prices even if asking rent growth slows.

When combined with a strong outlook for the fundamental drivers of our shelter inflation model—a strong labor market, a low vacancy rate, and spillovers from home price gains—we estimate shelter inflation of 4½% year-over-year for end-2023 and 4¼% for end-2024, both above the last cycle’s high, which raises our end-2023 core PCE forecast by 0.1pp to 2.2% and our end-2024 forecast by 0.05pp to 2.25%.

China Property Plunge Worsens as Shimao Deal Raises ‘Red Flag’

Shares of Shimao Group and its property-services unit both tumbled by the most ever on Tuesday, while a Bloomberg index of property stocks dropped 4.3% to the lowest level since February 2017. A connected-party acquisition announced by the developer late Monday “not only implies tight liquidity conditions for Shimao, but is also a corporate governance red flag,” JPMorgan Chase & Co. analysts wrote as they downgraded both stocks. (…)

Record losses in Shimao Group’s shares and bonds have been particularly unnerving, given that the company was until recently considered among the sector’s strongest players — able to withstand the financing curbs that led to defaults by China Evergrande Group and Kaisa Group Holdings Ltd. (…)

Ranked 13th among Chinese developers by contracted sales, Shimao Group poses a much smaller systemic risk to Asia’s largest economy than does Evergrande. But the former company’s woes have undermined hopes that higher-rated developers would be able to weather the Chinese government’s crackdown on the real estate industry.

Shimao Group had passed all of the so-called three red lines — metrics introduced to curb borrowing among developers — according to Bloomberg-compiled data including first-half results. That would typically suggest a more robust financial position and easier access to debt markets. (…)

The developer and its subsidiaries need to refinance or repay $2.5 billion in bond maturities through 2022. That includes the 30 million yuan repayment on a 4.5% local bond due Dec. 17 and a 2 billion yuan note due January, according to data compiled by Bloomberg. Shimao Group has about $10.1 billion in outstanding local and offshore bonds.

Cash Glut in Eurozone Drives Dollar Demand Cash-rich eurozone banks are rushing to change their euros into dollars by the end of the year, driving a key measure of demand for the greenback.

The interest rates on three-month euro cross-currency basis swaps, in which one party borrows a currency and lends their own in return, have turned more negative in recent weeks. That means traders in Europe are paying a premium to exchange excess euros for dollars.

The steeper cost in part reflects a wave of programs initiated by the European Central Bank, analysts and investors say. Intended to boost lending to households and businesses during the economic recovery from Covid-19, the programs have saddled eurozone banks with more cash than they want, prompting them to seek ways to get rid of it. (…)

Nearly $1.6 trillion flowed into the Fed’s reverse repo facility on Monday—near the record. Money into the facility has hit repeated highs this year after the Fed boosted the return to 0.05% from 0%.

The facility has been made even more attractive when compared with short-dated European government debt, which often comes with negative yields, meaning banks would lose money on holding them to maturity. The yield on the benchmark two-year German government bond stood at minus 0.692% on Monday. (…)

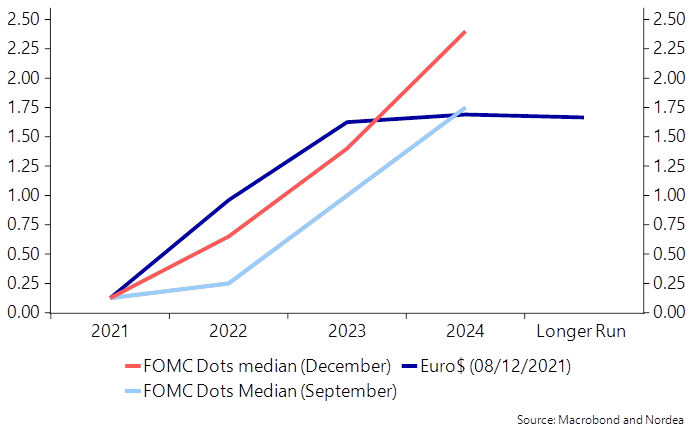

Nordea:

We expect the dots to support the dollar and push US STIRs even further. Pricings are, however, from a rates perspective, already pretty aggressive in the white and red strips (the 1 and 2 years sectors of the Eurodollar bundles). Three hikes will slowly but surely be baked into 2022, but market pricing on terminal rates remain low and could be a driver for a lower EURUSD going into H1 2022.

Dots to show a dramatic change

A hasty policy shift by central banks anxious to tame surging inflation is the biggest downside risk for global stocks next year, according to an informal Bloomberg News survey of fund managers.

And with the post-pandemic rebound now past its peak, this month’s poll of 106 investors also shows that more market participants expect value stocks to outperform equities that soared this year on future growth expectations. While risks lurk, more than 40% of respondents singled out a more robust economic expansion as the main upside catalyst for 2022. (…)

The findings are in line with the latest Bank of America Corp. survey of global fund managers, which showed that hawkish central banks are seen as the biggest tail risk for the first time since May 2018, followed by inflation and Covid-19’s resurgence. Investors are bracing for major policy meetings of the Federal Reserve, the European Central Bank and the Bank of England this week, which might provide clarity on the pace of monetary tightening and the wind down of stimulus measures. (…)

BTW: A group of 37 retail trading favorites continued its decline after shedding almost a quarter of its value over the past three weeks. Still, AMC’s up almost 1,000% this year and GameStop has rallied 627%. (Bloomberg)

China reports first Omicron case as fears mount for factory supply chains

Omicron Will Slow Oil Demand Recovery but Not Destroy It, IEA Says The new variant’s emergence will allow the supply of oil to overtake the rate at which the world is consuming it, easing the supply tightness of recent months, the International Energy Agency said Tuesday.

The IEA trimmed its 2022 supply forecast from non-OPEC producers by 100,000 barrels a day and cut its demand forecast by the same amount, saying it expects the surge in coronavirus cases to stymie the recovery in global demand.

Air travel and, in particular, the consumption of jet fuel, will be most affected by the Omicron variant, the IEA said in its monthly market report. But overall, the variant’s emergence will “temporarily slow, but not upend, the recovery in oil demand,” the Paris-based energy watchdog said. (…)

The IEA said that Saudi Arabia and Russia—the two leaders of OPEC+—could also set production records, if the alliance continues its policy of unwinding production cuts implemented last year when the pandemic’s global economic impact at its worst.

That steadily rising output may combine with slightly lower demand than previously expected to create a 1.7 million barrel a day surplus in the first quarter of 2022. (…)

Toyota, in Reversal, Says It Will Shift More Rapidly to EVs Toyota stepped up its commitment to battery electric vehicles, saying it would have 30 EV models available by 2030 and aimed to sell 3.5 million battery EVs globally by 2030.

-

Lithium Prices Charged by EV Demand, Scant Supply The lithium price surge is setting off a scramble for supply and fueling fears about long-term battery metals shortages

An index of lithium prices from research firm and price provider Benchmark Mineral Intelligence doubled between May and November and is up some 240% for the year. The index is at its highest level in data going back five years. (…)

While there is plenty of lithium in the world, converting it into battery-grade chemicals is a long, expensive ordeal. With traders and corporate buyers riding momentum, prices are prone to big moves in both directions. (…)

Even though commodities are a tiny part of total vehicle cost, they could contribute to rising average prices for lithium-ion battery packs, according to research firm BloombergNEF. That would be the first such increase in at least a decade. Years of tumbling battery costs have made electric vehicles more competitive with gasoline powered cars. (…)

“There’s enough lithium out there. The issue is the investment required to get there,” said Eric Norris, president of Albemarle’s lithium unit, on the company’s earnings call last month. (…)