This a.m.: ADVANCE MONTHLY SALES FOR RETAIL AND FOOD SERVICES, SEPTEMBER 2021

Advance estimates of U.S. retail and food services sales for September 2021, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $625.4 billion, an increase of 0.7 percent (±0.5 percent) from the previous month, and 13.9 percent (±0.7 percent) above September 2020. Total sales for the July 2021 through September 2021 period were up 14.9 percent (±0.7 percent) from the same period a year ago. The July 2021 to August 2021 percent change was revised from up 0.7 percent (±0.5 percent) to up 0.9 percent (±0.2 percent).

Retail trade sales were up 0.8 percent (±0.4 percent) from August 2021, and up 12.2 percent (±0.7 percent) above last year. Gasoline stations were up 38.2 percent (±1.6 percent) from September 2020, while food services and drinking places were up 29.5 percent (±3.7 percent) from last year.

U.S. Producer Prices Moderate Slightly in September

The Producer Price Index for Final Demand rose 0.5% m/m (8.6% y/y) in September following a 0.7% m/m (8.3% y/y) gain in August. The year-to-year increase is the largest in the series history, dating back to 2009. A 0.6% rise for last month had been expected by the Action Economics Forecast Survey. The PPI excluding food and energy prices rose 0.2% m/m (6.8% y/y), down from a 0.6% m/m (6.7% y/y) gain in August. A 0.5% increase had been expected. The PPI less prices of food, energy and trade services edged up 0.1% m/m (5.9% y/y) versus 0.3% (6.3% y/y) in August. This was the smallest monthly increase in this new “core” measure since May 2020.

The rise in prices for final demand goods accelerated to 1.3% m/m (13.3% y/y) in September versus a 1.0% m/m (12.6% y/y) increase in August. This was the largest y/y rise in the series history. Final demand goods prices less prices of foods and energy rose 0.6% (8.3% y/y) in September, the same monthly gain as in August. The Bureau of Labor Statistics estimated that nearly 80% of the September increase in the headline index can be attributed to the increase in goods prices. Prices of both energy and food soared in September—food up 2.0% m/m (12.9% y/y) and energy up 2.8% m/m (36.3% y/y) with meaningful monthly increases in all energy components (led by a 3.9% m/m rise in gasoline prices).

By contrast, final demand services prices rose a more moderate 0.2% m/m (6.4% y/y) in September following a 0.7% m/m increase in August. This was the smallest monthly rise since December 2020. The moderation was led by a record 16.7% m/m drop in airfares. Offsetting this were meaningful monthly gains in both retail and wholesale trade services margins. Retail margins increased 0.5% m/m (10.9% y/y) and wholesale margins rose 1.5% m/m (11.7% y/y), by far a record increase. To be sure, the margins data in this report are often difficult to interpret. Still, in a rising input cost world, that firms at both the retail and wholesale level were able to expand their margins meaningfully could indicate that firms have more pricing power than previously thought and furthermore that inflation pressures may be broadening.

The monthly rise in construction costs slowed to 0.1% m/m (5.2% y/y) in September from a 0.2% m/m (5.0% y/y) gain in August.

Pick the line that fits your narrative…

I pick Goods, still exploding across the board, and even more upstream Intermediate Demand-Processed Goods.

U.S Initial Unemployment Insurance Claims Continue to Fall

Initial claims for unemployment insurance fell to 293,000 (-64.8% y/y) in the week ending October 9, from 329,000 the previous week, which was revised from 326,000. The Action Economics Forecast Survey had expected 329,000 initial claims for the latest week. The 4-week moving average was 334,250, a decrease of 10,500 from the previous unrevised week and the lowest since March 14, 2020, when it was 225,000.

Initial claims for the federal Pandemic Unemployment Assistance (PUA) program in the week ended October 9 were 21,624 (-93.6% y/y) versus 23,506 in the previous week. The latest number was near the lowest level since the program began on April 4, 2020, at the start of the pandemic.

By comparison, these claims averaged 107,756 per week during August. The PUA program provided benefits to individuals who are not eligible for regular state unemployment insurance benefits, such as the self-employed. This program expired on September 6, explaining the smaller number of new claims during the latest several of weeks. Given the brief history of this program, these and other COVID-related series are not seasonally adjusted.

Continued weekly claims for regular state unemployment insurance fell during the week of October 2 to 2.593 million (-72.0% y/y) from 2.727 million in the prior week, revised from 2.714 million. The insured rate of unemployment slipped to 1.9% from 2.0%.

Continued weekly claims in the Pandemic Assistance Program (PUA) program dropped to 549,103 in the September 25 week (-95.0% y/y) from 647,690 the prior week, as the program wound down. Continued weekly claims for Pandemic Emergency Unemployment Compensation (PEUC) fell sharply to 440,435 in the week of September 25, from 630,814 in the prior week and from 3.645 million in the week ended September 4. This program covered people who had exhausted their state unemployment insurance benefits.

In the week ended September 25, the total number of all state, federal, PUA and PEUC continued claims fell sharply w/w to 3.649 million from 4.172 million the week prior and from 11.250 million in the week ending September 4. These total claims averaged 6.025 million over the four weeks ended September 25. These figures are not seasonally adjusted.

Bespoke’s chart:

(Bespoke)

Toyota Cuts November Outlook by 15% on Parts Shortage, Covid

Toyota Motor Corp. cut its global car production target for November by around 15% from an earlier plan as a shortage of parts continues to weigh on the world’s No. 1 automaker.

The Japanese company had initially planned to make 1 million cars next month but now expects to do only around 850,000 to 900,000 units, it said in a statement Friday. (…)

“This adjustment will affect approximately 50,000 units in Japan, and between 50,000 units and 100,000 units overseas.”

Toyota’s full-year production target of 9 million vehicles for the 12 months ending March 31, 2022 will be maintained however “due to the easing of restrictions on Covid-19 in Southeast Asia.” Smaller-than-expected production cuts in September and October also helped, it said.

“The worst period is over,” Kazunari Kumakura, the chief officer at Toyota’s purchasing group, said at a media briefing. “We’re seeing lower risks,” he said, although added as chip supply normalizes, supply and demand will remain tight.

(…) since we expect the shortage of semiconductors to continue in the long term, we will consider the use of substitutes where possible.” (…)

(…) New-car registrations plummeted 25% [in September] to 972,723, the lowest for the month since 1995, the European Automobile Manufacturers’ Association said Friday. The lobby group largely attributes the drop to the semiconductor shortage, which worsened when Covid-19 outbreaks idled chip packaging and testing facilities in Southeast Asia.

After three consecutive declines, sales in Europe have fallen in more months than they’ve risen this year. While contraction was unthinkable in early 2021 — the ACEA predicted roughly 10% growth for the year — some market researchers are now expecting it. (…)

Companies that have cut their earnings guidance in recent weeks include France’s Faurecia SA, Germany’s Hella GmbH & Co. and U.S.-listed Aptiv Plc. After months of battling component shortages alongside high commodity prices and shipping constraints, manufacturers face more disruptions, according to Fitch Ratings.

“We only expect semiconductor supplies to start showing signs of improvement from” the second half of next year onwards, the credit rater said in a report. “However, there will still be a shortage to some extent until mid-2023.

Europe’s largest economies are also suffering. Germany’s leading research institutes lowered their joint forecast for growth this year to just 2.4%, from 3.7%, citing supply logjams that will hinder the nation’s recovery into next year. The U.K. expanded slower than expected in August after a surprise contraction in July. (…)

WORKERS STRIKE BACK

Deere Workers Go on Strike for First Time in 35 Years More than 10,000 workers walked off the job at the farm- and construction-equipment maker after earlier rejecting a deal with pay raises and bonuses over six years.

(…) The Moline, Ill.-based manufacturer, known for its green and yellow tractors, faces worker demands for higher wages and broadened benefits as labor unions push similar measures at major U.S. food producers, restaurant chains and vehicle makers, in some cases launching strikes. (…)

Fourteen hundred employees at cereal maker Kellogg Co. have been on strike against the food company amid negotiations over a labor contract with the Bakery, Confectionery, Tobacco Workers and Grain Millers International Union. Workers represented by the UAW at commercial truck maker Volvo went on strike off and on during the spring and summer as members voted down three contract proposals, before agreeing to a six-year contract in July.

Bakery workers for food company Mondelez International Inc. last month ended a weekslong strike after agreeing to a new four-year contract that included hourly wage increases and a higher company match for 401(k) contributions. In Buffalo, N.Y., Starbucks Corp. is pushing back against a unionization drive by employees at area stores who are seeking expanded wages, training and staffing.

The International Alliance of Theatrical Stage Employees, which represents over 150,000 behind-the-scenes workers, said it would strike on Monday unless a deal for a new contract is reached with producers. (…)

Under terms of Deere’s tentative deal with the UAW, workers would have received wage raises of 5% to 6% this year, based on their job duties; 3% raises in 2023 and 2025; and lump-sum bonuses in three other years, according to a summary from the union. The deal also would have provided enhanced benefits for retirees and restored cost-of-living wage adjustments that had been part of previous Deere contracts.

Workers overwhelmingly voted down the contract Sunday, with some saying that the deal didn’t do enough to erase two decades’ worth of concessions by the union during periods when equipment markets were weak. (…)

Clearly related:

- Nearly 40% of U.S. Households Face Financial Difficulties Amid Pandemic People cited problems such as paying utility bills or credit-card debt, according to a recent poll. About one-fifth have depleted all of their savings.

U.S. households are struggling in many ways over a year into the coronavirus pandemic, according to the poll conducted by the Harvard T.H. Chan School of Public Health, the Robert Wood Johnson Foundation and National Public Radio.

Nearly 60% of households earning less than $50,000 a year reported facing serious financial challenges in recent months. Of those, 30% lost all of their savings, according to the poll.

The survey questioned about 3,600 adults in August and early September about a variety of potential problems during the pandemic and how the effects have continued in more recent months. In addition to financial concerns, respondents were asked about healthcare, education, child care and personal safety. (…)

Close to 20% of those polled said their financial situation is better now than before the Covid-19 outbreak, compared with 32% who said their situation is worse. About half, 49%, said it stayed the same. (…)

About 67% of those surveyed said they received financial assistance from federal and state governments through unemployment benefits, loans and stimulus payments. Of those who received assistance, 23% said it “helped a lot,” while 44% said it “helped a little,” according to the poll. (…)

- Unacceptable, unsustainable:

Hence:

- September’s Atlanta Fed’s Wage Growth Tracker underlines that power is shifting. Job switchers are getting biggest wage rises in almost 20 years. The overall level of wages rose by the most since the eve of the financial crisis:

![]()

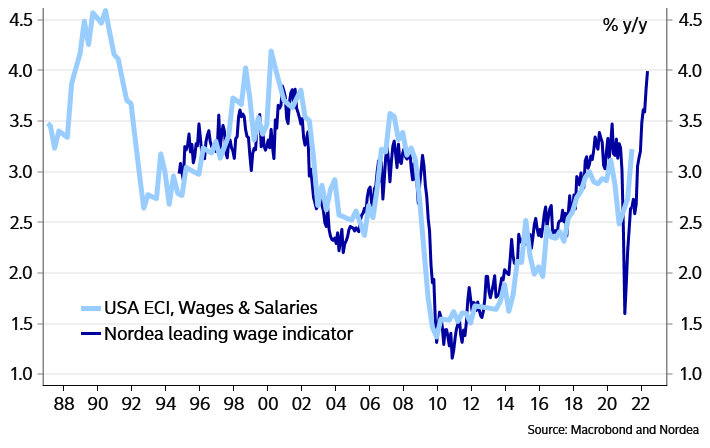

- Nordea’s wage models “strongly indicate that wage growth in 2022 will be extremely high, most likely at a time when an economic growth slowdown spells much weaker productivity growth than currently. That should make a transitory inflation argumentation quite hollow.”

US wage growth should be very high in 2022

- London Taxi Firm Offers £5,000 Welcome Salary to Lure Drivers Addison Lee Ltd., London’s largest taxi firm, is offering 5,000 pounds ($6,861) for four weeks of work to recruit drivers amid a nationwide shortage of staff. Addison Lee is trying to hire 1,000 drivers after business passenger-car trips jumped more than 40% between August and September.

HIGHER FOR LONGER

- Metals Prices Surge After Gas Crunch Crimps Output Higher energy bills prompt smelters to cut back on zinc and aluminum production

(…) Belgium-based Nyrstar said Wednesday that rising energy bills and the added cost of the European Union’s taxes on carbon emissions meant it was “no longer economically feasible” to operate the three plants in the Netherlands, Belgium and France at full capacity. (…)

Earlier this week, before Nyrstar’s cutbacks were announced, the International Lead and Zinc Study Group cut its forecasts for a zinc surplus this year by 136,000 tons, to 217,000 tons, to reflect stronger-than-expected demand. Next year, the group forecasts a smaller surplus of 44,000 tons.

Nyrstar’s curtailments could mean between 40,000 and 50,000 tons of lost zinc production a month, according to estimates from ING. Energy-related production slowdowns in China meant zinc output there was also likely to fall short of expectations, the bank said. (…)

Meanwhile, China’s aluminum production has been cut by 10% this year, or roughly three million tons, estimates Robin Bhar, an independent metals consultant.

“We are seeing extraordinarily strong demand at a time when you’re crimping supply for aluminum and other metals…There is a big dislocation between supply and demand,” he said.

A weaker dollar has also supported metals denominated in dollars this week by making them cheaper for overseas buyers.

- Ikea Expects Shortages Due to Supply-Chain Crisis Until Mid-2022 “The biggest challenge has been getting products out of China, where there has been a very limited capacity,” Chief Executive Officer Jon Abrahamsson Ring of Inter Ikea, the worldwide franchiser for the brand, said in an interview.

- Canadian Tools Maker Lee Valley Warns of Yearlong Supply Delays

(…) “To bring in a container from Asia that used to cost C$7,000 now costs C$34,000 unless you’re Home Depot and can afford to charter a ship,” Chief Executive Robin Lee said in an interview. “I don’t think the public understands how much of what they buy is comprised of freight.”

Meanwhile, shortages for raw materials, such as magnesium, are slowing production of finished goods, causing further delays and price increases. High-grade Baltic birch plywood used in some Lee Valley products now costs twice what it did a year ago, Lee said. (…)

“We are now seeing lead times for some products that exceed one year, if our order even gets accepted – and not all do,” Lee wrote in an email to customers. The retailer is releasing its Christmas catalog “uncomfortably early” and customers “can count on many prices increasing,” he wrote. Right now, he expects those increases to be between 5% and 9%. (…)

“I don’t think we will be out of the woods” during the current fiscal year, the CEO said. That period runs through next August. “This is a very big challenge for the whole supply infrastructure.” (…)

The price spike for transports and raw materials seen in the last six months has meant increased costs, which the company plans to absorb rather than passing over to Ikea customers. (…)

NO WORRIES!

- Canadians can be confident Bank of Canada will keep inflation under control, governor says

- China’s Central Bank Says Inflation Risks Are Controllable

Sun Guofeng, head of the monetary policy department, said at the briefing in Beijing on Friday that producer price inflation will remain elevated in the short term before falling toward the end of the year, though imported inflation and the impact of the global commodity boom is controllable. (…)

While consumer inflation is expected to pick up, it will remain within reasonable range, Sun said. Small businesses in downstream industries may be affected by the increase in costs, and the PBOC has increased support to those firms, he said. (…)

The PBOC officials said authorities have asked banks to keep loans to the real estate industry stable and orderly to limit contagion from the debt crisis of developer China Evergrande Group. Evergrande’s risks are controllable and unlikely to spread, they said.

However:

- RBC CEO warns ‘persistent inflation’ is building, disputes central bank forecast

- MOYNIHAN SAYS INFLATION ISN’T TEMPORARY, ‘IT’S PERMANENT’

MORGAN STANLEY CEO GORMAN SAYS INFLATION IS ‘NOT TRANSITORY’

DIMON: INFLATION HAS TRANSITORY AND PERMANENT COMPONENTS - Goldman Sachs Group President John Waldron also said this week that inflation is not transitory — a sentiment echoed by BlackRock Inc. CEO Larry Fink, who added it’s “definitely not transitory.”

- “To us, a nowadays admittedly backward-looking central bank as the Fed should have no alternative than to admit that the transitory thesis was wrong and move closer to a first rate hike. Sadly, we don’t think they will do that at this stage. The Fed has basically promised that a tapering decision is an independent decision and should not be taken as a first step to a rate hike”. (Nordea)

- “On the face of it, lower real yields imply the fear that a policy mistake lies ahead. The Fed needs to help the labor market revive, and it is keen to taper off its QE asset purchases before it can start to raise interest rates. That leads to the risk that it waits too long to raise rates, allows inflation to take hold, and has to raise rates more in consequence. That is the kind of miserable prospect that might make it sensible to accept a negative real yield. The decline in Biden’s political fortunes might have a lot to do with this.” (John Authers)

CHINESE COCKROACHES

From Almost Daily Grant’s:

Contagion is afoot in China’s lynchpin property sector. In the wake of China Evergrande’s implosion under the weight of $300 billion in liabilities, peers try, with varying degrees of success, to keep their own heads above water. Modern Land (China) Co. requested a three-month extension on a dollar bond due Oct. 25 earlier this week, noting that it hopes to avert “any potential payment default.” U.S.-listed peer Xinyuan Real Estate Co. today completed an exchange offer, swapping $200 million worth of senior debt maturing tomorrow for new senior notes due in 2023, in the process earning a downgrade to single-C from Fitch Ratings and the resignation of accountant Ernst & Young Hua Ming LLP. That comes on the heels of last week’s default on a $206 million bond by Fantasia Holdings Group Co.

Beijing, which arguably helped usher in the current tumult by rolling out the so-called three red lines policies limiting balance sheet growth, appears content to let the situation play out rather than ride to the rescue. “The industry is in a period of survival of the fittest and does not require excessive administrative intervention,” Kuang Weida, director of the Center for Urban and Real Estate Research at Renmin University of China, tells Yicai Global. An unnamed senior official concurs with that assessment, telling Reuters that “property curbs will be painful, but this is the price that must be paid. In the past, we always loosened controls due to economic downturns, but this time round the leadership’s determination looks very firm.”

Time will tell how durable that determination is: Some $64 billion worth of Chinese property developer dollar-denominated debt currently trades at distressed levels according to data from Bloomberg, equivalent to a hefty 46% share of such global bonds fetching option-adjusted spreads north of 1,000 basis points relative to Treasurys. The real estate industry’s cross-border bond issuance stood at $232 billion at the end of September according to Fitch, with nearly one-third of that sum set to mature by the end of 2022.

That may prove problematic, as up to one-third of the 60 real estate firms that have issued dollar-pay debt are currently frozen out of the capital markets, a European bank higher-up estimates to the Financial Times. “International investors are probably used to more aggressive, intervention-style policy,” the publicity-shy banker observed. “They are looking for kung fu but they’re getting tai chi.”

More broadly, the starring role of real estate in China’s economic miracle (pegged at between 23% and 30% of GDP by various observers) begs the question of what consequences may follow an early autumn freeze. Contracted sales among China’s 100 largest developers plunged by 36% year-over-year in September, one of the most important selling months of the year, according to data provider CRIC. With activity on the fritz, highly leveraged industry players are obliged cut prices to generate the necessary revenues to service their debts. “Virtually all developers have offered discounts over the past two months,” property agent Huang Jun relays to The Wall Street Journal. “Just like Evergrande, they may be under pressure to sell more flats,” irrespective of price. Indeed, the 21 large developers listed on the Hong Kong stock exchange saw their average interest coverage ratio slip below 1 to 1 as of June 30 according to Refinitiv, compared to nearly 1.5 to 1 at the end of 2020.

“Fire sales of Evergrande’s land reserves could drive down land prices in many areas of the country, which would be quite frightening,” an anonymous government source tells the FT. “The only viable solution might be to gradually nationalize the whole real estate sector.”

In other words, laissez-faire with Chinese characteristics.

But not total laissez-faire:

China Eases Mortgages for Rest of Year on Evergrande Contagion Worries

China is loosening restrictions on home loans at some of its largest banks, according to people familiar with the matter, adding to signs of growing concern by authorities about contagion from the debt crisis at China Evergrande Group.

Financial regulators told some major banks late last month to accelerate approval of mortgages in the last quarter, said the people, asking not to be identified discussing a private matter. Lenders were also permitted to apply to sell securities backed by residential mortgages to free up loan quotas, easing a ban imposed early this year, the people said. (…)

By issuing residential mortgage-backed securities, banks can move loans off their balance sheet and raise capital to dole out more. The issuance of RMBS in September hit the highest level this year, according to Bloomberg calculations based on data from the China Securitization Analytics website.

(…) Analysts have lowered their consensus 12-month earnings projection by nearly 5% over the past three weeks to the lowest since July 2020, Bloomberg-compiled data show, amid weak momentum in domestic consumer spending.

What Bank Earnings From JPMorgan, Bank of America Tell Us About the U.S. Economy On Wall Street, M&A is on fire, but on Main Street, loan growth is muted. Here’s what bank earnings reveal about the bigger picture.

Customer spending has eclipsed pre-pandemic levels, bank executives said, a trend they see continuing into the holidays. Spending on Citigroup C 0.77% credit cards jumped 20% from a year ago to a record. Late fees are up and more people are starting to carry balances. Executives said they were back to fighting for card customers.

“That is a tremendous amount of spending that’s going on,” said Bank of America BAC 4.47% Chief Executive Brian Moynihan, “and it’s accelerating.” (…)

At Wells Fargo WFC -1.61% and Bank of America, total outstanding loans were down from a year ago but up from the second quarter. (…)

Morgan Stanley and Bank of America both notched gains in overall trading revenue. JPMorgan JPM 1.53% Chase & Co., Citigroup and Wells Fargo reported lower trading revenue. (…)

JPMorgan, Morgan Stanley, Bank of America and Citigroup all reported record quarters for mergers-and-acquisitions fees. Goldman Sachs’s GS 1.27% league-leading team is due to report Friday. Executives said pipelines for potential future deals remain full. That is a sign company executives are confident enough in the economy to attempt transformative deals.

- Wall Street Bosses See Windfall Lasting, Fueling Pay and Hiring The surge in dealmaking and other revenue gains will probably translate into higher compensation costs at JPMorgan in the coming year, as the firm rewards employees’ performance, the bank told analysts on Wednesday. Rivals including Citigroup mentioned efforts to beef up their desks with hiring. Bank of America said the fight for talent will add to its compensation costs, too.

Almost Daily Grant’s offered this yesterday:

Behold the below pair of headlines from Bloomberg yesterday:

- Almost 20% of U.S. Households Lost Entire Savings During Covid

- Coach K’s Final Game at Duke Sends Tickets Surging Past $50,000

Here’s my own contribution: