Economists Lift US Growth Forecasts, See Fed Higher for Longer This supports expectations that the Federal Reserve will keep interest rates higher for longer.

Gross domestic product is expected to advance an annualized 1.8% in the third quarter, nearly quadruple the 0.5% pace projected in July, according to the latest Bloomberg monthly survey of economists. They also see the economy expanding somewhat in the last three months of the year, rather than contracting. (…)

Economists in the survey now see the Fed holding interest rates higher for longer amid risks that a stronger economy will keep inflation above their goal. While economists don’t see further hikes on the horizon, they also don’t expect the central bank to cut rates until the second quarter of next year — which is three months later than July’s estimate.

However, economists did revise up their expectations for bond yields through the end of 2025. The two-year Treasury yield is now seen ending the current quarter at 4.82% compared to last month’s projection of 4.65%. (…)

Excluding food and energy, forecasters now see the personal consumption expenditures price index cooling more quickly through the end of this year compared to their July projections. Their estimates for the overall PCE measure — which is the Fed’s preferred inflation target — were little changed. (…)

At the same time, unemployment estimates were marked lower through the end of next year and hiring was seen higher, also supportive of a soft landing.

![]() Be warned that Blomberg’s “Aug. 11-16 survey of economists included 68 responses, and many were submitted before a government report showed retail sales beat estimates in July after upward revisions to the prior two months.” (…)

Be warned that Blomberg’s “Aug. 11-16 survey of economists included 68 responses, and many were submitted before a government report showed retail sales beat estimates in July after upward revisions to the prior two months.” (…)

The Atlanta Fed’s GDPNow for Q3 jumped from +4.1% to 5.0% after the retail sales report and to 5.8% Wednesday after new data on housing and industrial production.

Some economists have argued that “weird” seasonal adjustments boosted the retail stats in July. But unadjusted data show total sales growth accelerating from +1.8% YoY in June to +2.5% in July. More significantly, excluding gasoline stations where sales fluctuate with gas prices, growth went from +4.8% in June to +5.3% in July.

My calculation of retail inflation (0.35 x CPI-Durables + 0.65 x CPI-Nondurables) gives “CPI-Retail” down 1.1% in June and down 0.6% in July.

Goods demand seems to be reaccelerating. If so, inventories will get normalized faster, helping manufacturing demand, particularly China’s, right on time for the holidays…Data on this Inventories to Sales Ratios chart is at the end of June.

BofA’s Warning of a ‘5% World’ Sinks in With Yields Pushing Higher

All around the world, bond traders are finally coming to the realization that the rock-bottom yields of recent history might be gone for good.

The surprisingly resilient US economy, ballooning debt and deficits, and escalating concerns that the Federal Reserve will hold interest rates high are driving yields on the longest-dated Treasuries back to the highest levels in over a decade.

That’s prompted a rethink of what “normal” in the Treasury market will look like. At Bank of America Corp., strategists are warning investors to brace for the return of the “5% world” that prevailed before the global financial crisis ushered in a long era of near-zero US rates. And BlackRock Inc. and Pacific Investment Management Co. say inflation could remain stubbornly above the Fed’s target, leaving room for long-term yields to push even higher.

“There is a remarkable repricing higher in longer-term rates,” said Jean Boivin, a former Bank of Canada official who now heads the BlackRock Investment Institute.

“The market is coming more to the view that there is going to be long-term inflation pressures despite recent progress,” he said. “Macro uncertainty is going to remain the story for the next few years, and that requires greater compensation to own long-dated bonds.” (…)

While higher rates will soften the blow by boosting bondholders’ interest payments, they also threaten to weigh on everything from consumer spending and home sales to the prices of high-flying tech stocks. What’s more, they will increase the US government’s financing costs, worsening the deficits that are already forcing it to borrow some $1 trillion this quarter to cover the gap. (…)

Broader economic shifts are also driving speculation that the low rates — and inflation — of the post-crisis period were an anomaly. Among them: demographics that may push up wages as aging workers retire; a shift away from globalization; and drives to combat global warning by shifting away from fossil fuels. (…)

“People are going to need more term premium to own long-term bonds,” she said, referring to the higher payments investors normally demand for the risk of parting with their money for longer.

Even with the recent rise in yields, though, no such premium has returned. In fact, it remains negative as long-term rates hold below short-term ones — an inversion of the yield curve that’s usually seen as a harbinger of a recession. But that gap has started to narrow, cutting a New York Fed measure of the term premium to around minus 0.56% from nearly 1% in mid-July.

That upward pressure has also been exacerbated by US federal spending, which is creating a flood of new debt sales to plug the deficit even as the economy remains at — or near — full employment. At the same time, the Bank of Japan’s decision to finally allow 10-year yields there to push higher will likely cut Japanese demand for US Treasuries.

BlackRock’s Boivin says there’s major shift underway at the world’s central banks. For years, he said, they kept interest rates well below the rate that’s considered neutral to spur their economies and ward off the risk of deflation.

“This has been flipped now,” he said. “So even if the long-term neutral rate is not changed, central banks will hold policy above that neutral rate to stave off inflationary pressure.”

KKR’s Henry McVey agrees:

While inflation has abated, we remain in a new regime characterized by above average inflation and rates, as well as slower, though positive real economic growth. Overall, we expect inflation to remain elevated, contrary to market optimism.The structural labor shortage, insufficient housing supply, ongoing geopolitical conflicts and the energy transition are drivers of elevated inflation.

(…) as we head into 2024, we remain above consensus in Europe and the US as a result of higher ‘sticky’ core inflation and in China as well because of easier year-over-year comparisons.Japan is also now transitioning from a long period of deflation to one of inflation, led by labor shortages and higher wages.

China’s State Developers Warn of Losses as Crisis Spreads

China’s state-owned property developers are warning of widespread losses, fueling concerns that the housing crisis is expanding from the private sector to companies with government backing.

Eighteen out of 38 state-owned enterprise builders listed in Hong Kong and the mainland reported preliminary losses in the six months ended June 30, up from 11 that warned of full-year losses in 2022, according to a Bloomberg tally based on corporate filings. Two years ago, only four firms with controlling or major state shareholdings posted losses.

The warnings signal state builders are no longer immune from the two-year housing slump that has weakened the economy and triggered dozens of defaults by private peers, with speculation that Country Garden Holdings Co. may be next. Authorities have in recent weeks stepped up pledges to support the property sector, though analysts are skeptical that the measures will be enough to revive the market anytime soon. (…)

Companies seeing losses include some of the biggest developers owned by the central government. Shenzhen Overseas Chinese Town Co. warned of a loss of as much as 1.7 billion yuan ($233 million), partly due to a marketing strategy to speed up home sales. That followed a loss in the second half of last year, which was its first since its 1997 listing. (…)

“SOEs could be kitchen-sinking their results for better years ahead,” Chan said. “The key is whether they can still receive liquidity support from banks. For smaller SOE developers, it will be a case-by-case situation.” (…)

But losses will reduce their scope to take on unfinished projects left by defaulted private-sector firms, further denting homebuyer sentiment. Chinese regulators see asset sales as a key step to easing the debt crisis, as President Xi Jinping’s government largely steers clear of direct bailouts.

“Sector consolidation anyhow takes time,” CreditSights’ Zeng said. (…)

- Investors Fear China’s ‘Lehman Moment Looms The troubles at a big trust company are making investors worry about financial contagion from property developers’ distress.

(…) “Zhongzhi is a black box. They don’t have periodic disclosures, it’s a private company, and some investors don’t know what kinds of assets they’re investing in,” said Xiaoxi Zhang, an analyst at Gavekal Research.

The group’s difficulties, coming on the heels of the financial distress at Chinese property giant Country Garden Holdings, have fueled worries about China’s shadow-banking system and how intertwined it is with the property sector.

“The worry is that a ‘Lehman moment’ beckons, threatening the solvency of China’s financial system,” Zhang wrote in a note earlier this week. She added that China’s “regulatory vigilance” meant that would be unlikely. (…)

China’s property downturn has already caused dozens of developers to default on their debt, and many trusts have unwound their exposure to the sector, according to a report from Nomura.

Trust funds in China still had the equivalent of about $155 billion in exposure to the property sector at the end of the first quarter, according to data from the China Trustee Association. That “is now under great threat, in our view,” Nomura said, adding that trust funds have much larger exposures to financial markets, which increases the risk of contagion. (…)

Bloomberg adds this:

Underlining Zhongzhi’s importance, regulators have formed a task force as they seek to prevent contagion. Behind the scenes the firm has hired KPMG to carry out what is likely to be a protracted restructuring process. Potential asset sales threaten to weigh on broader markets. (…

Zhongrong has 270 products totaling 39.5 billion yuan due this year, according to data provider Use Trust. (…)

It’s unclear how many products Zhongzhi has defaulted on and whether the company has sufficient assets to cover the shortfall if liquidated. (…)

About 106 trust products worth 44 billion yuan defaulted this year through July 31, according to Use Trust. Real estate investments accounted for 74% of the defaults by value. Last year also saw billions of dollars in defaults. (…)

While it’s unlikely Zhongzhi’s woes will impact the big commercial banks, it could spread to other asset managers if wealthy investors start pulling their money, said Dinny McMahon, an analyst for Trivium China and author of China’s Great Wall of Debt. (…)

- China Evergrande Seeks U.S. Court Approval for $19 Billion Debt Restructuring The company clinched a restructuring deal with a group of its foreign bondholders this spring and is seeking court approval for a global deal

(…) Court approval of the debt restructuring would make the deal legally binding in the U.S. and would close the door to any disputes against the plan that could be brought in America. Many of China Evergrande’s $19 billion in foreign bonds are governed by U.S. law. (…)

Overseas creditors eventually agreed to a consensual deal in the spring of this year. Holders of the developer’s $19 billion in foreign debt can choose to swap their holdings into new long-term debt or take some principal losses and get a mix of shorter-term bonds and equity-linked notes backed by shares of Evergrande or two of its listed subsidiaries, including China Evergrande New Energy Vehicle Group.

All of the company’s offshore creditors have until next week to vote on the plan, which requires three-quarters’ support to pass. (…)

Higher Interest Rates and Sluggish Economy Fuel European Bankruptcies EU bankruptcies surge to the highest level since 2015, nudged by the end of pandemic-era aid

(…) The number of European Union businesses filing for bankruptcy in the three months to the end of June rose 8.4% from the previous quarter, reaching the highest level since 2015, according to Eurostat, the European Union’s statistics office. Registrations of new businesses fell 0.6%.

Bankruptcy filings rose in all sectors of the European economy, according to Eurostat, with hotels, restaurants and transportation companies hit especially hard in the second quarter. (…)

In July, the number of companies going into administration in Germany rose 24% compared with a year earlier, according to the Federal Statistics Office, as a combination of high costs for energy and raw materials, rising interest rates, and the late impact of phased out pandemic-era subsidies forced companies to seek protection from creditors.

“We’re now seeing the market shakeout,” said Christoph Niering, head of the Professional Association of Insolvency Administrators in Germany.

Niering says many companies that are seeking protection now were already struggling before the pandemic. But government support during the pandemic and in the wake of Russia’s invasion of Ukraine kept them on life support. Now, the crash is unfolding in slow motion. (…)

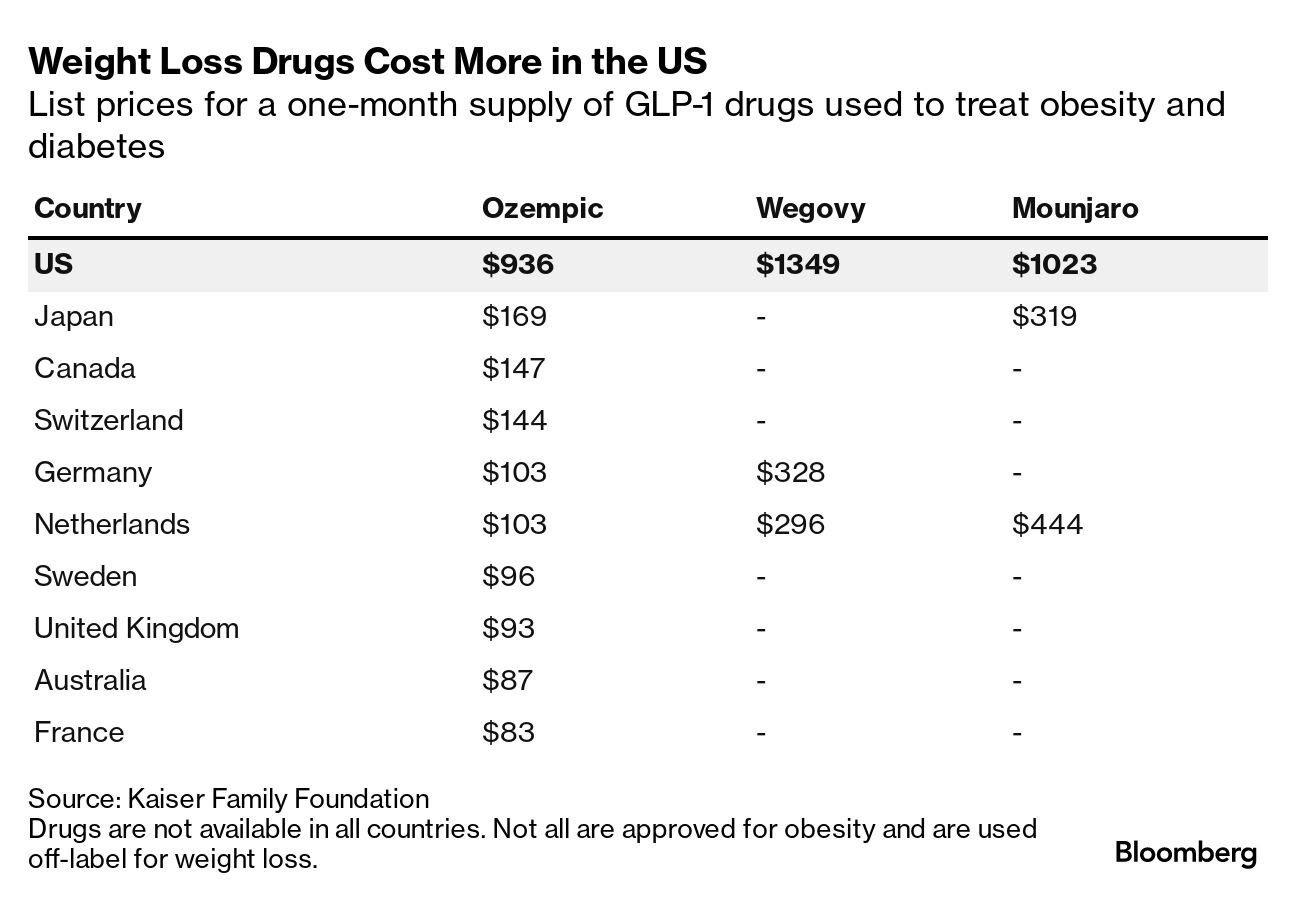

The Ozempic Craze Could Put These Companies on a Crash Diet Anti-obesity medications could affect industries that benefit from America’s food problem.

(…) Until recently, though, investors in industries that help treat the consequences of obesity weren’t really sweating. But after a study was released this month showing Novo Nordisk’s Wegovy (the weight-loss version of Ozempic) helped reduce heart attacks and strokes, companies that make medical devices like glucose-monitoring systems and sleep-apnea machines plunged in value. Developers of drugs for fatty liver disease, which is linked to obesity, have also fallen sharply. (…)

Some analysts are even starting to project that reduced cravings could moderately curb demand for fast-food restaurants and packaged snacks.

To understand the potential impact on some sectors, it is important to bear in mind that drugs like Ozempic and Mounjaro don’t just let you binge on french fries guilt-free. These drugs, originally developed to treat Type 2 diabetes, mimic a gut hormone called glucagon-like peptide-1, or GLP-1, which helps suppress appetite (Mounjaro mimics an additional hormone as well).

People on drugs like Wegovy are less likely to crave Krispy Kremes. And if they stay on the drug for years (unlikely at this stage due to restrictions on most insurance plans), their weight loss could help prevent all sorts of complications, like Type 2 diabetes. That could in turn mean fewer sales of things like insulin pumps and sleep apnea machines. And people who slim down could hit the cancel button on their dieting apps. (…)

All this is very hypothetical for now: Paying for the treatment of 100 million obese Americans would literally make Medicare insolvent at the drugs’ current prices. Eventually, though, as data shows longer-term benefits that extend beyond weight loss, insurance coverage will expand.

(…) Intuitive Surgical, the maker of da Vinci robots used in bariatric surgery, warned investors last month that the drugs are starting to hurt demand. (…)

Intuitive’s warning prompted a broader decline in a sector that racks up about $40 billion in annual sales for things like knee replacements, kidney disease and heart-failure machines. The impact could be biggest for businesses that treat conditions that are highly correlated with obesity such as sleep apnea, Type 2 diabetes, and total knee replacements, according to a Morgan Stanley report. (…)

- America’s Obsession With Weight-Loss Drugs Is Affecting the Economy of Denmark Novo Nordisk’s market capitalization has matched the GDP of its home country

(…) Novo Nordisk’s U.S. sales of Ozempic and Wegovy have been so strong that it has had to convert dollars into kroner in unusually large quantities, raising the krone’s value relative to the euro, said Danske Bank director Jens Naervig Pedersen. (…)

Denmark’s central bankers have responded by keeping interest rates below the European Central Bank’s, weakening the krone, said Pedersen. (…)

FYI: So far, US insurers haven’t been convinced the medications are worth the cost. Just a quarter of private insurance plans cover the drugs, and they’re not available through Medicare. (Bloomberg)