HAPPY HOLIDAYS!

The Daily Edge will be published sporadically in the next 2 weeks.

A special thank you to donators who help support this blog. Very, very much appreciated.

Apologies if have not sent a personalized thank you note like I normally do. The recent weeks/months have been particularly busy for me.

On January 3rd, I will begin my 14th year blogging!

U.S. Leading Economic Indicators Strengthen in November

The Conference Board’s Composite Leading Economic Indicators index rose 1.1% (9.8% y/y) during November following an unrevised 0.9% October increase. The 0.3% September rise also was unrevised. It was the largest increase in six months and outpaced a 0.9% rise expected in the Action Economics Forecast Survey. The Leading Index is comprised of 10 components which tend to precede changes in overall economic activity.

Eight of the ten index components contributed positively to the November increase including the length of the average workweek, unemployment insurance claims, the ISM orders index, building permits, the interest rate spread between 10-year Treasuries and Fed funds as well as the leading credit index. Orders for consumer goods and materials as well as stock prices also contributed positively. The index of consumer expectations for business & economic conditions fell while real nondefense capital goods orders excluding aircraft held steady.

The Index of Coincident Economic Indicators rose 0.3% (3.6% y/y) in November after an unrevised 0.5% October increase. Stability in September also was unrevised. All four of the component series rose including nonagricultural employment, personal income less transfers, industrial production and real manufacturing & trade sales.

The Index of Lagging Indicators eased 0.1% during November (+0.8% y/y) following a 0.5% October rise, revised from 0.4%. September’s increase was revised to 0.9% from 1.0%. The average duration of unemployment, the change in labor costs per unit of output slipped as did the six-month change in the services CPI. The business inventory/sales ratio, commercial & industrial loans outstanding and the consumer installment credit/personal income ratio rose. The banks’ prime rate held steady.

U.S. Industrial Production Increases Moderately in November

Industrial production increased 0.5% (5.3% y/y) during November following a 1.7% October rise, revised from 1.6%. Motor vehicle parts shortages and recovery from Hurricane Ida affected production last month. A 0.7% rise had been expected in the Action Economics Forecast Survey. Manufacturing output rose 0.7% last month (4.6% y/y) following a 1.4% increase during October, revised from 1.2%.

Durable goods production rose 0.8% (4.9% y/y) last month after a 1.4% October gain. Motor vehicle production rose 2.2% (-5.4% y/y) following a 10.1% rise. Excluding the motor vehicle sector, factory output rose 0.6% (5.5% y/y) after a 0.8% gain. Elsewhere in the durable goods sector, high-tech product production rose 0.7% (6.3% y/y) after a 0.3% rise in October. (…)

In the nondurable goods sector, production improved 0.5% (4.7% y/y) after rising 1.3% in October. (…)

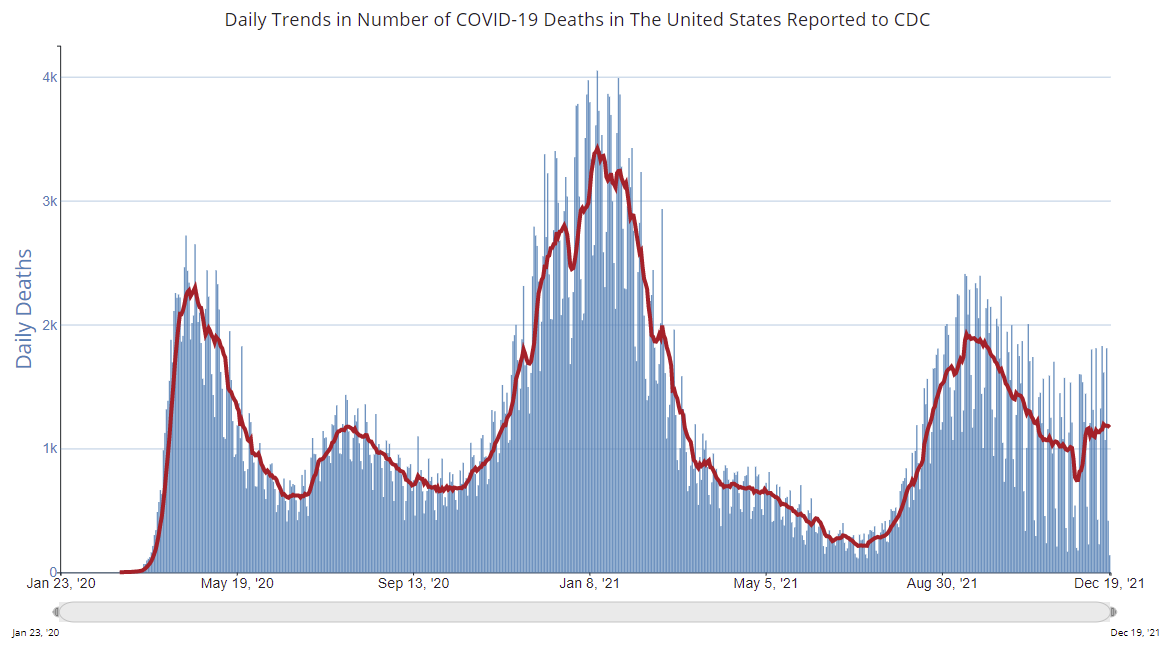

U.S. In-Store Holiday Shopping Holds Up Despite Omicron

Foot traffic to stores and shopping centers in the U.S. on Dec. 18 — the last Saturday before Christmas — rose 19% from a year ago, according to data from Sensormatic Solutions. (…)

Black Friday week and the first three weeks of December clocked foot traffic increases of 14% and higher compared to last year.

While store visits jumped from last year — the first holiday season during the coronavirus pandemic — they didn’t fully rebound to 2019 levels. Shopper traffic on Saturday was down 26% from two years ago, according to Sensormatic Solutions, a subsidiary of Johnson Controls International Plc that analyzes foot traffic by counting mobile devices at stores.

The Chase consumer card spending tracker is up 1.2% from pre-Covid trends (7-day average through December 14). Millennials’ spending is up 8.3%, Gen x’s +0.7% and Boomers’ -5.3%. “Buy-Now-Pay-later”?

Shipping and Logistics Costs Are Expected to Keep Rising in 2022 Executives say the tight capacity and high demand that have sent prices surging this year will extend into next year

Transportation and logistics providers are seeking big boosts in prices for contracts for the coming year, signaling that the inflationary pressure driven by strong demand and tight capacity in freight markets is likely to persist.

With high shipping demand still far outweighing tight capacity across the freight sector, industry experts say transport operators have leverage to raise prices when negotiating new contracts. Ocean-shipping executives say they expect the rates set in many annual contracts will double compared with agreements struck earlier this year, before supply-chain bottlenecks squeezed capacity. Some trucking companies project double-digit growth in contract rates for 2022.

Prices have been rising across the freight sector, including in parcel delivery, trucking, ocean shipping and warehousing. Most freight-transportation contracts are negotiated annually, although many large shippers may have multiyear agreements with a variety of carriers. (…)

Overall, domestic shipping rates for moving goods by road and rail in the U.S. are up about 23% this year from 2020, according to Cass Information Systems Inc., which handles freight payments for companies.

A separate measure in the Logistics Managers’ Index that tracks overall logistics prices, including transportation, warehousing and inventory prices, reached a record in November, up 3.4% from October and a 14% increase year-over-year. The index was launched in 2016. (…)

Mr. Leathers, who said contract rates could rise by high single-digit to mid-double-digit percentages in 2022, expects price increases to moderate as transportation demand eases and companies finish replenishing depleted inventories. However, he said, “We don’t foresee that until 2023. All of 2022 we view as a capacity-constrained market with inflationary pressure and with significant equipment disruptions.” (…)

Delivery giants FedEx Corp. and United Parcel Service Inc. both said rates would go up an average of 5.9% next year across most services, the first time in eight years that either company had annual increases above 4.9%. (…)

Xeneta said the spot price to ship a 40-foot container from Shanghai to Los Angeles earlier this month was 75% higher than the same time last year. Carriers “go into contract negotiations right now holding the lion’s share of the aces,” said Peter Sand, Xeneta’s chief analyst.

Seko Logistics, an Itasca, Ill.-based freight forwarder, says its contracted rate to ship a 40-foot container from Asia to the U.S. West Coast could double next year to between $6,500 and $7,000. In 2019, the firm paid ocean carriers about $1,500 for the same service. (…)

Prices to lease industrial properties have jumped 25% on average nationwide over rates tenants paid at the end of five-year leases that expired in the third quarter, real-estate firm CBRE Group Inc. said in early December. (…)

Overall, transportation rarely exceeds more than 7% of the cost of goods being shipped, (…)

European gas prices hit record as Russian gas flows via Yamal reverse European gas prices hit a new high on Tuesday after Russian shipments to Germany via a major transit pipeline reversed direction, a move the Kremlin said had no political backdrop as one western firm said Gazprom was meeting its supply obligations.

Defensive bubble stocks = umbrellas in a hurricane When a bubble crashes, every part of it goes down

From Richard Bernstein Advisors:

(…) Many investors tried to take a similar approach during the late-90s, but unfortunately, with little success.

- Strategy 1: Buy proven leaders. During the Tech Bubble, the largest stocks in the Tech sector were widely considered established winners with solid fundamentals, such as Microsoft, Cisco and Intel. Not only did the stocks of the ten largest “proven leaders” crash by an average of 84% during the bear market, half of them never recovered their peak, while those that did took an average of 15 years to do so.

- Strategy 2: Buy tomorrow’s winners. What if investors were able to predict the future winners? Of today’s ten largest Tech stocks, also including Communication Services and Amazon, those that were publicly traded at the peak of the Tech Bubble fell by an average of 72% during the bear market and took over 11 years to recover their peak.

One of too many: Nikola Corp, which went public via SPAC last year, agreed to pay $125 million to settle with the SEC over charges that it defrauded investors. (SEC via Axios)