U.S. Flash PMI: Recovery gains momentum amid sustained upturn in demand

U.S. output growth regained growth momentum in October, as business activity rose at the fastest rate for 20 months and business optimism improved markedly. The upturn was largely driven by service providers, though manufacturing firms also reported a further solid increase in production.

Adjusted for seasonal factors, the IHS Markit Flash U.S. Composite PMI Output Index posted 55.5 at the start of the final quarter of 2020, up from 54.3 in September and signalling the fastest increase in private sector business activity since February 2019. Service sector firms recorded a marked and accelerated rate of expansion in output.

The quicker pace of increase in activity signalled the return of growth momentum, following a slight dip in the pace of expansion at the end of the third quarter.

Although the upturn in activity quickened, the pace of new business growth eased slightly in October. Slower expansions in new orders were seen among manufacturers and service providers, with some firms stating that the ongoing impact of the coronavirus disease 2019 (COVID-19) pandemic had weighed on demand. Other companies noted that a number of clients were holding back on placing orders until after the upcoming presidential election. Nonetheless, the rise in new business remained solid overall and was the second-fastest since March 2019.

Meanwhile, the increase in foreign client demand slowed notably, as manufacturers registered a renewed contraction in new export orders.

With the rate of growth in activity outpacing that of new orders, firms recorded a slower accumulation in backlogs of work. As a result of this reduced pressure on capacity, companies expanded their workforce numbers at a slower rate than that seen in September.

On the price front, input costs rose strongly in October, albeit at the slowest pace for four months. The softer rise was driven by service providers, as manufacturers indicated a faster increase in cost burdens. At the same time, the rate of output charge inflation eased, as firms sought to boost sales by price discounting and struggled to pass on higher costs to clients.

Finally, business confidence picked up notably across the manufacturing and service sectors, signalling the greatest degree of confidence since May 2018. Greater optimism regarding the outlook for output over the coming year stemmed from expectations of sustained client demand, political uncertainty easing after the election and hopes of an end to COVID-19 related restrictions at some point over the coming year.

The seasonally adjusted IHS Markit Flash U.S. Services PMI™ Business Activity Index registered 56.0 in October, up from 54.6 in September. The index reading bounced back from the slight dip seen at the end of the third quarter, and indicated the sharpest expansion in business activity since February 2019.

The rate of new business growth remained strong overall in October, but softened amid ongoing COVID-19 restrictions and a slower expansion of new export business.

Reflecting softer pressure on capacity, firms increased their workforce numbers at a slower pace in October. The rate of employment growth was faster than the series average, but dipped to a three-month low.

Meanwhile, inflationary pressures also eased. Despite a further strong rise in cost burdens, service providers sought to generate more sales and limit increases in output charges.

Service sector firms were, however, much more upbeat regarding the outlook for business activity over the next year. The degree of optimism was the strongest since April 2018 amid hopes of an end to COVID-19 restrictions.

Goods producers signalled the quickest improvement in the health of the manufacturing sector since the start of 2019, as highlighted by the IHS Markit Flash U.S. Manufacturing PMI™ posting 53.3, up fractionally from 53.2 in September. October data signalled a fourth successive monthly expansion and a further move away from the substantial contraction seen in April.

Despite the rate of production growth slowing at the start of the fourth quarter, the expansion in new orders accelerated and was the sharpest since January 2019. The upturn broadly stemmed from domestic clients as new export orders fell for the first time since July.

Nonetheless, firms were better able to process new business inflows as the accumulation in backlogs of work eased to only a marginal rate. As such, manufacturers registered a slower rise in employment in October. Some firms, however, stated that difficulties finding suitable candidates weighed on their ability to hire.

In line with their service sector counterparts, manufacturers indicated greater confidence in the outlook for output.

Goods producers noted the increased use of discounting to attract clients during October, with selling prices rising only moderately. In contrast, cost burdens rose the steepest rate since January 2019 amid supplier shortages.

PMI readings are diffusion indices, measuring the percent of respondents saying biz is better this month than last month. How much better and how does it compare with 6 or 12 months ago is not specified.

The Philly Fed polled 143 firms between Oct. 5-15 asking about their level of new orders vis-a-vis their expectations before March 2020. Actual vs pre-pandemic budget. “All firms” are experiencing a 15.3% shortfall in new orders vs budget; manufacturers: -7.6%, non-manufacturers -18.9%, all shortfalls roughly unchanged since June.

These next charts plot actual new orders for various manufacturing sectors for the 12 months ended in August. Manufacturing has been much stronger than services in 2020. Yet, manufacturing orders remain 5% to 13% lower than in February, the only exception being consumer durable goods which lately saw a surge in new orders after their collapse through May.

August total manufacturing shipments were down 6.0% from February and 5.3% YoY. New orders still being negative, shipments growth will likely keep swooshing, if not trending downward in coming months.

China Trade War Didn’t Boost U.S. Manufacturing Might Hundreds of billions of dollars in tariffs on Chinese goods imposed by the Trump administration didn’t achieve the central objective of reversing a U.S. decline in manufacturing, economic data shows.

The tariffs did succeed in reducing the trade deficit with China in 2019, but the overall U.S. trade imbalance was bigger than ever that year and has continued climbing, soaring to a record $84 billion in August as U.S. importers shifted to cheaper sources of goods from Vietnam, Mexico and other countries. The trade deficit with China also has risen amid the pandemic, and is back to where it was at the start of the Trump administration.

Another goal—reshoring of U.S. factory production—hasn’t happened either. Job growth in manufacturing started to slow in July 2018, and manufacturing production peaked in December 2018.

Mr. Trump’s trade advisers nonetheless say the tariffs succeeded in forcing China to agree to a phase one trade deal in January, in which Beijing agreed to buy more U.S. goods, enforce intellectual property protections, remove regulatory barriers to agricultural trade and financial services and to not manipulate its currency.

They also say the tariffs—which remain on about $370 billion in Chinese goods annually—will over time force China to end unfair practices and help rebuild the U.S. manufacturing base. (…)

An industry-by-industry analysis by the Federal Reserve showed that tariffs did help boost employment by 0.3%, in industries exposed to trade with China, by giving protection to some domestic industries to cheaper Chinese imports.

But these gains were more than offset by higher costs of importing Chinese parts, which cut manufacturing employment by 1.1%. Retaliatory tariffs imposed by China against U.S. exports, the analysis found, reduced U.S. factory jobs by 0.7%. (…)

US chokehold pushes China chip self-sufficiency up the agenda Beijing’s plans for sector in spotlight as Communist party develops next five-year plan

NY Fed: How Has China’s Economy Performed under the COVID-19 Shock?

(…) Our analysis of China’s economic performance focuses on alternative growth indicators, or proxies, due to long-standing controversies over the accuracy of China’s official GDP growth statistics; (…)

Our alternative indicators are based on methodologies recently published in a special China-focused issue of the New York Fed’s Economic Policy Review (EPR). The first two proxies use weighted indexes of certain economic variables, with the weights derived from regressions of satellite nighttime lights on provincial level data. It is well-established that satellite nighttime lights are strongly correlated with measures of economic activity, both in terms of levels and growth rates. We refer to one approach as “NTL-Narrow,” and it is based on the “Li Keqiang index” in that it uses similar underlying series, but also includes official GDP growth, as we find it to have explanatory power. The nighttime lights regression suggests placing a considerably larger weight on loans relative to electricity and rail freight than does the original Li Keqiang index.

The second alternative indicator we refer to as “NTL-Broad,” which incorporates a broader range of data, such as air passenger transport and retail sales, among other sources. Finally, the third indicator uses a methodology called sparse partial least squares regression (SPLS), which employs a very broad range of about sixty-two monthly series and is “trained” to explain variation in China’s imports, retail sales, and a diffusion index of industrial production.

The two panels in the chart below compare the average of our alternative indicators to China’s official GDP and to China’s imports, as reported by exporting countries, following the method of Fernald, Hsu, and Spiegel up through the middle of 2019. The reason to compare the alternative indicator to China’s imports is two-fold: First, imports are expected to be well-correlated with China’s business cycle, so they should provide a window into China’s true economic performance. And second, by using China’s imports as reported by its trading partners, we can bypass inaccuracies in China’s own statistical system. All the data have been converted to similar units in that the average and standard deviation of each series are zero and one, respectively‘

GDP, imports, and the “Average Alternative” indicator show similar cyclical patterns until around 2013, when the official GDP figures become much smoother through about the middle of 2018, after which the series track each other more closely again. The Average Alternative shows more cyclical variation in growth than has been reported in official GDP over at least the past five years. By contrast, the alternative indicator performs better than official GDP data with China’s imports over this same period. The details of these indicators and their correlations with both Chinese and global activity are beyond the scope of this post, so the interested reader should refer to our EPR article for the technical discussion.What do the alternative indicators say about China’s GDP growth immediately before, during, and after the COVID-19 lockdown? We focus on relative changes in growth rates in terms of units of official GDP, since we cannot identify the “true” growth rate under any of our methodologies, but can make comparisons of the values of our alternative indicators over periods of time. For reference, China’s official GDP growth rate dropped from about 6 percent in the fourth quarter of 2019 to -6.8 percent in the first quarter of 2020, and then rebounded to 3.2 percent and 4.9 percent in the second and third quarters, respectively, of 2020.

The charts below plot the change in growth, relative to the end of 2013, as implied by the average of our three alternative indicators against the change in the official growth rate (left panel), and the three alternatives separately (right panel). First, there is no evidence that the decline in the official GDP growth rate in the first quarter was understated—in fact, the average of the alternatives declined by roughly two-thirds as much. We therefore argue that the official statistics correctly portrayed the magnitude of the COVID-19 hit to GDP growth in China. There is no evidence from these indicators that the authorities “sugarcoated” the growth data.

Second, there is considerable variation among the alternatives themselves. The NTL-Broad indicator shows a larger decline in GDP growth than did the official statistics, while the other indicators tend to be closer together and show smaller declines. These differences largely reflect the degree to which the alternatives capture declines in service-oriented versus goods‑producing sectors. Both the NTL-Broad and the SPLS alternatives better include—albeit imperfectly—service-oriented industries compared with the NTL-Narrow. This is a very important distinction because a key, and essentially unprecedented, feature of the COVID-19 crisis has been a collapse in service-oriented activities, both in China and around the world. For this reason, we believe that the NTL-Broad and SPLS indicators are giving the best read on China’s economy at present. However, the NTL‑Broad may be putting too much weight on the collapse in air passenger traffic and real estate activity in the first quarter, while the SPLS may be better reflecting the fact that some important goods-producing sectors (such as heavy industry, medical equipment, and electronics) held up relatively well.The alternatives suggest that the growth rebounds in the second and third quarters were strong, but perhaps not as large on average as portrayed in the official statistics. The cumulative change in growth during the first three quarters of 2020 ended up being very similar in both our alternative and the official data. By all accounts, manufacturing, infrastructure investment, and property construction have rebounded quite strongly in China, responding to government-directed fiscal and credit stimulus. By contrast, consumption in China has experienced a slower rebound and showed positive year-over-year growth only in the third quarter of this year.

China was “first in, first out” of economic “lockdown” under the pandemic and appears poised to show quite strong quarterly growth for the remainder of 2020. China’s economic rebound should be driven by domestic economic stimulus, as evident in a large increase in its aggregate credit impulse (the change in new credit as a percent of GDP), as illustrated in the chart below. With China possessing the world’s second largest economy (at market exchange rates), a strong rebound in China should help attenuate declines in economic activity elsewhere. Indeed, during its recovery from the global financial crisis, China’s GDP grew by over 9 percent for nine consecutive quarters.

But there are reasons why the strength of rebound might not last. As discussed in our EPR article, the accelerating phases of China’s business cycles have lasted only about four quarters over each of the past three cycles, less than half the length of the cycles during the early- to mid-2000s. The shorter periods of stimulus reflect the government’s on‑again, off-again efforts to rein in the high growth of debt at the local government, corporate, and, increasingly, household sectors. Given the recent trend of policy cycles, by the first or second quarter of next year, China may well be tightening macroeconomic policy again due to concerns over financial stability.Moreover, as discussed by our colleague Matthew Higgins in his article in the EPR’s special issue, growth in China was already facing structural headwinds even before the COVID-19 crisis, owing to demographics and declining returns to capital accumulation. Higgins lays out three scenarios for growth over the coming decade under which per capita income growth could slow to between 2.7 percent to 4.9 percent, both of which would be well below the official per capita growth rate of about 6 percent in 2019.

Will Americans Go on a Spending Spree? In his latest essay, Richmond Fed President Tom Barkin explores whether the $1.1 trillion extra in people’s pockets will lead to large future spending after the pandemic.

(…) When stimulus boosts income at the same time spending drops, naturally savings will rise. But the effects were uneven. The less fortunate received the great majority of the stimulus payments, but they tend to spend a greater percentage of what they make, as they are more likely to live paycheck to paycheck. Researchers found that, in April, the top income quartile accounted for 40 percent of the decline in consumer spending, and high-income spending has still not recovered. In contrast, as of September, low-income spending is exceeding pre-crisis levels.

As the saving rate grew, we also saw a significant shift in spending from services to goods. As of August, spending on goods was up 5.8 percent from a year ago, and sectors like residential, automotive and recreational equipment were booming. But with continuing health concerns and capacity limitations, services spending is still down 7.2 percent from a year ago. This is challenging the travel, restaurant and entertainment sectors, among others.

Will these increased savings, combined with pent-up demand, fuel consumption that can support the recovery in the coming months? No other spike on record matches the intensity of the current saving rate increase, but there is one other period in which we saw it increase dramatically — during World War II. Right before World War II, the personal saving rate averaged 5 percent. During the war it climbed upward, peaking in 1944 at 27.9 percent, then dropped rapidly. It fell to a three-year average of 7.4 percent from 1947 to 1949. Similar to today, government-imposed restrictions on consumption (both rations and the redirection of resources to the war effort) decreased consumer spending. After the war, pent-up demand lifted the recovery: $24.2 billion was added to consumer spending between 1945 and 1946.2

Could something like this happen again? If we get a vaccine or compelling virus treatment, could we see a trillion-dollar boost to the economy?

Economic theory suggests we temper our optimism. There is a lot of research on how people behave after they receive windfalls. Asset-driven wealth, such as home price appreciation or stock market growth, doesn’t appear to increase spending very much, perhaps because those gains tend to be concentrated among those already wealthy and can be costly to liquidate. Tax transfers often increase spending more, especially for those at lower incomes, but the marginal propensity to consume tax windfalls is still only in the range of 40 percent. And, as I noted earlier, uncertainty matters. People tend to spend gradually to retirement and the higher the uncertainty, the higher the propensity to save.

What does all of this mean for today? With service sector capacity still constrained, we should expect any spending to continue to focus on goods. That may mean a healthy holiday season. With additional stimulus not yet forthcoming, we should expect lower-income families to tap the savings they accrued through the stimulus. And if we get a vaccine, one has to imagine that higher-income individuals will want to take a trip or at least go out to a nice dinner.

At the same time, we know that the wealthy are less likely to spend their savings, and one only has so many vacation days. In addition, service sector spending is historically steadier than spending on goods — missed haircuts or dental appointments or business trips are unlikely to be made up. In a recent Gallup poll, among Americans who are currently able to save money, 76 percent plan to keep adding to their savings in the next six months. So, while some resurgence is likely, it may well look a lot more like a steady path back to normal than like the celebration of V-J Day.

State and Local Governments: Economic Shocks and Fiscal Challenges

(…) State and local governments are significant players in the U.S economy. At the beginning of 2020, they employed approximately 20 million workers, which represented 13 percent of total U.S. employment. In 2017, their expenditures totaled $3.1 trillion or approximately 15 percent of U.S. gross domestic product. Local governments spent just over half of this amount, with their largest expenditure shares going to K-12 (40 percent), health care (10 percent), and police services (6 percent). State governments spent a modestly smaller sum of money, with the largest shares devoted to public welfare (43 percent), higher education (18 percent), and health services (9 percent). (…)

State and local governments are typically required by state laws to balance their budgets regularly, so when their revenues fall, they often have no recourse but to cut spending. When this belt tightening happens, state and local governments almost always end up paring down on essential services, including education, health care, and social welfare programs. Research tells us that these kinds of funding disruptions create long-lasting damage to individuals’ earnings. (…)

Next year’s budgets are expected to more fully capture the fiscal effects of the COVID-19 pandemic. Cities are forecast to see a 13 percent decline in revenues in 2021, although it is not yet clear how commercial property tax revenues will be affected by near-term business closures and longer-term changes in the demand for office space. Moreover, it is uncertain how the expiration of eviction moratoriums will affect the value of multifamily housing units or how the crisis will ultimately affect the value of owner-occupied residential property.

States and local governments tend to respond to revenue declines by cutting social services and canceling or postponing capital projects. And these austerity measures tend to involve payroll reductions through layoffs, furloughs, and hiring freezes. Following the Great Recession, for example, we saw large cutbacks in local public employment — which did not recover to pre-recession levels until 2019. As a result of the COVID-19 pandemic, we are now seeing large declines in local public employment, but the changes are more abrupt and on a larger scale than during past recessions.

Evidence from the previous recession also suggests that overall education funding will decline sharply due to COVID-19. Public schools are mainly funded by state and local governments, in almost equal proportions. As revenues fall, resources devoted to education will likely decline as well. (…)

Quantifying the effects of educational disruptions, the evidence suggests that when spending goes down by $1,000 per student, several bad things happen: Average test scores in math and reading fall by 3.9 percent of a standard deviation, the test score gap between black and white students increases by 6 percent, and the college-going rate declines by 2.6 percent. Another study found that a 12-week school closure (similar to the one we experienced recently) could reduce test scores in math by 9 percent of a standard deviation. (…)

State and local governments are responsible for a growing share of public service provision in the United States. The fact that these governments are limited in their ability to fully smooth expenditure when revenue drops means that, in the absence of sizable federal transfers, a large amount of local government services will be disrupted by the current economic downturn. State and local spending is critical for delivering human capital, but a key feature of human capital is that skills beget skills. Consequently, disruptions now are likely to cause significant long-term value losses. The considerable impact of state and local government spending on everyday lives makes it clear that it is not only relevant for the recovery, but also for the long run.

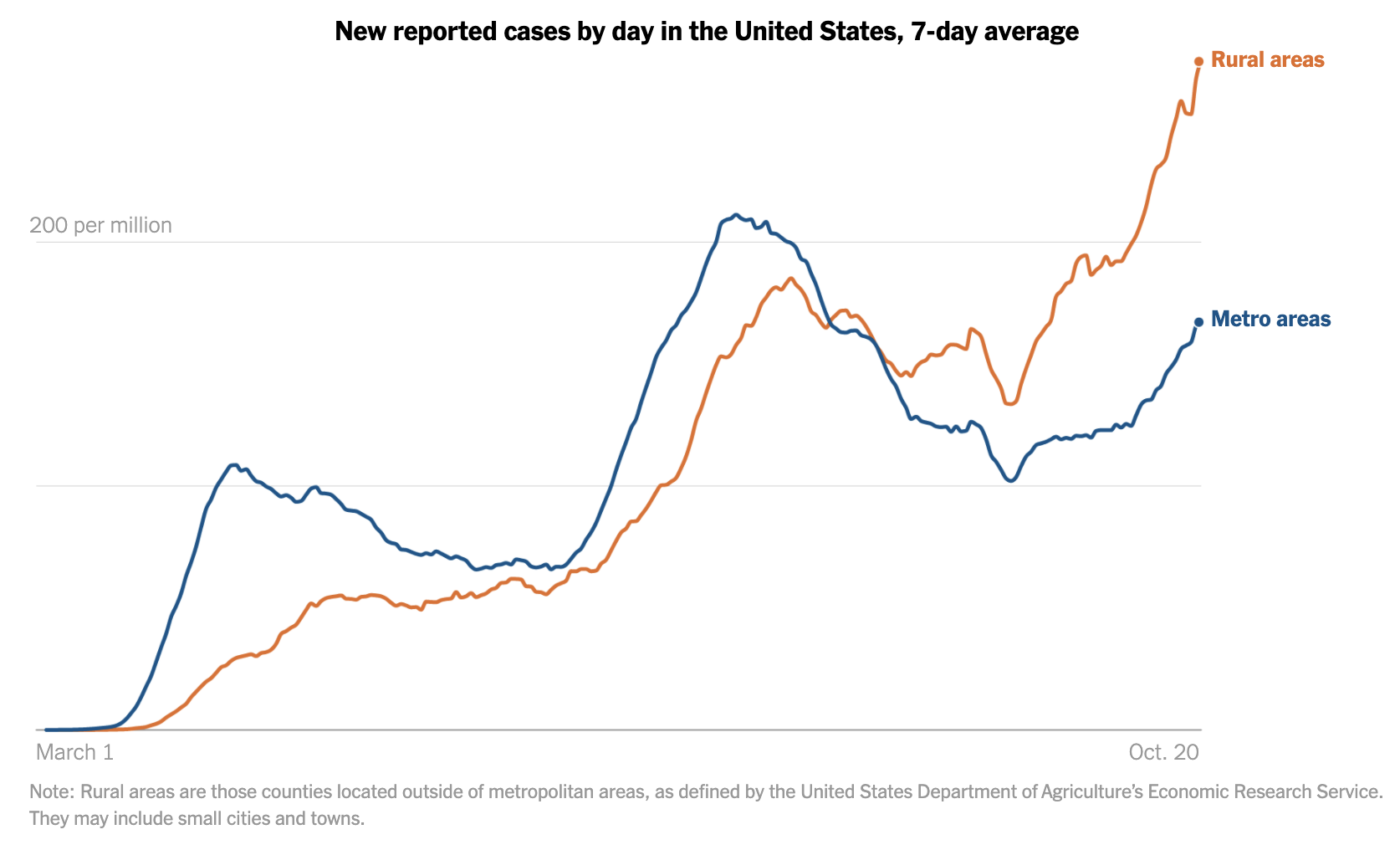

VIRUS UPDATE

Turning all corners:")

")

EARNINGS WATCH

- We now have 135 reports in, a 84% beat rate and a +17.7% surprise factor with all sectors surprising positively in both earnings and revenues (only exception on revenues: Utilities: -9.0% surprise).

- The estimated earnings growth rate for the S&P 500 for 20Q3 is -16.7%. If the energy sector is excluded, the growth rate improves to -12.4%. 20Q3 revenue is expected to be -3.6% from 19Q3. Excluding the energy sector, the growth estimate is -0.6%.

- The estimated earnings growth rate for the S&P 500 for 20Q4 is -12.4%. If the energy sector is excluded, the growth rate improves to -9.5%.

- Trailing EPS are now $137.85, on their way to $132.13 for the whole year 2020 and $166.61 estimated for 2021.

VALUATIONS

- P/E RATIOS, USA VS WORLD EX-USA

- P/E RATIOS: QUALITY, VALUE, GROWTH

Aswath Damodaran tackles value investing in a 3-part series.

- Value Investing I: The Glory Days

- Value Investing II: A Lost Decade

- Value Investing III: Rebirth, Reincarnation or Requiem?

Dividend Darlings Trail Stock Market Despite Pumped-Up Yields Some investors are fretting over the sustainability of big dividend payouts from Wall Street’s “dividend aristocrats,” who are trailing the broader stock market this year.

(…) The S&P 500 Dividend Aristocrats Index, which measures the performance of 65 companies, has fallen 0.7% this year, while the broader S&P 500 has risen 7.3%. That puts the benchmark index on pace to outperform the dividend aristocrats index by the widest margin since 2007. (…) The index recently offered a dividend yield of about 2.7%—humble in nominal terms, but still greater than the S&P 500’s dividend yield of about 1.7% and more than triple the yield of the 10-year U.S. Treasury note.

Even so, that hasn’t been enough to persuade investors who have yanked more than $40 billion from global dividend-focused mutual and exchange-traded funds in 2020 through Wednesday, according to data from EPFR. That surpasses the more than $3 billion that was pulled during the same approximate period in 2019. (…)

Some analysts are advising yield-seeking clients to focus more on companies with stable balance sheets and a trend of dividend increases, rather than the firms with the biggest overall dividend yields. (…)

At the close of trading Friday, about 70% of S&P 500 companies had dividend yields above the 10-year Treasury yield, compared with nearly 48% at the end of last year, according to Dow Jones Market Data. The yield on the 10-year Treasury settled Friday at 0.840%. (…)

ProShares which offers the NOBL Dividend Aristocrat ETF provides a few stats, some of which I reproduce here FYI:

(Source: Bloomberg, 9/30/08 to 6/30/20 via ProShares)

(Source: Bloomberg, 9/30/08 to 6/30/20 via ProShares)

P/B alone is not sufficient, it needs to be accompanied by ROE. Return on assets is a fair proxy for ROE (sorry, no data here for Growth):

(Source: Bloomberg, calendar year estimates as of 8/20/20 via ProShares)

(Source: Bloomberg, calendar year estimates as of 8/20/20 via ProShares)

Utility stocks see surge in new uptrends

Utility stocks have managed to hold up better than usual. Earlier in the month, many of those stocks showed short-term surges, which typically lead to lower prices for such a staid sector.

There have been positives for months, like insider buying interest. Those buys have tapered off, but sales have dropped even further, so the Buy/Sell Ratio is still impressively high.

As many of those stocks have held up, more and more of them are crossing above their long-term 200-day moving averages. There was a total wipeout in these stocks during the pandemic crash in March, and even as late as mid-May, every utility stock was below its 200-day average. Over the past week, that has climbed above 80%.

Over the past 30 years, there have been only 3 other times when this sector went from fewer than 5% of stocks above their 200-day averages to more than 80% of them being so within a year’s time.

All 3 of them triggered during the initial recovery from a bear market, leading to large, sustained gains in the months ahead. The risk/reward was heavily skewed to the upside, and none of them saw an abnormally large loss at any point within the next year.

On a short-term basis, a sector like this has a lot of trouble when it reaches overbought levels. But on a medium- to long-term basis, this recovery has impressively positive precedents.

TECHNICALS WATCH

Even though equities have marked time last week and are down 2.3% from their Oct. 12 high, my favorite technical analysis service remains quite positive seeing improving buying/selling balances across all equity cap segments.

But one of my past heroes seem to think differently. Bob Farrell is talking with David Rosenberg, courtesy of CMG Wealth’s Steve Blumenthal:

(…) I view [stocks] as having had an initial “A” wave down.

- I divide market declines into A, B, and C waves.

- A is a sharp down move

- B is the inevitable recovery that happens over the shorter run from three months or six months.

- And then there’s a C wave, and the C wave will be long if the fundamentals are poor and short if the fundamentals are not so bad (or the C wave is shorter if fundamentals are ok and it is more of a liquidity event, as Dave mentioned).

So, when I look at what the bulk of stocks have done, they’ve had this sharp reaction from a bull market high.

- You can argue about this, but I think we’ve had a B wave recovery into June for the majority of stocks.

- About 5% of stocks in the S&P have accounted for all the gains from the lows and the rest of these stocks have been going sideways or down since June.

- Maybe some made marginal highs but overall this is more typical of how a C wave develops, which is a more drawn out corrective process.

- So I think, you know, there’s been a lot of argument about, you know what, what we should expect in 2021 from the market, and it isn’t, you can’t, I can’t look at it as just the market, it looks to me like we’re at a very extreme point on the bull market in the tech and growth stocks. We don’t know if we’ve reached a high yet, this might be just a correction and one more surge to come.

- But I think we’re that close to a high and the growth tech bull market… That doesn’t mean I think it’s going to be a long bear market like fall of 2000 and gross, but I think we’re going to get at least a cyclical type of bear market and growth for different reasons.

I think we’ve had a lot of argument about, which is correct, should we keep going with growth or should we switch to value? And it’s frustrating for many because growth keeps going and value keeps lagging.

- I think we’re setting up for a change in 2021.

- The change, usually occurs when you have a change in leadership in down markets.

- If you remember the top in 2000, which I’m sure you do, we topped in March. It started with the crack in the big growth stocks (at the time the tech stocks).

- And at that time, all the value stocks had been underperforming for a couple of years. And they didn’t go down very much. And so they resisted and their relative performance improved while the money was moving into the highly regarded tech stocks.

- I don’t want to make too big comparisons, but I think to me the, the odds are that things are likely to change for growth. They’re certainly over and over endorsed.

- We all believe that technology is making this world better and it’s going to continue to change how we behave and help us do things differently. And I’m not trying to be an anti-technology person,

- I’m just trying to say, as far as the tech stocks are concerned, there’s too much of an aura of invincibility about them. It seems to me that we are close to a top area for the growth side of the market.

(…)- I want to say that we just shouldn’t look at the S&P. If you want to get the broader context of markets, you look at the New York Stock Exchange index which has 1,700 stocks, and the New York Stock Exchange index has had about two-thirds recovery of losses.

- And I think from that standpoint it fits with the typical ABC pattern that I’ve seen in history. When you have markets that shake out and are going into some kind of a bear phase, you ask, “Is the market predicting that there’s going to be a bad economy to come?” I don’t know but I just think, the odds are increased that we’re in a very uncertain period.

- With the election, with so many things that are happening on the bond market front.

- I think the big weakness coming, or the big threat coming next year is that bond market investors are going to have a tough time that the bond market is likely get at its low point in terms of yields.

It’s important to remember that where the most money goes, the profits are least and the risks are highest.

- And we’ve had this big surge into bonds for a long time.

- It’s a 40-year bull market, and we’ve had calls for the bottom and lots of times and I’ve made some that I’ve been wrong about.

- But I do think you’ve got a chance here or a good likelihood that what the 10-year is doing is building a bottom or a rally (higher yields which means losses in terms of price).

- And I think that that’s a background for being a tougher environment for the growth stocks. And we know the government is not very happy with some of the things that some of the leading growth companies or tech companies are doing now.

(…)- And I do look at it though from a perspective of how people behave and you know when they got locked up, they all went into a whole new industry created to trade stocks instead of bet on football games.

- And we do have that speculative element in there and I watch the put-call ratios all the time. There are many investor sentiment polls that give you different ideas of whether people are bullish or bearish but when you look at the put-call numbers, we’ve had some of the lowest numbers on a continuing basis in the last couple of months vs. the last 10 years.

- This is something that makes me think that this is a period where the market is peaking.

- It’s hard for to make a forecast because we have an election that is uncertain and we don’t know how things are going to turn out in an environment that’s so fraught with controversy.

- On an overall basis, I’m looking for some kind of a peak in growth stocks (the growth bull market), where we’ll get some kind of a cyclical correction.

- And I think in that this likelihood you beget relative strength in the, the out-of-favor areas are many of them that were very little interest in buying and buying now. And I think that that’s something to watch, particularly once, we know who wins the election. That’s going to make a difference, what party wins or, whether it’s across the board or not. There’s all kinds of things we can answer, so saying what’s going to happen in the next few weeks toward the end of the year is pretty difficult. Thus, I’d rather be more on the sidelines, letting things clarify but looking for this kind of change.

(Ed Yardeni)

(Ed Yardeni)China’s purchases of U.S. farm goods at 71% of target under trade deal: U.S. China has substantially increased purchases of U.S. farm goods and implemented 50 of 57 technical commitments aimed at lowering structural barriers to U.S. imports since the two nations signed a trade deal in January, the U.S. government said on Friday.

In a joint statement, the U.S. Trade Representative’s (USTR) office and the U.S. Department of Agriculture (USDA) said China had bought over $23 billion in U.S. agricultural goods to date, or about 71% of the target set under the so-called Phase 1 deal. (…)

The report showed outstanding sales of U.S. corn to China were at an all-time high of 8.7 million tons, while U.S. soybeans sales for marketing year 2021 to China were at double the levels seen in 2017.

U.S. exports of sorghum to China from January to August 2020 totaled $617 million, up from $561 million for the same period in 2017, it said.

U.S. pork exports to China hit an all-time record in just the first five months of 2020, and U.S. beef and beef products exports to China through August 2020 are already more than triple the total for 2017, it said.

In addition to these products, USDA expects 2020 sales to China to hit record or near-record levels for other U.S. agricultural products including pet food, alfalfa hay, pecans, peanuts, and prepared foods.