Payroll employment rises by 531,000 in October; unemployment rate edges down to 4.6%

Total nonfarm payroll employment rose by 531,000 in October, and the unemployment rate edged down by 0.2 percentage point to 4.6 percent, the U.S. Bureau of Labor Statistics reported today. Job growth was widespread, with notable job gains in leisure and hospitality, in professional and business services, in manufacturing, and in transportation and warehousing. Employment in public education declined over the month. (…)

The labor force participation rate was unchanged at 61.6 percent in October and has remained within a narrow range of 61.4 percent to 61.7 percent since June 2020. The participation rate is 1.7 percentage points lower than in February 2020. The employment-population ratio, at 58.8 percent, was little changed over the month. This measure is up from its low of 51.3 percent in April 2020 but remains below the figure of 61.1 percent in February 2020. (…)

Thus far this year, monthly job growth has averaged 582,000. (…)

The change in total nonfarm payroll employment for August was revised up by 117,000, from +366,000 to +483,000, and the change for September was revised up by 118,000, from +194,000 to +312,000. With these revisions, employment in August and September combined is 235,000 higher than previously reported.

U.S. Productivity Declines & Unit Labor Costs Surge in Q3’21

Nonfarm business sector productivity fell 5.0% (SAAR) during Q3’21 following a 2.4% Q2 increase, revised from 2.1%. It was the sharpest decline since Q2’81. A 1.8% decline had been expected in the Action Economics Forecast Survey.

Nonfarm business production grew 1.7% last quarter (6.1% y/y). The gain was the smallest in five quarters. Growth of hours-worked surged to 7.0% (6.7% y/y), the strongest rise in three quarters.

Compensation per hour rose 2.9% (4.3% y/y), the fourth straight quarter of growth.

The rise in compensation and the fall in productivity combined to lift unit labor costs 8.3% to a record level, following a 1.1% increase in Q2. A 5.6% increase had been expected.

In the manufacturing sector, productivity declined 1.0% after surging 8.5% in Q2. Output rose a steady 5.7% last quarter (6.3% y/y) and hours-worked increased 6.7% (3.8% y/y) after falling 2.5%.

Factory sector compensation rose 1.9% in Q3, firm for the fourth straight quarter. Unit labor costs rose 2.9% and reversed much of the Q2 decline.

This is the YoY trend:

Since Q4’19, unit labor costs are up 4.4% annualized, way above trend. Let’s see how this, and biz sales, evolve as the economy “normalizes”.

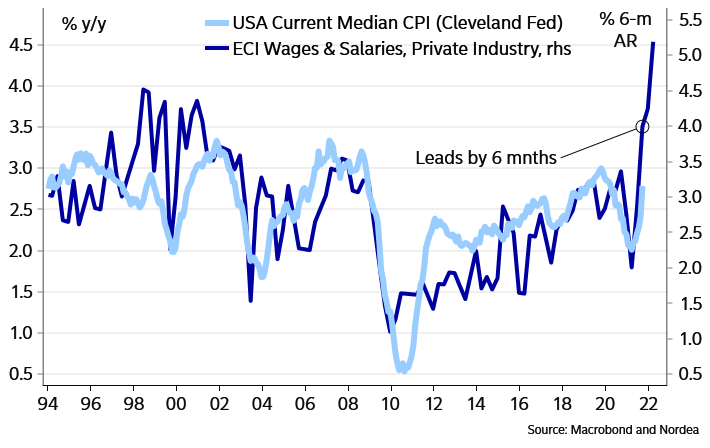

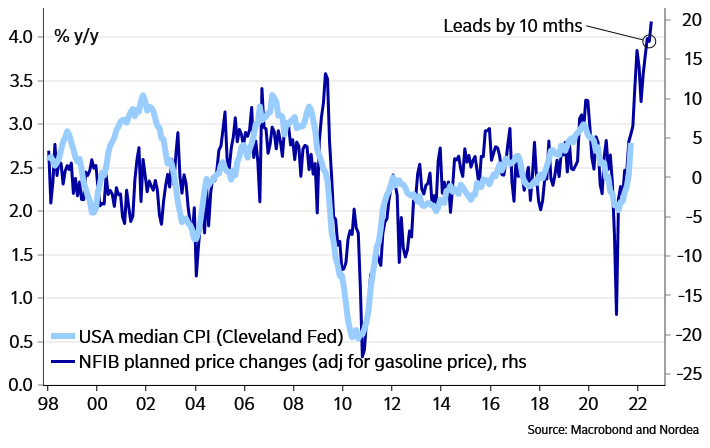

At its Wednesday presser, Powell said “The inflation that we’re seeing is really not due to a tight labor market.” He may be right, but he also could have added “yet” as these Nordea charts suggest:

High labour cost increases should lead to higher median CPI

US companies continue to signal major price hikes

BTW: “the Bakery, Confectionary, Tobacco Workers and Grain Millers’ Union yesterday declined to bring Kellogg’s latest proposal, termed its “best and final offer” by management, to those striking laborers for a vote. “There’s no question that today’s business environment is as challenging as we’ve ever seen it,” lamented CEO Steve Cahillane.” (ADG)

OPEC, Russia Stick to Gradual Oil Production Boost Producers reject U.S. pressure to boost output faster and ease prices

OPEC and a group of Russia-led producers agreed to keep to their gradual, monthly increase in oil output, deciding to boost production by 400,000 barrels a day next month and rebuffing stepped-up pressure from the U.S. to boost output and ease prices. (…)

In recent days, apart from public comments, U.S. officials have reached out to Saudi Arabia, the United Arab Emirates and Iraq, asking to get more oil to the market, according to people familiar with the matter. (…)

“If we increase output all of a sudden and demand is hit in one area because of a new wave of covid, the price would collapse,” a Saudi oil official said. “So bringing back more oil to the market rapidly is not on the cards at the moment.”

- Other supply problems: the number of dairy cows in the U.S. is plunging at a pace not seen in more than a decade, leading to weak production. (…) Global stockpiles of milk powder, which are exported around the world and can be reconstituted into the beverage, have been dropping for four years. (Bloomberg)

- And meat:

U.K. Rate-Decision Surprise Ripples Across Global Bond Markets The Bank of England holds fire on an interest-rate move, triggering the biggest U.K. bond-yield drop in years.

The bank has said it expects to raise borrowing costs soon, moving ahead of the Federal Reserve and other major central banks in withdrawing stimulus to tame inflation.

But the bank held fire Thursday, surprising investors who had become convinced an increase was coming. Yields on one-year government bonds, known as gilts in the U.K., nearly halved within hours, dropping 0.22 percentage point, in their biggest daily move since the 2009 financial crisis. The move also sent the pound down 1.4% against the dollar to $1.349, its biggest one-day fall in more than a year. (…)

Yields on U.S. two-year Treasury notes slipped 0.07 percentage point to 0.41%. German one-year government-bond yields fell 0.08 percentage point to negative 0.83%, their biggest one-day drop since the coronavirus market panic of March 2020, according to FactSet. (…)

Mr. Bailey said he was clear the need for tighter policy was closely linked to developments in the labor market and on inflation.

“It was a very close call,” he said at a news conference. “We are in a situation where the calls are close, they’re quite hard.” (…)

New forecasts showed officials expect annual inflation will be close to 2% in two years and below 2% in three if interest rates are ratcheted higher, to around 1% by the end of next year, as implied by prices in financial markets when the BOE concluded its forecasts. That suggests officials anticipate a slower and steadier path of rate increases than investors. (…)

It expects supply-chain disruption and labor shortages to dog the U.K. throughout next year, pulling expected growth in 2022 to 5%, from a forecast of 6% previously. (…)

Euro zone retail sales record surprise fall on weak Germany

Retail sales, a proxy for consumer demand, in the 19 countries sharing the euro, fell 0.3% month-on-month in September and were up 2.5% from a year earlier, the European Union’s statistics office said.

Economists polled by Reuters had expected a 0.3% monthly rise in retail sales and a 1.5% year-on-year increase.

Part of the month-on-month miss, however, may be down to revisions as retail sales in August were now estimated to be up 1% compared with a 0.3% rise reported earlier. (…)

Eurostat said car fuel sales rose 1% on the month while food, drinks and tobacco sales rose 0.7%. But non food sales dropped by 1.5%, including a 1.4% decline in Internet and mail order sales.

Germany, the euro zone’s biggest economy, recorded the largest, 2.5% drop in retail sales but Finland and the Netherlands were also deep in negative territory.

- German Cases Hit Fresh Record as Fourth Wave Spreads in Europe

- Rising Covid infections in Europe spark fears of new wave WHO says pace of transmission across continent and Central Asia is a ‘grave concern’

U.S. Trade Deficit Deepens to New Record in September

The U.S. trade deficit in goods and services increased to $80.93 billion during September from $72.81 billion in August, revised from $73.25 billion. The latest deficit was a record for the series which extends back to January 1992. A deficit of $80.3 billion was expected in the Action Economics Forecast Survey. Exports declined 3.0% in September (+16.6% y/y) following a 0.6% August gain while September imports rose 0.6% (19.9% y/y) after increasing 1.3% in August.

The trade deficit in goods deepened to $98.2 billion in September from $80.2 billion in August, revised from $89.41 billion. It compared to a $96.25 billion deficit in the advance report issued last week. Exports of goods fell 4.7% (+16.8% y/y) after a 0.8% August rise. Holding back the export total, industrial supplies & materials exports fell 9.9% (31.3% y/y) following a 6.7% rise. Capital goods exports declined 3.6% (+12.3% y/y) after falling 1.9% in August. Auto exports fell 2.0% (-11.7% y/y) following an 8.0% drop. Food exports were off 1.2% (-3.6% y/y), the third decline in four months. Increasing were nonauto consumer goods exports which strengthened 3.7% (30.5% y/y) in September after rising sharply in four of the prior five months.

Imports of goods rose 0.9% in September (18.4% y/y), about the same as in August. Capital goods imports increased 4.0% (18.7% y/y) after falling in three of the prior four months. (…) Nonauto consumer goods imports eased 0.1% (+12.4% y/y), the third decline in four months. Auto imports dropped 7.7% (-16.6% y/y), and they’ve fallen 21.8% since December of last year.

Petroleum imports rose 4.3% in September and have roughly doubled y/y. The monthly rise occurred despite a decline in the price of crude oil to an average $64.43 per barrel from $65.06 in August. The price was substantially higher than $37.60 per barrel one year earlier. Nonpetroleum imports rose 0.6% (14.3% y/y) after rising 1.0% in August.

The real (adjusted for price changes) trade deficit in goods deepened to $111.0 billion (chained 2012 dollars) in September from $101.5 billion in August. Real exports of goods fell 4.9% (+0.8% y/y) after a 0.5% rise. Real imports of goods increased 1.0% (9.9% y/y), the same as in August. (…)

The chart below plots imports and exports, nominal and real, with Q4’19 = 100. Imports are up 13.2% (5.9% real) while exports are unchanged (and down 9.3% in real terms).

JPMorgan cuts China growth forecast for fifth time since August

JPMorgan cuts its fourth quarter growth forecast for China to 4.0% quarter-on-quarter from 5.0% on Friday, citing the impact of power shortages and the recurrence of COVID-19 clusters hitting consumer spending and services.

“Looking back, we have downgraded China’s growth forecasts five times since August,” JPMorgan’s Haibin Zhu said in a note, adding the bank now expected full-year growth of 7.8% and 4.7% in 2022.

China’s housing market is more than “adjusting”: watch commodities!

EARNINGS WATCH

We now have 420 reports in, an 81% beat rate and a declining +10.7% surprise factor, bested by Financials at +18.9% after having cut their loan-loss reserves.

Trailing EPS are now $197.49. 2021e: $204.21. 2022e: $220.63.

Q4’21 EPS are seen up 22.0%, in line with the 21.7% growth expected on Oct.1.

But 2022 growth has been reduced from +9.2% to +7.5%.

![]() We got the first tally of Q4 pre-announcements from Refinitiv/IBES: not off to a good start. Eight more companies than at the same time last year have pre-announced, all negative plus 2 more. Compared with Q3, the N/P ratio has tripled.

We got the first tally of Q4 pre-announcements from Refinitiv/IBES: not off to a good start. Eight more companies than at the same time last year have pre-announced, all negative plus 2 more. Compared with Q3, the N/P ratio has tripled.

Meanwhile, fear is gone:

Canada’s Banks Get Green Light to Resume Share Buybacks, Dividend Increases

![]() Why a New Pill to Treat Covid Could Be a Game Changer Molnupiravir, an antiviral pill being developed by Merck & Co., has been touted as a potential game changer in the fight against Covid-19. The experimental medication was shown to reduce the risk of hospitalization or death by about half in a late-stage study of adults with mild-to-moderate cases. The promise of a drug that patients can easily get and take at home has prompted some governments to order supplies even before most regulators have decided whether to approve its use.

Why a New Pill to Treat Covid Could Be a Game Changer Molnupiravir, an antiviral pill being developed by Merck & Co., has been touted as a potential game changer in the fight against Covid-19. The experimental medication was shown to reduce the risk of hospitalization or death by about half in a late-stage study of adults with mild-to-moderate cases. The promise of a drug that patients can easily get and take at home has prompted some governments to order supplies even before most regulators have decided whether to approve its use.

- Pfizer said its antiviral pill was 89% effective at preventing people at high risk of severe Covid-19 from dying or needing hospitalization, as it plans to ask the FDA to authorize the drug’s use this month. (WSJ)