CONSUMER WATCH

The Chase consumer card spending tracker, updated through November 30, points to a very strong month, ending softly.

Spending on discretionary goods was particularly strong. J.P. Morgan’s calculations give 2.4% growth in November control sales, the strongest growth rate since March and 50% stronger than October’s 1.6% actual growth. So far, so good, but did November borrow from December?

This is from the National Retail Federation:

- In total, 179.8 million unique shoppers made in-store and online purchases during the holiday weekend, exceeding NRF’s initial expectations by over 21 million. The figure compares with 186.4 million shoppers in 2020 and is in line with the average of the last four years. As retailers continue to extend deals and other offers into October and early November, half (49 percent) of shoppers said they took advantage of early holiday sales or promotions before Thanksgiving this year.

- Thanksgiving weekend shoppers spent an average of $301.27 on holiday-related purchases such as gifts, décor, apparel and toys. This is down slightly from $311.75 in 2020.

- The vast majority (84 percent) of holiday shoppers reported they have already started shopping and have completed more than half (52 percent) of their holiday purchases on average.

From Axios:

Spending on Cyber Monday falls 1.4%. (…) During Cyber Week, which begins on Thanksgiving and ends on Cyber Monday, spending totaled $33.9 billion, which is also a decrease of 1.4%. Spending climbed in the days before the Thanksgiving holiday amidst a drumbeat of coverage about supply chain snarls, spurring consumers to start shopping early. Shoppers have shelled out $109.8 billion since November 1, up 11.9% versus the same period a year prior.

Inflation, Falling Unemployment Prompt Fed Pivot The Fed is making plans to accelerate the winding down of its stimulus program, ending by March instead of June and opening the door to raising rates next spring rather than later in the year.

The abrupt shift opens the door to the Fed raising interest rates next spring rather than later in the year to curb inflation, marking a significant policy pivot by Chairman Jerome Powell shortly after President Biden offered him a second four-year term leading the central bank.

With this move, Mr. Powell would be focusing the Fed’s efforts more on restraining inflation and less on encouraging employment to return to its pre-pandemic levels. Inflation has surged this year—to 5% in October from a year earlier, according to the Fed’s preferred gauge—amid strong demand for goods and services and supply-chain bottlenecks associated with reopening the economy. (…)

The Fed still expects inflation to decline next year, but Mr. Powell indicated the central bank doesn’t want to bet the farm on it. “Almost all forecasters do expect that inflation will be coming down meaningfully in the second half of next year,” he said. “The point is we can’t act as though we’re sure of that.” (…)

“We said in the new framework that on inflation, we would wait until we saw the whites in their eyes before firing…and now we’ve seen them,” said Fed governor Randal Quarles in an interview last Wednesday. “We never said we’d let the army march over us.” (…)

“If we didn’t have higher inflation readings, you might let the economy go a little bit more to see if we can get through Covid and have those [unemployed] individuals come back,” said San Francisco Fed President Mary Daly during a webinar last Thursday. “But the same people who might be sidelined and not getting jobs, they’re also paying higher prices. And inflation is a pretty regressive tax.”

We’ve all been warned.

Nordea:

Turning to this week’s US CPI print, we expect core inflation to print >5% with risk to the upside, while headline inflation prints around 6.7%.

US core CPI model built on OER & used car inflation

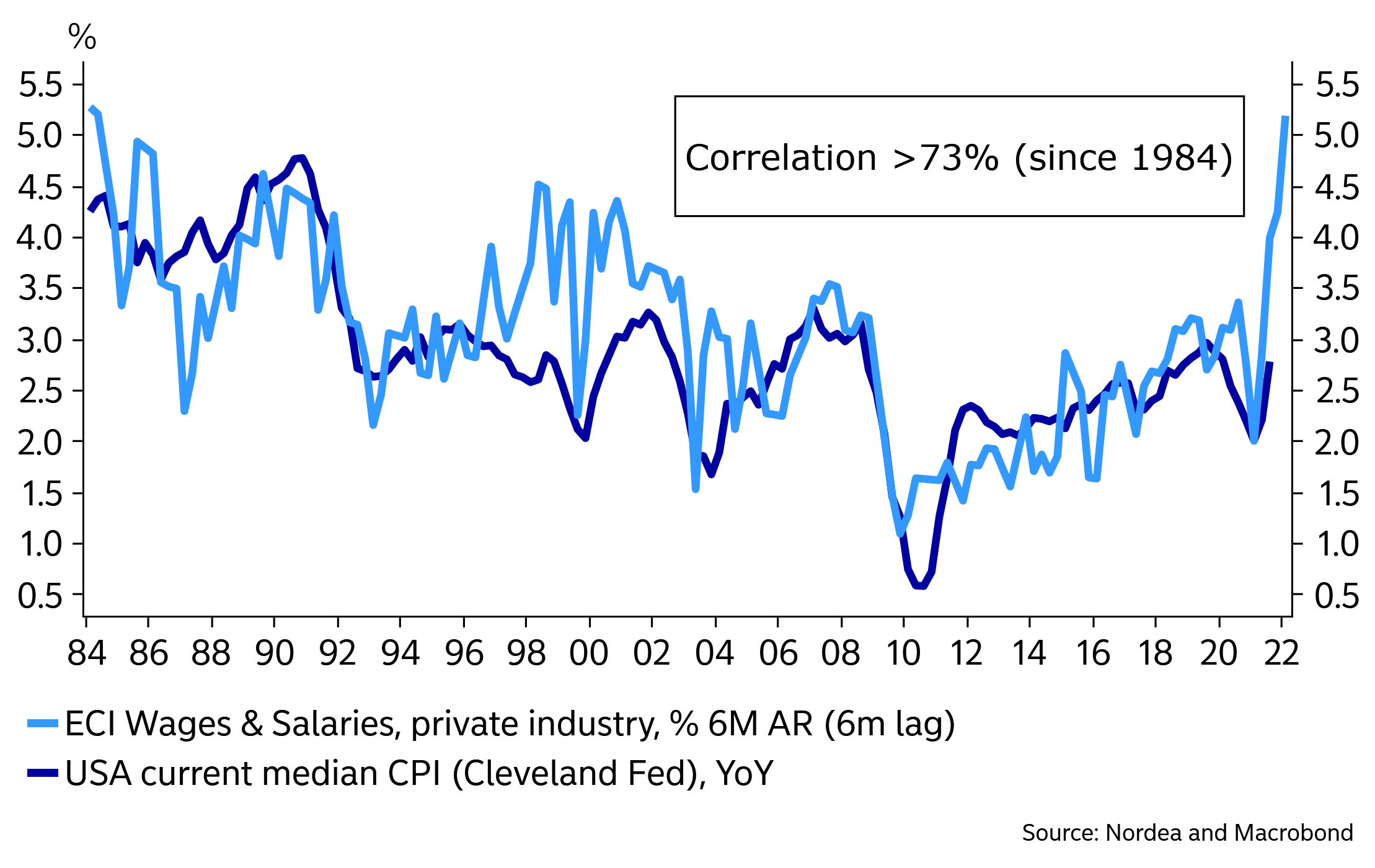

Looking into 2022 we see broad wage growth pushing inflation further up. Wage growth has a clear spillover to higher median CPI with a time lag of 6-9 months (with a correlation of >70% since 1984), which is exactly the kind of inflation that the Fed will have a harder time to refute.

Broad wage growth leads to higher median CPI

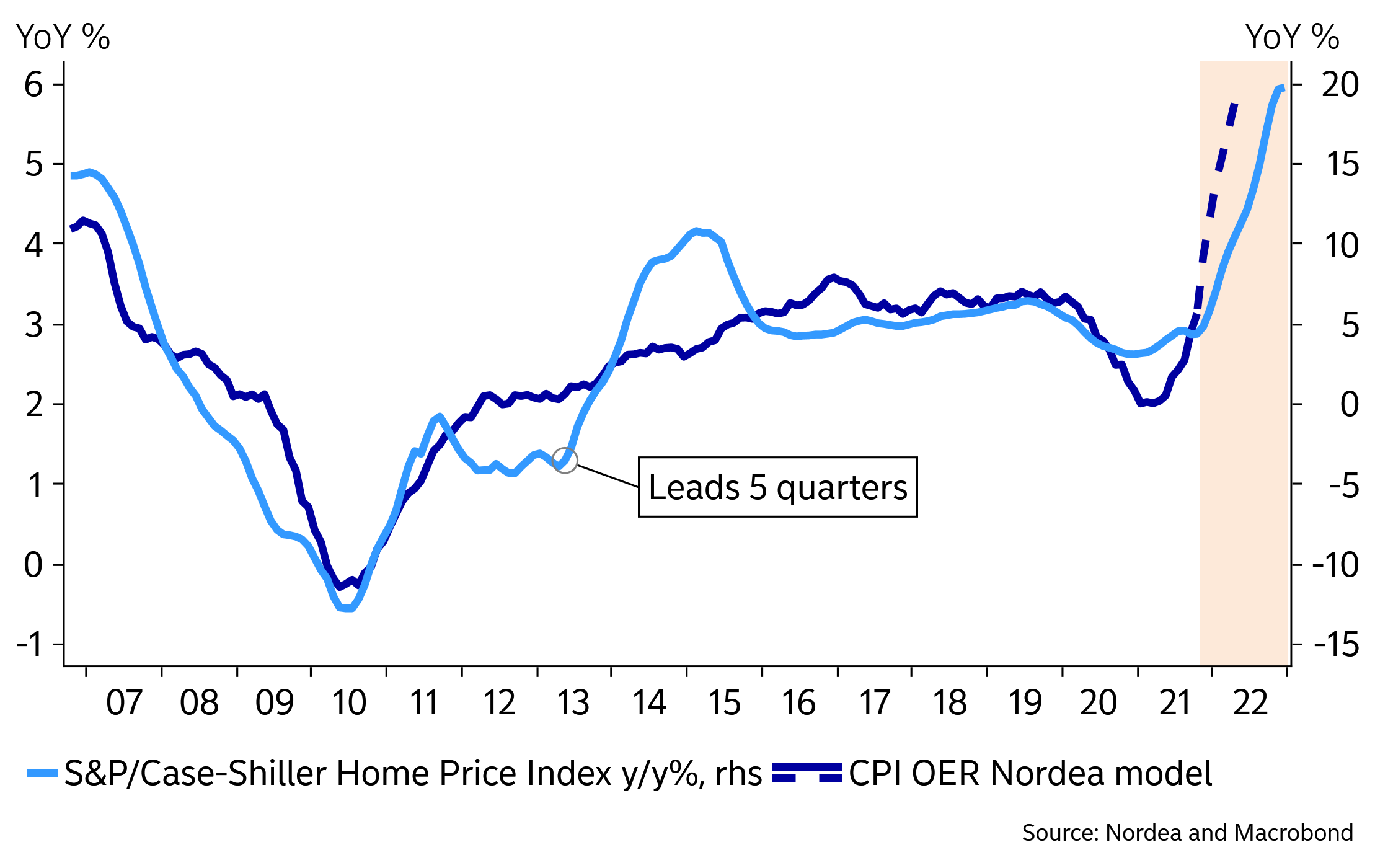

While we cannot expect car prices to rise well into 2022, we expect OER – the largest CPI component – to slowly but surely push inflation higher in 2022. Our model is broadly in line with house price forecasts from Fannie Mae and OER inflation projections from Dallas Fed. The main difference is that we see higher risks of front-loaded inflation. According to our models the yearly contribution to core inflation from the OER component could be as large as 1.7%.

Our model hints of 5-6% OER as soon as in 1H 2022

Inflation Pressure Hits New Warehouse Leases Landlords are incorporating higher prices into increasingly expensive contracts, extending the rising costs in supply chains

(…) Prices to lease industrial properties are up an average of 25% over the rates at the end of five-year contracts that expired this year, according to a report real-estate firm CBRE Group Inc. released Monday. (…)

The U.S. national average vacancy rate fell to 3.6% in the third quarter, down from 4.3% the year before, and the lowest level in data going back to 2002, CBRE said in an earlier report. Space is especially tight at key distribution hubs like the Inland Empire in Southern California, where the vacancy rate recently dipped to 0.7%.

CBRE says leasing rates in the third quarter were up 10.4% year-over-year. (…) Rents to replace leases expiring this year in central New Jersey, Philadelphia and the Inland Empire near the ports of Los Angeles and Long Beach were more than 60% higher than rates for leases that started in 2016. (…)

“Transitory” inflation indeed!

- Lumber prices surge amid B.C. flooding, higher U.S. duties Cash prices jumped US$100 last week to US$745 for 1,000 board feet of two-by-fours made from Western spruce, pine and fir, or SPF. With that 15-per-cent gain, the latest rally has resulted in cash prices soaring 75 per cent over the past 13 weeks.

Hopefully transitory:

POINTS OF VIEWS

- Morgan Stanley: “We reiterate our view that tapering is tightening for the markets and it will lead to lower valuations like it always does at this stage of any recovery. How much lower? We forecast S&P 500 forward P/Es to fall to 18x, or approximately 12% below current levels. Obviously, for the more expensive parts of the market, that decline will be larger.”

- Goldman Sachs: “Investors have drawn parallels between recent equity volatility and 4Q 2018 when the S&P 500 plunged nearly 20%. However, by several measures, the present looks more favorable for equities than three years ago. The annualized pace of US economic growth is nearly double what it was in 2018 (3.0% vs. 6.5%), the nominal Treasury yield is much lower (1.4% vs. 3%), while core PCE is higher (4% vs 2%). The relative value of equities vs. bonds is compelling (32nd %-ile vs. history)”.

The current forward P/E is 21.1x ($216 FW EPS). Core CPI is 4.6%. The Rule of 20 says Fair P/E is 15.4 and Fair Value 3050. Sounds exaggerated? It also did in 2000.

Investors currently don’t care about inflation. Assume they are right and inflation quickly returns to the Fed’s 2% goal. The R20 Fair P/E would then be 18 and Fair Value somewhere between 3600 and 3900.

On Goldman’s assertion that “by several measures, the present looks more favorable for equities than three years ago”, I would respectfully mention that the S&P 500 Index was trading at 19x in September 2018 (now 23.0) and the R20 P/E was 21.2 (now 27.6). Equities troughed in December 2018 at a P/E of 14.6 and a R20 P/E of 16.8. Inflation was stable at 2.2% then. Trailing EPS jumped 8% during those 3 months.

Some people seem to care about something:

Meanwhile, watch the moving averages:

China Evergrande’s Managed Restructuring Is Under Way; Shares Hit 11-Year Low The developer’s bonds also fell to historic lows, after Chinese authorities stepped up their involvement in its affairs and the company moved closer to a reorganization of its hefty international debt.

(…) Evergrande said Monday that “in view of the operations and financial challenges” it is facing, its board has set up a risk-management committee whose members include representatives from several state-owned enterprises. (…)

The containment process has begun…

As of end-June, Evergrande had total debts of the equivalent of roughly $89 billion, out of a broader set of liabilities topping more than $300 billion. Most of its debt is onshore but it has nearly $20 billion in offshore bonds.

- China Moves to Boost Slowing Economy China’s central bank said it would reduce the amount of money banks are required to set aside as it moved to stimulate a slowing economy that has been weighed down by a slump in the property market.

(…) On Monday, the People’s Bank of China said it would reduce the reserve requirement ratio for banks by 0.5 percentage point to 8.4%, starting Dec. 15, which would unleash about 1.2 trillion yuan, or $188.3 billion, into the financial system. It was the second such move this year after an earlier one in July.

Separately on Monday, the Communist Party’s top decision-making body said that stability is the “top priority” for China’s economy next year, signaling that Beijing will shift toward supporting growth in 2022. (…)

From Markit’s November PMI: “At the composite level, new order growth slowed to a fractional pace that was the slowest for three months.”

- China Increasingly Obscures True State of Its Economy New data restrictions have made it harder for foreigners to get details on what’s happening inside China, including about port activity, supplies and political dissent cases. Companies and governments are left trying to figure out how to engage.

(…) One driving force behind the expanding secrecy is a new data-security law that went into effect on Sept. 1, after Chinese officials grew concerned about the transfer of potentially sensitive data overseas. It subjects almost all data-related activities to government oversight, including their collection, storage, use and transmission.

Since the law was passed, companies in mainland China have grown more reluctant to share information with multinationals in strategic sectors like finance, healthcare, public transportation and infrastructure, according to Jonathan Crompton, a Hong Kong-based lawyer at the law firm Reynolds Porter Chamberlain LLP. (…)

Suppliers of metals like cobalt and lithium used in electronics have grown reluctant to share information with customers outside China, said one executive at a major U.S. technology company. Data the suppliers now consider sensitive includes details like how much of a given metal they have available or what percentage of their supplies are recycled, the person said, making it difficult to plan production and ensure compliance with environmental rules. (…)

In early November, global ship-tracking platforms began to notice disruptions to the flow of location data of vessels in Chinese waters. Some local providers had stopped sharing detailed information of ship positions, citing the new data-security law. A Chinese state media report on Nov. 1 described a nationwide crackdown on local providers of such data, citing national security implications.

While satellite imagery is still available, removing access to more detailed, real-time vessel movements around China makes it difficult for companies to accurately track their shipments to and from the world’s largest exporting nation, said Nikos Psaltopoulos, chief operations officer at Athens-based global maritime analytics company MarineTraffic. It also hinders the ability of financial institutions to gather information on port activity to make accurate macroeconomic predictions on growth and trade, he said. (…)

One of the most dramatic reversals in Beijing’s openness has been in academia—once seen as a beacon of engagement between China and the West. China has steadily closed off Western scholars’ access to research archives and made it more difficult for Chinese universities to host international conferences. (…)

Russia and Ukraine: War or Bluff? By: George Friedman “My bet is this is a bluff. But I wouldn’t bet the house on it.”

Short of buzz!

Source: YCharts

Axios’ Sara Fischer and Felix Salmon write:

At 10:15 on Monday morning, BuzzFeed was worth $1.93 billion. Less than one hour later, at 11:11am, the company had shed 43% of its value and was worth just $1.1 billion.

At the end of its first day as a public company, the market had settled on a valuation of $1.15 billion — for BuzzFeed and HuffPost and Complex. That compares to a valuation of $1.7 billion for BuzzFeed alone when it raised $200 million from NBCU in 2016.

When it started trading after merging with a SPAC named 890 Fifth Avenue, BuzzFeed had just 1.6 million shares trading on the Nasdaq exchange. That’s because 94% of the SPAC’s shareholders had opted to redeem their shares for $10 each, rather than hoping BuzzFeed stock would trade higher than that.