MANUFACTURING PMIs

Eurozone: Manufacturing orders fall for first time in almost two years as inflationary surge continues

Eurozone manufacturing fragility was once again clear in the latest PMI® survey for May as manufacturing new orders fell for the first time since June 2020. Although output growth picked up marginally from April’s recent low, it remained sluggish, while business confidence was among the lowest seen over the past two years amid sustained concerns surrounding the outlook for prices, supply chains and demand.

Prices data signalled still-substantial inflationary pressures in May despite rates of increase in both input costs and output charges easing slightly. Meanwhile, there were also signs, albeit limited, of some supply disruptions easing as delivery times lengthened to the second-weakest extent since the beginning of 2021.

The S&P Global Eurozone Manufacturing PMI® fell to 54.6 in May, down from 55.5 in April and signalling a weaker improvement in the health of the euro area manufacturing sector. Overall, the headline index fell to its lowest mark for 18 months. By sub-sector, latest data showed weaker upturns across each of the three monitored market groups.

The strongest-growing euro area constituent in May was once again the Netherlands, although the expansion here slowed to an 18-month low. Weaker rates of growth were also seen across the next-best performing manufacturing economies in Austria and Ireland. The only monitored nations to record stronger improvements were Germany and Spain.

Eurozone manufacturing output expanded midway through the second quarter. The rate of growth accelerated slightly from April’s recent low, but was nonetheless the second-weakest in 23 months of expansion. Stronger (but still marginal) gains in production came amid tentative signs of receding supply-chain pressure as average input lead times lengthened to a lesser extent than in April. In fact, the deterioration in vendor performance was the second-softest since January 2021.

Moreover, euro area manufacturers added to their stocks of purchases at the quickest pace in three months during May. That said, amid soaring input price inflation and weakening demand, the rate of purchasing activity growth was unchanged from April’s 17-month low.

Latest survey data signalled steep cost pressures across euro area manufacturing firms in May. Although the rate of increase softened, it was among the steepest on record amid widespread reports of surging energy and raw material prices. In a bid to offset margin pressures, surveyed goods producers charged higher prices. Overall, the rate of output price inflation was the second-strongest in the series history, surpassed only by that seen in April.

A consequence of rising selling charges was falling demand during May. New orders placed with euro area manufacturers declined for the first time since June 2020. In addition to price rises, survey respondents also linked weaker demand to the war in Ukraine, supply issues and heightened uncertainty. Furthermore, the decline was broad-based, according to market grouping data, and led by the intermediate goods category. Similarly, new export orders also decreased at the sharpest pace for nearly two years.

Concerns surrounding the outlook for inflation, demand and supply chains anchored business confidence at a relatively subdued level during May. Overall, euro area businesses were optimistic towards the coming 12 months, but the level of positive sentiment was among the weakest seen over the past two years.

China: Manufacturing sector conditions deteriorate at softer pace in May

May survey data signalled a move towards more stable operating conditions across China’s manufacturing sector, as firms signalled notably softer falls in both production and new orders. Firms also registered a slower reduction in purchasing activity, though supply chain delays remained severe overall. Prices data meanwhile showed that the rate of input price inflation moderated but remained strong, but efforts to attract new business led to a renewed fall in selling prices.

Companies were more cautious around the 12-month outlook for output in May, with overall optimism slipping to a five-month low amid concerns over the longevity of COVID-19 restrictions and the war in Ukraine.

At 48.1 in May, the headline seasonally adjusted Purchasing Managers’ Index™ (PMI™) rose from a 26-month low of 46.0 in April and signalled a third successive monthly deterioration in business conditions. That said, the rate of decline was modest overall.

Helping to move the headline index upwards was a softer reduction in production during May. The rate of contraction eased notably compared to that seen in April, though was nonetheless the second-sharpest recorded since February 2020. Where lower output was reported, firms often attributed this to the ongoing pandemic and subsequent restrictions that had disrupted operations and logistics.

Total new orders fell for the third month running, albeit at a reduced rate. Notably, the latest drop in sales was the slowest seen over this period and only mild, with some firms noting a relative improvement in demand conditions since April. Underlying data indicated that weaker foreign demand was a key factor weighing on new business, as export orders continued to fall markedly, which some firms linked to difficulties in shipping items to clients.

Average suppliers’ delivery times meanwhile continued to lengthen sharply in May, though delays were not as widespread as those seen in April. Panellists frequently mentioned that COVID-19 restrictions had weighed heavily on logistics and transport.

In line with the trend seen for output, purchasing activity fell at a slower, but still marked, rate in May. At the same time, inventories of both finished goods and purchased items fell at mild rates as firms looked to streamline stocks amid relatively muted demand conditions.

Lower production requirements and staff resignations meanwhile led to a further drop in employment across China’s manufacturing sector. Disruptions to operations due to measures to contain the COVID-19 virus meanwhile led to a further increase in backlogs of work.

The rate of input cost inflation moderated for the second month in a row in May, but remained sharp overall. Firms often mentioned that expenses had risen due to higher costs for raw materials, transport and fuel. At the same time, selling prices fell for the first time in five months amid efforts to stimulate client demand. Though modest, the rate of discounting was the quickest seen since April 2020.

Business confidence regarding the 12-month outlook for production slipped to its lowest for five months in May. While many firms were confident of a strong post-pandemic recovery, others cited concerns over the time it will take to contain the virus as well as the Ukraine war.

Japan: Manufacturing conditions improve at softest pace for three months

Japanese manufacturers indicated that operating conditions improved at a solid, albeit softer rate in May. Both output and new orders rose at slower rates midway through the second quarter, with rates of growth easing to the weakest in the respective three- and eight-month sequences of expansion. The slowdown in demand was coupled with reports of increased supply chain pressures, as delivery delays and material shortages added further upward pressure on costs. Manufacturers signalled that input prices had risen at the quickest rate for nearly 14 years, and the fourth-sharpest pace in the survey history. Firms also noted that sustained disruption had encouraged them to boost safety stocks, with holdings of raw materials increasing at the second-strongest rate since the series began.

The headline au Jibun Bank Japan Manufacturing Purchasing Managers’ Index™ (PMI) dipped slightly from 53.5 in April to 53.3 in May, signalling a solid albeit softer improvement in the health of the sector. Moreover, the increase marked the softest improvement in manufacturing conditions since February.

Latest data pointed to a mild expansion in output. While growth was recorded for the third month in a row, the rate of increase was the slowest in this sequence. Higher production levels were often associated with rising new orders, although some firms noted that higher prices and material shortages had dampened growth.

Similarly, new orders among Japanese manufacturers rose at slower rate. The pace of expansion was only marginal and the softest recorded in the current eight-month sequence of growth. Higher sales were linked to improved client confidence domestically, while the rise in COVID-19 cases in China in particular had dampened international sales. As such, new export orders declined for the third successive month and at the sharpest pace since July 2020.

Japanese goods producers indicated a further rise in purchasing activity in May, the eighth in as many months. The rate of growth eased from that seen in April amid difficulties sourcing and receiving inputs amid delivery delays and material shortages. In fact, average lead times lengthened at the joint-strongest rate for seven months. In an effort to protect against delays, manufacturers sought to build safety stocks, with inventories of raw materials and semi-finished goods rising at the second-fastest pace on record.

May data signalled further rises in average cost burdens among Japanese manufacturers. The rate of input price inflation was substantial and the fourth-quickest in the survey history. Firms continued to partially pass on costs to clients to protect margins, as output prices rose at a further marked rate. That said, the rate of inflation slowed for the first time in three months.

There were indications of greater pressure on production capacity during May, as the rate of backlog accumulation accelerated to the strongest since April 2021. Japanese manufacturers looked to increase capacity in response. Workforce numbers were raised for the fourteenth month running, with the rate of job creation quickening from the previous survey period.

Looking ahead, business optimism at Japanese manufacturers strengthened midway through the second quarter as firms continued to forecast a rise in output in the coming year. Manufacturers predicted that the impacts of the pandemic and Russia-Ukraine war would dissipate and drive a strong recovery in demand and supply chains.

EMPLOYMENT WATCH

Before Friday’s Non-Farm Payrolls release:

- State of the Labor Market (Indeed)

(…) new job postings have fallen from their series high earlier this year of 90.3% above pre-pandemic baseline. But at 73.9%, new job postings growth is still above any point between February 2020 and December 2021. This moderation indicates employer demand is slowing from its extraordinary peak but remains strong.

Total Job Postings on Indeed

% change in job postings since Feb 1, 2020, seasonally adjusted, to May

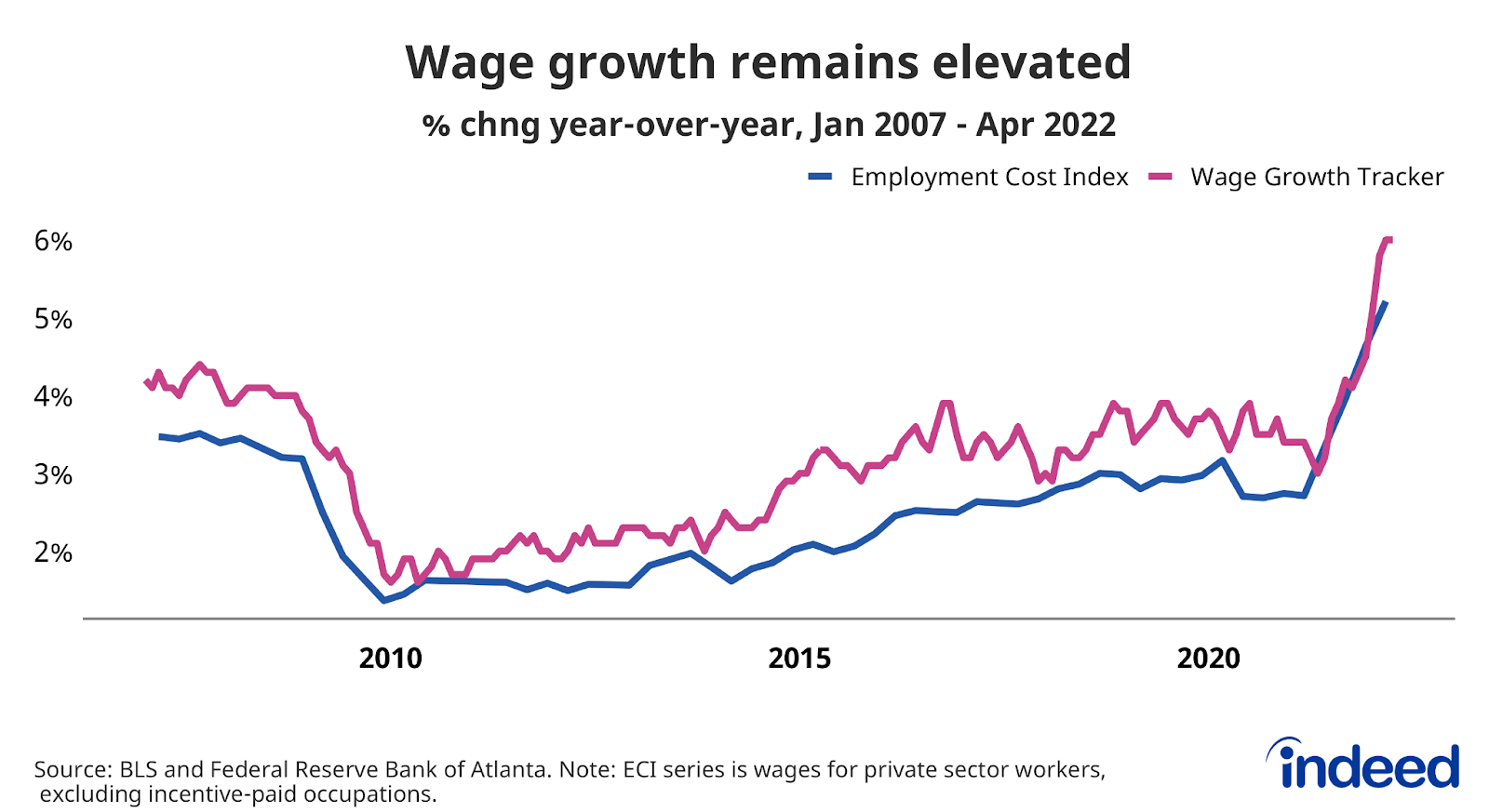

20, 2022 (Canada, USA)Strong demand for workers combined with acute hiring difficulties across multiple sectors have driven wages up roughly 6% on an annual basis, a higher growth rate than at any point in over the past 20 years.

- Small Business Jobs Index (Paychex)

The national index slowed 0.27 percent in May, the largest one-month decrease since the onset of the COVID-19 pandemic more than two years ago. The pace of small business growth has slowed at an increasing rate each month since January 2022.

Hourly earnings growth increased for the 12th consecutive month, from 2.72 percent in May 2021 to 5.19 percent in May 2022. One-month and three-month annualized growth also set new highs, 7.00 percent and 5.53 percent, respectively.

Threat of summer of strikes as UK pay divide widens

Total pay in the UK private sector, including bonuses, rose by 11.7% in the twelve months to March, easily outstripping the 7% increase in the cost of living recorded in the consumer price index. Empirically, we find that changes in bonuses help predict future changes in regular pay: regular pay growth is likely to rise from here, in the private sector at least.

Just as striking, perhaps, is the disparity between rates of pay growth in the private and public sectors. Total UK public sector pay rose by just 1.6% in the twelve months to March, with the gap between the rate of increase in private and public sector pay the largest on record. With the UK labour market already very tight, this gap between private and public sector pay growth is unsustainable. Unless it begins to close, and soon, an increase in industrial action, which often takes places during periods of high inflation, seems very likely.

CONSUMER WATCH

BIG is soft

Big Lots reported worse-than-expected Q1’22 results with a net loss of $0.39 compared to estimate of +$0.93. Sales slowed materially in April. From the call:

- markdowns will hurt margins in Q2, as inventories get right-sized and BIG offers more attractive opening prices. Q2 margins in “low-30’s vs 36.7% in Q1.

- the sales miss was largely in discretionary categories, consistent with recent commentary from other discount retailers

- management noted attractive merchandise buying opportunities across home, apparel, and shoes.

Survey says:

MS’ US Equity Strategy Team recently ran a survey of ~2,000 US Consumers with MS’ AlphaWise Team. More than 50% of consumers are planning to cut back on spending over the next six months due to inflation and an even higher share of lower income consumers are expecting to reduce spending. The majority of these spending cuts are expected to come from highly discretionary categories including dining out and footwear / apparel.

Morgan Stanley via The Market Ear

French Consumer Spending Down Further in April

French consumer spending on goods declined further in April (-0.4%mom in real terms), well below expectations, and the March print was revised down. This is the fifth consecutive month of declines in consumer spending, consistent with a 12pt loss in consumer confidence from January to May, driven by expectations of a weaker financial situation and rising unemployment over the next 12 months.

Over the first quarter, consumer spending on goods declined by 2.2%, consistent with a reduction in private consumption in Q1 of 1.5%qoq.

The April print was essentially driven by a strong decline in manufactured goods consumption (-0.7%mom), which was depressed by food products consumption (-1.1%mom) and consumer spending on durable goods (-0.7%mom). (GS)

Last 2 months: -11.0% a.r.!!!

Missed Payments, Rising Interest Rates Put ‘Buy Now, Pay Later’ to the Test Affirm, Afterpay and Klarna grew rapidly during the consumer-spending boom, but rising delinquencies and a slowing economy are clouding that outlook of some investors.

(…) But late payments or related losses are piling up for the industry’s biggest players— Affirm Holdings Inc., Afterpay and Zip Co. ZIP -8.74% Their borrowing costs, meanwhile, are rising. Buy-now-pay-later companies sometimes rely on credit lines whose rates rise and fall along with the Federal Reserve’s benchmark rate, which has risen 0.75 percentage point so far this year and is poised to go up even more. (…)

Klarna last week said it plans to lay off about 10% of its staff. It also has tightened lending standards “to reflect this evolving market context,” a spokeswoman said. (…)

Subprime consumers accounted for about 43% of shoppers who applied for payment plans or loans at retailers’ checkout between the fourth quarter of 2019 and 2021, according to credit-reporting firm TransUnion, though they only made up about 15% of the U.S. adult population. (…)

At Affirm, about 3.7% of outstanding loan dollars held on the company’s balance sheet were at least 30 days late at the end of March, up from 1.4% a year earlier. (…)

Afterpay’s losses equaled 1.17% of total payment dollars processed during its latest quarter, compared with 0.9% for its latest full year ended June 2021. Zip said its “bad debts and expected credit losses” surged 403% in the last six months of 2021 compared with the same period a year prior. Zip said the increase was in part due to companies it acquired in 2021. (…)

Affirm’s most recent securitization in April priced at a weighted average yield of 4.61%, roughly 3.3 percentage points more than its February 2021 securitization, according to Finsight. (…)

EARNINGS WATCH

Earnings revisions breadth continues fading… (The Market Ear)

Zombie Firms Face Slow Death in US as Era of Easy Credit Ends

(…) From meme-stock favorite AMC Entertainment Holdings Inc. to household names such as American Airlines Group Inc. and Carnival Corp., their ranks have swelled in recent years, comprising roughly a fifth of the country’s 3,000 largest publicly-traded companies and accounting for about $900 billion of debt. (…)

Of course, there have been any number of moments over the past decade when zombie firms have appeared on the cusp of a reckoning, only for markets to be tossed a last-minute lifeline. But industry watchers note that what makes this time different is the presence of rampant inflation, which will limit the ability of policy makers to ride to the rescue at the 11th hour. (…)

Junk-rated companies, those ranked below BBB- by S&P Global Ratings and Baa3 by Moody’s Investors Service, have borrowed just $56 billion in the bond market this year, a more than 75% decline from a year ago.

In fact, issuance in May of just $2.2 billion is set to be the slowest for the month in data going back to 2002.

“If rates had not been so low, many of them would have gone under” already, said Viral Acharya, a professor at New York University’s Stern School of Business and former deputy governor of the Reserve Bank of India. “Unless we have another full-blown financial crisis, I don’t think the Fed’s capacity to bail out is necessarily that high. Especially when they are explicitly saying they want to reduce demand. How is that consistent with keeping these firms alive?” (…)

Cruise-ship operator Carnival sold $1 billion of eight-year notes that yield 10.5% earlier this month, a stark contrast to the $2 billion it was able to raise just seven months prior at a rate of 6%. (…)

Of the 50 largest zombies by outstanding debt, half reported lower operating margins in their latest results, data compiled by Bloomberg show. (…)

Roughly 620 companies didn’t earn enough to meet their interest payments over the past year, down from 695 12 months prior, but still well above pre-pandemic levels. [455 on average between 2015 and 2019 when there were 478]

{kind=link}