Bank of England tells banks to cut rainy-day fund to boost lending

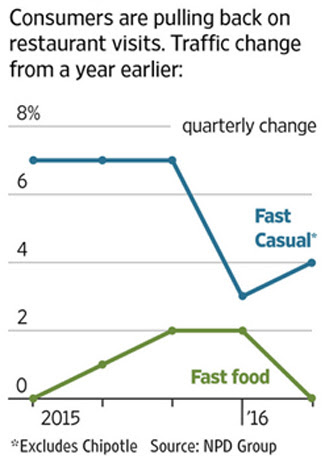

U.S. Light Vehicle Sales Ease

Total sales of light vehicles during June declined 4.5% versus May (-2.0% y/y) to 16.66 million units (SAAR), the lowest level in three months.

Auto sales fell 5.0% to 6.76 million units (-11.2% y/y). The decline reflected a 4.1% fall (-10.1% y/y) in domestic car sales to 4.95 million units. Imported car sales declined 7.3% to 1.81 million (-14.0% y/y).

Sales of light trucks declined 4.2% to 9.90 million units (+5.5% y/y). Sales of imported light trucks fell 6.9% to 1.66 million units (+22 .7% y/y). Domestic light truck sales declined 3.6% to 8.24 million units (+2.6% y/y). Truck sales edged up to 59.4% of the light vehicle market.

Imports share of the light vehicle market of 20.8% compared to 19.8% during all of last year. Imports share of the passenger car market of 26.7% compared to 27.1% during all of last year. Imports share of the light truck market eased to 16.8%.

And this from Toni Sagami:

A Midyear Burst of Minimum-Wage Increases Starts on July 1

On July 1, 14 U.S. cities, states and counties, plus the District of Columbia, will raise their minimum wage in a mid-year burst that reflects the legislative momentum to boost pay floors across the country while federal legislation stalls.

In total, the minimum wage will rise in 15 places: two states – Maryland and Oregon, plus Washington, D.C., Los Angeles County, Calif., and 11 cities. That includes Chicago, eight cities in California and two in Kentucky, according to a new analysis by the right-leaning Employment Policies Institute.

A newer twist is that the boosts are reaching higher overall levels than in the past. While the federal minimum wage has been $7.25 an hour since 2009, cities and states are embracing increases that go as high as $15 an hour.

San Francisco’s minimum wage, which will rise to $13.00 Friday from $12.25, is set to reach $15 by 2018. Chicago’s minimum, which will jump to $10.50 an hour Friday from $10.00, is set to reach $13 by 2019.

The mayor of the nation’s capital this week signed legislation that will raise the minimum wage there to $15 by 2020. And the states of New York and California approved eventual $15 levels earlier this year.

Weak Global PMI rounds off worst quarter for three years

Global manufacturing remained mired in near-stagnation in June, recording one of the weakest expansions seen since late-2012, a time when the world was struggling in the face of the escalating eurozone debt crisis.

The JPMorgan Global PMI, compiled by Markit from its worldwide business surveys, rose from 50.0 in May to 50.4 in June, but as such only indicated a marginal improvement in business conditions.

The PMI has been signalling a near-stagnant global manufacturing economy over the past year, with signs of the trend worsening rather than improving in recent months. Over the second quarter as a whole the rate of expansion slipped slightly lower to the weakest for three years.

Other survey indices showed broadly no change in global exports and employment, as well as ongoing inventory reduction. New orders rose at a slightly faster rate, driving the first (albeit marginal) increase in backlogs of work since last October.

(…) In both the UK and Eurozone as a whole, growth remained sluggish, however, and companies often reported that worries about the outlook had increased in the lead up to the UK vote, suggesting the decision by the UK to leave the EU could cause a pull-back in business activity in the UK especially in coming months.

Growth also picked up in the US, but likewise remained worryingly weak, suggesting US factories remained stuck in one of their weakest phases since the global financial crisis, with the second quarter average of the PMI at its lowest since the third quarter of 2009.

The expansions seen in the US and Europe contrasted with an ongoing downturn in manufacturing activity across Asia. Asia’s factories reported a deterioration in business conditions for the sixteenth successive month, with the rate of decline unchanged in June. The weak PMI rounded off the worst quarter for Asian manufacturers since the third quarter of last year, and the second-worst since the third quarter of 2012.

Japan’s manufacturing sector was among the worst performing in Asia (behind Turkey, where the PMI signalled the steepest downturn since April 2009, and Malaysia). Faced with a strong yen and ongoing supply chain disruptions resulting from recent earthquakes, Japanese manufacturers reported a fourth successive monthly export-led decline in manufacturing activity, according to the Nikkei PMI. Exports were falling at the fastest rates for three years over the second quarter.

Asia ex-Japan also remained in decline, with the rate of contraction accelerating marginally in June, dragged down by the Caixin PMI recording the steepest deterioration in China since February.

Other Nikkei PMIs showed varying trends across Asia: Malaysia saw one of the steepest downturns seen in recent years, but growth accelerated in India, Indonesia and South Korea, while Taiwan saw a return to modest growth after two months of decline. However, in all cases growth rates were modest at best, leaving Vietnam as the strongest growing Asian manufacturing economy for the third month in a row.

In all, only six of the 24 countries for which June manufacturing PMIs are available reported a downturn (Canada PMI data are published on July 4th). The steepest decline was again seen in Brazil where, although the rate of contraction eased, the survey continued to signal one of the steepest downturns ever recorded.

Something very worrying seems to be happening in China’s jobs market

(…) Guidepoint, a firm that analyzes big data across various industries, recently released a report on China job postings.

The firm found that since early 2013, the spikes and drops in new job postings from property agencies have preceded a similar pattern in the overall housing market by about six months.

The number of new job postings from property agencies now seems to be topping out, according to the research, suggesting a drop in property prices could be on the way.

“If this continues, the recent topping off of new job posting growth would signal that the housing prices across China may be ready to turn yet again,” said Erik Haines, who leads the data and analytics team at Guidepoint.

The homebuilding industry shows a similar trend, which again points to the likelihood of a price drop and fewer construction jobs to fill. (…)

That could have some dark consequences. By the IMF’s calculations, residential investment made up 15% of fixed-asset investment and 15% of total urban employment in China in 2015. With about 911 million working-age people, that means more than 136 million jobs may be at risk.

Let’s not forget that China’s labor market is the No. 1 concern for the country’s leadership.

And here’s the employment picture in manufacturing courtesy of Markit:

Hmmm..But what about China’s structural transition away from manufacturing? From CEBM Research:

In an effort to increase transparency on the structural changes underway in China’s economy, the Mastercard Caixin -BBD China New Economy Index (NEI) was established. (…)

The NEI, published monthly, uses big data analysis to track changes in contribution to overall economic activity in nine sectors of China’s New Economy including 1) Energy Conservation & Environmental Protection, 2) New IT & Information Services, 3) Biotech, 4) Advanced Equipment Manufacturing, 5) Renewable Energy, 6) Advanced Materials, 7) New Energy Vehicles, 8) High-tech Services/Research and Development, and 9) Financial & Legal Services. In addition to providing a high level view of ongoing structural changes in the balance between the Old Economy and New Economy, the NEI dives deeper into the capital, labor and technological inputs driving change across the New Economy and within new economy sectors and industries.

(…) From August 2015 to June 2016, New Economy labor demand increased steadily from 5.4 million to 11.5 million (Chart 7), although there were short-term drawdowns after Chinese New Year and also in April and May. The New Economy’s share of total demand for labor increased slightly, rising from 26.8% in August 2015 to 27.6% in April 2016.

Big ship to steer!

PBOC Says Don’t Underestimate Risks to China’s Economy

China’s central bank said it’s closely monitoring domestic and external risks to the economy and that the complexity of the situation shouldn’t be underestimated.

The People’s Bank of China cited market volatility spurred by the U.K.’s decision to leave the European Union, according to a statement released late Monday after a quarterly monetary policy committee meeting. Domestic economic and financial performance remains stable overall, the advisory panel led by PBOC Governor Zhou Xiaochuan said.

The central bank, which has kept its main interest rate at a record low since October, was more upbeat on the U.S. economy, which it said is “recovering moderately.” The PBOC repeated that risks in global financial markets have risen and that it will maintain prudent monetary policy and keep the yuan stable at a reasonable level. (…)

Renzi ready to defy Brussels and bail out Italy’s troubled banks Regulators fear intervention would dent credibility of union’s new rule book

Matteo Renzi, the Italian prime minister, is determined to intervene with public funds if necessary despite warnings from Brussels and Berlin over the need to respect rules that make creditors rather than taxpayers fund bank rescues, according to several officials and bankers familiar with their plans.

The threat has raised alarm among Europe’s regulators, who fear such a brazen intervention would devastate the credibility of the union’s newly implemented banking rule book during its first real test. In the race to find workable solutions, Margrethe Vestager, the EU’s competition chief, has laid out options for Rome to address its banking problems without breaking the bail-in principles of Europe’s banking union.

Italy is the eurozone’s biggest vulnerability following the shock outcome of the UK vote to leave the EU, with bank stocks plunging by a third. Concerns are building before the outcome of bank stress test results due this month and a constitutional referendum in Italy in early October, on which Mr Renzi has wagered his job. Citi has described the referendum as “probably the single biggest risk on the European political landscape this year outside the UK”. (…)

From Moody’s:

At the beginning of last week, Italian media outlets, including the newspaper II Sole, reported that the Italian government was contemplating measures to shield Italian banks from market turmoil arising from the consequences of the UK vote on 23 June to leave the EU. This plan was reported to take the form of a €40 billion capital injection to bolster bank balance sheets – a move that we said would be positive, despite considerable obstacles, including obtaining the EC’s approval.

In its statement Friday, the EC made clear that the liquidity support it had authorized was an entirely separate matter to any potential capital injection. This confirms our view that notwithstanding the clear signal from the Italian government that it is willing to support its banks, EU governments face considerable constraints in providing banks with public capital without first triggering a bail-in of creditors.

EARNINGS WATCH

Factset weekly summary:

In terms of estimate revisions for companies in the S&P 500, analysts have made smaller cuts than average to earnings estimates for Q2 2016. On a per-share basis, estimated earnings for the second quarter have fallen by 2.6%. This percentage decline is smaller than the trailing 5-year average (-4.4%) and trailing 10-year average (-5.5%) for a quarter.

As a result of the downward revisions to earnings estimates, the estimated year-over-year earnings decline for Q2 2016 is -5.3% today, which is larger than the expected earnings decline of -2.8% at the start of the quarter (March 31). Four sectors are predicted to report year-over-year earnings growth, led by the Telecom Services and Consumer Discretionary sectors. Six sectors are projected to report a year-over-year decline in earnings, led by the Energy, Materials, and Information Technology sectors.

If the Energy sector is excluded, the estimated earnings decline for the S&P 500 would improve to -1.8% from -5.3%.

As a result of downward revisions to sales estimates, the estimated sales decline for Q2 2016 is -0.8%, which is larger than the estimated sales decline of -0.5% at the start of the quarter. Six sectors are projected to report year-over- year growth in revenues, led by the Telecom Services and Health Care sectors. Four sectors are predicted to report a year-over-year decline in revenues, led by the Energy and Materials sectors.

If the Energy sector is excluded, the estimated revenue decline for the S&P 500 would improve to 2.2% from -0.8%.

In addition, a slightly smaller percentage of S&P 500 companies have lowered the bar for earnings for Q2 2016 relative to recent averages. Of the 113 companies that have issued EPS guidance for the first quarter, 81 have issued negative EPS guidance and 32 have issued positive EPS guidance. The percentage of companies issuing negative EPS guidance is 72%, which is slightly below the 5-year average of 74%.

As we know, the various aggregators each have their own way. Thomson Reuters’ tally is more positive than Factset’s in both actual EPS and pre-announcements. TR says that 14 more companies have positively pre-announced Q2, up appreciably from 23 last year and 26 in Q1’16.

TR does not provide an industry breakdown but Factset’s data suggest that IT, Health Care and Industrials are providing most of the additional positive pre-announcements vs last year and vs Q1’16.

TR calculates that Q2 EPS will decline 4.0% YoY vs –3.8% 2 weeks ago. Given the better pre-announcements, Q2 results could surprise more than usual…

…even though the economy fails to surprise anybody, except on the downside:

Brexit fears now fading away, the S&P 500 Index is back hitting the 2100 wall, even though transportation stocks keep sliding. Ed Yardeni constructs an Index of the S&P 500 excluding Financials, Transports and Utilities and tracks this index with the Transportation Composite. The last time these two normally well synched indices diverged meaningfully was in 2015. It took the 13% August correction in the SPX to reconnect them again but they have been diverging again since.

Meanwhile, the Rule of 20 P/E is back above 20 at 20.1 with no backwind from earnings and pretty stable inflation. Until earnings start rising again, only a strong lift in sentiment can boost equities. Very difficult to se this coming from the economy, China and politics. Can our central bankers do their trick again? I am not betting on that.

Wall Street Strategists Are Subdued on Stocks

(…) Eighteen equity strategists tracked by research firm Birinyi Associates expect the S&P 500 to finish the year at roughly 2150. That forecast is down from a forecast of 2200 at the beginning of the year. It closed Friday at 2103.

Perhaps more surprising is the level of caution among these prognosticators, usually an optimistic bunch. Seven of those 18 strategists have lowered their year-end targets since the beginning of the year. Many have held their forecasts steady. Goldman Sachs’s David Kostin, one of the more bearish strategists on Wall Street, sees the S&P 500 finishing the year at 2100 and rising slightly to 2125 in 12 months. (…)

Deutsche Bank’s David Bianco turned more cautious last week after the U.K. referendum. He cut his S&P 500 year-end forecast by 50 points to 2150, warning that Brexit will weigh on U.S. earnings in the coming quarters. (…)

Stock Market to Bond Market: ‘La-La-La I Can’t Hear You’

(…) Since the Brexit vote, Treasury yields have tumbled, and they kept falling even as shares recovered. On Friday, 10-year and 30-year yields set new lows, as did British and Japanese benchmarks. Bondholders think central banks will worry about the economic impact of Brexit, keeping rates lower for longer. This is quite different from what happened after Lehman, when bond yields rebounded with shares, as bond investors made the same mistaken judgment that there would be few long-run effects from a midsize U.S. bank failure.

Last week’s divergence of bonds and equities isn’t healthy. Bond markets are screaming that the world economy is slowing, and shareholders have their fingers in their ears singing “la-la-la I can’t hear you.” Stocks are no longer about growth, but about a desperate search for safe alternatives to low-yielding bonds. (…)

Since Brexit, the bond-driven nature of the stock market has been particularly stark. Four sectors in the S&P 500 are now higher than they were on the eve of the British vote, and none are a bet on the American economy’s underlying strengths.

Utilities, consumer staples, health care and telecommunications sell stuff people need even in bad times; this is a defensive rally, not a dash for growth. (…)