Eurozone composite PMI: Service sector resilience helps sustain robust eurozone growth in May, but momentum fades

The eurozone economy continued to expand at a strong rate midway through the second quarter as recently-relaxed COVID-19 restrictions supported a sustained uplift in activity levels. The main driving force behind the latest expansion was once again the eurozone’s dominant service sector as ongoing supply-side disruptions, the war in Ukraine and subdued demand for goods restrained manufacturing output growth.

Despite service sector resilience, there was an overall loss of momentum within the sector in May, leading private sector business output to rise at the slowest pace since January amid fading post-pandemic catch-up effects, growing uncertainty and rapid inflation.

Nevertheless, combined new business intakes across manufacturing and services firms continued to grow in May, while there was further evidence of squeezed capacities as backlogs of work rose once again. Employment growth accelerated to a ten-month high amid a broad-based improvement in hiring trends at the sector level.

With regards to inflation, output charges were raised to the second-greatest extent on record in May amid another substantial increase in firms’ operating costs.

The seasonally adjusted S&P Global Eurozone PMI® Composite Output Index fell to a four-month low of 54.8 in May, down from 55.8 in April. While the headline measure was still indicative of economic growth across the euro area, it also highlighted a loss of momentum. This slowdown was exclusively a result of a softer service sector expansion amid signs that the post-lockdown rebound was losing some strength. Nevertheless, services activity continued to rise at a robust pace and masked clear weakness within the goods-producing sector. Although manufacturing output growth edged slightly higher from April’s 22-month low, it was subdued and below its long-run average.

Of the monitored euro area constituents, Ireland was the fastest-growing economy in May. That said, the expansion here slowed to a four-month low. Slowdowns were more or less broad at a country level during the latest survey period, with Spain the only exception as the rate of growth here was unchanged since April. At the other end of the spectrum, Italy was the worst performer and recorded a modest expansion in private sector output.

Latest survey data pointed to a further increase in new business receipts across the euro area private sector in May. That said, the expansion in demand for goods and services slowed to a four-month low amid a drop in manufacturing new orders and signs that the post-lockdown rebound in services was beginning to fade. Foreign client demand was also a drag on order volumes in May as new export business fell at the fastest pace for nearly two years.

Nevertheless, there was evidence of sustained capacity constraints across the eurozone private sector in May as backlogs of work rose for a fifteenth month in a row. Staffing issues, material shortages and rising new order intakes each contributed to a build-up of outstanding business.

To help work through backlogs and accommodate for anticipated demand, private sector employment across the euro area increased during May. In fact, the rate of job creation accelerated to a ten-month high.

However, business confidence eased slightly and was among the weakest seen since mid-2020. The war in Ukraine, rising prices, supply frictions and a general slowdown in the economy were cited as concerns by surveyed companies.

On the prices front, latest survey data continued to highlight severe inflationary pressures across the euro area. Although the increase in input costs was the slowest for three months, it was faster than anything seen prior to this. Rising wage and energy bills were accompanied by higher raw material and fuel costs, according to firms. To protect margins, prices charged were raised during May. Overall, the rate of output price inflation was the second-steepest on record and surpassed only by that seen in April.

The S&P Global Eurozone PMI Services Business Activity Index posted 56.1 in May. Although this marked a decline from 57.7 in April, it was consistent with euro area services activity rising at a strong rate. Furthermore, it signalled the second-fastest expansion in services output since last September.

New business intakes continued to rise across the service sector in May, supported by a renewed increase in new orders from overseas customers. That said, overall demand for services rose at a slower rate when compared to April.

Nevertheless, capacity pressures intensified, as signalled by a faster rise in backlogs of work. The rate of accumulation in work-in-hand was the fastest for ten months. To boost activity levels, employment was raised to the quickest extent since July 2007.

Meanwhile, there was a further steep rise in operating expenses, leading firms to increase prices for the provision of services across the euro area at a sharp pace. Overall, the rate of output price inflation was the second-fastest on record behind April’s peak.

Strong demand for services helped sustain a robust pace of economic growth in May, suggesting the eurozone is expanding at an underlying rate equivalent to GDP growth of just over 0.5%.

However, risks appear to be skewed to the downside for the coming months. The manufacturing sector remains worryingly constrained by supply shortages and businesses and households alike remain beset by soaring costs. There are also signs that the boost to the economy from pent-up demand for services as pandemic restrictions are relaxed is starting to fade.

Eurozone retail sales show weak start to 2Q Sales decreased by 1.3% in April as weak consumer confidence and high inflation weighed on the economy.

Retail sales data show a bleak start to the quarter. The drop of -1.3% month-on-month was mainly driven by very poor German figures where sales fell by 5.4%. Spain counterbalanced that with a surge in spending of 5.3%, but the overall trend was cautiously down for most eurozone economies. In terms of spending, the decline was seen across the board with both food and non-food products seeing a tick down in spending. Food saw a larger decline though, which comes at a time when food prices have started to surge. (…)

The eurozone consumer is in a rough spot at the moment. With inflation soaring, real incomes are being squeezed massively at the moment. This results in very low consumer confidence at the moment, which is currently at levels usually associated with recession. But, be careful to extrapolate these figures one-for-one to household consumption. A strong surge in post-pandemic services spending seems underway according to the European Commission sentiment survey, which will mitigate the impact of weak retail sales. Nevertheless, it does show that weak survey data is translating into weak hard data for the second quarter, which confirms our view of a seriously slowing or perhaps even contracting economy in the current quarter.

INFLATION WATCH

Consumers are paying more for their everyday goods.

Highlights for the four week period ending May 15:

- Grocery prices were up 13.2% vs. YA, a rate that has steadily increased from around 7-8% at the turn of the year.

- Health & beauty prices were up 10.1% vs. YA. While this is down from inflationary rates seen in late 2021 and early 2022, it is slightly above rates seen earlier in 2021.

- Prices for household items were up 15.8% vs. YA, a rate that is up from prior weeks and from what we saw at the turn of the year.

- Middle income consumers have overtaken low income consumers for the most-impacted group for the first time in May.

US gasoline product supplied You were here vs you are here…

MPAS via The Market Ear

Soaring costs squeeze farmers’ returns in North American grain belt

Eurozone producer prices hit record as inflation spreads beyond energy

Turkish inflation hits 23-year high

South Korean inflation surges by most in almost 14 years

![]()

![]() Earlier this month, a 1955 Mercedes-Benz 300 SLR Uhlenhaut Coupe sold for $142 million in Germany. It was the highest price ever paid for a car at auction. (Bloomberg)

Earlier this month, a 1955 Mercedes-Benz 300 SLR Uhlenhaut Coupe sold for $142 million in Germany. It was the highest price ever paid for a car at auction. (Bloomberg)

Goldman’s Waldron Warns of Unprecedented Economic Shocks, Echoing Dimon

Goldman’s Waldron Warns of Unprecedented Economic Shocks, Echoing Dimon

“This is among — if not the most — complex, dynamic environments I’ve ever seen in my career,” Goldman President John Waldron said at an investor conference Thursday. “The confluence of the number of shocks to the system to me is unprecedented.” (…) “No question we are seeing a tougher capital-markets environment.” (…)

- Global Recession Probability Indicator

Federal Reserve’s Portfolio Runoff Has Begun The central bank is allowing securities to exit from its $8.9 trillion portfolio by not reinvesting the proceeds when they mature.

Bank of Canada’s Beaudry: Policy Rate Might Be Headed Toward 3% or Above The rapid acceleration in prices has increased the likelihood the Bank of Canada may need to double its policy interest rate, from its current 1.5% level to 3% or higher, to drive inflation toward its 2% target, a senior central bank official said Thursday.

EARNINGS WATCH

Microsoft Cuts Forecasts, Citing Dollar Strength Microsoft cut sales and earnings guidance for the quarter ending June 30, blaming the impact of foreign-exchange rates as the stronger U.S. dollar takes a toll.

The company told investors that it now expects foreign-exchange moves to reduce sales by $460 million more than it had previously anticipated in the current quarter. Profit will suffer too, Microsoft warned.

Earnings are expected to be between $2.24 a share and $2.32 a share, down from prior guidance of $2.28 a share to $2.35 a share. (…)

The U.S. Dollar Index, which tracks the currency against a basket of others, is up more than 6% so far this year and hit its highest level since 2002 last month.

A strong dollar allows Americans to buy goods from other countries at lower prices. But it can also hurt U.S. manufacturers by making products more expensive for foreigners, and it means U.S. businesses receive fewer dollars for their exports. (…)

Microsoft said in its April earnings report that a stronger dollar reduced the software company’s revenue and earnings by $302 million and 3 cents a share, respectively.

Microsoft is the latest multinational company to warn of the stronger dollar’s impact on financials. Salesforce Inc. CRM 7.00%▲ earlier this week cited the stronger dollar in lowering its sales outlook for the year. The business-software company doubled the impact that it expects this year from the stronger dollar to $600 million from its $300 million forecast in March. (…)

On Thursday, Microsoft also lowered its gross-margin guidance to a range of $35.45 billion to $36.05 billion, down from between $35.80 billion and $36.40 billion. Operating income is now expected to be between $20.60 billion and $21.30 billion, down from a range of $20.90 billion to $21.60 billion.

(…) The S&P 500 Foreign Revenue Exposure Index has dropped around 17% so far this year, compared with the broad S&P 500 index’s 13% decline. Meanwhile, the S&P 500 U.S. Revenue Exposure Index, which includes companies more dependent on domestic sales, has lost just 7%. (…)

Elon Musk Says Tesla Needs to Cut Staff by 10%: Report The CEO said he had a “super bad feeling” about the economy. Tesla has about 100,000 employees worldwide.

Coinbase to Rescind Employment Offers, Extend Hiring Freeze

![]() Cutting staff amid the “great talent shortage”? Biz must be getting pretty bad…

Cutting staff amid the “great talent shortage”? Biz must be getting pretty bad…

Well, manufacturers’ new orders are weakening while inventories are rising. Something will soon need to give. “The spread between new orders and inventories points to weakness in the ISM PMI later this year.”

Source: @TheTerminal, Bloomberg Finance L.P.

David Rosenberg adds the link between financial conditions and the ISM PMI…

…and then makes the link between the PMI and profits:

TECHNICALS WATCH

From CMG Wealth:

- S&P 500 Large Cap Index – 13/34–Week EMA Trend

- Volume Demand vs. Volume Supply

Source: Ned Davis Research

Tiger Global’s Hedge Fund Lost 52% for the Year Through May The losses have prompted the firm to cut its management fee by 0.5% through December 2023 in both its hedge fund and long-only fund.

(…) Tiger also said that starting in June, it would pay out investors exiting from those funds with both cash and shares in a new side pocket it would create containing stakes in private companies that would be paid out as those investments are realized. (…)

Many hedge funds investing in both public and private companies ramped up their reliance on private bets last year, at what turned out to be the top of the market. The losses have erased years of gains and put a question mark over what had been one of the industry’s top-performing strategies. (…)

But the selloff has exposed vulnerabilities that were glossed over when growth and technology stocks were gaining. Coatue Management LLC earlier this year told clients it would be side-pocketing private investments and paying out redeeming investors only partly with cash.

Tiger’s hedge fund now will collect a 1% management fee, said a person familiar with the firm. The firm has a modified high-water mark in place for its hedge fund, allowing it to collect an incentive fee of 10% on investment gains even if clients haven’t been made whole from broader losses at Tiger. (…)

![]() There are an estimated 2.5 million weddings happening in the US this year, the most since 1984, according to the Wedding Report. (Bloomberg)

There are an estimated 2.5 million weddings happening in the US this year, the most since 1984, according to the Wedding Report. (Bloomberg)

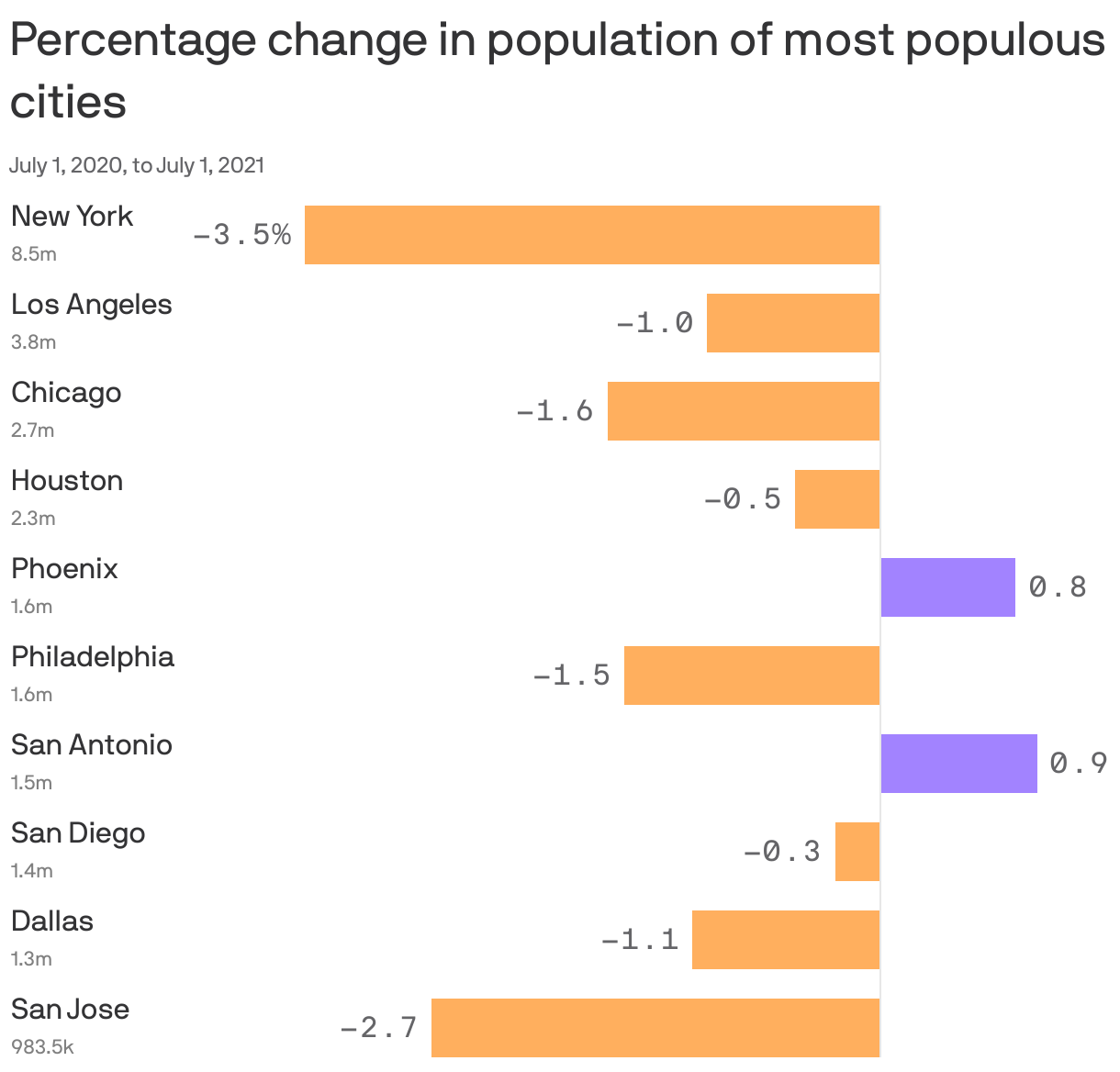

All new households? That would be +2% with consequences on the housing market.