U.S. Leading Economic Indicators Firm

The Conference Board’s Composite Index of Leading Economic Indicators increased 0.6% during April (1.9% y/y), following an unrevised 0.2% March gain. It was the largest increase since June, and beat expectations for a 0.3% rise in the Action Economics Forecast Survey. The three-month change in the index improved to 2.3% (AR). A longer workweek, fewer initial claims for jobless insurance, more building permits, higher stock prices, a steeper interest rate yield curve and the leading credit index had the largest positive effects on the index. Weaker consumer expectations for business & economic conditions had the only negative contribution.

The coincident index increased 0.3% (1.8% y/y) after zero change. April’s gain was the largest monthly in three months. Three-month growth improved to zero (AR) after being slightly negative. Nonfarm payrolls, personal income less transfers, manufacturing & trade sales and industrial production each contributed positively to the index.

The lagging index increased 0.3% (4.1% y/y) after an unrevised 0.4% gain. Three-month growth increased to 6.8%, its strongest in three years. More C&I loans, a longer duration of unemployment and a higher consumer installment debt/personal income ratio contributed positively to the index rise last month.

Chicago Fed National Activity Index Indicates Economic Improvement

The National Activity Index from the Federal Reserve Bank of Chicago increased to 0.10 during April, the first positive reading since January. It still suggested, however, that economic growth was slightly below trend. At -0.22, the three month moving average has been in negative territory since February 2015. During the last ten years, there has been a 77% correlation between the Chicago Fed Index and the q/q change in real GDP.

Each of the component series improved last month. The Production & Income reading moved up sharply to 0.19, the highest point in nine months. The Personal Consumption & Housing figure rose to -0.07, its best level this year. The Employment, Unemployment & Hours figure rose to a still-depressed -0.02. The Sales, Orders & Inventories figure was fairly steady at 0.00. The Fed reported that 45 of the 85 component series made positive contributions to the total while 40 made negative contributions.

Pretty weak heart beat as CalculatedRisk illustrates:

Philly Fed Back Down to Negative Territory

Like its New York sibling, today’s report on manufacturing in the Philadelphia region weakened modestly this month and came in weaker than expected. While economists were expecting a positive reading of 3.0, the actual reading remained sub-zero at -1.8. The headline reading saw a nice bounce in March, but the last two months have seen all of that given back. Even though General Business Conditions showed a modest decline this month, the majority of components actually increased with the biggest jumps coming in Inventories, Number of Employees, and Shipments. On the downside, the only declines were in Delivery Times, Unfilled Orders, and New Orders. (Bespoke)

![]() Note that the prices received measure jumped to the highest level since October 2014.

Note that the prices received measure jumped to the highest level since October 2014.

Two-thirds of U.S. would struggle to cover $1,000 crisis: poll

(…) These financial difficulties span all income levels, according to the poll conducted by The Associated Press-NORC Center for Public Affairs Research. Seventy-five per cent of people in households making less than $50,000 a year would have difficulty coming up with $1,000 to cover an unexpected bill. But when income rose to between $50,000 and $100,000, the difficulty decreased only modestly to 67 per cent.

A third said they would have to borrow from a bank or from friends and family, or put the bill on a credit card. Thirteen per cent would skip paying other bills, and 11 per cent said they would likely not pay the bill at all.

Even for the country’s wealthiest 20 per cent – households making more than $100,000 a year – 38 per cent say they would have at least some difficulty coming up with $1,000. (…)

Despite an absence of savings, two-thirds of Americans said they feel positive about their finances, according to survey data released Wednesday by AP-NORC, a sign that they’re managing day-to-day expenses fine. (…)

The AP-NORC results also correlate with a 2015 study by the Federal Reserve in which 47 per cent of respondents said they either could not cover a $400 emergency expense or would have to sell something or borrow money.

And the struggle affects retirement savings as well. When AP-NORC asked if they will have enough savings to retire when they want to, 54 per cent of working Americans say they are not very or not at all confident they will have enough. Only 14 per cent say they are confident they can retire on time.

AP-NORC release is here.

Doug Short has a post on Five Decades of Middle Class Wages with these 2 charts among many others:

Now let’s multiply the real average hourly earnings by the average hours per week. We thus get a hypothetical number for average weekly earnings of this middle-class cohort, currently at $723 — well below its $830 peak back in the early 1970s.

Scandal-hit VW agrees to 4.8% pay hike for workers

Auto maker Volkswagen and Germany’s industrial union have agreed on wage increases that will see pay rise 4.8 per cent by next year, the kind of deal that could help the 19-country euro zone raise inflation from current dangerously weak levels.

The company said Friday that workers would get 2.8 per cent more on Sept. 1 and then another 2.0 per cent on Aug. 1, 2017. (…)

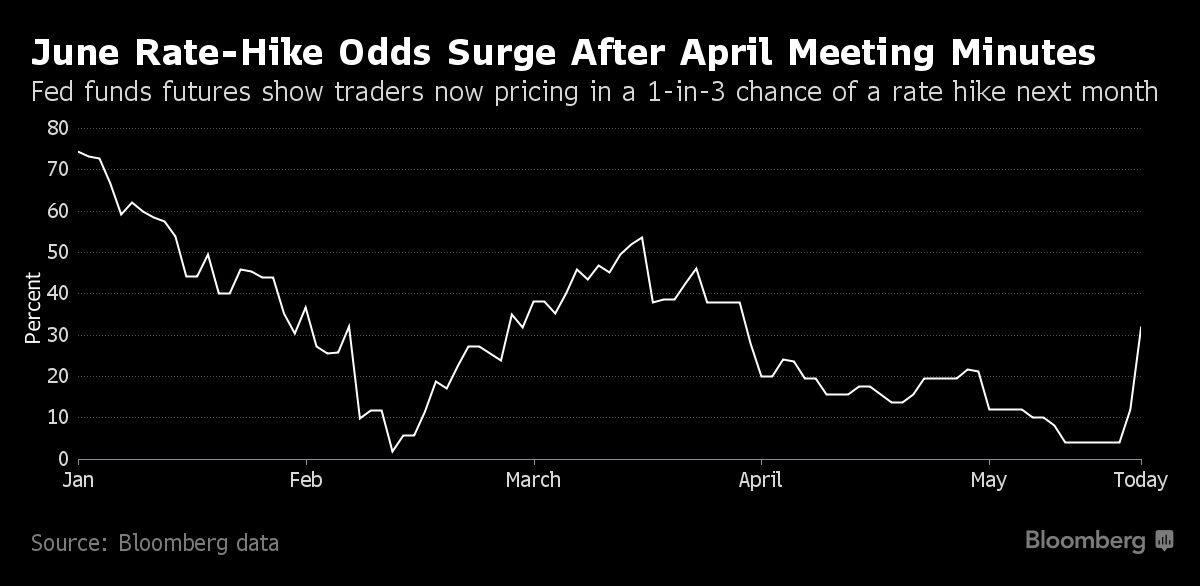

Dudley joins chorus of Fed officials seeing rate hikes soon The U.S. economy could be strong enough to warrant an interest rate increase in June or July, New York Federal Reserve President William Dudley said on Thursday, cementing Wall Street’s view that the Fed will tighten policy soon.

Mish Shedlock takes Dudley to his words in Hikes Data Dependent Says NY Fed: So, Let’s Look at the Data, and concludes like I do:

I do not pretend to know where interest rates should be.

The Fed is even more clueless because they don’t know either, but they believe they do.

So, I am not arguing the Fed should not hike. Rather I present the case the Fed has no idea what the hell they are doing. (…)

The solution is to get rid of the Fed, get rid Davis Bacon and all the prevailing wage laws, and be thankful that innovation lowers costs of living.

Instead, we have to deal with and listen to a bunch of central planning fools prove they have no idea what they are doing with clueless acts to produce inflation then deal with the consequences when they do.

Palos Management’s Hubert Marleau adds this interesting info on the FOMC meetings:

Two Sigma, a large hedge fund, utilizes advanced technological applications using ordinary language processing techniques to analyse the Fed’s minutes. (…)Two Sigma research’s more technical analysis points out the following:

1. There is big emphasis on the financial markets. Although this emphasis is less than it was in late 2008, it accounts for about 22% of the meeting time.

2. Inflation—specifically, the fact that it’s increasing—is gaining a lot of attention. Discussion concerning this topic takes as much as 24% of the meeting time.

3. Only 5% of the meeting time is devoted to discussion regarding employment.

4. Growth is of major concern. The Fed spends 24% of the meeting time on this topic.

5. Policy takes up another 19% of meeting time. I suspect that this concerns normalisation.

6. Trade only takes up 4% of meeting time.

China’s Debt Bomb: No One Really Knows the Payload

As an addendum to my Wednesday post Certain Uncertainties, this great chart from Visual Capitalist:

![China's Debt Bomb [Chart]](https://i0.wp.com/2oqz471sa19h3vbwa53m33yj.wpengine.netdna-cdn.com/wp-content/uploads/2016/05/china-debt-bomb.png?resize=600%2C1205)

There is a lot more on this in ValueWalk’s China’s Debt-To-GDP Set To Reach 300 Percent In 2020.

U.S.-based stock funds continue trend of outflows in latest week: Lipper Investors pulled another $3.9 billion from U.S.-based stock funds during the week that ended May 18, Lipper data showed on Thursday, bolstering a trend of outflows that has persisted most of this year.

(…) Year-to-date outflows from U.S.-based stock funds now total $45 billion, rivaling the $50 billion in outflows for all of 2011, the last year of major cash withdrawals. The funds bled more than $72 billion in 2008, at the peak of the financial crisis, Lipper data show. (…)

During the latest week, U.S.-based funds focused on domestic shares accounted for 62 percent of the stock outflows. European and Japanese stock funds posted their 16th straight week of outflows, according to the data. (…)