U.S. shoppers spend less over holiday weekend amid discounting

Early holiday promotions and a belief that deals will always be available took a toll on consumer spending over the Thanksgiving weekend as shoppers spent an average of 3.5 percent less than a year ago, the National Retail Federation said on Sunday. (…)

Shay said more 23 percent of consumers this year have not even started shopping for the season, which is up 4 percent from last year and indicates those sales are yet to come. The NRF stuck to its forecast for retail sales to rise 3.6 percent this holiday season, on the back of strong jobs and wage growth. (…)

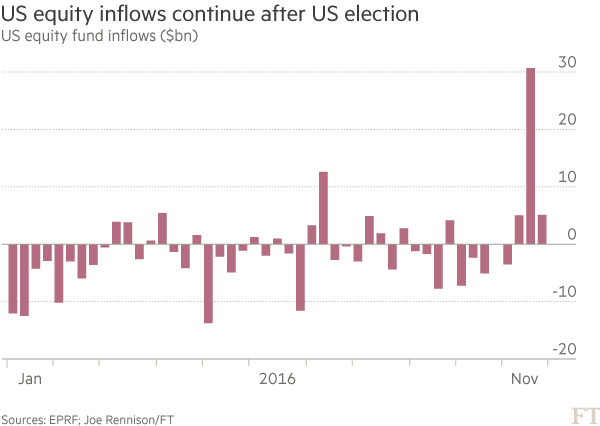

US flash PMI surveys signal robust post-election economy in November

November’s flash PMI surveys provide the first snapshot of US business conditions in the wake of the surprise election result, and show a reassuring picture of sustained solid economic expansion and hiring. As such, the surveys give a clear green light for the Fed to hike interest rates again in December.

Markit PMI v US GDP

At 54.9, the flash Composite PMI showed business activity across manufacturing and services growing at a rate unchanged on October, which had in turn been the fastest for almost a year. The surveys indicate that the economy is expanding at a respectable annualised rate of 2.5% in the fourth quarter.

An acceleration in growth in manufacturing, fuelled mainly by rising domestic demand and an easing in the recent inventory-adjustment drag, offset a slight cooling in service sector growth, although even the latter notched up a robust expansion overall. (…)

Hiring also continued at a solid pace, with the survey’s employment indicators consistent with non-farm payrolls rising by 135,000 in November. Employment continued to be driven by the service sector, although factory jobs rose at an increased rate in November.

The Cass Freight Index and its analysis:

Consistent with what many in the industry have been calling a “more than normal fall surge” in volumes, the Cass Shipments Index was up on a YOY basis for the first time in 20 months. (…)Although it is far too early to make a ‘change in trend’ call, data is beginning to suggest that the consumer is finally starting to spend a little and that the industrial economy’s rate of deceleration has eased. Simply put, the winter of the overall freight recession we have seen for over a year and a half in the U.S. may not be over, but it is showing signs of thawing. (…)

Parcel volumes associated with e‐commerce continue to show outstanding rates of growth, with both FedEx and UPS reporting strong U.S. domestic volumes in the most recent quarter reported by each, up 10.0% and 5.2% respectively. According to the proprietary Avondale Partner’s index in the most recent month available (September), airfreight has also been showing some improving strength with the Asia Pacific lane jumping 7.5% and the Europe Atlantic lane growing 4.7%.

Rail volumes have been part of the weakness, but have become increasingly less bad, and in recent weeks have actually turned slightly positive. The Association of American Railroads (AAR) reported that October YOY overall traffic for U.S. Class 1 railroads declined, as intermodal units fell only slightly (‐0.6%) and commodity carloads originated only fell 3.8%. Rails have seen persistent weakness, with overall volumes being negative 89 out of the last 92 weeks. With the most recent week of data (ending November 12th) posting growth of 2.1%, however, rails may not serve as such a large drag to the overall Cass Shipments Index in coming months.

Why have rail volumes been so weak? We see the strength of the U.S. Dollar driving fewer exports and less domestic manufacturing as the primary driver. In the chart below, we have inverted the value of the dollar to make the inverse relationship easier to see. The current currency valuation would suggest continued weakness in rail volumes. (…)

We continue to assert that the trucking industry provides one of the more reliable reads on the pulse of the domestic economy, as it gives us clues about the health of both the manufacturing and retail sectors. We should note that as the first industrial‐led recovery (2009‐2014) since 1961 came to an end, and the shift from ‘brick and mortar’ retailing to e‐commerce/omni‐channel continues, we are becoming more focused on the number of loads moved by truck and less focused on the number of tons moved by truck. Tonnage itself appears to be growing (three month moving average +1.02 not seasonally adjusted). Counter to this, truck loads have now contracted on a YOY basis five out of the last seven months. No matter how it is measured, the data coming out of the trucking industry has been both volatile and uninspiring.

- Transportation stocks have surged lately as eco surprises turned a little positive (charts from Ed Yardeni):

Donald Trump’s Spending Push Rankles Some in GOP Signs of tension are emerging among Republican lawmakers as President-elect Donald Trump looks poised to stand by promises to slash taxes while spending more on big-ticket items, such as infrastructure and the military.

(…) This suggests the GOP will be willing to tolerate higher deficits in the short-run under Mr. Trump because the party is largely united on overhauling corporate and individual income taxes. Democrats say there is no proof tax cuts pay for themselves. (…)

For Republicans, the bigger fight will be over Mr. Trump’s proposed infrastructure plan. The president-elect has been passionate about rebuilding roads and ports but sketchy on the details of how to pay for it, stirring concerns among Republicans who are uneasy over approving a costly stimulus program. (…)

Mr. Trump inherits a much weaker fiscal position than Presidents Ronald Reagan and George W. Bush did. When Mr. Reagan took office, the Congressional Budget Office projected the U.S. would run a surplus of 2% of GDP over the coming five years, while in 2001, they projected even larger surpluses of 3.3%.

By contrast, the U.S. is now running rising deficits, and the federal debt stands at about 77% of GDP, compared with 25% in 1981 and 31% in 2001. (…)

HOUSING

This chart compares house price valuation metrics (price-to-income and price-to-rent ratios) across six countries. (The Daily Shot)

OPEC Tries to Salvage Deal as Saudis Say Cut Isn’t Essential

(…) With only two days to go before ministers from the Organization of Petroleum Exporting Countries try to finalize the first production decrease in eight years, the foundations for a deal are looking shaky. A final round of diplomacy focused on internal divisions over how to share the cuts and Russian resistance to reducing supply, which already forced the cancellation of crucial talks with non-OPEC suppliers. Khalid Al-Falih, the Saudi oil minister, for the first time on Sunday floated the possibility of leaving Vienna without an agreement. (…)

How Much Bank Stocks Can Gain from Higher Rates Over the past six or so years, superlow interest rates, combined with far more stringent regulation, have taken a heavy toll on banks. So rising long-term bond yields and the prospect the era of superlow rates generally is winding down have investors salivating over a windfall.

(…) “Low rates have led to the lowest bank net interest margins in six decades and lowest revenue growth in eight decades,” said CLSA banking analyst Mike Mayo. (…)

Between 1996 and 2006, U.S. banks had an average return on assets of 1.23%, according to Federal Deposit Insurance Corp. data. Since 2010, the average has been just 0.94%, the data show. (…)

The impact on banks of lower-for-longer rates is especially evident in net interest income, the money generated by the difference between the interest a bank receives on its assets and pays on its liabilities. After growing at a steady clip from 1985 to 2010, net interest income at U.S. banks has stagnated—going to $432 billion at the end of 2015 from $430 billion at the start of 2010, according to FDIC data.

At the same time, total assets at banks in the U.S. rose around 22% to $15.97 trillion.

This growth of assets without growth in interest income is “particularly damning,” said Mr. Davis. “The assets require capital. Shareholders provide the capital. A lot of additional capital has been provided in which the return at the margin is minimal.”

Adding to the pressure: Regulators have required banks to hold more equity. That, combined with lower returns on assets, has led to far lower returns on equity. Between 1996 and 2006, the return on equity for U.S. banks averaged 13.65%, according to FDIC data. Since 2010, the average has been 8.40%. (…)

The shape of the yield curve amplifies the impact of superlow rates. Looking at data from 1995 to 2012, researchers from the Bank for International Settlements found banks lose more from very low rates and flat yield curves than they gain from rising rates and steeper curves. “This indicates that the impact of interest rates on bank profitability is particularly large when they are low,” the researchers concluded. (…)

That shows up in banks’ net interest margins. At the start of 2010, these averaged 3.84% for U.S. banks. By the second quarter of 2016, they had fallen to 3.08%, FDIC data show.

- Easy math, isn’t it? From the same WSJ just two days earlier (my emphasis):

(…) Given President-elect Donald Trump’s lack of experience and ever-changing positions, the people he puts in place are likely to exert significant influence on policy. One is Jeb Hensarling, chairman of the House Financial Services Committee and a potential candidate for Treasury secretary. Even if he stays in Congress, he will be instrumental in shaping any new bank legislation.

Another person to watch is Thomas Hoenig, who is vice chairman of the Federal Deposit Insurance Corp. Mr. Hoenig’s name has been making the rounds as a possible pick for Federal Reserve vice chairman for supervision. (…)

Both men have argued publicly that holding more loss-absorbing equity capital is the best way to make systemically important banks more resilient. Mr. Hensarling has proposed legislation that would exempt banks from a broad range of regulations in exchange for holding higher levels of capital.

Specifically, he focuses on the “leverage ratio” of tangible equity to total assets plus off-balance-sheet exposures. This would be more stringent than the current regulatory standards, which measure capital against risk-weighted assets. To qualify for relief, Mr. Hensarling wants banks to maintain “tangible equity,” defined in the proposal as Tier 1 common equity plus preferred shares, equivalent to 10% of total assets and exposures.

Calculations by The Wall Street Journal show that none of the six biggest banks in the U.S. would qualify for regulatory relief under this standard. Collectively, they would fall short by about $115 billion of equity capital. This estimate could undercount the amount of needed capital because it is based on total assets and doesn’t take into account off-balance-sheet exposures.

J.P. Morgan Chase is short by the most, about $44 billion. But Morgan Stanley’s shortfall is biggest relative to its size, at 18% of its market capitalization. The need to issue shares or cut dividends and buybacks to get to the standard suggests they would hesitate to make the trade, even in exchange for substantial regulatory relief.

Mr. Hoenig hasn’t proposed anything so specific, but in speeches he has argued against lowering capital requirements for systemically important banks. He has also favored use of the more stringent leverage ratio and tangible equity capital. Mr. Hensarling’s proposals cite Mr. Hoenig’s arguments for inspiration.

There are other reasons why big banks are rallying, including higher interest rates and trading volumes. But investors hoping for increased capital returns should temper expectations.

I don’t pretend to be a bank analyst but the correct complete analysis is to merge both the income and the balance sheet sides. On the one hand, banking incomes should benefit from wider spreads and lesser regulatory costs. But banks have amply demonstrated that they can’t control their greed. So more capital will be required to protect depositors and taxpayers as the second WSJ piece said.

The WSJ calculations show a $115B shortfall for the 6 largest banks. The same calculations by RBC Capital total $376B on $901B of Tier Capital, a required 40% jump in capital. Under either calculations, the additional capital is significant and highly dilutive.

(…) And ‘optimistic’ might be an understatement. According to the

(…) And ‘optimistic’ might be an understatement. According to the