- 17 days have passed since VA. started reopening. (ZH)

- Wuhan, the hub of China’s coronavirus outbreak, said it tested nearly seven million people in 12 days, concluding a campaign to test the entire population after several infections prompted fears of a second wave. A total of 6.68 million people underwent nucleic acid tests, of which 206 asymptomatic cases were reported, according to Bloomberg calculations.

- Indonesia deployed hundreds of thousands of army and police personnel across the vast archipelago to enforce social-distancing rules after a record surge in infections in the past week cast doubt on plans to reopen Southeast Asia’s largest economy.

French hospital tests show sustained Covid-19 immunity The FT reports that “tests on coronavirus-infected healthworkers in two French hospitals show that 98 per cent of them maintained strong immunity a month later”.

French hospital tests show sustained Covid-19 immunity The FT reports that “tests on coronavirus-infected healthworkers in two French hospitals show that 98 per cent of them maintained strong immunity a month later”.

More young people are testing positive for coronavirus in US, study finds Scientists found that half of those who had tested positive for Covid-19 in Washington state by early May were aged under 40, significantly more than at the initial stage of the outbreak.

(…) The findings could point to progression of the pandemic in other areas, since “Washington state is the first in the United States with Covid-19 experience and [has] the longest outbreak timeline”, Malmgren said in a non-peer reviewed paper posted on preprint website medRxiv.org on Saturday. (…) The scientists warned that given the increasing prevalence of Covid-19 among young people, the reopening could put them and their families at greater risk. (…)

While new cases have been declining in Washington state, the researchers found that the proportion of children and young adults confirmed with Covid-19 rose from 20 per cent on March 1 to 50 per cent early this month.

And there was “no decline in cases” in the 0 to 19 age group, Malmgren said in the paper. In contrast, the incidence of the disease among people aged 60 and older fell by 55 per cent from the peak of cases. (…)

“The shift from older to younger population Covid-19 infection may mask a true decline in cases and the need for future health care capacity if the currently infected portion of the population is younger, less likely to report symptoms, and at less risk of a severe life-threatening disease requiring hospitalisation,” the researchers said. (…)

The trend of younger people contracting the virus has also been reported in other countries. In Brazil, doctors have said that half their patients were young, and many were dying – 15 per cent of deaths in the country were people aged under 50, which was 10 times the proportion in Europe, The Washington Post reported.

The situation was worse in Mexico, with nearly a quarter of deaths among people aged between 25 and 49, according to health authorities. (…) (SCMP)

- Revelers celebrate Memorial Day weekend Saturday at Osage Beach, on the Lake of the Ozarks in Missouri. (Axios)

PANDENOMICS

Worst of Shutdowns May Be Over Recovering air travel, hotel bookings and mortgage applications are among the early signs the U.S. economy is slowly creeping back to life

Truck loads are growing again. Air travel and hotel bookings are up slightly. Mortgage applications are rising. And more people are applying to open new businesses. (…) for the first time since the pandemic forced widespread U.S. business closures in March, it appears conditions in some corners of the economy aren’t getting worse, and might even be improving. (…)]

The number of travelers passing through Transportation Security Administration security screening checkpoints fell to 87,534 on April 14, 96% below the same day a year earlier. But by May 24, the figure had more than tripled to 267,451, although that is still down 87% from the same day a year earlier. (…)

“You can see [the burgeoning rebound] in the data, which is encouraging,” he said, “but you have to be cautious that we’re rebounding from extremely depressed levels.” (…)

Still, the economic outlook remains highly uncertain. The latest hopeful signs coincide with a surge in emergency spending from Congress, a decline in the daily number of newly reported Covid-19 cases in the U.S. and the slow reopening of all 50 states—all factors that could prove temporary. (…)

Job losses often persist for months after a recovery begins. The 2007-09 recession ended in June 2009, according to the National Bureau of Economic Research. But the unemployment rate didn’t peak until months later, at 10% in October 2009, and remained above 9% for nearly another two years. (…)

A few charts from CalculatedRisk to appreciate where we are and where we come from:

- World trade has been falling throughout May: (ING)

YoY growth in the number of idle container ships ") Source: Bloomberg

Source: Bloomberg

The Conference Board Leading Economic Index®(LEI) for the US dropped 4.4 percent in April, following a decline of 7.4 percent in March. The decline marks the end of more than 11 years of economic expansion and clearly indicates the US economy is now in deep recession territory.

This downturn differs from previous recessions—the bursting of the tech bubble in 2001 and the Great Recession of 2008–2009. This time, there were few indications of a potential downturn, but once the shock of the pandemic hit, the drop was much sharper.

The underlying components of the index show spotty improvements in financial markets in April. However, the widespread damage to labor markets and industrial activity suggests the imminent reopening of some sectors won’t be enough to generate a fast rebound for the economy at large.

State, Local Budget Woes Create Drag for Recovery Prospects The hit to U.S. state and local finances from the coronavirus pandemic could be a drag on the nation’s economic recovery for years to come, if the past is any guide.

(…) The condition of state and local government finances affects the health of the broader economy because their spending amounts to almost 11% of gross domestic product, and they employ about one of every eight American workers, including teachers, police officers and firefighters. (…)

Across the country, states and cities are being squeezed by a combination of lost revenues and rising spending on services like unemployment insurance and health care. Unlike the federal government, they cannot run deficits, so the gap must be filled by spending cuts, tax increases or both.

Moody’s Analytics estimates they will need to make $500 billion in cuts over the next two years due to the economic effects of the coronavirus. (…)

Based on evidence from the last recession, Mr. Chodorow-Reich estimates that every dollar in cuts costs the overall economy $1.50 to $2. (…)

Following the last recession, states and localities continued to cut jobs and spending long after the recovery began. They didn’t start sustained hiring until August 2013, according to the Labor Department. Spending cuts continued until early 2014, according to the Commerce Department. Public spending and employment didn’t return to their previous peaks until last fall. (…)

Economy Recovering, but Unemployment Likely to Remain High, Trump Adviser Says The first shoots of an economic recovery from shutdowns caused by the coronavirus pandemic are starting to emerge, but the U.S. is likely to face a sustained period of record-high unemployment.

(…) “It looks like the economy is picking up at a very rapid rate,” Mr. Hassett said. “In which case we could potentially move on to other things that the president has mentioned, like the payroll tax cut and potentially even a capital-gains holiday.”

Mr. Hassett, an economist, said he thought the unemployment rate would begin to fall in June, but would remain above 10% this fall, when Americans head to the polls for the presidential elections. Voters, he said, will be focused on a rapidly improving economy, not a historically high rate of joblessness.

By the fall, “all the signs of economic recovery are going to be raging everywhere,” he said, adding businesses have the capacity to quickly ramp up and that unemployed Americans are ready to return to work, factors that could fuel a fast recovery. (…)

Consumer Debt During the Coronacrisis

Consumer Debt During the Coronacrisis

(…) total unemployment insurance (UI) benefits (including the $600/week federal supplement) more than offset lost income for low-earning workers. We estimate that net income will increase by over 170% for UI-eligible workers in the bottom income quintile and by over 50% for workers in the second quintile. Thus, income replacement rates are very high for the most affected workers, suggesting that most of these workers should not have trouble making payments despite losing their jobs. The current generosity of unemployment benefits is an important contrast to past recessions.

In addition to generous UI benefits, stimulus payments to individuals will also help consumers meet debt obligations. A recent NBER paper found that 25% of the spending increase following the receipt of stimulus payments went to pay bills. Our current fiscal outlook includes additional payments to individuals later this year (consistent with the Phase 4 fiscal package released by House Democrats earlier this week), which should further help households make payments.

(…) the CARES Act guarantees forbearance on all GSE-backed mortgages for up to 180 days, with extensions possible. (…) The CARES Act also suspended payments and interest on federal student debt through September, made it easier to extract cash from 401(k) plans, and barred lenders from reporting certain delinquent payments to credit agencies.

(…) many private mortgage, credit card, and auto lenders are offering deferred and alternative payment plans, while governors from 10 states reached an agreement with private student loan providers to guarantee forbearance and suspend late fees. Additionally, most telecommunication providers adopted formal accommodation policies for households negatively affected by the coronavirus, and anecdotes suggest a similar response from some landlords.

Beyond the short term, we see two reasons that defaults and delinquencies might rise. First, defaults could increase later in 2020 if UI benefits are not extended, and will likely rise in 2021 as benefits are reduced while unemployment is still elevated. Second, higher out-of-pocket medical expenses due to loss of employer-based health insurance could push more households to default. (…) (Goldman Sachs)

(…) When it comes to actual loans, banks in Italy have processed and approved requests for around €13 billion ($14.3 billion). That is far below the €300 billion the government is making available. European companies are particularly dependent on bank lending, unlike in the U.S. where capital markets are relied upon much more heavily.

For banks, the problem is simple: No matter how much money is thrown at them by governments, there is a limit to how much risk they can take.

Nowhere is the problem more evident than in southern Europe, where the fragile banking sector is still trying to get rid of huge portfolios of bad loans from the last decade’s crisis. Corporate indebtedness in the region is also high.

(…) besides the higher risk-aversion due to dire economic projections, there are other hurdles. The main one is that in Italy, bankers can be held legally responsible for the decision to issue the guaranteed loan and can potentially face criminal sanctions if the credit turns bad. (…)

Another problem is that companies under debt restructuring aren’t eligible for state guarantees. (…)

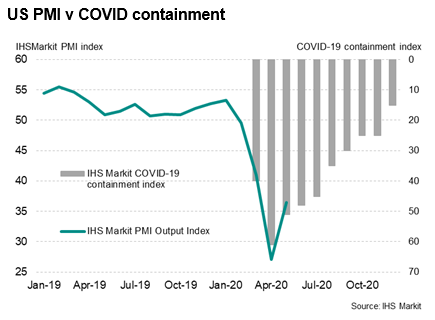

(…) The good news going forward is that, barring any second waves of infections, all major economies look set to loosen coronavirus restrictions further in coming months according to government ‘road maps’, which should help lift the PMIs further as we move into the second half of the year (see charts).

However, as the charts also highlight, at least some containment measures are set to be retained in all countries through to the end of the year, and likely into 2021, unless an effective treatment or vaccine for COVID-19 is found. These restrictions will inevitably limit growth of demand and employment as economies try to recover, meaning returns to pre-pandemic levels of GDP and employment look set to be frustratingly long in all cases.

")

Walks a bit like a ‘v’, talks a bit like a ‘v’ but this is not a ‘v’. Germany’s most prominent leading indicator just staged a strong comeback but the route to normalcy remains long. The Ifo index posted the strongest monthly increase in May, after two record-sized drops, and stood at 79,5 from 74.3 in April. This is still the second weakest reading since reunification. The increase was mainly driven by a strongest monthly improvement ever in the expectations component. The current assessment component actually dropped again but still remains slightly above the record lows seen during the 2008/9 recession.

Today’s Ifo index echoes more real-time signals that economic and social activity has started to pick up significantly since the first lifting of the lockdown measures in late April. Just to be clear, it is currently still impossible to measure the more permanent damage the crisis has caused and what its impact will be on future growth. Reviving economic activity and returning optimism are highly welcome but are definitely no reason for complacency or even hubris. The fact that capacity utilization in the industry has dropped to its lowest level since 2009 as well as that access to finance is a much bigger impediment to production than during the financial crisis illustrate the depth of the crisis. Even in a more benign scenario, with more gradual lifting of the lockdown measures and no second wave of the virus, the German economy is unlikely to return to its pre-crisis level before 2022.

In short, the low point of the slump should now be behind us and there even is the chance for a short-lived strong rebound in the coming months. However, given the absolute low level of the Ifo index and the fact that the damage of the last two months is likely to weigh on growth going ahead, don’t be mistaken: this is not a ‘v’.

China Recovery

China recovery is well underway, suggesting a quick economic recovery. (Morgan Stanley Research)

-

Fiscal stimulus stronger than headline numbers suggest

As announced by the government work report, the official on-budget deficit ratio will increase significantly by 0.8pp to 3.6% in 2020. But the effective deficit, which we argue is a more relevant indicator to measure the on-budget fiscal stance by taking financing through drawdown of fiscal deposits and transfers from other fiscal accounts into account, will increase even more, by 1.6pp to around 6.5% this year, according to the budget report released on the MOF website over the weekend. Overall, even though central government special bonds issuance would be only half of our expectation at Rmb 1tr, after incorporating the additional detail in the budget report, our augmented fiscal deficit points to a slightly stronger fiscal stimulus than our previous forecast, but still notably smaller than that in GFC. (Goldman Sachs)

(…) “China now has a middle income group of between 500 and 700 million people, and that alone can be a source to power Chinese economic growth for the next five years,” the state researchers wrote. (…)

Xi said China would use a “new development pattern” consisting of “both the great domestic economic circle and the international economic circle”, instead of relying solely foreign markets.

While China will not give up on the international market, it will increasingly tilt its manufacturing might to meet the demands of its huge domestic market. (…)

Xi compared the restriction on hi-tech exports to China to putting a hand around the country’s throat. (…)

The national plan forms the basis for hundreds of mini five-year plans used by provinces, cities and industries, keeping the whole country’s development priorities on the same page. (…)

Michael Pettis, a professor of finance at Peking University’s Guanghua school of management, said centralised planning “won’t work well as the Chinese economy has already reached a certain level of maturity”.

“What you need are institutional reforms that allow the Chinese people to become more productive … You need every business-person to make his own plans.”

Coronavirus Threatens to Hobble the U.S. Shale-Oil Boom for Years The coronavirus pandemic is going to thin the ranks of shale companies and leave survivors that are smaller, leaner and less able to pursue growth at any cost.

(…) Shale-oil companies have sharply reduced their drilling budgets for the year, with the top 15 by market capitalization slashing spending by an average of 48%, a Wall Street Journal review of company disclosures found. Forty-six independent U.S. producers planned a combined $38 billion in capital investments this year, the lowest dollar amount since 2004, according to Cowen. (…)

Since mid-March, operators have idled almost two-thirds of the U.S. rigs that had been drilling for oil, bringing the nation’s oil-rig count to the lowest since July 2009, according to services firm Baker Hughes Co. BKR -0.79% That all but ensures U.S. production is going to fall, even if companies decide to restart existing wells sooner than expected.

U.S. oil output fell to 11.5 million barrels a day in mid-May [from 13m earlier this year], according to the Energy Department, after companies turned off wells. Some estimate production has already sunk lower. (…)

The Energy Department now expects U.S. oil production to slide to about 10.8 million barrels a day early next year, down from its January forecast of 13.5 million daily by that time.

Daniel Yergin, vice chairman of IHS Markit, expects U.S. oil output to bottom around nine million barrels a day next summer, before eventually returning to about 11 million barrels a day. (…)

Large public U.S. producers poured a total of $1.18 trillion into drilling and pumping oil over the past decade, largely in shale plays. But they came up well short of making their money back, collectively bringing in $819 billion in cash from their oil operations, according to Evercore ISI. (…)

Fitch Ratings Inc. said the default rate among high-yield U.S. exploration and production companies could reach 25% in 2020, the highest since March 2017. (…) “Thirty dollars doesn’t fix anything.” (…)

PANDEMONIUM

China condemned the U.S. adding 33 Chinese entities to a trade blacklist, a move that risks potential retaliation from Beijing as tensions between the world’s two-biggest economies deteriorate further.

The U.S. Department of Commerce on Saturday expanded its so-called entities list, which restricts access to American technology and other items, to include 24 Chinese companies and universities it said had ties to the military and another 9 entities it accused of human rights violations in Xinjiang. (…)

China’s Foreign Minister Wang Yi on Sunday warned U.S. politicians were pushing relations to a “new Cold War,” as American politicians condemned Beijing’s move to impose a national security law on Hong Kong. (…)

The recent move from the U.S. may prompt China to take some “proportionate countermeasures,” said Zhou.The “unreliable entity list” could be one option and “retaliation could be taken as early as after the Two Sessions,” Zhou said, referring to the annual legislative meetings currently underway in Beijing and scheduled to end on May 28.

Meanwhile…

The Future of the Dollar U.S. Financial Power Depends on Washington, Not Beijing

By Henry M. Paulson Jr. in Foreign Affairs

(…) That the dollar has maintained this stature for so long is a historic anomaly, particularly in the context of a rising China. The Chinese renminbi (RMB) has by far the greatest potential to assume a role rivaling that of the dollar. China’s economic size, prospects for future growth, integration into the global economy, and accelerated efforts to internationalize the RMB all favor an expanded role for the Chinese currency. But by themselves, these conditions are insufficient. And China’s much-touted successes in the realm of fintech—including its rapid deployment of mobile payment systems and the recent pilot project by the People’s Bank of China to test a digital RMB—will not change that. A central bank–backed digital currency does not alter the fundamental nature of the RMB.

Beijing still has major hurdles to overcome before the RMB can truly emerge as a primary global reserve currency. Among other transformative measures, it needs to make more progress in moving to a market-driven economy, improve corporate governance, and develop efficient, well-regulated financial markets that earn the respect of international investors so that Beijing can eliminate capital controls and turn the RMB into a market-determined currency. (…)

Above all, the United States must preserve the conditions that created the dollar’s primacy in the first place: a vibrant economy rooted in sound macroeconomic and fiscal policies; a transparent, open political system; and economic, political, and security leadership abroad. In short, sustaining the dollar’s status will not be determined by what happens in China. Rather, it will depend almost entirely on the United States’ ability to adapt its post-COVID-19 economy so that it remains a model of success. (…)

Over time, the international monetary system will likely once again give relatively equal weight to two or more global reserve currencies. The RMB is a chief contender, as it is already a reserve currency along with the yen, euro, and pound. And short of a major catastrophe, the Chinese economy is on course to becoming the world’s largest in the foreseeable future. It will also be the first major economy to recover from the COVID-19 crisis. (…)

Although a Beijing-backed digital currency in and of itself is unlikely to undermine the dollar’s supremacy, it could certainly facilitate China’s efforts to internationalize the RMB. In countries with unstable currencies, such as Venezuela, a digital RMB is an attractive alternative to the local currency. Chinese firms such as Tencent, which already have a sizable presence in developing countries in Africa and Latin America, could scale up their presence there, leading a future digital RMB to gain market share. This could help enhance the RMB’s global status and become part of a broader strategy to project Chinese economic and political influence abroad. (…)

The danger is that overzealous U.S. regulators might raise the entry barrier for U.S. firms to serve those who prefer digital finance over conventional banking in the United States and unbanked consumers around the world—about two billion people, according to the World Bank, the bulk of whom reside in developing countries with weaker financial markets and volatile currencies. (…)

The dollar’s status is a proxy for the fundamental soundness of the American political and economic system. To safeguard the dollar’s position, the U.S. economy must remain a model of success and for emulation. That, in turn, requires a political system capable of implementing policies that will allow more Americans to flourish and achieve economic prosperity. It also requires a political system capable of maintaining the country’s fiscal health. History knows of no country that remained on top without fiscal prudence over the long term. The U.S. political system must be responsive to today’s economic challenges. (…)

Washington should also be mindful that unilateral sanctions—made possible by the primacy of the dollar—are not free of cost. Weaponizing the dollar in this way can energize both U.S. allies and foes to develop alternative reserve currencies—and maybe even to join forces to do so. That is precisely why the European Union has been pushing to further promote the euro in international transactions.

By the same token, whether the RMB joins the dollar as a major reserve currency will be determined entirely by how China reshapes its own economy. But if Beijing successfully implements the needed reforms, it will create an economy that is more attractive for the export of U.S. goods and services and establish a more level playing field for U.S. companies operating in China—changes that will benefit the United States.

The value of a national currency to its holders is ultimately a reflection of the country’s economic and political fundamentals. How the United States emerges in the years following the COVID-19 crisis will be an important test. First and foremost, the country must foster macroeconomic policies that put it on a sustainable path to manage the national debt and the trajectory of the structural fiscal deficit, and it must not squander the fundamentals that have sustained its economic might, all of which are rooted in a spirit of innovation and effective government. If Washington adheres to this course, there is every reason to have confidence in the dollar.

Nearly half of Twitter accounts pushing to reopen America may be bots There has been a huge upswell of Twitter bot activity since the start of the coronavirus pandemic, amplifying medical disinformation and the push to reopen America.

Nearly half of Twitter accounts pushing to reopen America may be bots There has been a huge upswell of Twitter bot activity since the start of the coronavirus pandemic, amplifying medical disinformation and the push to reopen America.

(…) Across US and foreign elections, natural disasters, and other politicized events, the level of bot involvement is normally between 10 and 20%, she says.

But in a new study, the researchers have found that bots may account for between 45 and 60% of Twitter accounts discussing covid-19. Many of those accounts were created in February and have since been spreading and amplifying misinformation, including false medical advice, conspiracy theories about the origin of the virus, and pushes to end stay-at-home orders and reopen America. (…)

But it’s not just the volume of accounts that worries Carley, the center’s director. Their patterns of behavior have grown more sophisticated, too. Bots are now often more deeply networked with other accounts, making it easier for them to disseminate their messages widely. They also engage in more strategies to target at-risk groups like immigrants and minorities and help real accounts engaged in hate speech to form online groups. (…)

EARNINGS WATCH

We now have 478 reports in and blended earnings are set top drop 12.6%. Five sectors remained positive!

But not for long:

Trailing EPS are $158.87, down only 3.4% from the end of March but that will change after Q2 which is expected to show a $17 decline (-43%) in YoY EPS, 3 times as much as in Q1 (-14.5%). Full year: $125.79e. 2021: $164.04e, like nothing lasting happened.

Barry Ritholz:

What if the pandemic – an externality seperate from the business cycle – did not cause the bull to end? What if this is only a temporary pause, an artificial reduction in earnings that reverses as circumstances normalize? It could be more akin to a natural disaster (Volcano or meteor strike) than a cyclical economic contraction – then what? (…)

Asking if stocks are too expensive right here mid pandemic is the wrong way to think about this. A better question: Whether the post-recovery profit environment will justify currently lofty but temporary stock valuations. How you answer that earnings question will determine your investing posture.

The Rule of 20 P/E is 20.3 at today’s pre-opening of 3000 using trailing EPS. It is 19.7 using 2021 estimates, fair value if you believe.

SentimenTrader has this Smart vs Dumb money indicator measuring what people do as opposed to what they say:

The Smart Money Confidence and Dumb Money Confidence indices are a unique innovation that allows subscribers to see, in one quick glance, what the “good” market timers are doing with their money compared to what “bad” market timers are doing.

Our Confidence indices use mostly real-money gauges – there are few opinions involved here. Generally, we want to follow the Smart Money traders when they reach an extreme – we want to bet on a market rally when they are confident of rising prices, and we want to be short (or in cash) when they are expecting a market decline. The higher the confidence number, the more aggressively we should be looking for higher prices.

(…) Dumb Money (…) traders have proven themselves over history to be bad at market timing. They get very bullish after a market rally, and bearish after a market fall. By the time the majority of them catch on to a trend, it’s too late – the trend is about to reverse. It tells us how confident we should be in selling the market.

Not fool proof but interesting.

It was better to follow Smart money in 2015…

…and again in late 2018 and during the last 6 months.

Now that we’re in the post-panic chop, there is much less of a unified picture. We’ve discussed this several times recently, like some surveys and other measures showing pessimism while the behavior of options traders suggests overwhelming optimism.

It gets confusing, which is why we like to rely more heavily on aggregate models that take most of those factors into account. When we do that, we can see that both Smart Money Confidence and Dumb Money Confidence are both high, which is confusing in itself. Normally, the two move opposite each other.

Even so, the spread between them is nearing zero. During bear markets, we start to enter the danger zone when sentiment becomes neutral after bouts of severe pessimism. That’s where we are now.

This happened in 2016 and 2019 as well. The spread neared zero while the S&P 500 was still below its 200-day average. After those, buyers persisted and that was a good sign longer-term.

But the spread has closed mainly because Dumb money is getting more confident as the economy reopens, medical news improve, vaccine hopes rise and momentum is positive.

Let’s go back to 2009-09. The S&P 500 peaked in June 2007 at 1503. It dropped 12% to 1323 in March 2008, recovered 6% to 1400 by May, lost 8% in the following 3 months before starting its 50% descent to March 6, 2009.

In May 2008, Q1 EPS were down 16%. The rate of decline accelerated to -18% in Q2 and Q3 before reaching -65% in Q4 which began reporting in Mid-February 2009.

Q2’20 EPS, which will get reported starting in mid-July, are seen down 48% YoY.

Smart money felt very clever buying apparently good value stocks from Dumb money in the fall of 2008 but the smart heads succumbed to depression throughout 2009 when everybody should have been buying. Dumb money got merry in April 2009 and proved much smarter than Smart money for the next 12 months.

While the Smart/Dumb ratio is now almost one, I tend to dismiss it like in late 2008. Eventually, earnings matter.

The market has been rising on Smart money but I think Dumbo is currently the smarter one.

Is it really?

- The move to zero commissions in October and the lockdowns boosted individual investor volumes. (GS)

Securities trading was among the most common uses for the government stimulus checks in nearly every income bracket, according to software and data aggregation company Envestnet Yodlee. For many consumers, trading was the second or third most common use for the funds, behind only increasing savings and cash withdrawals, the data showed. (…) Yodlee’s data is based on bank account transfers of 2.5 million Americans that received checks. “There’s clearly a correlation between Covid and people being reengaged with their money,” Bill Parsons, Group President, Data Analytics at Envestnet Yodlee told CNBC. (…)

Insiders are supposed to be smart and they don’t seem very merry now: (Barron’s)

Global GDP Growth Forecasts BofA has revised lower 2020 GDP growth for 28 of 43 countries.

Global GDP Growth Forecasts BofA has revised lower 2020 GDP growth for 28 of 43 countries.

")

") Source: Bloomberg

Source: Bloomberg

")

{kind=link}