TECHNICALS WATCH

High equity valuations have been more than offset by rising earnings, low interest rates and strong technical trends. At this time, earnings and interest rates remain supportive. Many technical measures, however, have deteriorated, signalling increasing investor wariness.

Per Lowry’s Research, unlike market bottoms which are events, market peaks are generally a process developing over weeks and months. This needs a rigorous and objective analysis based on a deep knowledge and understanding of past trends.

A casual look at the S&P 500 Index triggers few worries, except perhaps one of missing this latest buy-the-dip opportunity:

The fact that the equal-weighted S&P 500 has broken its 2020-21 trend may be a first warning but there is continued support from the still rising moving averages:

And the tech stalwarts remain popular:

The problems emerge with the smaller cap stocks which have been see-sawing since March and are at a critical junction with their various moving averages with only the 200dma still being supportive.

In effect, leadership is getting narrower and narrower and even the appetite for the leaders is waning:

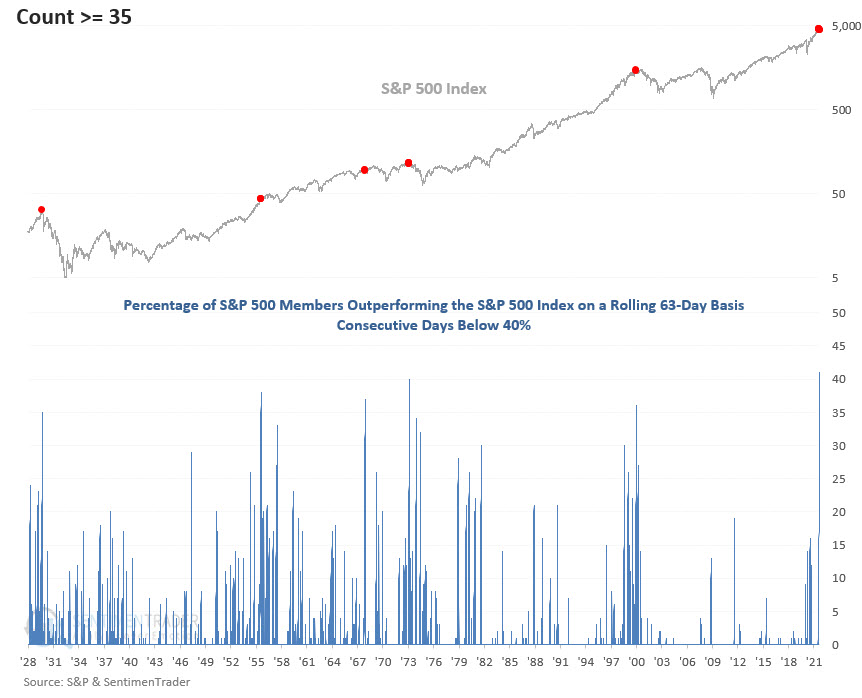

@DeanChristians tweeted this unusual breadth chart last week with this explanation: “If we count the number of days when fewer than 40% of S&P 500 members outperform the Index on a rolling 63-day basis, the indicator surpassed the longest streak in history on 9/13/21.” See the red dots?

These BofA charts (via The Market Ear) show the explosion in equity inflows last week: yet, these buy-the-dips funds failed to boost equities as sellers dominated.

Selling volume has overcome buying volume in recent weeks, indicating a rising desire to own zero-return cash. TINA is apparently not quite as powerful, and not only in the USA:

China’s Evergrande Moment: Bear Stearns, LTCM, Lehman or Minsky?

- John Authers: China’s Evergrande Moment Is Looking More LTCM Than Minsky The Chinese government’s likely response implies a nasty and messy market, but not an all-out implosion.

(…) Will it be a Minsky Moment, akin to the Lehman collapse? Or will it be more akin to the LTCM Moment? Or might it just be altogether less momentous? To measure this we need to resuscitate another concept of which many of us thought we had heard the last more than two decades ago: Asian contagion. How much effect will Evergrande’s troubles have on the rest of us?

To define the terms: a Minsky Moment, named for the economist Hyman Minsky, happens when confidence breaks after a prolonged period of speculation. The most famous example is the Lehman Moment, which came in 2008 when Lehman Brothers went bankrupt as a result of excessive subprime lending, and the knock-on effects brought the global financial system to a standstill. An LTCM Moment is named for the implosion of the Long-Term Capital Management hedge fund in 1998, which also followed a sudden loss of confidence after a period of excessive speculation.

The difference between LTCM and Lehman lay in what the authorities did about it. After LTCM, the Federal Reserve banged the heads of creditors together to bail it out, and then cut interest rates. That sparked the last mad 18 months of the 1990s bull market. The Lehman Moment happened when the government decided not to repeat the LTCM experience, because it had created too much moral hazard — the irresponsible behavior that comes when people are sure they will be bailed out. The result was the worst U.S. market crisis in eight decades, and arguably the greatest global financial crisis ever. (…)

Yes, Evergrande is big enough to create a Minsky Moment within the Chinese market. But we should expect the response to be far more LTCM than Lehman. (…)

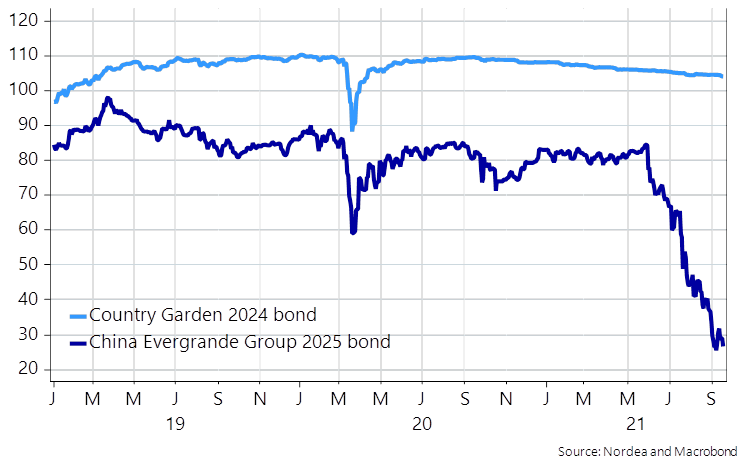

There is evident contagion in the real estate sector; yields of companies in other industries, including even banks, haven’t moved much, at least yet. And, as this chart produced by Societe Generale SA shows, there has been no contagion from high-yield to investment-grade debt:

(…) The news from the broader real estate market is terrifying. China is pockmarked with speculative properties and it isn’t at all clear that there will ever be buyers for them. This is terrible collateral.

So why is there still relative calm? It boils down to a close reading of the Chinese authorities’ intentions. They have no interest in staging their own Lehman. There has been alarm about the possibility of a Minsky moment for years in Chinese circles, frequently voiced out loud. Officials know what could happen and are determined to prevent it if they can. Efforts to rein in credit have been going on for years. And Evergrande is in trouble largely because the government itself decided to clamp down on property developers through the “three red lines” policy last year.

Governments can easily make mistakes, of course. But the Chinese plainly intend this to be more LTCM than Lehman. (…)

Another reason to expect the Chinese government to do something to ensure an orderly process is that they have no choice. To use another familiar phrase from the Lehman debacle, Evergrande is far too big to fail. (…)

A final point is that we also have an idea of the likely playbook from the failure of the smaller but even more interconnected Baoshang Bank two years ago. To quote Wei Yao of Societe Generale:

While we do think that Evergrande is systemically important, we also reckon that Chinese policymakers have the willingness, capability and knowhow to stem a financial market meltdown. On this front, the default of Baoshang Bank on its interbank liabilities in May 2019 is a good reference. Compared with Baoshang at the time of default, Evergrande has much more total debt, but similar amount of liabilities to financial institutions and in the capital markets. Also, Baoshang had more complex ties in the financial system (with over RMB300bn interbank liabilities with over 700 counterparties) and, very importantly, its default was a complete surprise.

The Baoshang episode showed, to quote Yao, that avoiding a systemic liquidity squeeze was “the absolute priority for the the People’s Bank of China” and that it had the means to do so. Policy makers are also able to buy time to make a restructuring less painful.

-

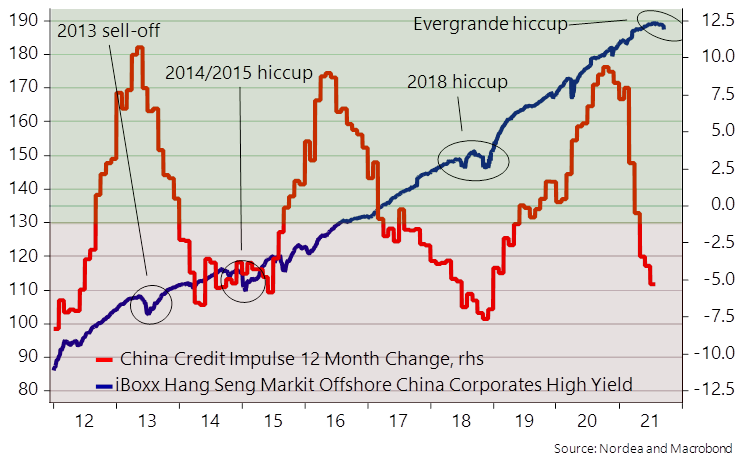

There’s a Lehman in China every 36 months Is Evergrande a Lehman event? We sincerely doubt it. It is (way) easier to contain Evergrande than Lehman, but it doesn’t mean that the Evergrande blow-up doesn’t come with repercussions. Markets will likely stay in “stagflation mode”.

(…) Contagion effects from Evergrande are likely to be decently contained and markets are yet to care about true spill-over effects in for example Country Gardens (Chinas biggest real estate developer) tradable bonds, while Chinese high yield has been selling moderately off in a broader scale. This doesn’t seem like a market truly scared of a true Lehman-like contagious meltdown scenario despite Evergrande bonds trading at a “recovery rate” of one to four or thereabout. This could be our famous last words, but we struggle to get really scared about Evergrande, but obviously one can never say never(grande).

Contagious effects from Evergrande still remain sparse in a bigger perspective

We tend to get a round of “China is melting down” with an interval of 2-3 years and they usually always occur when the Chinese credit impulse is negative. China is a credit-fuelled economy and there are always casualties when the authorities decide to take the foot of the pedal.

This was also the case in 2014/2015 and 2018 when the Chinese markets suffered markedly due to a clearly negative credit impulse and in sharp contrast to the US in 2008 Chinese authorities hold all the ammo needed to turn the tide on credit growth (if needed). They can essentially credit grow the “beep” out of everyone trying to bet against them if they want.

There’s a Lehman in China every 36 months and usually the authorities solve it

It doesn’t mean that the Evergrande/China slowdown comes without global repercussions. The global credit impulse has been (mainly) driven by China in recent years but currently we see a very uniform decelerating impulse across jurisdictions. The interesting thing is that the impulse is now clearly negative (a contraction of credit on the second derivate) likely because of a voluntary drawdown on the revolving facilities that were widely utilized during Q2/Q3-2020. In other words, credit growth is slowing fast as 1) liquidity facilities are not as needed now and 2) the impulse from the fiscal and monetary side is weakening in YoY terms. Gravity pulls.

The big question is if this is something to worry about. We think it warrants a shift in asset allocation trends away from cyclicals to defensives

In FX space, a slowing credit impulse is good news for our view that the USD will continue to perform versus European peers as Europe is clearly more interlinked with Chinese developments than the US. It likely also means that Eastern Europe FX will suffer versus EUR during the late autumn as e.g. Poland and Hungary are high beta to German performance (whatever Germany does, Poland does times 1.5).

The PMIs next week will look solid in Europe due to service sector reopening effects but that is likely also going to be the “peak” of the #Euroboom narrative. At least we don’t buy it with one single penny as Germany lags China by a bit more than a quarter and China is clearly slowing, and then we haven’t even touched upon the possibility of Powell launching a NFP-targeting tapering process already on Wednesday.

The surge in natural gas prices has helped prompt worries about stagflation, or at least about a negative impact on growth, especially in Europe (where natural gas prices have surged more than in the US). A person of a bullish persuasion would now argue, and rightly so, that rising prices may reflect strong demand, and if that’s the case there’s nothing much to worry about. But does it really?

If it on the other hand reflects green new deal-driven supply shortages, or shortages for other reasons, we may face some hiccups… (such as depressed spending and production growth). (…)

FYI: Evergrande has presold 1.4 million apartments, yet unfinished ($200B).

Natural-Gas Prices Surge, and Winter Is Still Months Away The jump in prices is prompting worries about winter shortages and forecasts for the most expensive fuel since frackers flooded the market.

(…) Europe is short of gas and coal and if the wind doesn’t blow, the worst-case scenario could play out: widespread blackouts that force businesses and factories to shut.

The unprecedented energy crunch has been brewing for years, with Europe growing increasingly dependent on intermittent sources of energy such as wind and solar while investments in fossil fuels declined. Environmental policy has also pushed some countries to shut their coal and nuclear fleets, reducing the number of power plants that could serve as back-up in times of shortages. (…)

“It will be expensive for consumers, it will be expensive for big energy users,” Dermot Nolan, a former chief executive officer of U.K. energy regulator Ofgem, said in a Bloomberg TV interview. (…)

Europe’s gas prices have more than tripled this year as top supplier Russia has been curbing the additional deliveries the continent needs to refill its depleted storage sites after a cold winter last year. (…)

Higher gas prices boosted the cost of producing electricity as renewables faltered. Low wind speeds forced European utilities to burn expensive coal, depleting stockpiles of the dirtiest of fossil fuels. Energy policy also played a role, with the cost of polluting in the European Union surging more than 80% this year.

“Gas supply is short, coal supply is short and renewables aren’t going great, so we are now in this crazy situation,” said Dale Hazelton, head of thermal coal at Wood Mackenzie Ltd. “Coal companies just don’t have supply available, they can’t get the equipment, the manufacturers are backed up and they don’t really want to invest.” (…)

“If we end up having a very cold winter in Asia as well as in Europe, then we may end up seeing a ridiculous spike in gas prices.” (…)

Europe will need to curtail demand if the winter is cold, Goldman Sachs Group Inc. said, predicting the region will face blackouts. (…)

Supplies are unlikely to improve significantly any time soon. Russia is facing an energy crunch of its own and Gazprom is directing its additional production to domestic inventories. Prices could stay high even if Europe ends up with a mild winter, said Fabian Ronningen, an analyst at energy consultant Rystad Energy AS. (…)

- A doubling of energy prices in Europe plus the U.K. would cost consumers an extra 128 billion euros a year, equivalent to $150.6 billion, according to research by SEB. Energy makes up 9.5% of the basket of goods and services in a key eurozone inflation measure. (WSJ)

EARNINGS WATCH

While we await the start of the Q3 earnings season, we are monitoring trends in pre-announcements. In total, guidance so far looks ok, in fact somewhat better than Q2 at the same time with 3 fewer negatives.

The glass half empty view is that 10 fewer companies have updated their guidance and 65 are positive or in line, down from 72 at the same time in Q2. In the last week, 4 S&P 500 companies pre-announced, 1 positive, 3 negatives.

The combination of a slowing economy and rising inflation is making analysts more cautious on their earnings forecasts:

Amid COVID surge, states that cut benefits still see no hiring boost

New state-level data released Friday by the Bureau of Labor Statistics showed the group of mostly Republican led states that dropped a $300 weekly unemployment benefit over the summer added jobs in August at less than half the pace of states that retained the benefits. (…)

But some of those same states, notably Florida and Texas, are also hotbeds of opposition to government health mandates like mask wearing, and the surge of infections there in July and August appeared to dent hiring across the sorts of “close contact” businesses that have suffered most during the health crisis and had begun to recover quickly.

Overall employment in the leisure and hospitality fell about 0.5% in the 26 states that ended benefits, and rose 1% elsewhere. (…)

Economists analyzing the unemployment issue have seen little evidence yet that cutting off the benefits has provided a clear boost to local labor markets, in part because of difficulties separating the influence of the payments from larger shifts in the labor force, or of the potentially offsetting damage done by the pandemic. (…)

“The behavioral response to UI-benefit expiration remains highly uncertain due to the unprecedented size of the benefit swings and the highly unusual economic and health situation,” Goldman economist Joseph Briggs wrote on Friday.

Americans Haven’t Been This Down on Housing Market Since 1982

The share of people who think now is a good time to buy a home fell in September to 29%, extending the plunge from March when the proportion was more than twice as high, data from the University of Michigan consumer sentiment survey showed Friday. It’s also the smallest chunk of respondents since 1982.

Back then, the average for a 30-year fixed rate mortgage topped 15%. That compares with today’s 2.86% rate, according to Freddie Mac. (…)

Honda Says Japan Output 60% Below Plan on Parts Shortage The Japanese automaker expects the impact to extend beyond this month and said the level of operations in early October will be about 70% of its initial plan, according to a statement on its website that notes the estimates are as of Sept. 14. The announcement comes as its bigger rival Toyota Motor Corp. on Friday outlined plans to shutter factories in October. It said 27 out of 28 lines in all of its 14 plants in Japan would face suspensions of as many as 11 days.

(…) As the semiconductor crunch persists, automakers are building closer ties with chip companies such as Intel Corp., Qualcomm Inc. and Nvidia Corp. to monitor supply.

U.S. production of new vehicles this fall will continue to be constrained by the chip shortage and the spread of Covid-19 in Southeast Asia. On Thursday, IHS Markit slashed its vehicle production forecast for this year by 6.2%, or 5.02 million vehicles, the biggest decrease to the outlook since the chip shortage emerged.

FDA panel votes against Pfizer’s Covid-19 booster jab application Advisory committee endorses third dose only for elderly and at-risk groups in blow to Biden

- Bad Advice on Covid Vaccine Boosters The FDA’s advisory panel downplays growing evidence of waning antibodies.

From the WSJ editorial board:

(…) The evidence for boosters is strong and growing. The most compelling comes from Israel, which started giving third doses in July after infections and hospitalizations started climbing among people who were vaccinated this winter. One study from Israel found that the Pfizer vaccine’s protection against symptomatic infection had fallen to 40% from mid-June to July compared to more than 95% from January to April. Those who were vaccinated in January had only 16% protection compared to 79% for those vaccinated in April. (…)

A study from the Kaiser Permanente Southern California health system found that vaccine efficacy against infection declined from 88% in the first month after full vaccination to 47% after five or more months.

Some evidence suggests that protection against severe illness is declining too. A study published by the Centers for Disease Control and Prevention on Friday found that the Pfizer vaccine was 77% effective against hospitalization after four months versus 91% within the first 120 days.

It’s true that the evidence for boosters is stronger for older Americans who generate lower levels of antibodies after the first two doses and are at higher risk for severe illness. Pfizer’s studies showed a third dose boosted antibody counts for those over age 65 by 12-fold compared to one month after the second dose, while increasing five-fold for younger adults. A new study in the New England Journal of Medicine this week from Israel found that a third shot reduced the risk of infection for those over 60 by 11-fold and severe illness by 20-fold.

Some on the FDA advisory panel opposed boosters on grounds that the initial shots still offer sufficiently high levels of protection against severe illness for younger Americans. But many people under age 65 are still getting severely ill even if they aren’t hospitalized. Pfizer says the side effects from a third dose are no greater than for the second. (…)

By the way, the U.S. government is paying only about $20 for a vaccine dose compared to $2,100 for a monoclonal antibody treatment for somebody who gets sick. The economic cost-benefit seems to favor boosters. (…)

- Health Experts Urge Patience on Wider Use of Covid-19 Booster Shots Dr. Anthony Fauci and the director of the National Institutes of Health, Dr. Francis Collins, expect broader approval of the extra injections in the coming weeks.