U.S. Jobless Claims Fall Sharply Filings for unemployment benefits in the U.S. fell to a pandemic low of 310,000 last week after trending near pandemic lows since mid-July.

The four-week moving average, which smooths out weekly volatility in the data, fell to 339,500, also a pandemic low. (…) While claims are down sharply from levels earlier this year, they remain nearly 100,000 above their pre-pandemic trend. Weekly claims averaged 218,000 in 2019. More broadly, the economy had roughly 5.3 million fewer jobs in August compared with the pandemic’s onset in February 2020. (…)

Sept. 6 marked the expiration of enhanced unemployment benefits for many Americans, such as a $300 weekly supplement to regular state benefits that was included in government pandemic aid. About half of U.S. states had opted to end their participation earlier this summer. So far, states aren’t taking the Biden administration up on the extension option, Oxford Economics said in a client note Thursday.

States that ended the programs early have so far seen about the same rate of job growth as those that didn’t.

Details from Haver Analytics:

Initial claims for the federal Pandemic Unemployment Assistance (PUA) program in the week ended September 4 declined 6,323 to 96,198, the lowest level in five weeks. The PUA program provides benefits to individuals who are not eligible for regular state unemployment insurance benefits, such as the self-employed. Given the brief history of this program, these and other COVID-related series are not seasonally adjusted.

Continued weeks claimed for regular state unemployment insurance fell to 2.783 million (-79.4% y/y) in the week ended August 28 from 2.805 million in the prior week, revised from 2.748 million. This was also the lowest level of continuing claims since the beginning of the pandemic. The associated rate of insured unemployment held steady at 2.0%, the pandemic low.

Continued weeks claimed in the PUA program, lagged an additional week, were 5.091 million in the August 22 week, down by two-thirds y/y. Continued weeks claimed for Pandemic Emergency Unemployment Compensation (PEUC) increased 7,646 to 3.808 million. This program covers people who have exhausted their state unemployment insurance benefits.

In the week ended August 21, the total number of all state, federal, PUA and PEUC continued claims was 11.930 million, down 255,757 from the prior week. These claims averaged 11.987 million over four weeks ended August 21. These figures are not seasonally adjusted.

From Bespoke:

One other interesting point to note on this week’s claims data was the impact of Hurricane Ida. Regular state claims fell by 8K nationally on a non-seasonally adjusted basis this week, and that count would have been much better without the epicenter of recent hurricane news: Louisiana. With the state still recovering from the storm, claims more than quadrupled this week. In fact, the increase was even larger than that of the most populous state, California, which saw claims rise by 5.6K.

(Bespoke)

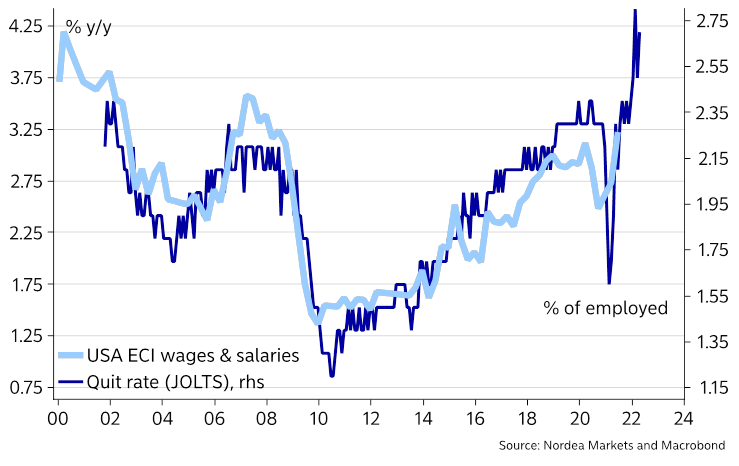

Atlanta Fed’s Wage Growth Tracker Was 3.9 Percent in August, from 3.6% in July and 3.4% in January.

- Hourly wages are up 4.1%, from 3.9% and 3.5% respectively.

- Services wages: +4.0%, from 3.6% and 3.7% respectively.

- Job switchers: +4.8% vs +3.3% for job stayers.

![]()

BMO’s CEO Says Businesses Seeing Strong Demand, Pricing Power

Bank of Montreal Chief Executive Officer Darryl White said the lender’s business clients in both the U.S. and Canada are seeing demand pick up, but are still struggling with rising costs and supply constraints.

“They’re seeing an interesting and very helpful demand increase for their products and services,” White said Thursday at the Scotiabank Financials Summit. “They’re having a reasonably — I won’t say easy — but a facilitative time in terms of driving price increases for their own products and services.” (…)

Fed Officials Prepare for November Reduction in Bond Buying Phasing out the Fed’s pandemic-era stimulus by the middle of 2022 could clear the path for an interest-rate increase

(…) Mr. Powell said in a recent speech that at their July meeting, he believed that “if the economy evolved broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year.” New York Fed President John Williams, a top ally of Mr. Powell’s, made a nearly identical statement during a virtual appearance on Wednesday. (…)

Mr. Williams told reporters Wednesday that while the pandemic was likely a factor in a hiring slowdown last month, he said the overall path of employment gains this year has been sturdy. He said he is more focused on overall hiring this year than on monthly fluctuations, a sign that the August job figures wouldn’t alter plans to taper in November. “Some months come in stronger, some not so strong—it’s really about the accumulation,” he said. (…)

- ECB Sticks With Easy-Money Policies to Counter Delta’s Impact European Central Bank President Christine Lagarde signaled that the bank will keep monetary policy loose for some time amid a resurgence in Covid-19 cases globally and signs of economic slowdown in China and the U.S. that have prompted caution from the Federal Reserve. While the ECB said it would slightly scale back its massive bond-buying program to reflect brighter prospects for the eurozone economy, Ms. Lagarde emphasized at a news conference that the decision didn’t constitute a plan to reverse its easy-money policies.

- John Authers:

(…) the ECB’s inflation projections are rising, which implies that it will be more aggressive about tapering. The ECB also increased its growth projections, which on the face of it would also imply that it is time to taper. Lagarde conceded that inflationary pressures look more durable than they did earlier this year — which in itself sounds a little hawkish.

However, Lagarde continues to say she is confident that the current inflation is driven by transitory bottlenecks, and the market evidently attached lot of importance to that. Further, growth is still expected to regress to an anemic 2.1% in 2023, when inflation is projected to be 1.5% on both a headline and a core basis — not remotely the kind of projection to worry anyone, and indeed a justification for continuing to juice the market with asset purchases. (…)

That is how the lady managed to taper without the faintest sign of a tantrum. It has been achieved with a slight strengthening of the euro compared to the dollar. The fact that she has done this probably makes it a little easier for the Fed to start to taper sooner rather than later — although the inflation data over the next week, starting with producer prices on Friday, will be rather more important. And even if the central banks have avoided the mistake of eight years ago, there remains the risk that they will commit a new one.

In a speech Thursday a day after a stand-pat decision, Governor Tiff Macklem provided details on what he called the central bank’s “monetary policy for the recovery.” Macklem reiterated the bank intends to bring its bond purchases to a roughly neutral pace where holdings and stimulus levels remain stable, and keep it there for a “period of time” before it begins withdrawing extraordinary support from the economy.

And when policy makers start paring back that stimulus, the first move will be to increase the central bank’s policy interest rate rather than reducing bond holdings, Macklem said.

“When we need to reduce the amount of monetary stimulus, you can expect us to begin by raising our policy interest rate,” Macklem said in remarks prepared for a virtual speech to the Quebec chamber of commerce. “What this all means is it is reasonable to expect that when we reach the reinvestment phase, we will remain there for a period of time, at least until we raise the policy interest rate.”’ (…)

Toyota Cuts Production Forecast by 300,000 Cars on Covid Hit

Toyota Motor Corp. trimmed its production outlook for this year by about 3% because the spread of the coronavirus in Southeast Asia has disrupted access to semiconductors and other key parts.

The world’s No. 1 automaker, which is adjusting output in September and October, now expects to produce 9 million vehicles in the fiscal year through March, down from 9.3 million previously forecast. The company is sticking to its forecast for operating profit of 2.5 trillion yen ($22.7 billion) this year, factoring in the potential to reduce costs. (…)

Covid continues to impact suppliers in Southeast Asia, Toyota Chief Purchasing Group Officer Kazunari Kumakura said Friday. Though the automaker is also being impacted by the industrywide shortage of semiconductors, the spread of Covid is the “overwhelming” reason for the most recent planned cuts, he said. (…)

Airlines Warn of Dimming Outlook Amid Delta Variant United, Southwest, American Airlines and others said a surge in Covid-19 cases has hampered travel demand, a trend that is stymieing hopes for a speedy airline recovery.

(…) A pickup in business travel that took root over the summer has stalled, airline executives said Thursday. Airlines had been counting on offices to reopen, bringing business travelers back out this fall when summer vacation traffic typically slows down. But many large companies are now delaying returns to the workplace, in some cases through the rest of the year. (…)

“It’s probably about a 90-day pause in return to travel for that next leg up that we were expecting to see, but it’s coming,” [Delta’s] Mr. Bastian said.

United no longer expects to report an adjusted pretax profit this quarter, and said it will likely lose money in the fourth quarter if current trends continue. The airline now says its total third-quarter revenue will be 33% lower than it was two years ago. (…)

Carriers said that the recent traffic declines are smaller than the sharp drops during previous spikes in Covid-19 cases. The number of people passing through U.S. airports on peak days over the Labor Day holiday weekend neared highs seen earlier this summer, and some airlines said that winter holiday bookings appear to be on track.

Airlines are still bringing on the thousands of workers they would need to meet another travel surge next summer, after many carriers were caught flat-footed when travel rebounded this year. (…)

Oil Prices Fall After China Says It Plans to Release Stockpiles The move adds to pressures swaying the oil market, including worries that the recent rise in cases of the Delta variant of the Covid-19 virus will hurt demand and dent the 2021 rebound in prices.

Macro Conditions Deteriorate as Bear Market Probability Rises

Macro Conditions Deteriorate as Bear Market Probability Rises

SentimenTrader’s warning comes along with many big brokerage firms, uncharacteristically, also warning of a correction.

(…) To differentiate temporary slowdowns from real problems, we look for significant macro deterioration. The Macro Index Model combines 11 diverse indicators to determine the state of the U.S. economy.

Macro Index Model Inputs

- New Home Sales

- Housing Starts

- Building Permits

- Initial Claims

- Continued Claims

- Heavy Truck Sales

- 10 year – 3 month Treasury yield curve

- S&P 500 vs. its 10-month moving average

- ISM manufacturing PMI

- Margin debt

- Year-over-year headline inflation

This index leans towards housing and labor markets. Housing indicators are extremely useful as leading economic indicators and labor market indicators are very timely for calling recessions, with few false signals. Stock market investors should be bullish when the Macro Index is above 0.7 and bearish when the Macro Index is below or equal to 0.7.

Once the final reports were in for August, the model plunged below 46%, the 2nd-lowest reading of the past decade.

At the same time, the Bear Market Probability Model has jumped again. This is a model outlined by Goldman Sachs using five fundamental inputs.

Bear Market Probability Model Inputs

- The U.S. Unemployment Rate

- ISM Manufacturing Index

- Yield Curve

- Inflation Rate

- P/E Ratio

Each month’s reading is ranked versus all other historical readings and assigned a score. The higher the score, the higher the probability of a bear market in the months ahead. Last May, the model was in the bottom 10% of all months since 1950. This month, it jumped into the top 10% of all months.

There is some overlap between the two models, with a correlation of +0.25 (out of a scale from -1.0 to +1.0) since 1968. However, it’s still rare to see both of them at such extremes at the same time.

The chart below shows the spread between the Bear Market Probability and Macro Index models. The higher the spread, the higher the probability of a bear market combined with poor macro conditions.

The chart shows that the S&P 500’s annualized return is a horrid -17.6% when the spread is above 20% like it is now. The table below shows forward returns in the S&P after the spread crosses above +20% for the first time in at least a year.

Looking at the Risk/Reward Table, it was ugly across most time frames up to two years later.

E Pluribus Unum

From Axios’ Mike Allen:

Top Republicans are calling for a public uprising to protest President Biden’s broad vaccine mandates, eight months after more than 500 people stormed the U.S. Capitol to try to overturn the election.

It has been decades since America has witnessed such blatant and sustained calls for mass civil disobedience against the U.S. government.

J.D. Vance — author of “Hillbilly Elegy” and a candidate for the GOP U.S. Senate nomination in Ohio — urged “mass civil disobedience” to Biden’s plan to use federal authority to mandate vaccination for roughly two-third of America workers.

“I have a simple message for America’s business community,” Vance wrote. “DO NOT COMPLY.”

Several Republican governors say they’ll go to court to try to stop the mandate for federal employees, contractors and private employers with 100+ workers (enforced by OSHA).

South Dakota Gov. Kristi Noem told Sean Hannity on Fox News: “In South Dakota, we’re going to be free. … We will take action. My legal team is already working.”

A top House Republican aide tells me: “Every Republican in the country — especially those running to the right in primaries — is salivating over Joe Biden [igniting] the vax debate.”

“Republicans think that he’s made even pro-vax conservatives into ‘anti-vax mandate’ Americans.” (…)

Invoking a civil-rights parallel, the official added: “Basically Biden is staring down Southern governors (and some Northern allies). … Is America divided? Yes. But Biden is uniting the 75% vs. the 25% that is in opposition.”

The official’s bottom line: “That is unity politics in a divided nation — unifying the overwhelming majority threatened by an unruly minority.”

Act fast or miss the digital payments boat, BIS tells central banks

China Needs to Regulate Its AI Giants, Tech Watchdog Says

China should regulate the use of artificial intelligence to curb risks posed by the growing use of the technology, a senior government official said Friday.

Protecting national security as well as users’ interests and privacy should remain paramount as the adoption of AI rises, said Zhao Zeliang, deputy director of Cyberspace Administration of China, the internet industry overseer.

“Like other things, AI can bring negative affects too,” he said at a media event in Beijing. Regulating the AI industry “is as important as developing it.” (…)

")