U.S. JOLTS: Job Openings Surge to Record Level in July

The Bureau of Labor Statistics reported that on the last business day of July, the level of job openings rose 7.4% m/m (62.8% y/y) to a record 10.93 million from 10.19 million in June, revised from 10.07 million. The total job openings rate surged to a record 6.9% from an unrevised 6.5% in June. The job openings rate is calculated as job openings as a percent of total employment plus jobs that have not yet been filled. The level of hiring fell 2.3% (+6.9% y/y) as the hiring rate declined to 4.5% in July from 4.7% in June, revised from 4.6%. Despite the decline, the rate was higher than the 3.8% low this past January. The overall layoff & discharge rate rose slightly to 1.0% in July from the record low of 0.9% in both May and June. The quits rate held at 2.7%, remaining above a low of 1.6% in April 2020.

The private-sector job openings rate also strengthened to a record 7.3% in July from 6.9% in June. It was increased from 3.6% April 2020. The leisure & hospitality rate surged to a record 10.7% in July while the professional & business services rate reached a record 8.1%. The factory sector job openings rate held at the record 6.7% in July while the education & health services rate jumped to a series high of 7.7%. The construction sector rate in July eased m/m to 4.2% and has moved sideways since March. The government sector job openings rate rose sharply in July to a record 4.6. The private sector job openings level rose 7.1% to 9.88 million, up roughly two-thirds y/y.

Finding workers to fill job openings remained difficult in July. The private sector hiring rate fell to 4.9% from 5.2% in June, though it remained up from January’s 4.2% low. It remained well below the record 7.2% in May of last year. The level of private sector hiring declined 3.6% in July (+4.6% y/y) to 6.17 million. (…)

Workers continue to look for new job opportunities. The private sector 3.1% quits rate in July equaled the record high. It modestly increased m/m and remained well above 2.6% in January. The rate has been trending higher since the low of 1.8% in the spring of 2020 and compared to 0.7% in government. The July level of job quits in the private sector increased roughly one-third y/y. In government, the level of quits fell 34.1% y/y.

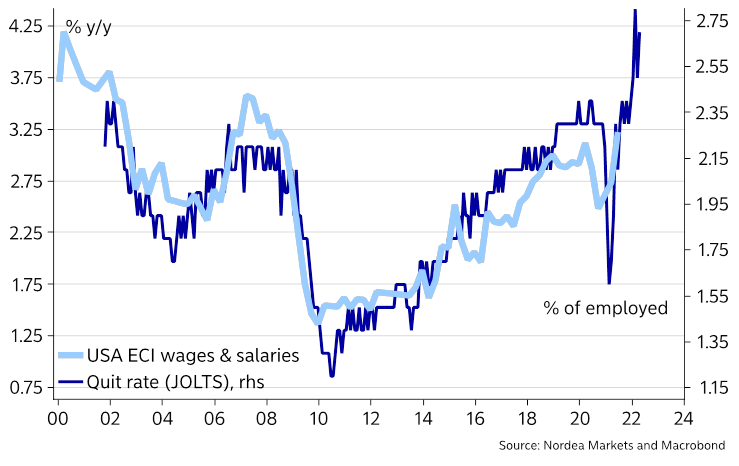

Wage growth is coming!

ING:

OK, this is for July, and some of the vacancies may have disappeared in August given the softening in activity in the wake of Covid-19 resurgence, but this report still suggests the appetite to hire is incredibly strong. This was affirmed in the August NFIB small business employment data showing a net 50% of small firms have vacancies they can’t fill – an all-time high just like today’s job opening number.

The quit rate – the proportion of private sectors workers quitting their job to move to another – rose back to match the all-time high of 3.1% for the series that goes back 20 years. This can indicate wage pressures as we assume that if the quit rate is on the rise, firms no longer think purely about having to raise pay to attract staff but also need to consider raising pay for staff retention purposes.

Interestingly for the leisure and hospitality industry, it actually dropped back a touch, but for most other industries, it is on a clear upward path, especially in construction, manufacturing and wholesale & retail trade. (…)

US quit rate – the proportion of workers quitting their job to move to a new employer

U.S. Economic Growth Slowed Over the Summer Due to Delta Variant, Fed’s Beige Book Says Report on economic activity cited a widespread pullback in dining out, travel and tourism related to latest Covid-19 surge

(…) Many respondents told the Fed that shipping delays and higher freight costs have harmed their businesses. (…)

Firms also continued to struggle with finding workers, prompting many to raise wages and offer more-flexible schedules. A trucking company in the Cleveland area said it had already offered five wage increases so far this year.

Those problems have pushed up prices. Many respondents to the Fed survey said they “anticipate significant hikes in their selling prices in the months ahead.” (…)

The actual Beige Book wording:

With persistent and extensive labor shortages, a number of Districts reported an acceleration in wages, and most characterized wage growth as strong—including all of the midwestern and western regions. Several Districts noted particularly brisk wage gains among lower-wage workers. Employers were reported to be using more frequent raises, bonuses, training, and flexible work arrangements to attract and retain workers.

- Fauci to Axios: COVID infections are 10x too high

Americans are getting infected with COVID at 10 times the rate needed to end the pandemic, Anthony Fauci tells Axios’ Eileen Drage O’Reilly.

The longer it takes to end this pandemic phase, the bigger the chance we’ll end up with a “monster variant” that is both dangerously transmissible and eludes vaccines.

“[W]e’re still in pandemic mode, because we have 160,000 new infections a day,” Fauci said. “That’s not even modestly good control.”

“In a country of our size, you can’t be hanging around and having 100,000 infections a day,” he continued. “You’ve got to get well below 10,000 before you start feeling comfortable.”

More from Axios:

The U.S. is averaging 1,500 deaths a day for the first time since March, Axios health care editor Tina Reed writes.

Daily death totals have more than quintupled since the start of August, The New York Times calculates.

Kids now make up more than a quarter (26.9%) of new weekly COVID cases nationwide, according to the American Academy of Pediatrics.

Homebuilder Comments in August: “Supply shortages are getting worse.”

Bank of Canada Maintains Bond Buying, Sees Second-Half Rebound

In a statement Wednesday from Ottawa, policy makers left their key interest rate at a historic low and maintained the current pace of bond purchases, but reiterated expectations that growth will accelerate in the second half of this year

The cautiously optimistic tone suggests policy makers led by Governor Tiff Macklem are unfazed by weaker than expected economic activity data last week that has cast some doubt over the pace of the recovery. (…)

The Bank of Canada has been taking steps to gradually return to more normal policy, reducing its asset purchase program three times since the end of last year. (…)

The Bank of Canada has said it will bring net purchases of bonds to zero before it starts to consider raising its policy rate, with swaps trading suggesting that investors are pricing in a 100% chance of a hike over the next 12 months. Three rate hikes over the next two years are fully priced in, which would leave Canada with the highest policy rate among Group of Seven economies. (…)

")

Inflation splits emerging countries into doves and hawks More than in the developed world, rising prices already pose a real threat to stability

China Tells Gaming Firms to End ‘Solitary’ Focus on Profit Chinese regulators summoned gaming companies including Tencent Holdings Ltd. and Netease Inc. to discuss further oversight of the industry and the need to deemphasize profits, prompting a steep share selloff.

(…) The agencies told the companies they must enforce the new regulations and break from “the solitary focus of pursuing profit” to prevent minors from becoming addicted to games. They should also remove “obscene and violent content” and avoid “unhealthy tendencies, such as money-worship and effeminacy.”

“The authorities ordered the enterprises and platforms to tighten examination of the contents of their games,” Xinhua said. “The platforms must also resist unfair competition to prevent excessive market concentration or even monopolies in the industry.” (…)

In today’s WSJ:

- How TikTok Serves Up Sex and Drug Videos to Minors An analysis of the videos served to these accounts found that through its powerful algorithms, TikTok can quickly drive minors—among the biggest users of the app—into endless spools of content about sex and drugs.

Chinese authorities are quite busy on many fronts. But front and center is Evergrande as Almost Daily Grant’s explains:

Any Evergrande-led property crack-up could loudly reverberate: Property loans inclusive of mortgages footed to RMB 70 trillion ($10.8 trillion) late last year, representing 39% of total outstanding loans according to the China Banking and Insurance Regulatory Commission. Things are already trending in the wrong direction, as nonperforming real estate loans on the books of China’s five largest banks jumped 30% over the first six months of the year to RMB 97 billion, Nikkei Asia relayed yesterday. Were a crisis to materialize, things could get ugly. Total Chinese bank assets reached $52 trillion as of June 30, upwards of 60% of global nominal GDP last year. (…)

The markets are getting increasingly nervous, as mainland-listed banks now trade at a record low 0.4 times book value, down from 0.75 times book earlier this year and 1.2 times in 2019. Similarly, the Bloomberg Barclays gauge of Chinese dollar-pay high-yield credit has blown out to a 1,256 basis point spread over Treasurys (a 1,000 basis point pickup typically indicates distress). That’s up from less than 800 basis points in early June. (…)

And there’s is this other non-trivial problem: Huarong:

- Huarong’s $3.4 billion Debacle on a South Korean Tourist Trap The undeveloped plot of land bought by the state-owned bad-asset manager is now worth about one-third what it paid, underscoring its woeful history of bribery-fueled investments

- State Giant Citic Throws Stricken Huarong a Lifeline China’s second-biggest financial holding company is leading a bid to pull bad bank back from the brink