Personal Income and Outlays, May 2021

Just out this a.m.:

Expenditures for March and April were revised up. No meaningful slowdown in May, Americans are still spending merrily. The savings rate was 12.4% in May, down from 14.5% in April. Core PCE inflation is 3.4% but last 3 months annualized: +6.6%. Last 2 months: +7.4% a.r.. No base effect there.

More analysis on Monday.

U.S. Initial Unemployment Insurance Claims Edged Down

Initial claims for unemployment insurance fell 7,000 in the week ended June 19 to 411,000 from an upwardly revised 418.000 in the previous week (initially (412,000). The Action Economics Forecast Survey panel expected new claims to decline to 380,000. The 4-week moving average edged up to 397,750 last week from 396,250 the previous week, a pandemic low.

Initial claims for the federal Pandemic Unemployment Assistance (PUA) program rose for the second consecutive week, increasing to 104,682 in the week ended June 19 from a downwardly revised 97,762 in the previous week (initially 118,025). The PUA program provides benefits to individuals who are not eligible for regular state unemployment insurance benefits, such as the self-employed. Given the brief history of this program, these and other COVID-related series are not seasonally adjusted.

Continuing claims for regular state unemployment insurance fell 144,000 to a new pandemic low of 3.390 million in the week ended June 12. The insured rate of unemployment slipped 0.1%-point to 2.4%, also a new pandemic low. This rate reached a high of 15.9% in the week of May 9, 2020.

Continuing claims for PUA fell to 5.950 million in the week ended June 5, the lowest since the week ended April 25, 2020, from 6.126 in the previous week. By contrast, continuing PEUC claims rose to 5.273 million in the week ended June 5 from 5.165 million in the previous week. The Pandemic Emergency Unemployment Compensation (PEUC) program covers people who have exhausted their state unemployment insurance benefits.

The total number of all state, federal, and PUA and PEUC continuing claims was 14.845 million in the week ended June 5, an increase in 3,756 from the previous week. The level of total continuing claims in the week ended May 29 was the lowest since early April 2020. These figures are not seasonally adjusted.

(Bespoke)

(Bespoke)

U.S. inflation likely to remain elevated for up to four years – BofA

BofA expects U.S. inflation to remain elevated for two to four years, against a rising perception of it being transitory, and said that only a financial market crash would prevent central banks from tightening policy in the next six months.

It was “fascinating so many deem inflation as transitory when stimulus, economic growth, asset/commodity/housing inflations (are) deemed permanent”, the investment bank’s top strategist Michael Hartnett said in a note on Friday. (…)

Good read: The Ghost of Arthur Burns along with my own THE INFLATION DEBATE: JFK, LBJ, JOE AND JAY

Related, from Grant’s Interest Rate Observer:

(…) The inflation horse was out of the barn, Martin admitted to his fellow FOMC committeemen in December 1967, and, to complicate matters, to quote Martin’s paraphrased words in the FOMC minutes, “many observers apparently had become convinced that the Committee would not move toward restraint under almost any conditions. The existence of that attitude, particularly abroad, was unfortunate.”

History is only a sometime friend to the forward-looking investor. Its study reveals the constancy of human behavior but also the variety of human experience. The Great Inflation that Martin unwittingly cultivated, and which he failed to prune, was one thing. Today’s pop-up inflation, which Powell is inclined to discount, is something else. Financial circumstances are different. Demographic, geopolitical and policy settings are especially different.

As inflation is unpredictable, we make no attempt to predict it, only to observe that the stars are aligning in a potentially inflationary pattern. From supply chains to globalization, from monetary policy to fiscal policy, from wage rates to the political zeitgeist, the forces of entitlement and demand might be gaining ground on the forces of production and supply.

Assume that what’s supposed to be transitory instead proves persistent. And assume that a stagflationary economy hands the Powell Fed the unwelcome choice of combating joblessness or attacking inflation. What would the FOMC elect to do? The new operating format isn’t much help:

The Committee’s employment and inflation objectives are generally complementary. However, under circumstances in which the Committee judges that the objectives are not complementary, it takes into account the employment shortfalls and inflation deviations and the potentially different time horizons over which employment and inflation are projected to return to levels judged consistent with its mandate.

Which, translated into English, with a little editorial license, means: “Because we control events, we won’t have to make that choice. But if we did, we would favor employment over price stability because, after all, we want to promote a higher rate of inflation to compensate for the embarrassing post-2008 decade in which the core PCE never got to 2%. Besides, we have the tools to reverse any unwanted deviation from 2%.” (…)

Drought indicators in Western U.S. flash warnings of the “big one.” Summer in the U.S. begins with widespread drought already at historic levels across 11 states. Experts warn of worsening conditions once wildfires start.

(…) Swain terms this process the aridification of the West—a complete shift in the region’s climate. “It is hard to call it drought anymore because it is a permanent state of being,” he says. “Things are moving in one direction rather than going back and forth.” (…)

The pressure is mounting on agriculture, which consumes 80% of California’s water. California’s Central Valley alone accounts for 17% of all irrigated land in the U.S. But the problem reaches far beyond the Golden State. (…)

FedEx shares fall as labor woes weigh on 2022 outlook

Shares in U.S. delivery firm FedEx Corp (FDX.N) shed more than 4% on Thursday after hiring difficulties tempered its 2022 earnings forecast that missed Wall Street expectations.

FedEx founder and CEO Fred Smith told analysts that operations at the Memphis-based company are being crimped by an inability to find enough workers.

Widespread labor shortages are hitting FedEx in the form of “higher wage rates and lower productivity, particularly in the (current fiscal) first quarter, and this is reflected in our overall outlook for the year,” Chief Financial Officer Mike Lenz said.

FedEx expects 2022 earnings, excluding some items, of $18.90 to $19.90 per share – less than analysts’ average estimate of $20.37, according to Refinitiv data. That sent its shares down $13.31 to $290.38 in extended trading. (…)

The pandemic created so much demand for package delivery and freight services that FedEx and rival United Parcel Service Inc (UPS.N) are turning away some business.

That means customers are less likely to push back when the carriers raise fees and add surcharges, said Edward Jones analyst Matt Arnold.

Still, Arnold said labor could continue to be an issue going into the holidays. (…)

Biden, Senators Agree to $1 Trillion Infrastructure Plan President Biden and a group of senators agreed to a roughly $1 trillion infrastructure plan, securing a long-sought bipartisan deal that lawmakers and the White House will now attempt to shepherd through a closely divided Congress.

While the latest deal falls far short of what the White House and progressives want to see in a broader economic agenda, most of the remaining priorities — including spending related to the environment, child care and elder care — may move through Congress in the legislative vehicle of budget reconciliation. That will let Democrats bypass Republican support, assuming the party remains unified in its thin majorities. (…)

Thursday’s agreement lists a hodgepodge of sources for funding the infrastructure spending while steering clear of raising taxes — something Republicans made clear was a red line. They range from repurposing other pandemic relief funds to investing in tougher Internal Revenue Service tax collection and selling oil from the Strategic Petroleum Reserve.

The plan avoids an increase in the 18.4-cents-per-gallon federal gas tax that infrastructure supporters have sought to provide a dedicated funding source for long-range construction projects.

Biden’s proposals to raise taxes on corporations and high-earning Americans remain firmly on the table, however. The administration is likely counting on most of its suite of tax proposals ending up in the reconciliation legislation, providing financing for the trillions in social spending that the bill is expected to include.

Companies drop plans to sublease space as more workers want to return to the office

TMX Group, Intelex Technologies Inc. and other companies trying to get rid of their downtown Toronto office space are reversing course, anticipating more of their employees will return to the workplace after more than a year at home. (…)

Downtown Toronto’s office vacancy rate was nearly 10 per cent at the end of March, the highest level since the global financial crisis, due to many companies trying to sublease some of their space.

Now some are rethinking those plans and taking space off the market as employees report they want to return to the office, at least for a few days a week.

“A lot of them have decided that they need an office presence and that is what is driving some of the decisions,” said Juana Ross, Toronto market research director for Cushman & Wakefield, a commercial real estate company. (…)

Space available to sublet, which is included in calculating the office vacancy rate, is declining, according to commercial real estate company Avison Young. (…)

Banks Pass the Fed’s Stress Tests. It’s Buyback Time.

Spac boom is creating ‘castles in the sky’, Jim Chanos warns Veteran short seller is betting against some Spac companies as market draws scrutiny from regulators

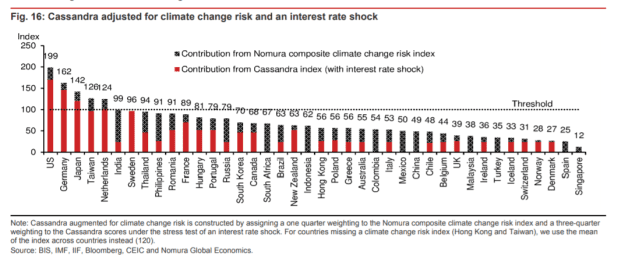

The U.S. is the country most vulnerable to a new financial crisis, Nomura warns

(…) The Singapore-based economics research team at Nomura built a model around five different early warning signs: the ratio of private credit to GDP, the debt service ratio, real equity prices, real property prices and the real effective exchange rate. Nomura says Cassandra correctly signalled two-thirds of the past 53 crises in 40 countries since the early 1990s, and it is currently warning that six economies – the U.S., Japan, Germany, Taiwan, Sweden and Netherlands – appear vulnerable to financial crises over the next 12 quarters.

Nomura also tested for interest-rate and climate change risk — and adding those to the model, the overall scores rose but the number of countries at the threshold to crisis vulnerability actually fell, as Sweden would drop out.

“I’m totally screwed.” WD My Book Live users wake up to find their data deleted Storage-device maker advises customers to unplug My Book Lives from the Internet ASAP.

Western Digital, maker of the popular My Disk external hard drives, is recommending customers unplug My Book Live storage devices from the Internet until further notice while company engineers investigate unexplained compromises that have completely wiped data from devices around the world.

The mass incidents of disk wiping came to light in this thread on Western Digital’s support forum. So far, there are no reports of deleted data later being restored. (…)

The My Book is a popular storage device for consumers and businesses. It plugs into computers, typically through USB. The affected model here, known as My Book Live, uses an ethernet cable to connect to a local network. From there, users can remotely access their files and make configuration changes through Western Digital cloud infrastructure. Western Digital stopped supporting the My Book Live in 2015. The support forum thread was first reported by Bleeping Computer.

On its website, Western Digital advised customers to disconnect their My Book Live devices to prevent further attacks while the company investigates the mass wiping. (…)

Scary stuff, particularly for the Internet Of Things industry.

")

")