Fed on Track for Rate-Hike Downshift After Cool Inflation Data

(…) Consumer prices rose 6.5% in the 12 months through December, marking the slowest inflation rate in more than a year. So-called core inflation, which excludes food and energy, was up 5.7% over the same period, the smallest advance in a year. Both figures matched median forecasts. (…)

Stripping out energy, rent and owners’ equivalent rent, services prices were up 0.3% last month, according to Bloomberg calculations. Removing medical care as well — an adjustment that helps offset a quirk in the CPI’s calculation of health insurance — services prices were up by a similar amount. (…)

Shelter costs — which are the biggest services component and make up about a third of the overall CPI index — increased 0.8% last month, an acceleration from November. Rents and owners’ equivalent rent both rose by the same amount, while hotel stays advanced 1.5% after falling in the prior month. (…)

Excluding food and energy, goods prices fell 0.3%, led by used cars. Gasoline prices dropped 9.4%, “by far” the largest contributor to the decrease in the headline figure, the Labor Department said. (…)

Pundits now break down the CPI into myriads of components trying to prove a point. Let’s se if we can find a good key:

- Core CPI: last 3 months: +3.2% a.r.; last 2 months: +3.0%. December: +3.6% a.r.

- Core CPI less shelter: last 3 months: -1.2% a.r.; last 2 months: -1.2%. December: -1.2% a.r.

- Core goods: last 3 months: -4.8% a.r.; last 2 months: -4.8%. December: -3.6% a.r.

- Services: last 3 months: +5.4% a.r.; last 2 months: +5.7%. December: +7.2% a.r.

- Services less shelter: last 3 months: +0.9% a.r.; last 2 months: +1.3%. December: +2.8% a.r.

- Median CPI: last 3 months: +5.6% a.r.; last 2 months: +5.4%. December: +4.8% a.r.

- 15 trimmed mean: last 3 months: +4.0% a.r.; last 2 months: +3.6%. December: +4.8% a.r.

If one really sees shelter inflation recede in 2023, CPI less shelter and Services les shelter are “mission accomplished”.

But “CPI-rent of shelter” inflation accelerated +0.8% in December after +0.6% in November and +0.7% in October despite the widely mediatized weakness in the new rental market.

Various recent research papers by the San Fran Fed and the Cleveland Fed suggest 9 to 12 months lags between new tenant-rent and all-tenant-rent.

The San Fran Fed finds a close relationship between rent inflation and unemployment which has yet to turn up, suggesting that rent inflation will stay high for a while.

Rent inflation correlates strongly with inverse of unemployment

I find as good, if not a better, relationship with wages. After all, people pay what they can, not what they want. But there have been significant lags in the past:

Not a slam dunk to be taken to the bank just yet…

We still aren’t below the 0.17% month-on-month threshold that over time would get us to the Fed’s 2% YoY target, but the last three months of data are a notable step down from the 0.5-0.6% MoM average seen through the second and third quarters of 2022, giving the Fed justification to raise rates by 25bp from now on.

Core MoM inflation readings and the key 0.17% MoM threshold to get to 2%. (ING)

Source: Macrobond, ING

-

NFIB survey points to steep decline in core inflation pressures over the summer

Source: Macrobond, ING

From my lens, services inflation remains the key: last 3 months: +5.4% a.r.; last 2 months: +5.7%. December: +7.2% a.r..

From John Authers today:

Even with accommodation costs excluded, services inflation is uncomfortably high and only just below its peak. Transport appears to be the biggest problem now:

The Cleveland Fed published a daily “Inflation Nowcast”. As of mid-January, it sees core CPI up 0.46% MoM (+5.6% a.r.) vs +0.30% (+3.6%) in December. If so, the January YoY increase would be 5.6% vs 5.7% in December.

Inflation readings now need to focus on 2 different issues: the impact on monetary policy and the impact on consumer spending, not necessarily in sync nowadays.

My CPI- Essentials index (blue bar: food+ energy+ shelter, weighted) has sharply decelerated after severely squeezing consumers between June 2021 and June 2022 as all 3 components exploded. In the last 6 months, inflation on essentials rose 3.2% annualized, +2.5% in the last 2 months, thanks to much lower pressures from food (red) and energy which have offset the acceleration in shelter costs.

This is helping consumers since these costs cannot be easily mitigated. With wages rising 5-6%, real discretionary income is not eroding like during the first half of the year.

The very mild winter in North America and Europe could keep energy prices in check for a while longer. Food commodities are also weakening.

With the recent slowing in wage growth, lower energy prices should normally translate in slower services inflation in coming months.

Meanwhile, goods inflation will keep declining for a while longer:

-

Tesla Cuts Prices Across Models Sold in U.S. The car maker cut prices for some of its vehicles sold in the U.S. by nearly 20%, aiming to lure new buyers at a time when Wall Street is concerned appetite for its cars is weakening.

Tesla also cut prices in Europe.

Also: Data: Cox Automotive; Chart: Axios Visuals

Data: Cox Automotive; Chart: Axios Visuals

- The market is pricing the probability of a 25-bps hike hit almost 93%. @NickTimiraos says 25bps is coming.

FYI from @charliebilello

-

The US Budget Deficit is widening again, hitting a 9-month high of $1.419 trillion in December (YoY change).

- The Interest Expense on US Public Debt rose to $775 billion over the past year, a record high. If it continues to increase at the current pace it will soon be the largest line item in the Federal budget, surpassing Social Security.

With a debt ceiling debate coming soon…![]()

China’s Government to Take Golden Shares in Alibaba, Tencent

Chinese government entities are set to take so-called “golden shares” in units of Alibaba Group Holding Ltd. and Tencent Holdings Ltd., suggesting Beijing is moving to ensure greater control over key players in the world’s largest internet arena.

The discussions are emerging as Beijing prepares to loosen its grip on the sector and move past a bruising crackdown that’s enveloped most every internet sphere for well over a year. That share structure, which in theory allows the government to nominate directors or sway important company decisions, could grant officials a tool to influence the industry over the longer term. (…)

“To me, the news is slightly positive,” said Banny Lam, head of research at Ceb International Inv Corp Ltd. “The two have been struggling with the issues of crackdown in recent years. For both Alibaba and Tencent, the government stake could potentially help them to get greenlights to do businesses in new areas and lower the risks of further clampdown by the regulators.” (…)

“A slight positive”? ![]()

China is looking less desirable to investors

Investors are facing a new economic and investing environment this year and determining their revised positions.

- Goldman Sachs’ Investment Strategy Group advised consumer and wealth management clients last month to “carefully reassess their strategic allocation to Chinese assets” as well as “exposure to countries and companies with significant exports to China.”

- JPMorgan’s Asia Pacific Economic Research team yesterday posed 10 broad questions about China in 2023, ranging from the path of reopening to whether policymakers will succeed in their ambition to grow productivity.

“Demographics have deteriorated faster than expected,” while “re-shoring and near-shoring” of manufacturing away from China is picking up momentum, Goldman’s report notes.

- The country’s competitiveness in tech is also expected to be curbed by the U.S.’ export controls on semiconductors, it says.

- And while the country’s reopening has been faster- and earlier-than-expected, the path for recovery in consumer spending is uncertain — “it could be gradual and incomplete,” JPMorgan analysts write.

Investors have already shed their exposure to China.

- In 2022, foreign investors became net sellers of Chinese fixed income and equities for the first time in 10 years, Goldman found.

- In the first nine months of last year, investors outside of China pulled out 27% of the stock of fixed income and 35% of the stock of equities that had been invested over the prior nine years, according to Goldman.

“One of our institutional brokers [today] made a comment that they’re not seeing a lot of these long-only managers coming back into these names — that there’s a lot of this skepticism due to a rough 2021 and 2022,” KraneShares CIO Brendan Ahern said during an investor call this morning.

- Simultaneously, Ahern sees this as an opportunity because “this underweight represents cash on the sidelines” that could provide a boost when moved back into the market.

Ahern and his team still see opportunities in Chinese internet companies, including mobile giant Tencent as well as Alibaba — two of his China Internet ETF’s top holdings.

- “As students of the Chinese markets, we have noticed the tone of policies toward internet companies changing over the last six months,” Ahern told Axios separately after the call.

- “The change in policy is driven by the necessity of raising domestic consumption,” he added.

But with Xi in full charge, I find it interesting to review his record since 2013: I can’t find many great decisions while I see many terrible ones…

Management, management, management!

Now with golden shares…

")

")

")

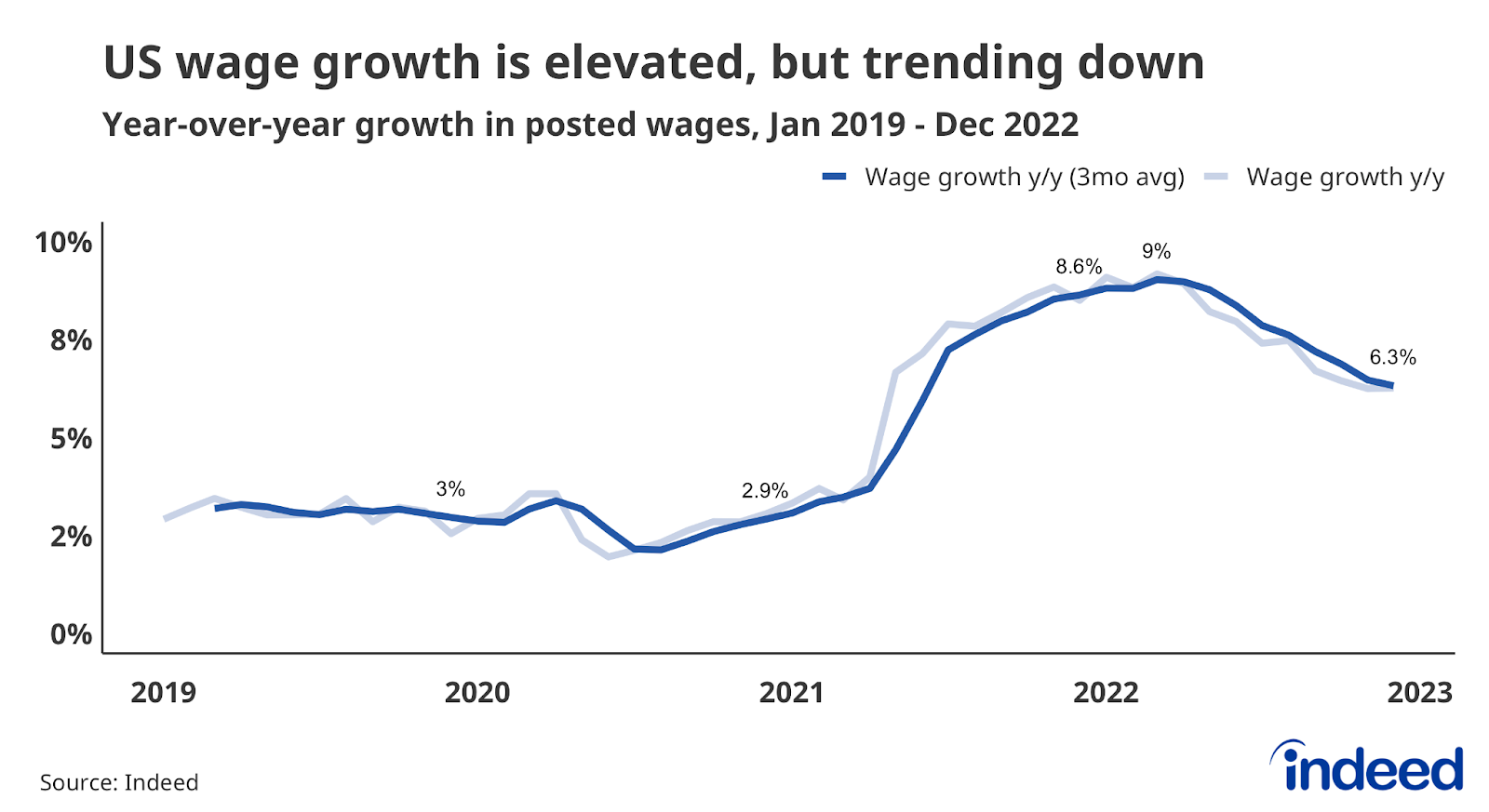

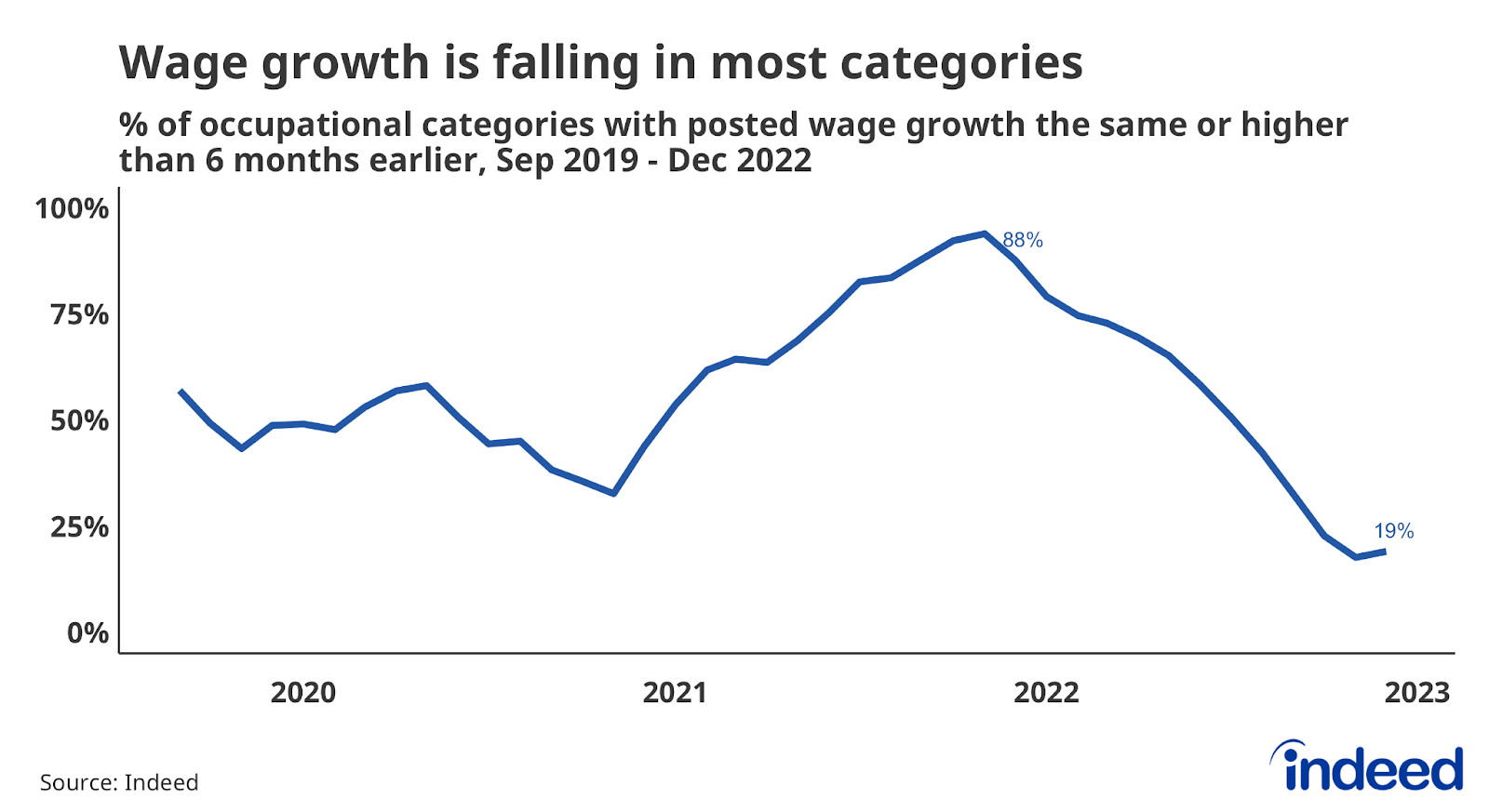

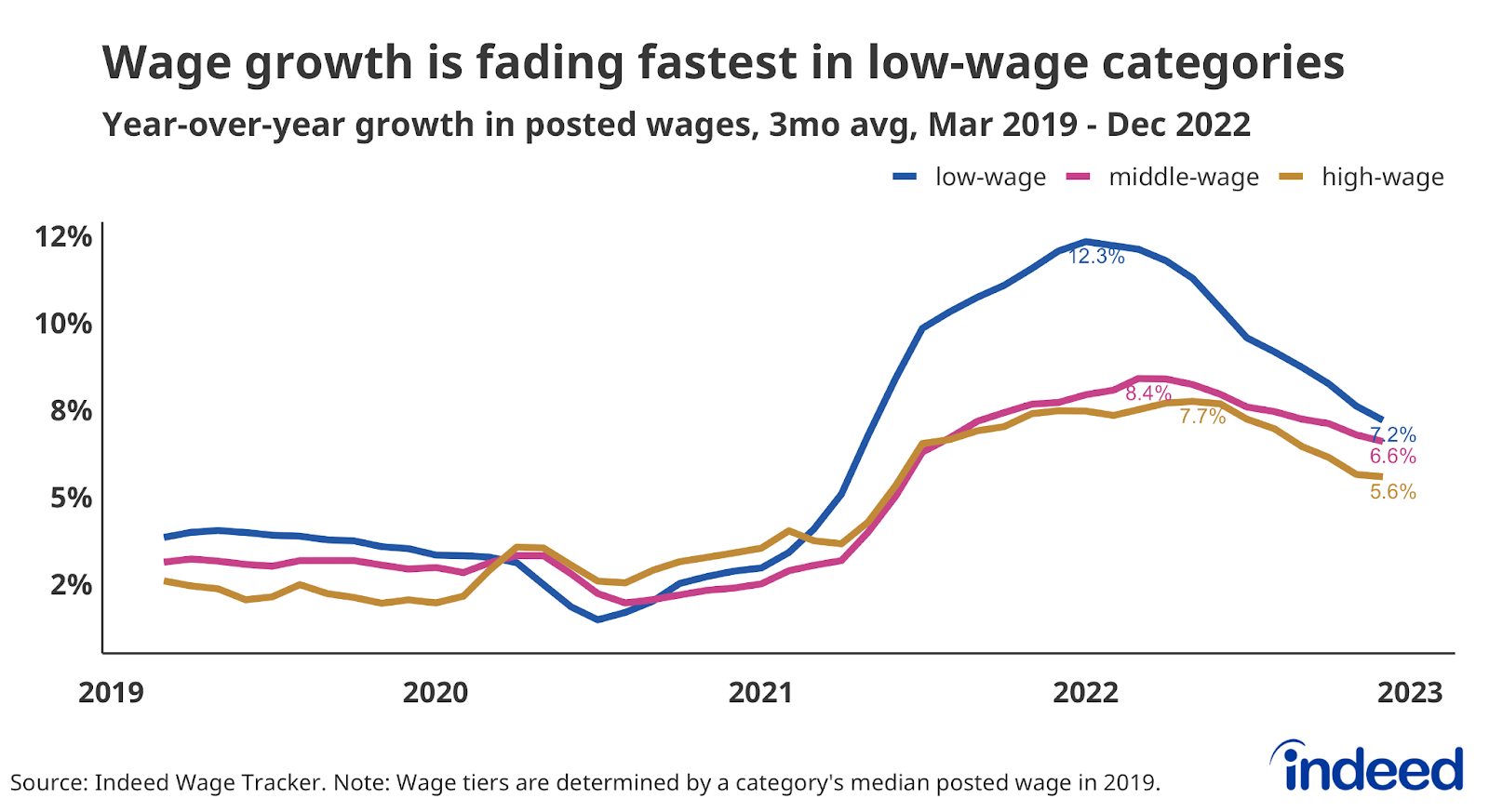

Lower-wage sectors continue to show a sharper wage growth decline than other sectors. Overall posted wage growth declined by 0.2 percentage points from November to December, but fell by 0.4 for lower-wage categories. Compare that to a 0.2 point decline for middle-wage categories and a flatlining for the high-wage group.

Lower-wage sectors continue to show a sharper wage growth decline than other sectors. Overall posted wage growth declined by 0.2 percentage points from November to December, but fell by 0.4 for lower-wage categories. Compare that to a 0.2 point decline for middle-wage categories and a flatlining for the high-wage group.

Source: Daily Shot

Source: Daily Shot