LABOR MARKET WATCH

Some subtle shifts in the U.S. labor market:

- Since August, 43% of Americans who entered the labor force had not found a job by mid-October.

- Since August, the number of unemployeds rose 11.4% and is now 12.1% above its pre-pandemic level. Meanwhile, continuing unemployment claims turned up in September, back to their April level, meaning that it now takes longer to find jobs after losing one.

- The next BLS measure of private job openings (for October in early December) is likely to show a meaningful drop judging by trends in Indeed Job Postings:

Consumer credit is already deteriorating amid a solid Q3 economy. The combo of high financing costs and rising unemployment could really accelerate the trend.

A few more stats:

- Fitch Ratings reports that 6.1% of subprime auto loans were 60 days+ overdue in September, highest since 1994. Yes, 1994, not 2008 or 2009 as we would suspect. They peaked at 5.0% in January 2009. Student loan payments resumed in October.

- Moody’s says that delinquency rates on newly opened credit card accounts are back to their 2008 levels.

- Several companies, from staples producers (e.g. General Mills) to luxury goods merchants (e.g. Harley Davidson, Malibu Boats) recently warned of changing consumer behavior impacting their Q4 revenues.

- A recent survey of auto dealers revealed that financing availability for new car buyers is tougher to get across 62% of auto dealers.

- In October, more than 90% of Affirm’s interest-bearing volume was offered with annual percentage rates up to 36%. And it has managed to keep its credit performance steady. Its 30-plus-day delinquency rate, excluding for its pay-in-four installments, was 2.4% in the quarter, down from 2.7% a year prior. Hmmm…

US Consumer Long-Term Inflation Expectations Reach 12-Year High Inflation views over 5-10 years rose to 3.2% in November

Consumers expect prices will climb at an annual rate of 3.2% over the next five to 10 years, up from 3% a month earlier, according to the preliminary November reading from the University of Michigan. They see costs rising 4.4% over the next year, compared to last month’s 4.2%, according to data released Friday. (…)

Nearly one in five consumers surveyed said that unemployment will cause more hardship than inflation over the coming year. The government’s latest jobs report showed hiring was concentrated in only a few sectors, while the unemployment rate climbed to the highest level since the start of 2022. (…)

An index of buying conditions for durable goods slumped from a month earlier by the most since November of last year. A record 36% of consumers spontaneously blamed high borrowing costs or tight credit conditions for poor motor-vehicle purchase conditions. The share of consumers blaming similar factors for poor home and durable goods buying conditions was the highest since 1982. (…)

China’s Consumption Recovery Is Losing Momentum, Data Show Alternative indicators show weakening consumer demand

An indicator of Chinese consumer demand for recreation and transport published by Paris-based QuantCube Technology, along with an independent survey of consumer sentiment by US company Morning Consult, both fell in October from the previous month. A poll of private business sentiment from the Cheung Kong Graduate School of Business also declined in the month. (…)

The QuantCube indicators are based on alternative data sources, such as web search queries, transportation figures reflecting people’s movements, and consumer reviews. (…)

Retail sales growth generated by China’s biggest online shopping festival, which runs from October through November, was slower than in previous years. The value of sales rose 2.1% from last year, significantly lower than the 14% increase recorded in 2022, and apparently the lowest in many years, Nomura Holdings Inc. economists led by Lu Ting said in a note citing third party data.

China’s property sector also shows signs of worsening this month, Nomura said, with sales in 21 major cities falling 44% from 2019 levels in the early weeks of November. That’s similar to the pace of contraction in July, before Beijing started a new round of property easing measures, the bank said. (…)

Data provider Syntun, meanwhile, estimated cumulative gross merchandising volume (GMV) sales across major e-commerce platforms rose 2.08% to 1.14 trillion yuan ($156.40 billion) compared with growth of 2.9% last year. (…)

The GMV figures take into account the value of all orders placed, and do not capture the amount that will be returned later.

Analysts and industry executives expect return rates to be high this year as consumers buy more in order to obtain larger discounts on checkout, only to return the items they do not need.

A Bain and Company report released last week found that 77% of the 3,000 consumers it surveyed had planned to spend less or the same amount on Singles Day compared with last year. (…)

- German Retailers See Bleak Outlook for 2023 Christmas Sales More than half of businesses foresee a decline on the year

(…) The lobby association expects nominal sales growth of 1.5% for November and December — a drop of 5.5% after taking the annual increase in consumer prices into account.

For the full year, including the food sector, it confirmed its prediction for sales to increase by some 3% to about €650 billion ($695 billion) — a decline of 4% after factoring in inflation. (…)

US Credit-Rating Outlook Changed to Negative by Moody’s Assessor cites risks from deficits, political polarization

The US was threatened with the loss of its last top credit rating on Friday, as Moody’s Investors Service signaled it was inclined to downgrade the nation because of wider budget deficits and political polarization.

The rating assessor lowered the outlook to negative from stable while affirming the nation’s rating at Aaa, the highest investment-grade notch. Amid higher interest rates, without measures to reduce spending or boost revenue, fiscal deficits will likely “remain very large, significantly weakening debt affordability,” Moody’s said.

“Interest rates have shifted materially and structurally higher,” William Foster, a senior credit officer at Moody’s, said in an interview. “This is the new environment for rates. Our expectation is that these higher rates and deficits around 6% of GDP for the next several years, and possibly higher, means that debt affordability will continue to pressure the US.” (…)

Moody’s sees federal interest payments relative to revenue and gross domestic product rising to around 26% and 4.5% by 2033, respectively, from 9.7% and 1.9% in 2022, according to Friday’s report. Those projections reflect the likelihood of higher-for-longer interest rates, the company said, with the average annual 10-year Treasury yield peaking at around 4.5% in 2024. (…)

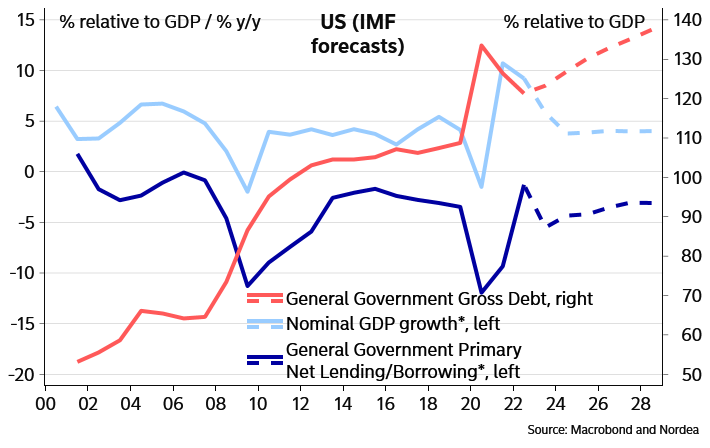

A US debt crisis is seldom seen as an imminent threat, and we do not expect such a crisis to surface any time soon either. (…) But the outlook is more worrying due to the massive primary deficits the US is running. One does not need to do any stress testing on the IMF baseline forecasts to find a rising debt-to-GDP ratio.

US public debt on a worrying path

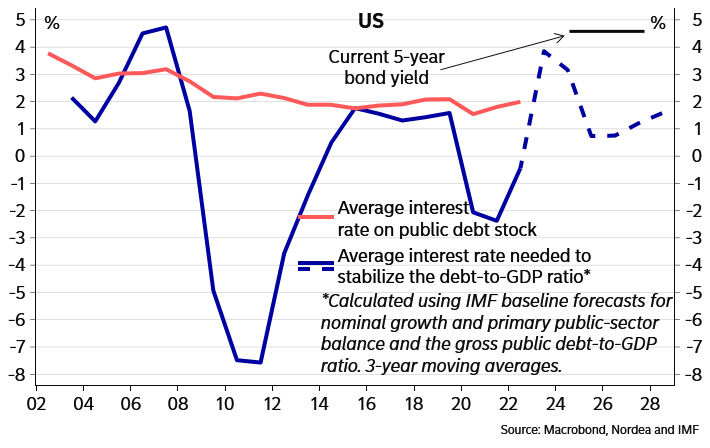

On a path set by the IMF forecasts for the following five years, the average interest rate that would stabilise the debt-to-GDP ratio is in the order of 1-2%. This is not far from the average interest rate on the debt stock of around 2% last year, but at current yield levels the average interest rises rapidly (around a third of US public debt matures over the next 12 months), putting the US debt on an unsustainable trajectory.

US debt metrics not compatible with the current level of interest rates

This is not to say that we expect to see a US debt crisis in the near future. Far from it. The global role of the dollar and the Treasury market allow the US to run irresponsible fiscal policies for longer than other countries, and we are unlikely to be close to the breaking point. And buying by the Fed also serves as a backstop, if needed. As we have argued before, cyclical considerations and new signals from central banks are a more likely driver of long bond yields than rising debt worries.

However, this does not mean that the US fiscal outlook would not pose considerable risks. Market focus could easily stay on the debt outlook and the huge amount of bonds that private investors have to buy at a time when the central bank is reducing its holdings, which could yet propel yields higher.

Government debt burdens can quickly become unsustainable if the willingness to finance new borrowing vanishes. The higher the debt burden, the higher the risk of this happening. As stated above, we do not think we are near such a point, but such risks certainly cannot be disregarded.

- The Clearest Sign Yet That Commercial Real Estate Is in Trouble Foreclosures are surging in an opaque and risky corner of commercial real-estate finance, offering one of the starkest signs yet that turmoil in the property market is worsening.

EARNINGS WATCH

Pre-announcements look ok only when compared with Q3’23 at the same time but last week was quite poor: of last week’s 18 pre-announcements, 16 were negative. Are we going to see the inverse of the Q2 trend which started poorly (3.0 N/P on July 28 with 112 pre-announcements but gradually improved in subsequent weeks? Remember GDP jumped 4.9% in Q3 with strong consumer spending.

Analysts keep revising upward however:

Yet, estimates for Q4 EPS are +5.8%, down from +11.0% on Oct. 1 and down from +7.0% last week. Go figure!

Note also that FactSet numbers are weaker:

- For the third quarter, the S&P 500 is reporting (year-over-year) earnings growth of 4.1%. [LSEG is at +6.3%]

- For the fourth quarter, analysts are now projecting (year-over-year) earnings growth of only 3.2%. [LSEG is at +5.8%]

Trailing EPS are now $218.73. Full year 2023: $220.62e. Forward EPS: $236.29e. Full year 2024: $245.31e. All per LSEG/IBES which most pros use.

Rosenberg Research:

While headline S&P 500 earnings per share (EPS) growth is running at +2.5% in Q3, that glow is being masked by just 7 stocks. Like the price action throughout much of 2023, the “Magnificent 7” (Tesla, Nvidia, Meta, Amazon, Alphabet, Microsoft and Apple) is doing all the heavy lifting — earnings are growing at a whopping +59% YoY pace.

The remaining companies are seeing a profit decline of -13%. This trend is expected to continue into the next quarter as well, with the Magnificent 7 projected to see a +45% net income surge with the rest at -2%.

(…) if we update our guidance tracker, which looks at available Bloomberg data and compares S&P 500 company projections to analyst expectations, we note that nearly 80% of revenue guidance for the coming Q4 reporting season have missed estimates; for EPS that number is at 60%.

Looking at full year guidance, 60% of revenue guidance has missed while 40% of EPS have done so as well. The fact that companies look to be facing pressure on the sales front is rather concerning for two reasons: i) it makes any growth in EPS of lower quality (managing costs rather than a demand pick-up) and ii) the close ties with nominal GDP growth.

This chart is from Goldman Sachs:

I have shown before how rising interest expense is biting into corporate profits. This chart via Callum Thomas shows how cash rich companies are benefitting from Fed tightening. All of the “Magnificient Seven” contribute to the grey line:

Source: Substack Notes Platform

Feeling contrarian?

Hezbollah Fires at Israeli Infantry Across Border

-

Israel Warns of Wider War as It Presses On in Gaza The chance of a full-scale war breaking out between Israel and forces in Lebanon has increased in recent days, Israeli officials say.