Fed Swaps Once Again Show Hike More Likely Than Not for May

The rate on the contract tied to that gathering rose to around 4.96% on Monday, around 13 basis points above the current effective rate on fed funds, the benchmark targeted by the central bank. The Fed tends to move in increments of 25 basis points — or multiples thereof — so that suggests odds of more than 50% that it will hike. (…)

Meanwhile, Treasury yields jumped, pulling back from their lowest levels of the year, as fears of banking-sector contagion eased amid renewed prospects of further US support for the industry.

The move was led by two-year notes, whose yields climbed as much as 22 basis points to 3.99%, paring the more than 1.5 percentage-point drop since fears of a banking crisis start sweeping through markets early this month.

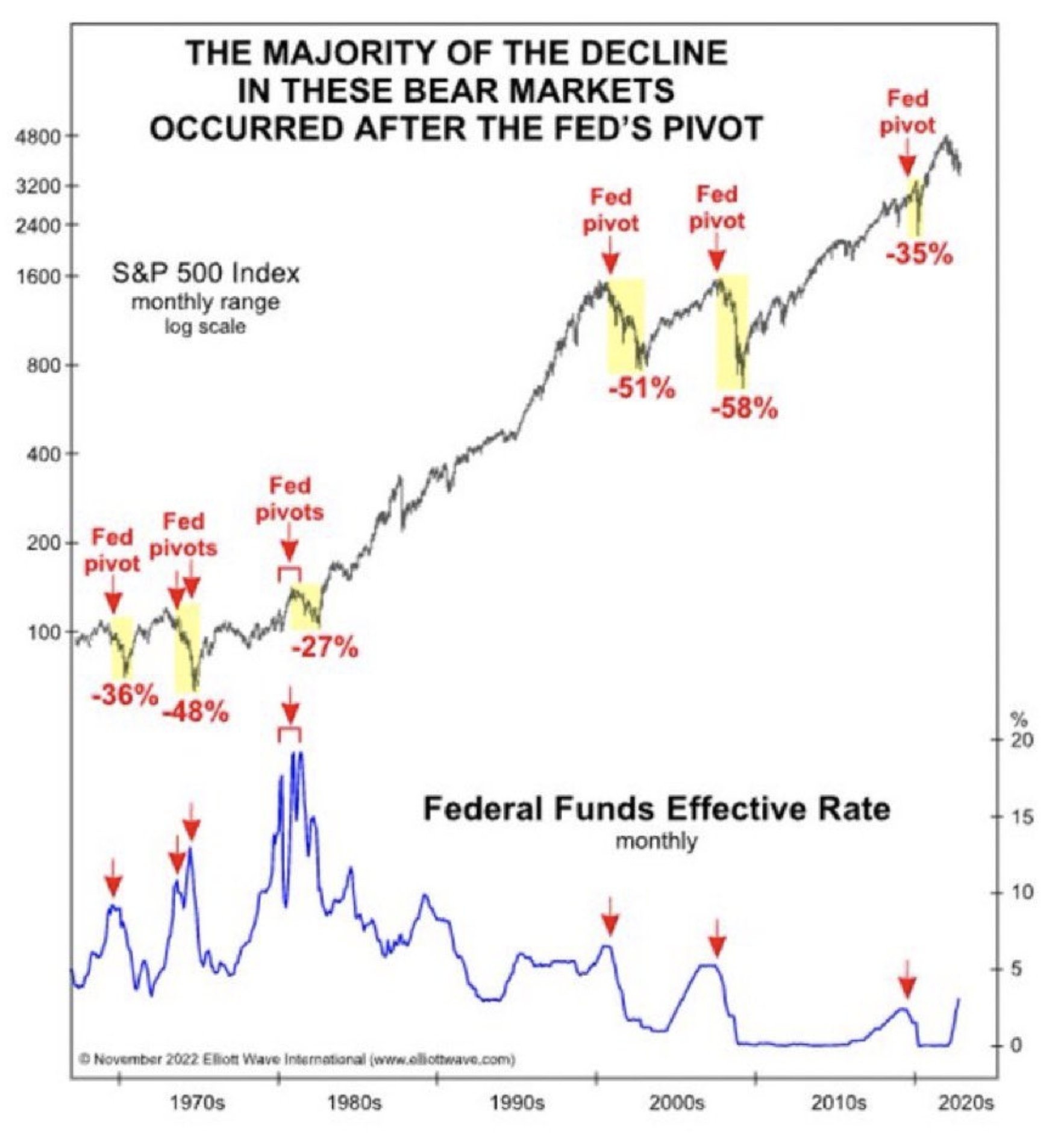

Traders are only pricing in a 35% chance of another hike at the May FOMC meeting. In other words, the Fed is done hiking. (Jim Bianco)

Traders are only pricing in a 35% chance of another hike at the May FOMC meeting. In other words, the Fed is done hiking. (Jim Bianco)

- The bond market “Vix” remains near a record peak.

@biancoresearch

- But 2-yr Treasury yields are sniffing lower Fed funds rates.

A Tale of Two Housing Markets: Prices Fall in the West While the East Booms In an unusual pattern, the 12 major housing markets west of Texas, plus Austin, saw home prices fall in January, while the opposite happened in the rest of the country

In all of the 12 major housing markets west of Texas, plus Austin, home prices fell in January on an annual basis, according to mortgage-data firm Black Knight Inc.’s home-price index. In the 37 biggest metro areas east of Colorado, except Austin, home prices rose year-over-year.

This pattern of geographical disparity is highly unusual, if not unprecedented, housing analysts say. “We’ve never seen anything quite like this where it’s so stark, west to east,” said Andy Walden, vice president of enterprise research strategy at Black Knight.

(…) the cities most closely associated with tech have the fastest falling home prices. San Jose, Calif., and San Francisco home prices were down more than 10% from a year earlier in January, and Seattle prices fell 7.5%.

In the Eastern half of the U.S., Florida and other Southern markets are still attracting companies and adding jobs. Orlando home prices were up 9.3%, while Miami prices rose 12%, the top increase among the 50 biggest metro areas. A slew of financial companies moved to Miami in 2021 and 2022, and their employees are still arriving, said Judy Zeder, an agent with the Jills Zeder Group at Coldwell Banker Realty in Miami.

“We still have a lot of buyers who are here that we still can’t find homes for,” she said. (…)

The metro areas posting the biggest price declines tend to fall into two categories: markets where prices skyrocketed in recent years as people moved in from other states, such as Phoenix and Austin, and markets where prices didn’t surge as dramatically during the boom but that were already prohibitively expensive, such as San Francisco and Los Angeles, said Black Knight’s Mr. Walden. (…)

This year, some of the most stretched prices can be found further east, a sign that prices in these markets may turn negative on an annual basis soon. In January, the analysis found Atlanta, Cape Coral, Fla., and Charlotte, N.C., were the most overvalued, based on how far prices have risen above their long-term pricing trends.

The top 10 were all in the South and Midwest. (…)

Eurozone Banks Cut Lending Even Before Latest Financial Turmoil Decline in bank lending could deepen as financial institutions move to retain deposits, strengthening effect of ECB rate moves

The banks cut their lending to eurozone businesses by 3 billion euros in February, equivalent to $3.23 billion, while the increase in lending compared with a year earlier slowed to 4.9% from 5.3% in January, according to data released by the European Central Bank on Monday. There was also a slowdown in lending to households. (…)

“It is clear that risks to financial stability have increased,” said Kristalina Georgieva, head of the International Monetary Fund, in a speech Sunday. “The rapid transition from a prolonged period of low interest rates to much higher rates inevitably generates stresses and vulnerabilities.”

Facing the threat of a withdrawal of deposits—a feature of both the SVB and Credit Suisse strains—banks are likely to have to pay savers more, and will therefore have to charge more for their loans. The figures released Monday showed households and businesses withdrew deposits from banks for the second straight month in February as they looked for higher returns. (…)

Some ECB policy makers are warning that the decline in bank lending has been sharper than during previous periods of monetary policy tightening, possibly amplifying the impact of the central bank’s monetary policy on the economy.

“The size and the speed of the adjustment indicate that the transmission of our monetary policy to the economy may have become stronger,” said Fabio Panetta, an ECB official, in a speech Wednesday. (…)

- Goldman sees further credit tightening ahead for Europe.

Source: Goldman Sachs via The Daily Shot

Source: Goldman Sachs via The Daily Shot

- From John Authers:

This means that trouble for banks in the the eurozone — whose rickety structure makes any crisis harder to quell — and especially in China could create far greater economic damage. The following chart from the Institute of International Finance shows that as of 2019, bank lending to the private sector was equivalent to gross domestic product in the eurozone, but barely half of GDP in the US. Apart from China, note that the UK also has particularly elevated exposure to its banking system, and that Japan is more bank-dependent than the eurozone. Countries least dependent on their banking systems include Egypt and Mexico:

- Money pulled from eurozone banks at record rate in February

- M1 growth, including currency and overnight deposits, contracted by a record 2.7% in February. (@fwred)

The U.S. money supply is also declining fast on a YoY basis but it rose much more than in the Eurozone during the pandemic years. In absolute terms, U.S. M2 remains 40% higher than in 2019.

Distress in Office Market Spreads to High-End Buildings Amenities gave many an advantage earlier in the pandemic, but defaults and vacancies are rising as interest rates climb

Defaults and vacancies are on the rise at high-end office buildings, in the latest sign that remote work and rising interest rates are spreading pain to more corners of the commercial real-estate market.

For much of the pandemic, buildings in central locations that feature modern amenities fared better than their less-pricey peers. Some even were able to increase rents while older, cheaper buildings saw surging vacancy rates and plummeting values. Now, these so-called class-A properties, whose rents generally fall into a city’s top quartile, are increasingly coming under pressure.

The amount of U.S. class-A office space in central business districts that is leased fell in the fourth quarter of last year for the first time since 2021, according to Moody’s Analytics. The owners of a number of high-end properties recently defaulted on their mortgages, highlighting the financial strain from rising interest rates and vacancies. (…)

Landlords who benefited from long-term leases are becoming more vulnerable as leases signed before the pandemic expire. Michael Silver, chairman of Vestian Global Workplace Services, said law firms he advises on their real estate often look to cut their space by around 30% when their leases expire. And unlike in 2021, more companies are worried about a recession and looking to cut costs. (…)

China grants billions in bailouts as Belt and Road Initiative falters New study attempts to capture total rescue loans from world’s biggest bilateral creditor

From the study’s abstract:

A key finding is that the global swap line network put in place by the People’s Bank of China is increasingly used as a financial rescue mechanism, with more than USD 170 billion in liquidity support extended to crisis countries, including repeated rollovers of swaps coming due. The swaps bolster gross reserves and are mostly drawn by distressed countries with low liquidity ratios.

In addition, we show that Chinese state-owned banks and enterprises have given out an additional USD 70 billion in rescue loans for balance of payments support. Taken together, China’s overseas bailouts correspond to more than 20 percent of total IMF lending over the past decade and bailout amounts are growing fast.

However, China’s rescue loans differ from those of established international lenders of last resort in that they (i) are opaque, (ii) carry relatively high interest rates, and (iii) are almost exclusively targeted to debtors of China’s Belt and Road Initiative. These findings have implications for the international financial and monetary architecture, which is becoming more multipolar, less institutionalized, and less transparent.

In effect, China is bailing itself out making bailed out countries even more dependent on China.

China’s new premier rolls out the welcome wagon for foreign companies

China’s new premier rolls out the welcome wagon for foreign companies

(…) “China will open its door wider and wider,” he told the executives, according to state broadcaster CCTV, urging them to “invest in China and take root in China.”

“No matter how the international situation changes, China will unswervingly expand its opening up to the outside world,” he said. “China’s economy has been deeply integrated into the global division of labor.”

Li pledged that the country will align with international economic and trade rules, give equal treatment to foreign investment and facilitate trade and investment by removing government controls. (…)

“You are not foreigners, but family,” Wang Wentao, the commerce minister, told attendees at the China Development Forum. (…)

(…) China launched private pension plans for the first time last year and Beijing has ensured that domestic banks and fund managers win the vast majority of the new business in a market that may eventually grow to $1.7 trillion. Global companies including BlackRock and Fidelity International Ltd have been off to a slow start. (…)

Given their tiny asset bases in China, most foreign money managers have so far been excluded from pilot trials in 36 cities, allowing banks like Industrial & Commercial Bank of China Ltd. and China Merchants Bank Co. to grab all the inflows. (…)

China’s fledging private pension system is loaded with promise, as Beijing desperately tries to entice retirement savings to support an aging population. The number of people over 60 is expected to jump more than 50% by 2040, according to the World Health Organization. China’s population shrank last year for the first time in six decades.

To address the problem, China has launched three pension pillars. The first two — a compulsory state-backed plan and a voluntary corporate matching option — don’t come close to meeting the future needs of most pensioners. (…)

The new private offering aims to fill the void, allowing clients to contribute up to 12,000 yuan a year in tax-sheltered plans, similar to Individual Retirement Accounts (IRAs) in the US that have become a $13 trillion market. The private pillar is estimated by Citic to grow to 12 trillion yuan by 2035, equal to the two other plans combined. UBS Group AG estimates the market could be worth $25 trillion by 2060, more than a third of China’s gross domestic product by then. (…)

The new plan is an attractive niche for asset managers since the tax breaks appeal to high-income earners and the money will be locked up for years with the same firm. Once a client opens a pension account with a bank, they can only invest in eligible funds distributed by that lender. That’s a rare, government-sponsored opportunity in China, where fickle investors are notorious for switching investments and banks. (…)

So far, most international firms’ wholly-owned businesses have been unable to join the pension party. They either lack sufficient assets to meet thresholds set by Beijing, or they’ve only recently won regulatory approval — often after lengthy delays — to buy out local partners to sell their own funds. (…)

The slow rollout could test global managers’ commitment to China as they face years of losses before building up scale, and it’s unlikely any foreign commercial bank will be selected for the trial, according to Zhou at GuanShao. He cited Citigroup Inc., which announced in December it will wind down its consumer bank in China as part of a wider retreat. Vanguard Group Inc. scrapped plans in 2021 to set up a wholly-owned fund business and now plans to exit the country entirely, people familiar told Bloomberg News. (…)

Chinese automakers rev up price war in race for market dominance

A brutal price war is raging across China’s auto sector, catalyzing a profound overhaul of the world’s largest car market as makers of new-energy vehicles and conventional fossil fuel cars face off to win a greater share of a market rattled by slowing sales.

The first shot was fired by U.S. electric vehicle (EV) maker Tesla Inc., which late last year rolled out massive subsidies and price cuts to spur sales. A flurry of domestic and foreign EV-makers followed suit, with BYD Co. Ltd., XPeng Inc., Nio Inc. and Volkswagen AG all racing to win customers by offering generous discounts.

Twisting Oreos for science (Axios)

Twisting Oreos for science (Axios)

A team at MIT has twisted apart over 1,000 Oreos in the name of science, attempting to solve that age-old problem: Is there any way to get the cream on both sides of the wafers?

- Turns out the answer is: Not really. Oreo’s filling stuck to just one wafer about 80% of the time, using both a machine and hand techniques to twist.

- “There was no combination of anything that we could do … that changed anything in our results,” Crystal Owens, a Ph.D. candidate in MIT’s mechanical engineering department, told The Wall Street Journal.

(

( The dash for dollars all happened before the

The dash for dollars all happened before the