Yesterday’s U.S. Flash PMI is quite significant, yet I found no mention of it anywhere this morning.

At 52.3, the headline S&P Global Flash US PMI Composite Output Index was up from 50.9 in December and signalled the fastest rise in business activity since June 2023. The expansion in output indicated a notable uptick in performance at the start of the year.

Output growth was led by service providers, as manufacturing firms continued to see a moderate drop in activity in January. The rate of decline in production at goods producers eased from that seen in December, however, linked to improved order inflows. Manufacturers also mentioned that delivery delays following severe storms and shipping disruptions at times hampered production. Suppliers’ delivery times at goods producers lengthened on average for the first time in 13 months.

New business expanded for the third successive month at US companies in January, with the rate of growth quickening to the sharpest since June 2023. The upturn in new orders was broad-based, as manufacturers registered the first rise in new sales since October 2023, and the fastest uptick since May 2022.

Service providers reported the strongest gain for seven months. More robust demand conditions were linked to greater client referrals and emerging reports of customers having worked through their buffer stocks.

Stronger demand was domestically focused, however, as new export orders fell for the second month running in January. The decrease was the quickest since October 2023 amid a faster drop in manufacturing new export sales and another marginal decline in the service sector.

Businesses were more upbeat in their expectations regarding the outlook for output at the start of 2024, as the degree of confidence reached the highest since May 2022. Increased optimism reportedly stemmed from hopes of improving demand conditions, investment in new machinery and the release of new service lines.

Companies in the US recorded another rise in employment during January, albeit slightly slower than seen in December. The increase in staffing numbers was only marginal overall and the second-softest since last August. Panellists highlighted that greater workforce numbers were due to increased business requirements and the hiring of skilled workers for long-held vacancies, but that hiring was often constrained by labor shortages.

The upturn in employment was also linked to efforts to clear backlogs of work amid a renewed accumulation of incomplete business in January. The level of outstanding work grew for the first time since last April, with the expansion driven by service providers. Manufacturers, meanwhile, recorded a slower but still marked drop in work-in-hand.

Inflationary pressures cooled at the start of the year, as input prices rose at a softer pace. The rate of increase was slower than the series average and the second-weakest since October 2020. That said, goods producers saw a sharper uptick in cost burdens. The pace of manufacturing input cost inflation picked up to the steepest since April 2023 amid challenges sourcing materials, higher prices for transportation and increased fuel costs.

A sectoral divergence was also evident for selling prices in January, as service providers signalled the slowest rise in output charges in the current sequence of inflation which began in June 2020 amid efforts to price competitively and drive new orders.

Manufacturers, meanwhile, raised their output prices at the steepest rate since April 2023 as firms sought to pass through higher costs to customers.

Measured overall, average prices charged for goods and services rose at a much-reduced rate in January, posting the smallest monthly rise since May 2020.

At 50.3, the S&P Global Flash US Manufacturing PMI was up from 47.9 in December, to signal the first improvement in operating conditions at goods producers in nine months. The upturn was only fractional, however, amid a further drop in production.

Although firms noted broadly sufficient availability of materials at suppliers, challenging trucking conditions due to storms and transportation delays reportedly weighed on vendor performance. Lead times lengthened for the first time in over a year and to the greatest extent since October 2022.

Purchasing activity at manufacturers continued to contract, with firms also depleting pre-production inventories further, but both rates of decline eased on the month. Stocks of finished goods saw a renewed expansion, indicating the fastest rise in post-production inventories since November 2022 as companies anticipate greater new orders in the coming months.

This preview of month-end PMIs indicates:

- Broadly accelerating demand (new orders) overall, including goods, suggesting that the inventory cycle might be complete after the strong year-end retail sales.

- Soft but growing employment, potentially easing wage demand/offers.

- Slowing inflation overall, the “smallest monthly rise since May 2020”. Remember the spring of 2020?

Look at the teal line below. Services prices charged rarely flirt with the 50 line:

The PMI Composite Output Prices Index has abruptly dropped lately, potentially dragging the CPI downward in coming months.

Ed Yardeni today warns of a “quite weak” ISM PMI in January, “rekindling recession fears”.

January’s average of the general business indexes that are compiled by three regional Fed surveys took a dive during January. This suggests that January’s national M-PMI might be quite weak, rekindling recession fears. It’s hard to believe that the rolling recession for goods producers and distributors isn’t bottoming given the recent strength in retail sales. We’ll be watching to see what January’s M-PMI report shows next Thursday.

Conflicting PMI reports happen. History suggests to put much more weight on S&P Global’s surveys.

The Bank of Canada held its policy interest rate steady for the fourth consecutive time on Wednesday, but dialled back its threat of further rate hikes in a notable shift in language that opens the door to possible rate cuts in the first half of this year.

While the bank remained on hold, it said that Canada’s sluggish economy has now entered a state of “excess supply,” which should help drag inflation down over time. And it effectively confirmed what financial markets have assumed for months: that interest rates have peaked for this business cycle.

“With overall demand in the economy no longer running ahead of supply, Governing Council’s discussion of monetary policy is shifting from whether our policy rate is restrictive enough to restore price stability, to how long it needs to stay at the current level,” Bank of Canada Governor Tiff Macklem said at a news conference after the rate announcement.

He did not rule out further rate hikes altogether, but suggested they were unlikely if inflation and economic activity developed in line with the bank’s projection. (…)

Despite broad-based progress, however, Mr. Macklem and his team remain concerned about “underlying” price pressures, as well as pockets of high inflation, notably fast-rising shelter and food prices.

Core measures of inflation, which strip out the most volatile components of the CPI, have been stuck in the 3.5-per-cent to 4-per-cent range for the better part of a year. Mr. Macklem said the bank needs to see “further and sustained easing of core inflation” before considering rate cuts. (…)

CHINA

I have considered China uninvestable for many years, mainly for political and governance reasons. Those concerns remain but seem increasingly priced in.

In some ways, China is where the U.S. was in 2008-09 after its real estate crisis, economically and “sentimentally”. Beijing (i.e. The Party) now clearly understands the problems and the urgency to address them with potent monetary and fiscal measures.

If the U.S. inventory cycle is effectively complete, Chinese manufacturing new orders should soon improve. When people feel that real estate is stabilizing, overall demand should gradually pick up. The Chinese consumer is in much better shape than Americans were in 2007-09 and Chinese politics are “much simpler”…

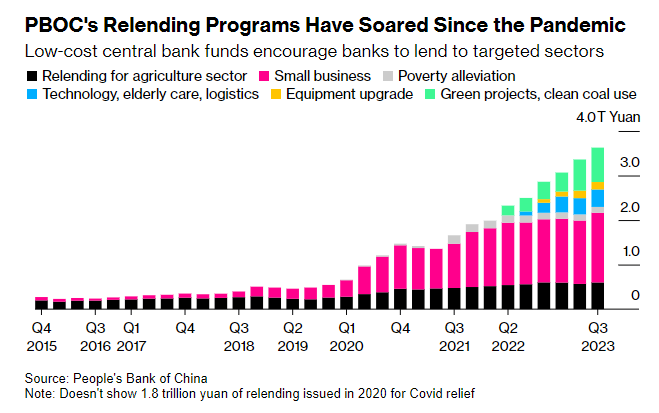

A local government financing vehicle in China’s Shandong province reached an agreement with creditors to partially repay and extend the payment deadline for nearly all of its 479 million yuan ($66.8 million) non-bond debts, highlighting the sector’s liquidity challenges despite government support.

Weifang Binhai Investment Development Co., which raises off-balance-sheet debt financing for the province’s infrastructure projects, hadn’t made payments as of Dec. 31, 2023, past the original deadline, according to the LGFV’s filing this month that was posted on Shanghai Stock Exchange’s private disclosure forum but seen by Bloomberg. (…)

In a news briefing earlier this week, People’s Bank of China Governor Pan Gongsheng vowed to provide financial support for local government debt. (…)

Some 83% of the 566 respondents in the survey conducted from early September to early October said China “is facing a downward trajectory” economically. Nearly two-thirds said they expected a recovery to take one to three years. (…)

The German chamber’s survey also found that some 54% of firms thought China’s investment appeal was falling compared to other markets, though just as many plan to boost their spending in the Asian nation over the next two years. (…)

Survey respondents also said their main reason for investment now was countering competition, with the poll finding that German firms were becoming more concerned about their Chinese rivals. While just 5% of respondents viewed China’s companies as top innovators in their industry, 46% predicted they’d be leaders in the next five years. (…)

The country is set for a boom in corporate profits and investors should be piling into shares of companies in sectors like health care, tourism and luxury goods, according to Charles Gave.

“The Chinese stock market is undervalued against cash, Chinese bonds, gold, and other world stock markets — and it is in a state of total panic,” Gave, whose group runs the Hong Kong-based asset-allocation consultancy Gavekal Research and some global funds, wrote in a note Wednesday. “It has to be the best value proposition in the world.”

He said China is at a stage where companies’ profit growth has started exceeding their cost of capital, implying earnings will boom and companies will resume investing and hiring. (…)

Some other fund houses are also turning a bit optimistic once again. Andrew Lapping, chief investment officer at Ranmore Fund Management, said the current setup is an “exciting opportunity” for investors. Alice Shen, a portfolio manager at VanEck, said China is at an “inflection point” and can become “the opportunistic buy of the year.”

Still, skepticism about China exposure is far from over. Remi Olu-Pitan, head of multi-asset growth and income at Schroders, said in a media briefing on Wednesday that China’s recent move may provide only a “tactical lift” to the country’s assets, but more is needed for a “structural” climb.

“The incentive to reduce exposure is pretty powerful and so we think this provides a pause, but we worry any recovery will be an opportunity to derisk,” she said.

To be sure, Gave made a similar bullish recommendation on China stocks in August — and that didn’t fare so well. The CSI 300 fell 8.7% from there into the end of the year.

Still, he has some wins to his name. He was bullish on Japan in May 2020, and since then the Topix Index has gained 71%. He said in June 2018 that world’s bear market will likely start in Europe, following which the MSCI Europe Index fell about 16% to a low in December of that year. (…)

Speaking of AI, interesting keynote video about this new gadget. (David, maybe you could take occasional space on this blog, “David’s Corner”?)

Speaking of AI, interesting keynote video about this new gadget. (David, maybe you could take occasional space on this blog, “David’s Corner”?)

Forrester offers a review of R1: rabbit’s r1 Personal AI Device (PAD): Exciting Technology With An Underwhelming Experience

Here’s what it shows us about the future:

- Devices will someday learn by watching us, not being programmed. While the r1 will be too complex for most consumers, it illustrates the possibilities — at least for digital tasks. In the future, devices will wield just the right balance of natural language and agent capabilities that learn what we do, need, and want without programming. Their ability to converse in language and emulate empathy will lead us to trust them; we hope that the PAD makers are trustworthy.

- These devices challenge the assumption that brands need piles of consumer data. With cameras + edge computing/intelligence, devices can simply watch and listen to consumers, learn, and then tell brands what consumers want. When you think about this, this trend will unwind marketing as we know it. Fortunately, that is still some way off, but it’s something to watch for.

- These virtual assistants will serve some purposes — not all. They’ll do simple, tedious tasks that we don’t want to do. They will learn what we want and engage brands that we trust to get these things. They may even someday do work for us. They will still leave the heavy mental lifting — literal and figurative — to humans. I hope this lets us be less into the details and more creative and innovative as a species. Who knows where that will lead?

Questions we should be asking:

- Is society or human beings ready or not to have agents learn from us and perhaps give them some training? Are we ready to trust them to act on our behalf? How good will these personal agents get at understanding the nuances of human behavior, having values, and not harming others while they seek to serve us? AI safety is a hot topic today to answer precisely these types of questions.

- Are LAMs a real thing? The other term we hear is world model. Agents will need models of our physical world and the actions that we humans take in both the physical and digital realms. Today’s large language models are a start, but the AI community has much work to do.

- Who is ultimately responsible for the actions that a model takes? If you allow your car to drive itself and it hurts someone, who is at fault? What if you train a model to spend money or communicate on your behalf? Are humans ready to assume the risks of letting an agent order groceries? Move money? Communicate with friends?