Note: I am travelling in Asia until April 24. Limited equipment and different time zones will limit the frequency and depth of my postings.

Note: I am travelling in Asia until April 24. Limited equipment and different time zones will limit the frequency and depth of my postings.

Stubborn inflation pressures persisted in March, derailing the case for the Federal Reserve to begin reducing interest rates in June and raising questions over whether it can deliver cuts this year without signs of an economic slowdown.

The consumer-price index, a measure of goods and services prices across the economy, rose 3.5% in March from a year earlier, the Labor Department said Wednesday. That was a touch higher than economists had forecast and a pickup from February’s 3.2%. So-called core prices, which exclude volatile food and energy categories, also rose more than expected on a monthly and annual basis. (…)

Futures contracts tied to the federal-funds rate show traders see rates ending the year around 5%, according to FactSet, implying just one or two quarter-point cuts this year. Entering January, traders had expected the Fed to cut interest rates six or seven times. (…)

Wednesday’s report had been hotly anticipated because Fed leaders had been willing to play down stronger-than-anticipated inflation readings in January and February as reflecting potential seasonal quirks. But a third straight month of above-expectations inflation data erodes that story and could lead Fed officials to postpone anticipated rate cuts until July or later.

Fed officials have been optimistic about achieving a so-called soft landing in which inflation slows without a sharp downturn in economic activity. To do that, some officials wanted to cut rates pre-emptively before the economy weakens notably. The latest report sets back that effort by depriving them of a credible justification for cutting rates, and it could prompt them to hold rates at their current level, the highest in 23 years, until they see more cracks in the economy. (…)

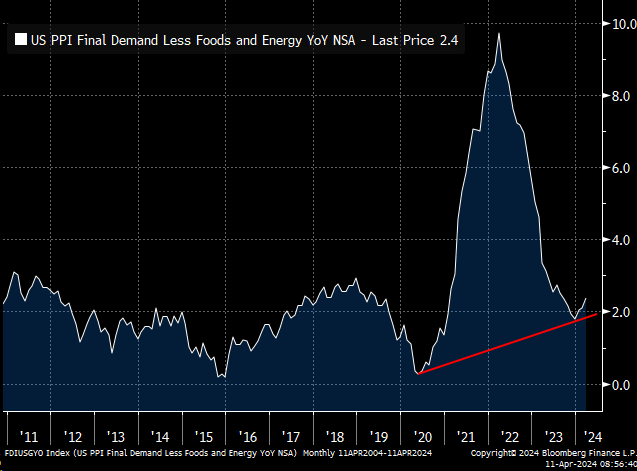

The overall core index climbed 0.4% from the previous month despite a decline in the prices of goods such as new and used cars and trucks. A problem area was services outside of housing. That category, which includes everything from car insurance to medical care, has been flagged by Fed officials as particularly important because it can be sticky and closely linked to strength of the labor market.

The cost of shelter also increased 0.4% from February, continuing to defy predictions that it would start rising more slowly given private-sector indexes that have shown a marked slowdown in new rents. (…)

On January 29, my post So, You Think You Can Disinflate? debunked the prevailing widespread conviction that Fed policies were causing the so-called “immaculate disinflation”:

So how could inflation “disappear” when demand was so strong, actually accelerating?

- Non-fuel import prices have been negative YoY since March 2023 after exploding in 2020-22. Since most U.S. consumer goods are imported, this largely explains the goods deflation experienced in 2023. Durable goods prices have declined every month since last June, –4.6% annualized in H2’23. Chinese goods import prices have been deflating all of 2023 and were down 3.0% YoY in December.

- The U.S. dollar jumped 13% between mid-2021 and the end of 2023, further reducing import costs.

- Oil prices are down 37% since their peak in June 2022. On a YoY basis, WTI prices dropped 18.1% in 2023. Natural gas prices are down 78% since their August 2022 peak and 61% YoY in 2023. Significantly lower energy costs (heating, cooling, lighting, transportation, manufacturing) helped protect corporate margins last year, alleviating the need to raise prices to offset other cost increases, such as labor.

In truth, this so-called American “immaculate disinflation” is really the result of the U.S. having imported deflating goods with a strong currency coupled with very significant corporate cost reductions from much lower energy prices.

In truth, the Fed’s policies had little, if anything, to do with this recent disinflation, other than, perhaps, higher interest rates having prevented demand from exploding even more…

The March CPI is the 3rd consecutive “bump” on Powell’s disinflationary road. On a quarterly basis, core CPI picked up to an annualized rate of 4.2% in Q1, from +3.4% in Q4’23. Annoying bump, if not an actual jump!

Core CPI MoM%, 3M annualized and YoY% changes

Source: Macrobond, ING

Perhaps the only “good” data in that CPI report is that CPI-Rent rose 0.37%, down from +0.41% in February, right on the Q1 average of +0.37% or 4.5% annualized. Goldman Sachs said the shelter data were “well behaved”.

Wells Fargo, which became more dubious on slowing rentflation after the February print, now says:

Services inflation, however, remains relatively stubborn. The core services index rose 0.5% in March, pushing the three-month annualized rate up to 6.8%. The sharp slowdown in “spot” rents measured by private sector sources remains painstakingly slow to manifest in the CPI. Primary shelter rose 0.4% again in March, with a slight moderation in rent of primary residences set against an unchanged rate of growth in the much-larger owners’ equivalent rent component. We continue to look for shelter inflation to cool this year, but another firm print in March keeps the caution flag up about the timing and extent to which housing inflation will materially slow.

Ed Yardeni is right saying that “Fed officials are likely to be alarmed by the jump in the CPI services inflation rate less rent of shelter. It rose sharply from 2.8% y/y last September to 5.3% in March. It tracks the less volatile “supercore” PCED inflation rate for services less energy and housing.”

The Atlanta Fed’s sticky-price consumer price index (CPI)—a weighted basket of items that change price relatively slowly—increased 5.0% annualized in March, following a 4.0% increase in February. On a year-over-year basis, the series is up 4.5%.

Here’s how David Rosenberg simply dismisses sticky inflation:

It is the “core sticky” price index, which has nothing to do with the contours of the business cycle and is inherently insensitive to Fed policy. That is the culprit: +0.4% MoM for back-to-back months and picking up in March to a +4.5% YoY pace from +4.4% in February. There’s your inflation story.

Yes David, THAT is the inflation story.

Ed Yardeni, still an inflation hopeful, nonetheless makes “no cuts at all” his “base case scenario. So is a 4.75%-5.00% yield on the 10-year Treasury bond in the next few months. We’ve been expecting the stock market rally to pause and suggested taking some profits, but we still expect the S&P 500 to end the year around 5400.”

The Atlanta Fed’s Wage Growth Tracker was +4.7% in March, down from +5.0% in February. For “job changers”, the Tracker in March was +5.2%, down from +5.3% in February. For “job stickers”, the Tracker was +4.5%, down from +4.7% the prior month.

Composition-adjusted wages are still rising around 5%. (All 3-m m.a.)

Meanwhile, this “new” problem is perking up. A jump in the red line nearer the blue line would be quite a bump.

Source: Chen Zhao, Alpine Macro

Source: Chen Zhao, Alpine Macro

Remember that the two major factors impacting services inflation are wages and energy.

(…) At a press conference after the decision, Mr. Macklem refused to put a timeline on when the bank would start easing monetary policy. But he did say a rate cut at the next meeting in June was “within the realm of possibilities,” as members of the governing council become more confident that inflation is heading back to the 2-per-cent target.

Both headline and core inflation fell more than expected in January and February, and a number of the bank’s indicators of future price pressures are easing.

“We are seeing what we need to see, but we need to see it for longer to be confident that progress toward price stability will be sustained,” Mr. Macklem said. “The further decline we’ve seen in core inflation is very recent. We need to be assured this is not just a temporary dip.” (…)

Mr. Macklem said that the governing council had discussed the possibility of a rate cut this week, but that there was a clear consensus to remain on hold for now. He said the officials remain wary of cutting interest rates too soon or moving too quickly once rate cuts start.

”We don’t want to leave monetary policy this restrictive longer than we need to. But if we lower our policy interest rate too early or cut too fast, we could jeopardize the progress we’ve made bringing inflation down,” Mr. Macklem said.

In its quarterly Monetary Policy Report, the bank downgraded its forecast for inflation and upgraded its forecast for economic growth, with the latter revision largely due to rapid population growth.

Annual consumer price index inflation hit a four-decade high of 8.1 per cent in 2022, and has been declining since then. Central bank economists now see inflation averaging 2.6 per cent this year, down from the previous estimate of 2.8 per cent.

Inflation is projected to remain close to 3 per cent in the second quarter of 2024, partly as a result of rising oil prices. It is then expected to move below 2.5 per cent in the second half of the year, led by slower price growth for shelter and food.

The bank expects inflation to reach its 2-per-cent target in 2025. (…)

Recent GDP growth, however, has come in stronger than the bank expected. The bank revised its first quarter annualized GDP forecast to 2.8 per cent from 0.5 per cent. And it upgraded its 2024 GDP forecast to 1.5 per cent from 0.8 per cent.

Much of this increase is being driven by much stronger-than-expected population growth, which has continued to drive overall economic growth even as GDP-per-capita has declined over the past 18 months.

Economic growth has also received a boost from the exceptionally strong U.S. economy, which has supported Canadian exports, as well as several idiosyncratic factors, such as the end of public sector strikes in Quebec. (…)

The bank noted that government spending is projected to pick up from 2.5 per cent in the second half of 2023 to 3.5 per cent in the first half of 2024, based on recent provincial government budgets. That estimate does not include spending in the upcoming Federal government budget, which will be delivered on April 16.

In the past, Mr. Macklem has warned that increased government spending could get in the way of inflation coming down. (…)

Alongside its updated forecasts, the bank also increased its estimate of the “neutral rate” by a quarter percentage point. The neutral rate is the bank’s estimate of where the policy rate would settle if inflation were on target and the bank was neither trying to stimulate nor restrain the economy.

The new estimate puts the neutral rate between 2.25 per cent and 3.25 per cent. This revision was driven largely by the U.S. policy makers increasing their neutral rate estimate, although there were also domestic factors involved, including changing demographics and savings patterns in Canada.

The neutral rate is a long-term concept, and in the press conference, Mr. Macklem said that the revision is not having an impact on the bank’s near-term monetary policy decisions.

ECB to set up June rate cut after rapid inflation fall

China’s public finances are being strained by a shaky economy, a prolonged property slump and a rising fiscal deficit.

That is the verdict of global credit-rating company Fitch, which revised its outlook for China’s A+ credit rating from stable to negative on Wednesday, while also affirming the rating. (…)

The move followed a similar change by Moody’s Investors Service in December. The New York-based firm kept China’s long-term rating of A1 intact but changed the outlook from stable to negative. (…)

China’s local governments are facing a mountain of liabilities, with some analysts putting their hidden debt as high as $11 trillion. They were squeezed by the real-estate slowdown, since for years land sales provided a steady stream of income to local governments and made up for shortfalls elsewhere. Local government-financing vehicles, which allowed regional governments to fund off their own balance sheets, compounded the pain.

The debt problems in the country’s local governments have forced Beijing to take a bigger role in financing economic growth. In March, China said it would issue $139 billion of ultralong special Treasury bonds this year, turning what was once a crisis management tool into a regular source of funding. Beijing has also approved “special refinancing bonds” for local governments and encouraged banks to lend to them.

But that may not be enough. Fitch said China’s gradual approach to managing the debt burden of local government financing vehicles means the risks are likely to remain for some time, draining fiscal resources. It thinks China’s government debt will hit 61.3% by the end of this year, up from 56.1% in 2023.

Fitch also predicts China’s fiscal deficit will rise to 7.1% of gross domestic product in 2024, up from 5.8% last year. The credit rating company said the median fiscal deficit of countries with an A rating is 3%. (…)