Nonfarm payrolls registered an increase of 175K compared to a prior three-month average of 276K (now 269K incorporating revisions). The increase fell short of consensus expectations for a 240K gain in what is only the fourth time in the past two years the initial print undershot the consensus.

On an industry basis, job growth remained solid in healthcare & social assistance (+87K), while picking up in manufacturing (+8K). However, elsewhere the picture was underwhelming. Leisure & hospitality and construction employment slowed sharply relative to their Q1 averages, suggesting the mild winter weather and early Easter/spring breaks may have pulled some hiring forward. Government hiring also downshifted notably, up by just 8K compared to an average of 55K the prior 12 months.

Higher-wage industries also struggled to add jobs, with payrolls declining in information, professional & business services and mining, flat within the utilities industry, and up only modestly in the financial industry in April.

The weak outturn in payrolls for higher-paying industries as well as gradual loosening in labor market conditions weighed on average hourly earnings (AHE) growth over the month. AHE for private sector workers increased 0.2%, which was a tick less than the consensus and our own expectations. On a year-ago basis, average hourly earnings growth slowed to 3.9%, the first sub-4% print in nearly three years. While average hourly earnings are less encompassing than the employment cost index and prone to revision, the subdued gain in April suggests the labor market is still on track to bring some relief on the inflation front this year after the downward trend in both labor costs and inflation stalled in Q1. While the slower rate of nominal wage growth in April may be good news for the Fed’s inflation fight, in the near term it is likely to challenge consumer spending, particularly when coupled with the slower rate of job growth and another dip in the average workweek.

The more volatile household survey showed employment rising by just 25K in April. A 63K increase in unemployment helped push the unemployment rate up a tenth to 3.9%. Although still low, the unemployment rate is now 0.3ppt above its 2023 average of 3.6%. The labor force participation rate held steady at 62.7% amid an 87K increase in the labor force in the month.

It was not all bad news in the household survey. Full-time employment rose by 949K, with a 649K decline in people working part-time for noneconomic reasons. The share of the “prime-age” population that was working in April also climbed a tick and is now just one-tenth away from reclaiming the high that was reached in the summer of 2023 (chart). Household employment growth over the past year remains significantly weaker than the payroll survey, but as we discussed at length in a recent report, we do not think the household measure is presaging an imminent collapse in payrolls.

After the recent re-acceleration suggesting “no landing”, Friday’s numbers are of the “soft landing” types, close to what could be a steady state level.

We will now need to closely monitor the next few months data. Hard landings typically start with softer numbers that then metastasize. Consider:

- The March JOLTS declined 3.7% from February while Indeed’s job postings are down another 2.6% through April 19. Openings in construction abruptly declined 40% in March to levels matching pre-pandemic levels.

- This jibes with the recent sharp drop in small biz hiring plans per the NFIB, pointing to sub-100k gains in private payrolls.

- S&P Global April services PMI showed a sudden, huge drop in employment. The ISM services employment index also declined 2.6 % to 45.9 in April.

- Healthcare/Education accounted for 95k (57%) of the total 167k private new jobs in April. Excluding Healthcare/Education, total employment rose 80k in April, after averaging 210k in 2023 and 179k in Q1’24.

- Leisure/Hospitality, highly discretionary expenditures, added only 5k jobs in April and 17k on average so far this year, down from 65k in 2023.

- Government jobs only increased 8k in April compared with 47k on average in the preceding 15 months.

- As seen below, services new orders declined in April, the first contraction in six months.

- Surprise! Wrapping it all together, Citi’s Economic Surprise Index — which measures the degree to which data is coming in better or worse than expectations — has fallen back to negative and is now at its lowest level since early 2023. That’s a big change from all the “re-accelerating” talk earlier this year. (Bloomberg’s Odd Lot)

Source: Bloomberg

Hopefully, April was but a one-off, but notice the reduced contribution that both employment (blue) and wages (black) made to aggregate payrolls growth. On a YoY basis, payrolls are up a still strong 5.6% in April but unchanged MoM.

Remember that the savings rate is historically low, providing little buffer if spending power eases meaningfully. Recent comments from consumer-centric companies paint a more cautious consumer.

The next item also points to slower demand for services (68% of total expenditures) and a rare decline in services employment (86% of total employment) and lower new orders:

The seasonally adjusted S&P Global US Services PMI® Business Activity Index fell for the third month running in April to 51.3 from 51.7 in March. The index pointed to a modest monthly increase in business activity, and one that was the slowest since last November.

Rising service sector output was sometimes linked by respondents to marketing activity, while other companies cited the impact of securing new orders. New business fell overall, however, leading to the slowdown in growth of activity.

The reduction in new business was the first in six months and often linked by companies to a reluctance among clients to spend or commit to new projects. In some cases, this hesitancy was due to high interest rates. That said, the drop in new orders was only slight.

New business from abroad was also down modestly at the start of the second quarter, and has now fallen for three consecutive months.

The drop in total new orders meant that incoming work was insufficient to replace completed projects, thereby leading service providers to deplete outstanding business. Backlogs were down for the third month running, albeit at a modest pace that was the softest in this sequence.

Employment also decreased in April, thereby ending a period of job creation stretching back to July 2020. Those respondents that lowered their workforce numbers often suggested that this was done through not backfilling positions after staff had left.

Despite the drop in employment, wage pressures remained a key factor pushing up input costs in April. Higher oil and gas prices were also reported. As a result, input costs rose sharply again and at a pace that was faster than the pre-pandemic average for the series. That said, the rate of inflation eased from that seen in March and was only slightly above the 40-month low seen in February.

Higher labor costs were often mentioned by those respondents that increased their selling prices in April. Charges have now increased on a monthly basis for almost four years, but as was the case with input costs the pace of output price inflation moderated from that seen in March.

US service providers remained optimistic that business activity will rise over the coming year, although sentiment fell to a five-month low. Some firms were confident that current marketing efforts would bear fruit in the months ahead, while others hoped to see interest rates start to come down. There were also some predictions that demand conditions will pick up following the presidential election.

Looking at business trends across the combined manufacturing and service sectors, the S&P Global US Composite PMI Output Index posted 51.3 in April, signaling growth of business activity for the fifteenth consecutive month. The reading was down from 52.1 in March, however, and pointed to the softest expansion in the year-to-date. Weaker increases in output were seen across both the manufacturing and services sectors.

New business decreased for the first time in six months amid renewed contractions in both monitored sectors. New business from abroad ticked higher, but growth here was limited to manufacturing.

Employment also decreased, ending a 45-month sequence of job creation. The fall was centered on the services sector as manufacturing employment continued to increase.

Both input costs and output prices rose at softer rates at the start of the second quarter.

Meanwhile, business confidence ticked down but firms remained optimistic overall that output will increase over the coming year.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, said:

“Service sector growth slowed in April to point to a sluggish start to the second quarter for the US economy. Alongside a concomitant cooling in the rate of growth of manufacturing output, the weaker service sector performance means overall business activity grew in April at the slowest rate seen so far this year. At current levels, the PMI indicates that GDP is expanding at a modest annualized rate of approximately 1.5% so far in the second quarter.

“Demand has weakened, as signaled by the first fall in new orders for goods and services for six months, in part a reflection of both businesses and households adjusting to higher costs and the prospect of higher for longer interest rates. Business optimism has likewise cooled, dropping to the lowest since November, and companies are taking a more cautious approach to staffing levels.

“From an inflation perspective, the April survey brought some good news in that prices charged for services rose at a much reduced rate, registering one of the smallest increases seen over the past four years as greater competition and lower wage growth were reported to have taken some of the heat out of price setting.”

- The ISM services index decreased by 2.0pt to 49.4 in April, below expectations for a modest increase. The underlying composition was weak, as the business activity component declined to its lowest level since May 2020 (-6.5pt to 50.9), and the employment (-2.6pt to 45.9) and new orders (-2.2pt to 52.2) components also declined. The supplier deliveries component increased by 3.1pt to 48.5 (nsa) and the new export orders index deceased 4.8pt to 47.9 (nsa). The prices paid measure increased by 5.8pt to 59.2 (sa). (GS)

The performance of Canada’s service sector remained subdued during April, with activity falling for an eleventh successive month. However, the rate of contraction was marginal as new business volumes stabilised, whilst employment increased marginally. Cost pressures persisted, and firms were able to increase their own charges to the steepest degree since last July. Confidence in the future remained positive, although sentiment softened to a three-month low and remained below its historical trend.

The headline index recorded 49.3 in April to signal an eleventh successive monthly fall in business activity. However, with the index improving from 46.4 in March to its highest since June 2023, the rate of contraction signalled was only marginal and noticeably weaker.

The slower decline in activity in part reflected a stabilisation of incoming new business volumes. Latest data showed no change in new work, thereby putting an end to an eight-month period of contraction. Panellists indicated that new projects and some unexpected client wins had led to some growth in new work. However, high interest rates and subdued underlying demand limited any gains. Moreover, new export sales continued to fall (albeit only marginally) amid reports of a lack of enquiries from foreign clients.

Despite broadly underwhelming trends in activity and new business, a marginal increase in employment was recorded for the third time in the past four months. Companies that took on additional workers generally did so to support new projects or sales efforts. Extra workers also helped firms to comfortably keep on top of their workloads, with business outstanding down for a twenty-second successive month in April, though only marginally.

Positive projections for activity also helped to support a rise in employment. Latest data showed that firms retained confidence in the outlook amid hopes that improved market conditions will support higher sales and activity. That said, elevated interest rates remain a concern for many panellists, with several signalling that recession risks in the outlook persist. Subsequently, confidence slipped in April to its lowest level for three months.

On the price front, typical operating costs increased sharply again during April. Wages remained a key source of higher operating expenses, although there were also reports that changes to carbon pricing had driven up fuel costs. More generally,vendors were said to be raising their prices. Service providers responded by increasing their own charges to the greatest degree since July 2023.

Private sector economic output in Canada fell in April, as reflected in the S&P Global Canada Composite PMI Output Index* which remained below the crucial 50.0 no-change mark for an eleventh successive month. That said, with only slight declines in output seen in the manufacturing and service sectors, the overall decline was slight and the weakest since last June. A similar trend was seen for new orders, with the overall contraction the softest in nine months.

Employment growth was sustained for a fourth successive month, with marginal gains seen across both manufacturing and services economies. Firms were able to keep on top of their overall workloads, with a slight fall in unfinished business signalled.

Meanwhile, input cost inflation remained elevated, despite softening slightly since March. Output charges increased at a stronger pace, with inflation accelerating to a nine-month high.

Finally, companies are confident that activity will rise over the coming year, although optimism softened slightly to a three-month low.

The seasonally adjusted HCOB Eurozone Composite PMI Output Index posted above the 50.0 mark which separates growth from contraction for a second successive month in April. Rising from 50.3 in March to 51.7, the headline index pointed to a moderate expansion in total business activity, but one that was nevertheless the sharpest in close to a year.

A solid and accelerated increase in output across the service sector drove recovery efforts across the euro area in April as manufacturing production continued to decline.

All five of the euro area countries for which composite PMI data are available saw business activity levels rise at the start of the second quarter, albeit to varying degrees. As was the case in the opening quarter of 2024, Spain was the top-performing economy,  with growth quickening to a one-year high. Italy recorded a fourth consecutive month of growth, despite the upturn cooling from March. Of note were trends in the eurozone’s two largest economies, Germany and France, which saw overall levels of economic activity rise for the first time in ten and 11 months, respectively. Expansions here were only marginal, however.

with growth quickening to a one-year high. Italy recorded a fourth consecutive month of growth, despite the upturn cooling from March. Of note were trends in the eurozone’s two largest economies, Germany and France, which saw overall levels of economic activity rise for the first time in ten and 11 months, respectively. Expansions here were only marginal, however.

Increased sales supported greater business activity in April. New orders placed with private sector firms in the eurozone rose for the first time since May last year, albeit only marginally, as a steeper fall in demand for goods partially offset greater new business at services companies. The latest survey data also suggest that the rejuvenation of sales activity was domestic-driven, as new export business fell for a twenty-sixth consecutive month.

Backlogs of work were also a factor underpinning higher output levels in April. That said, the rate at which incomplete orders were depleted slowed for a third month in a row and was the weakest in a year. Looking ahead, companies in the eurozone were optimistic that activity levels would continue rising in the coming 12 months. The level of positive sentiment was only narrowly weaker than March’s 25-month peak.

Euro area companies hired additional staff during April, extending the current period of job creation that commenced at the turn of the year. The rate of employment growth was the sharpest since mid-2023.

Turning to prices data, the latest HCOB PMI survey signalled stronger inflationary pressures across the euro area in April. After slowing in the previous month, increases in both input costs and output charges quickened and were above their respective series averages. Increases in operating expenses and selling prices remained historically steep in services, more than offsetting continued (albeit slower) decreases across the manufacturing sector.

Having signalled growth in the two prior months, the HCOB Eurozone Services PMI Business Activity Index signalled a strengthening of the euro area’s service sector recovery in April as it rose from 51.5 in March to 53.3. Overall, this pointed to the strongest expansion in services activity in just under a year.

Stronger demand conditions were a key reason for April’s sharper upturn in output, with new business volumes rising for a second successive month and at the quickest pace since May last year. The pick-up in sales led to an increase in the amount of work pending completion for the first time in ten months. The rate of backlog accumulation was only marginal, however.

Rising new business, in tandem with growing capacity pressures, led euro area service sector employment growth to accelerate. The rate of job creation was solid and the fastest since mid-2023. Business confidence dipped slightly from March’s 25-month peak but was strong overall and in line with the long-run average.

Price pressures crept up slightly across the euro area services economy in April. The rate of input cost inflation quickened from March’s eight-month low, albeit only marginally. Output charges also rose at a faster pace.

Commenting on the PMI data, Dr. Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said:

“This looks pretty nice. Service providers have now expanded their activity for the third consecutive month, putting an end to the lack of dynamism observed in the second half of last year. Encouragingly, employment has increased at a faster rate, aligning with the uptick in new business and the growth of the order book, which has seen its strongest expansion in eleven months. These trends suggest a growing optimism among service providers, a sentiment further bolstered by business expectations, which are currently at much higher levels compared to the average of the past two years.

“Productivity poses a significant challenge for the services industry and the ECB. Since early 2021, service providers have consistently expanded their staff, even during the weaker phases of 2022 and 2023. This trend suggests that companies, faced with staff turnover, may need to hire multiple individuals to maintain the same level of output, indicating reduced productivity.

Meanwhile, the PMI index for operating costs in the service sector, which largely comprises unit labour costs, has continued to increase at a rapid pace over the past twelve months, following a sharp uptick in 2022. The ECB is cognizant of this trend and is likely to proceed cautiously with regards to the extent of rate cuts.

“Service companies successfully passed on a portion of the increase in operating costs, indicating improving demand conditions. It means also that the market structure is characterized by healthy competition without being excessively destructive.

“Spain is outpacing Germany, Italy, and France, with its Services PMI remaining several points ahead of its peer economies. Despite political turbulences, Spain appears to be capitalizing disproportionately on tourism. Moreover, according to the IMF, the Spanish government is less focused on austerity measures compared to other top eurozone economies, meaning less of a break on the economy.”

The seasonally adjusted headline Caixin China General Services Business Activity Index fell to 52.5 in April, down from 52.7 in March. Although slightly softer, growth was again solid and has now been sustained for 16 consecutive months.

Central to the latest expansion in services activity was another rise in new business. After adjusting for seasonality, the volume of new work also expanded for the sixteenth month in a row. Moreover, the pace of growth was the fastest since May 2023 and solid overall. Panellists attributed the rise in new work to improved demand conditions and a broadening of customer bases on the back of business development efforts.

In line with overall new business, foreign demand for China services also rose in April. New export business increased at the fastest pace in ten months. Anecdotal evidence signalled that better external market conditions and rising tourism activity had supported the latest uptick in new business from abroad.

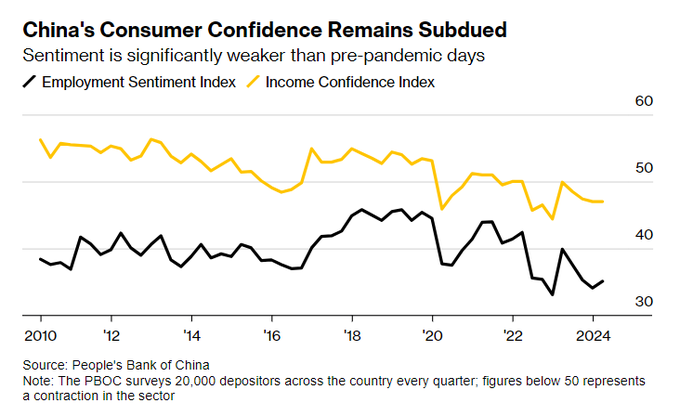

Meanwhile, work outstanding was little changed in April and this lack of capacity pressure led to Chinese service providers cutting their employment levels for a third straight month in April. Panellists reported that job shedding reflected a mixture of resignations and redundancies.

Overall business sentiment improved among Chinese service providers in April to the highest level since last December. There are hopes that market conditions can improve in the year ahead, which should spur new sales and activity at units.

Finally, average input costs continued to increase in the service sector during April. The rate of inflation rose slightly from March on account of higher input material, labour, and energy costs, but remained below its long-run survey average. In contrast, output price inflation, though mild, rose further above the series average in April as firms sought to share rising cost burdens with clients.

The Composite Output Index rose to 52.8 in April, up from 52.7 in March, to indicate a sustained expansion of overall Chinese business activity for the sixth successive month and at the fastest pace since May 2023. Underlying data revealed that output growth accelerated in the manufacturing sector but slipped slightly in services.

Composite new orders likewise rose at the fastest pace since last May,attributed to faster expansions in both manufacturing and service sectors. However, employment levels declined for a third straight month.

Rising input cost inflation, partly due to renewed manufacturing input cost inflation, meanwhile underpinned an increase in average selling prices.Business confidence was unchanged in April.

BTW:

China’s Politburo held its quarterly review of China’s economy last week and released an important statement which indicated a change in the government’s strategy to address the housing crisis. The previous strategy, loan guarantees and more social housing, did little to reduce the oversupply pressuring prices and causing much angsts in the population. Policymakers now want to tackle the oversupply problem (“study how to digest the existing housing inventory and optimize the new housing supply”). Easier said than done but a step in the right direction.

The Politburo also announced that the long-awaited “Third Plenum” will be held in July. This could result in long-awaited structural reforms to China’s tax/fiscal system and social safety net to address “insufficient domestic demand“.

EARNINGS WATCH

From LSEG IBES:

397 companies in the S&P 500 Index have reported earnings for Q1 2024. Of these companies, 76.8% reported earnings above analyst expectations and 16.9% reported earnings below analyst expectations. In a typical quarter (since 1994), 67% of companies beat estimates and 20% miss estimates. Over the past four quarters, 79% of companies beat the estimates and 17% missed estimates.

In aggregate, companies are reporting earnings that are 8.4% above estimates, which compares to a long-term (since 1994) average surprise factor of 4.2% and the average surprise factor over the prior four quarters of 7.0%.

Of these companies, 60.9% reported revenue above analyst expectations and 39.1% reported revenue below analyst expectations. In a typical quarter (since 2002), 62% of companies beat estimates and 38% miss estimates. Over the past four quarters, 65% of companies beat the estimates and 35% missed estimates.

In aggregate, companies are reporting revenues that are 0.8% above estimates, which compares to a long-term (since 2002) average surprise factor of 1.3% and the average surprise factor over the prior four quarters of 1.5%.

The estimated earnings growth rate for the S&P 500 for 24Q1 is 7.1%. If the energy sector is excluded, the growth rate improves to 10.2%.

The estimated earnings growth rate for the S&P 500 for 24Q2 is 11.1%. If the energy sector is excluded, the growth rate declines to 10.6%.

The estimated revenue growth rate for the S&P 500 for 24Q1 is 3.5%. If the energy sector is excluded, the growth rate improves to 4.1%.

Impressive!

But apparently not quite enough for Mr. Buffett:

Our cash and Treasury bills were $182 billion at the quarter end [+$17.3B in Q1] and I think it’s a fair assumption that they’ll probably be at about $200B at the end of this quarter…We’d love to spend it, but we won’t spend it unless we think they’re doing something that has very little risk and can make us a lot of money…I don’t think anybody sitting at this table has any idea of how to use it effectively…I don’t mind at all under current conditions building the cash position. When I look at the alternatives, what’s available in equity markets and the composition of what’s going on in the world, we find it quite attractive. (Warren Buffett)