NFIB: Nearly Half of Small Businesses Unable to Fill Job Openings

“Small business owners are struggling at record levels trying to get workers back in open positions,” said NFIB Chief Economist Bill Dunkelberg. “Owners are offering higher wages to try to remedy the labor shortage problem. Ultimately, higher labor costs are being passed on to customers in higher selling prices.”

U.S. Consumer Credit Usage Remains Steady During April

Consumer credit outstanding grew $18.6 billon during April, the same as in March, revised from $25.8 billion. February’s increase was revised to $18.2 billion from $26.1 billion. A $20.0 billion April rise had been expected in the Action Economics Forecast Survey. The ratio of consumer credit outstanding-to-disposable personal income rose m/m to 22.5% compared to 23.9% during all of last year and 25.7% during 2019.

Nonrevolving credit usage increased $20.6 billion, the strongest rise since June of last year. (…)

Revolving consumer credit balances declined $2.0 billion after a $1.4 billion March rise. Balances had been falling throughout 2020. (…)

The Fed’s Risky Fill-the-Punch-Bowl Strategy Growth is surging, the housing market is hot, and inflation is on the rise. It’s time to pull back.

Kevin Warsh, a former member of the Federal Reserve Board, writes in the WSJ:

(…) The Federal Reserve announced a new policy doctrine almost a year ago. In essence, the Fed said it would no longer consider lags when making monetary policy, forsaking the policy of “pre-emption” that was standard under Fed heads Paul Volcker, Alan Greenspan, Ben Bernanke and Janet Yellen. Jerome Powell’s Fed believes the party is just getting started and won’t remove the punch bowl until the fun is in full swing and the neighbors know it. Most in Washington can barely contain their enthusiasm for the new doctrine. Wall Street loves it too. (…)

Real economic growth is surging more than it did during the Reagan years. U.S. government spending is growing at the fastest clip since World War II. The housing market is running hotter than it did in the runup to 2008. Financial-market ebullience is stronger and broader than during the dot-com boom at the turn of the century. And economic output will shortly surpass historic highs. (…)

[The Fed might be right but] The risks the Fed is taking with its winsome forecast are significant, and the consequences of policy error are severe. (…)

No other major central bank has adopted anything like the Fed’s new framework. The People’s Bank of China has already removed significant accommodation. The Bank of Canada announced meaningful steps toward normalization. The Bank of Korea signaled interest in somewhat tighter policy. I expect other Group of 20 central banks to move further from the Fed’s policy in the coming months.

The resulting U.S. dollar weakness—in train since last fall—poses a host of dangers, including inflation risks. The Fed says it has the tools to stop an inflationary surge, but its new regime promises a tardy response. Late by design, the Fed would have to tighten policy more to stop an inflationary surge. (…)

If the Fed doesn’t begin action imminently, it may be too late. Others will fund the nation’s profligacy even after economic growth slows and the debt burden grows. But what interest rate investors will demand for the privilege?

Most large foreign buyers, including China, departed the Treasury auction market when the pandemic hit and haven’t meaningfully returned. Many foreign entities believe the Fed is monetizing the fiscal expansion and expect the new policy experiment to end badly. Leaders in China are poised to capitalize on an American policy error. (…)

The Biden administration might wonder if—in the absence of Fed intervention to keep interest rates exceptionally low—it can rely on the kindness of strangers to fund its grand ambitions. (…)

The Fed should change its policy regime. It should stop buying mortgage securities immediately. Soon after, it should slow its purchases of Treasury debt. It should not tolerate Fed-financed fiscal expansion. It should unlock the handcuffs imposed by its novel doctrine and render an informed and humble judgment on the state of the economy and the attendant risks to the outlook.

In May, the Institute of Supply Management (ISM) reported that lead time for production materials jumped to 85 days, up from 79 in April. The May reading is an entire work-day month (21 days) above the level from one year ago and the highest reading since 1979, or when ISM has been using the current methodology to track lead times.

Leadtimes are a valuable indicator of current and future demand. When backlogs rise and get stretched out, firms protect their production schedules by building safety stocks and placing long-dated orders for materials and supplies to meet expected future demand.

The current generation of policymakers probably does not follow lead times, but the old generation did. (…) Former Federal Reserve Chairman Alan Greenspan religiously tracked lead times, order backlogs, and delayed deliveries (i.e., vendor performance or nowadays called supplier delivery index) as signs of future inflation and inventory building. The latter is an essential part of demand-driven fast growth and inflation cycles since it adds a layer of demand, putting more pressure on prices.

In May, a record low 28% reading for the customer inventories index and a relatively high price index reading of 88% accompanied the record high reading for lead times. The old generation of policymakers would see these data points as evidence of a more general emergence of inflation pressures.

(…) the current generation of policymakers is running with a policy approach–doing nothing— that has never even been used to break an inflation cycle. In the past, delays in enacting monetary restraint triggered bad outcomes, so the odds of a successful outcome from a doing nothing policy approach seem very low, probably as low as the federal funds rate (0.06%).

- One Reason U.S. Treasuries Don’t Seem That Worried About Inflation Yields on government bonds might be agreeing with the Federal Reserve that price pressures are transitory, but they could also just be artificially low thanks to a constellation of arcane money market rates.

(…) The implication here is that a technical source of demand — banks buying U.S. Treasuries to satisfy liquidity requirements — has effectively put a lid on yields and potentially stripped them of some informational value regarding exactly what the market thinks of inflation risks. U.S. Treasury yields might be agreeing with the Federal Reserve that price pressures are transitory, but they could also just be artificially low thanks to a constellation of arcane money market rates. (…)

- Economist Who Said Inflation Was Dead Now Thinks It’s Alive Roger Bootle wrote the book about the taming of consumer prices in the 1990s and now sees a different course that will shape debate at central banks around the globe.

(…) “The danger of deflation has passed, and the risks have definitely tilted in the other direction. How high inflation will go, and for how long, that’s debatable. But I’m not in much doubt myself that there’s been a sea change.” (…)

“If I had to put my money on a single factor that was going to push up costs in the years to come, I would say it was the environmental emphasis and in particular the drive towards net-zero. This is going to lead to a whole series of costs and price increases across the economy.

“The second element is demand. In the era before low inflation, it was common for policymakers and academics to completely ignore supply side institutional factors as being quite irrelevant — it’s all about money.

“When you look at the demand factors, it’s pretty striking. We’re entering in a period when demand is going to be strong. We’ve got this pent-up demand because of Covid. You’ve got people with lots of money.

“I’m not sure complacency is quite the right word. I think it’s over-optimism with regard to inflation, but on two counts. One that’s it’s not going to go up that much, at least not sustainably. And two, if it does, as and when they need to, they’re going to be able to contain it.

“Policymakers have a natural inclination to lay off and think it’s all going to get sorted out. I think actually the conclusion ought to be quite the opposite. Because of the dangers, in this world, of big rises in interest rates, they ought to start rising raising interest rates sooner and moving by low amounts stealthily, in order to get interest rates up somewhere near a more normal level rather than being forced into it.” (…)

“A closer comparison is with the 50s and 60s before the inflationary take off at the end of the 60s. We then went through a long, a prolonged period of what seemed at the time by the way to be quite high inflation — we learned subsequently it wasn’t.”

Southwest Airlines Automates Some Job Recruiting Tasks as Air Travel Takes Off “The labor market is probably as tough as I’ve ever seen it, and so we’ve got to be able to move with speed, and that’s where all these tools come into play,” said Greg Muccio, the airline’s director of talent acquisition.

INFLATION WATCH

- From the (WSJ):

- “We are being hit from every possible angle,” said Franz Hofmeister, chief executive of Quaker Bakery Brands Inc. in Appleton, Wis. He says his costs for items including wheat, energy and new aluminum equipment have shot up at least 25% to 35% this year. Customers protested when his firm lifted prices for pizza crusts, burger buns and other goods by as much as 8%, but more increases might be needed. “The scary thing is, we don’t really see an end in sight to these cost pressures,” he said. (WSJ)

- At Hong Miao Toy, which produces dinosaur and educational toys in the city of Chenghai, founder Matt Lin says the company’s profit margins have fallen 30% this year. “I haven’t seen any raw material whose cost hasn’t gone up this year,” Mr. Lin said. “I don’t think we will ever return to the time before Covid.” He expects plastics costs to go higher as crude oil rises.

- Increased steel prices have added about $515 to the cost of an average U.S. light vehicle, according to Calum MacRae, an auto analyst at GlobalData.

- BSA Machine Tools, which makes lathes and other machines used in manufacturing, has been pushing back as suppliers of steel, aluminum and other components try to increase prices. (…) But in January, the company raised its own prices by around 5% to 6% to reflect extra costs. “We have no choice,” he said.

- Taiwan’s Covid-19 outbreak spreads to chip companies Disruptions to semiconductor groups comes as industry battles global shortage

- Cruise Ticket Prices Higher vs. 2019 Across All Operators (JPM)

- 5 reasons global shipping costs will continue to rise

1. Continued global imbalances push prices up further

Problems that had built up from the beginning of the pandemic have included imbalances in the production and demand for goods, with countries locking down and opening up at different times, as well as shipping companies cutting the capacity on major routes and shortages of empty containers. As the recovery has progressed, global demand has recovered strongly, especially in the sectors which are most closely linked to international trade in goods. Competition for ocean freight capacity has intensified as economies open up further and inventories are rebuilt across the several links of supply chains.

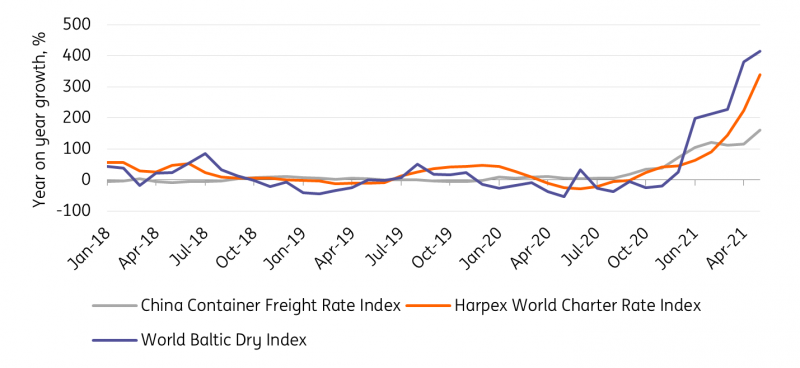

Global shipping costs

Year on year growth in freight rate indices, 2018 – May 2021

Source: China Ministry of Transport, Harper Petersen & Co. and Baltic Exchange via Macrobond, ING2. Few alternatives to ocean freight

A lack of alternatives to ocean freight means it’s hard to avoid surging transport costs at the moment. For higher value products, alternative modes of transportation would normally be an option, such as the shipment of electronic devices by air or via train, not least through the ‘Silk Road’. But capacity is currently limited, and tariffs have spiked as well. Shippers of lower value products such as household items, toys, promotional articles or t-shirts have seen freight costs increase from around 5% of their sourcing costs to more than 20%.

The difficulty of absorbing increases on this scale in margins means that consumers may start to feel the impacts through price increases, or changes in product availability.

3. An unbalanced recovery throughout 2021

Some counties are already exporting more goods than they did before the pandemic, while in others, including the US, exports continue to lag behind the overall recovery in output. Trade in goods will rise further while not only the major trading countries, but also their trade partners, continue recovering. With the competition for ocean freight capacity set to remain, the unbalanced recovery will continue to exacerbate some of the problems for world trade, including displaced empty containers. It all adds up to more pressure on freight rates in the near term.

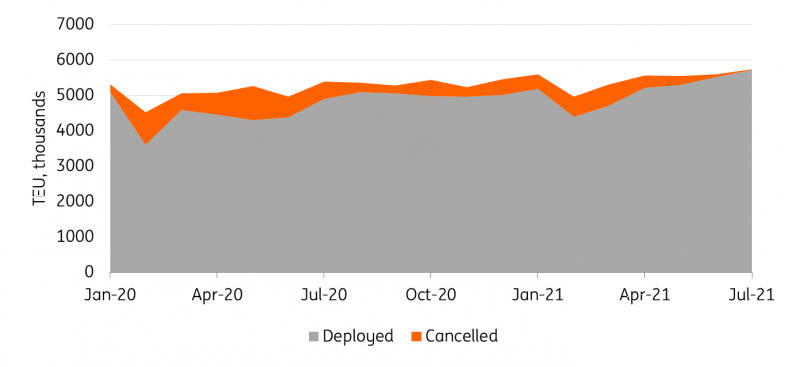

4. Reduced blank sailings will help ease capacity constraints

Globally, capacity on major shipping routes has recovered to levels before the major lockdowns in 2020, although blank sailings (cancelled port calls) continued to cut 10% of scheduled capacity through the first quarter. There are signs of improvement this quarter, which on current plans will average at 4%. But cancellations have partly been a response to delays, so while the system remains congested, shipping capacity may continue to be taken out of the system at short notice.

Deployed and cancelled shipping capacity

Total capacity on routes between Europe, North America and Asia

Source: eeSea, ING

5. Port congestion and closures keep creating delays

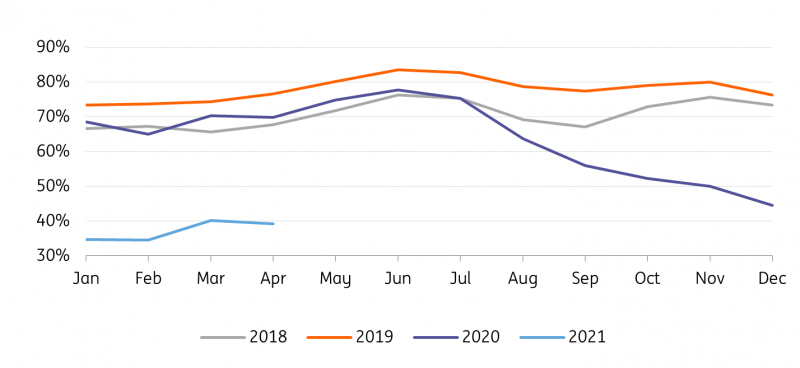

As the link between cancelled sailings and delays suggests, congestion is part of the problem. Shipping performance in 2021 has carried on where 2020 left off, in terms of lower rates of vessels keeping to schedule, and average delays for late vessels rising. There are some signs that average performance will start to improve as the share of vessels reaching their destinations on time stopped sliding in April, and average delays improved. But overall performance remains the lowest it has been in ten years of records.

Share of vessels arriving on time

Source: Sea-Intelligence, ING

At the same time, the pandemic is still leading to disruptions, like the sudden closing of China’s Yantian container port – part of the world’s 4th largest container port Shenzhen – in early June. Even though operations have resumed, congestion and the continuing need for measures to stop the spread of Covid-19 mean delays continue to mount. Although China and other major trading countries are making progress with vaccination programmes, creating immunity will take time and consequently handing interruptions will remain a risk over the coming months.

Container liners have enjoyed outstanding financial results during the pandemic, and over the first 5 months of 2021, new orders for container vessels reached a record high of 229 ships with a total cargo capacity of 2.2 million TEU. When the new capacity is ready for use, in 2023, it will represent a 6% increase after years of low deliveries, which the scrapping of old vessels is not expected to offset. Along with global growth moving past the catch-up phase of its recovery, the coming increase in ocean freight capacity will put downward pressure on shipping costs but won’t necessarily return freight rates to their pre-pandemic levels, as container liners seem to have learned to manage capacity better in their alliances.

In the near term, freight rates may yet reach new highs thanks to the combination of further increases in demand and the constraints of a congested system. And even when capacity constraints are eased, freight rates may remain at higher levels than before the pandemic.

Correlated:")

")

(Jim Paulsen, The Leuthold Group, via MarketWatch)

The Probability of a Bear Market is Rising

Now that data from May have been finalized, the Bear Market Probability model has risen to its highest level since January 2020. (…)

Bear Market Probability is a model outlined by Goldman Sachs using five fundamental inputs:

- The U.S. Unemployment Rate

- ISM Manufacturing Index

- Yield Curve

- Inflation Rate

- P/E Ratio

(…) There isn’t a lot in the table above that’s concerning. Shorter-term returns were weak, but a couple of them within an already tiny sample bucked that weakness and saw consistent strength. Over the next year, all but two record double-digit gains. It will be a more pressing concern if Bear Market Probability climbs above 70%.

China Tells Banks to Stress Test Their Evergrande Exposure

(…) While it’s not the first time regulators have required banks to report their Evergrande exposure, the directive suggests concerns about the company’s financial health have become serious enough to once again reach the upper levels of China’s government.

Evergrande bonds and shares have slumped in recent weeks amid a drumbeat of negative news, from late payments on short-term debt by some of its affiliates to a media report that authorities are scrutinizing the developer’s dealings with a bank in which it owns a major stake. (…)

Investor concerns about Evergrande’s access to funding have also increased as the developer has fallen behind peers in meeting regulatory borrowing limits known as the “three red lines.” The company remained in breach of all key measures for debt levels at the end of last year, even as almost half of the country’s 66 major developers met them, up from 14 six months earlier, according to data compiled by Bloomberg.

Evergrande said last week it would try to meet at least one of the red lines by the end of this month.

- Just last week: “The Chinese government has taken the reigns in the saga involving stricken lender China Huarong Asset Management Co., Reuters reports today, instructing Huarong to dispose of various non-core assets. More importantly for the firm’s international creditors, Beijing is set to “informally” back Huarong’s roughly $20 billion in dollar-denominated debt.” (ADG)

")