Truck Freight Demand Surged In July, Group Says The American Trucking Associations says a strengthening U.S. economy sent its shipping index to the second-highest level ever recorded

The amount of cargo hauled by U.S. truckers rose 2.8% in the latest reading of the American Trucking Associations’ monthly index. (…)

Carriers have had an up and down year since the ATA’s index hit a record high in January. (…)

The ATA sounded a note of caution, warning that high levels of inventories could hurt freight volumes in the next few months. The inventory-to-sales ratio for all businesses has reached its highest this year since the 2008-2009 recession, according to U.S. Census Bureau figures. (…)

Maybe truckers are gaining market share (vs economic snap back) since overall freight remains so-so:

Cass tends to support the market share thesis but warns it may not last:

Intermodal costs (which we measure all in, as opposed to linehaul only), on the other hand, were 2.9% below 2014 levels. The decrease comes in response to falling demand for intermodal as lower diesel prices have encouraged mode shifting to truckload. The ability for shippers to do this will remain limited, however, by tight demand in the trucking sector.

The cost of truckload shipping continues to rise, as higher contract rates continue to filter into the index. In July, average truckload linehaul rates were 3.6% higher than last year, and 11% higher than two years ago.

And from joc.com:

As the pace of the economy slowed in late 2014 and early 2015, more contract truckload capacity became available, and shippers shifted freight to contractual carrier partners.

Recall the August Empire State Manufacturing Index which plunged to –14.92 from +3.86. Not just a minor set back! This is worse than the 2010, 2011 and 2012 growth scares, yet nobody is scared. And the weakness was broad as every sub-index but one declined last month.

Significantly, new orders collapsed. New orders are the life blood in manufacturing and they have been declining since September 2014 but really evaporated last month.

CHINA FACTS

(…) container volume at the major Chinese ports rose 5 percent year-over-year in the first half of 2015 to nearly 78.2 million 20-foot-equivalent units, according to the Shanghai Shipping Exchange. (joc.com)

That is through June. July? Keep reading.

Cosco Pacific container throughput registered a meager 1.3 percent growth in July as China’s slowing exports dragged down volumes at the mainland’s second largest port operator.

- America is sending a growing number of empty containers back to Asia. For example, at the Port of Long Beach—one of the busiest ports in the world—the number of completely empty containers going to Asia was up by 24.3% in July. (Tony Sagami’s Rational Bear)

U.S. HOUSING

Seniors, Not Millennials, Are Creating New Households

The rate at which Americans are creating new households has increased over the past year to reach the highest level since before the recession began in 2007.

And it’s older Americans, not those ages 25 to 34, driving the uptick, according to new research from economist Jed Kolko of the Terner Center for Housing Innovation at the University of California, Berkeley.

Americans created 1.27 million households during the year ended in June, Mr. Kolko estimates. That’s in line with Census Department figures showing year-over-year household formation topping 1 million for three straight quarters. A similar streak hasn’t occurred since 2006.

Of those new households, 860,000, or about two-thirds, were created by Americans between 65 and 74 years old. Just 159,000, or 13%, were created by young people between 25 and 34 years old. (…)

Why that’s happening is a bit difficult to pin down. One possibility is more older adults are getting divorced.

Another factor is those 65 through 74 are the fastest-growing segment of the population and older adults live in smaller households than younger adults. “So population growth among older adults adds more households than population growth among younger adults,” Mr. Kolko wrote.

The increased number of households among young adults entirely reflects population growth rather than a smaller share are no longer living with their parents, Mr. Kolko said.

As a matter of fact:

A new report from Pew Research Center shows that a higher percentage of millennials, a group defined by Pew as adults born 1981 or later, is living with parents than in 2010, despite the ongoing recovery.

In the first third of 2015, 26% of millennials lived with their parents, up from a prerecession 22% in 2007 and 24% in 2010, when the recovery began. That translates to 16.3 million young adults in their family homes, compared with 13.4 million in 2007.

That’s despite the national unemployment rate for 18-to-34-year-olds falling to 7.7% in the first third of 2015, a significant recovery from the 12.4% rate five years prior. Wages, too, have edged up to a weekly median of $574, compared with a 2012 low of $547.

Of course, many millennials are living independently: 42.2 million of them in 2015. But that’s slightly fewer than the 42.7 million who lived independently in 2007.

(…) “This does have implications for the larger economy–the nation’s housing industry, builders, Realtors, landlords, the cable company, as well as places like Home Depot selling mops and brooms.”

Jed Kolko, an independent housing economist, suggested two headwinds were keeping young workers from living independently: declining marriage rates (married couples tend to form their own households) and rising rental costs, which have outpaced wage gains in many parts of the country.

In sought-after cities like New York, Miami and San Francisco, rental costs eat up 41% or more of the area’s median income. Burgeoning cities like Denver and Austin have also seen rents climb in recent years.

A study from the Federal Reserve Board also points to one factor that, unlike the labor or housing market, has resisted cyclical trends: student debt. As the Pew study notes, the recession drove many young adults towards higher education.

“Some enrolled in college to ride out the economic storm, while others went back to school to gain additional skills and make themselves more marketable,” the authors of the Pew study wrote.

But all that schooling came with a serious price tag. Lisa Dettling and Joanne Hsu, economists at the Federal Reserve Board, found that mean balances on student loans rose to $12,000 by early 2014, up from $5,300 in early 2005. By analyzing individual-level credit data, Ms. Dettling and Ms. Hsu show that each additional $10,000 in student loan debt makes someone 4.6% more likely to move in with a parent.

Even if student loans are a proxy for upward mobility (higher earnings might be more likely with a degree or credential), “any income effects signaled by large loan balances are swamped by a behavioral effect wherein large balances incentivize moving in with a parent,” they wrote.

But student debt tends to be distributed unevenly across the borrower population. And depending on the circumstances, a large loan balance can signal that the individual has a high capacity to borrow and feels secure taking on risk, or the opposite, that she or he has fewer resources and is forced to borrow more. Rising rents, by contrast, hit a wide swathe of the population.

“One thing that’s quite different from previous recessions is there’s a lot of inequality across areas in terms of rents,” said Hilary Hoynes, an economist at University of California at Berkeley. “The high price of housing in many of the top American cities would have the potential of affecting a large group of people.”

Speaking of student debt:

-

Grad-School Loan Binge Fans Debt Worries Graduate students represent just 14% of students in higher education but account for about 40% the $1.19 trillion in student debt. Many seek government-loan forgiveness.

(…) The doubling of student debt since the recession, to $1.19 trillion, has stoked a national discussion over how to rein in college costs and debt and is becoming a major issue in the 2016 presidential race. Little noted in the outcry is the disproportionate role played by postgraduate borrowers, who now account for roughly 40% of all student debt but represent just 14% of students in higher education.

Propelling the surge in grad-school debt is a welter of federal programs that make it easy for students to borrow large amounts, then to have substantial chunks of those debts eventually forgiven. Critics of the system say it makes it easier for graduate schools to raise tuition, and for some high-earning graduates such as doctors to escape debts they can afford to repay. (…)

Federal programs allow grad students to borrow essentially unlimited amounts—whatever their schools charge—while requiring only a scant credit check and no assessment of their ability to repay. Other government loan programs, such as those for undergraduate students and home buyers, set loan limits to prevent borrowers from getting too deep into debt. Undergraduates are capped at $57,500 total in federal loans.

As graduate-school enrollment swelled over the past decade, the number of Americans owing at least $100,000 in student debt more than quintupled to 1.82 million as of Jan. 1, New York Federal Reserve data show. The number of all student borrowers nearly doubled to 43.34 million.

(…) surging enrollment in the debt-forgiveness programs recently prompted the government to increase by $22 billion its estimate of the long-term costs of the provisions. And a recent move to expand the most generous repayment program to millions more borrowers will cost an estimated $15.3 billion. (…)

The typical college student who borrowed owed about $27,000 upon graduation in 2012, according to an analysis of federal data from the New America Foundation, a centrist think tank. Those earning a master’s typically owed between $50,000 and $60,000; law degrees, $141,000; and medical degrees, $162,000. (…)

After borrowing to earn her bachelor’s, Ms. Kurowski-Alicea says, her main motivation for earning a master’s and then a doctorate was to postpone repaying her student loans, which she said were too high for her minimum-wage income at the time. The government doesn’t require payments while students are in school.

“There’s no way to pay it afterward. It’s a continuous cycle,” says Ms. Kurowski-Alicea, of Clermont, Fla. (…)

Surge in emerging market capital outflows hits growth and currencies

A surge of capital gushing out of emerging markets has risen toward $1tn over the past 13 months, roughly double the amount that fled during the financial crisis amid slumping confidence in the world’s developing economies.

The sustained exodus of capital reinforces concerns that emerging market economies, suffering slowing growth and weakening currencies, are relinquishing their longstanding role as locomotives for global growth to become a drag on demand instead. (…)

But as the funds cascade out, a vicious circle is triggered. Currencies tumble against the US dollar, damping demand for imports and driving down aggregate demand. In June, for example, overall emerging market imports were 13.2 per cent lower year-on-year, according a moving average compiled by Capital Economics.

“The collapse in emerging market imports reflects a more fundamental drop in demand as capital outflows have forced domestic demand to shrink and lower commodity prices have eroded incomes in commodity-producing countries,” said Neil Shearing of Capital Economics. “So far, there is little sign that we have reached the bottom.” (…)

Chinese slowdown sends ripples across Asian banks Asian lenders are seeing their loan books rapidly deteriorate across the region as China’s slowing economy dampens trade and hurts companies that had borrowed heavily from the banks.

Among 23 major non-Chinese lenders, all but 6 reported an increase in soured loans in the first half of 2015, the strongest indication yet of how China’s slowdown is infecting banks’ balance sheets, data compiled by SNL Financial for Reuters show.

That trend accelerated in the second quarter, the banks’ data show.

“Second-quarter results have seen banks across Asia suffer rising bad loans after a period of historic lows in NPL levels,” said Josh Klaczek, JPMorgan head of Asia financials research. (…)

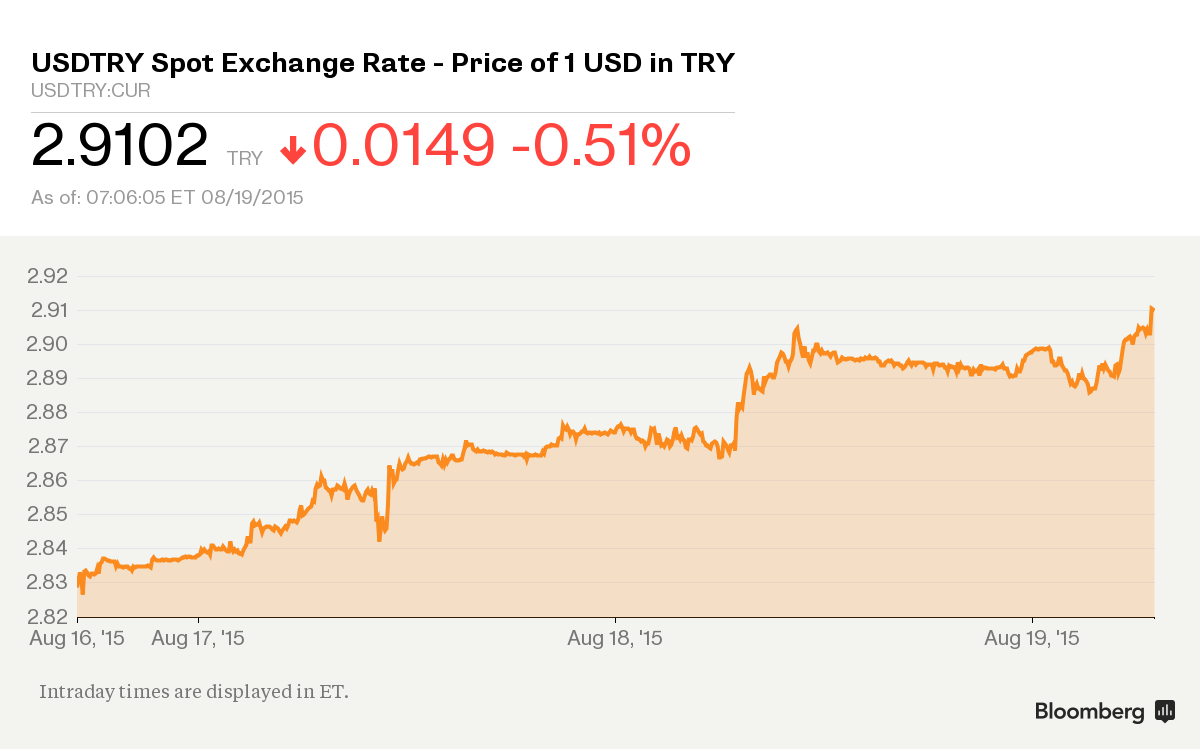

THE RACE TO THE BOTTOM:

The State Bank of Vietnam weakened its reference rate by 1 percent to 21,890 dong a dollar and increased the scope for fluctuations to 3 percent on either side, after doubling the range on Aug. 12. The dong fell 1.2 percent to 22,360 as of 3:04 p.m. in Hanoi, extending its drop this month to 2.4 percent, according to data compiled by Bloomberg. Malaysia’s ringgit leads regional losses so far in August with a 6.4 percent slide. (…)

“The dong will have enough room to fluctuate more flexibly to cope with negative impacts from international and domestic markets, not only from now until the rest of the year but also in early months of 2016,” the authority said in a statement on Wednesday.

The Vietnamese currency has declined 4.4 percent this year, putting the country’s exporters at a relative disadvantage to those in nations like Malaysia and Indonesia, whose currencies have fallen 15 percent and 11 percent, respectively. (…)

China has been Vietnam’s biggest trade partner since at least 2007.

Kazakhstan allowed its tenge to weaken the most since a devaluation 18 months ago, signaling Central Asia’s biggest crude exporter wants to adjust to declines in the currencies of its top trading partners, China and Russia.

The tenge declined 4.4 percent to 197 per dollar by 2:29 p.m. in Almaty. That was the steepest retreat since February 2014 when the central bank, which uses its foreign-currency reserves to manage the exchange rate within a trading band versus the dollar, depreciated it by about 20 percent.

Copper Below Key $5,000 Level Copper futures dipped below $5,000 for the first time since the financial crisis, dropping below a key level in a market that has been hit hard by mounting concerns over the health of China’s economy.

Copper’s decline comes as all metal prices continue their steep falls from the boom peaks of 2011. As with other base metals, copper has suffered from the oversupply that followed the boom and from concern over future demand from China, which consumes about 45% of the metal. (…)