Wary Fed Keeps Its Options Open Federal Reserve officials expressed renewed worry about financial-market turbulence and slow economic growth abroad, leaving doubts about whether the central bank will raise interest rates as early as March.

Futures markets place just a 25% probability on rate increase by then. The central bank sought to keep its options open while it assesses a potentially shifting economic landscape. (…)

“The [Fed] is closely monitoring global economic and financial developments and is assessing their implications for the labor market and inflation, and for the balance of risks to the outlook.” (…)

An even-more striking statement of uncertainty is that the Fed wouldn’t offer an assessment about risks to the economic outlook. To guide markets, officials normally say whether risks to the outlook are balanced, or tilted toward economic strength or weakness. Officials abandoned any such assessment this time around.

“Fed loses its balance,” was the headline that J.P. Morgan Chase economist Michael Feroli sent out to clients after the meeting. He noted the Fed has rarely punted on its risk assessment. One time included September 2007, at the dawn of the 2007-2009 financial crisis; another in March 2003, when the U.S. was preparing to invade Iraq and oil prices were surging. (…)

“Labor market conditions improved further even as economic growth slowed late last year,” the Fed said. While job gains were strong, it said, consumer spending and business investment were just moderate and net exports soft. Some of the fourth-quarter slowdown resulted from businesses reducing inventories, a development that should be temporary because eventually inventories will stabilize or even rise.

The Fed is also trying to assess a shifting inflation outlook. Officials said they expected it to remain low in the near term, thanks to new declines in energy prices, but to gradually rise. (…)

The Fed asserted it has little patience for a long run of very low inflation. In a statement of its long-run goals, released with its policy statement, it emphasized it wouldn’t tolerate inflation that is either persistently below its 2% objective or above it. Long-run deviations from the target were a concern, the statement said. Inflation has run below the Fed’s goal now for more than 3½ years. (…)

Pouring oil on troubled stock markets

(…) Last year Prof Mohaddes co-authored an International Monetary Fund paper that said a halving in oil prices would add 0.2 to 0.4 percentage points to global growth in the first year. In large importing countries, including most of the developed world, the impact was predicted to be closer to 1 per cent.

In Asia prices for naphtha — a type of refined oil that is an indicator of manufacturing activity — are strong relative to crude, unlike during the financial crisis when they collapsed alongside demand.

Apple, the world’s most valuable company by market capitalisation, cited lower commodity prices as one reason for its first sales decline.

“When you think about all the commodity-driven economies — Brazil and Russia and emerging markets, but also Canada and Australia in developed markets — clearly the economy is significantly weaker than a year ago,” said Luca Maestri, Apple’s chief financial officer, on Tuesday.

Equity investors are also worried about the systemic risk from the oil price rout via industrial companies and the banking system. Several of the largest banks in the US, including Bank of America, JPMorgan Chase, Citigroup and Wells Fargo, have in recent weeks cautioned about writedowns and provisions on their oil company loans.

Their exposure is no way near the scale of the subprime crisis — BofA has $21.3bn in energy-related loans, about 3 per cent of its portfolio — but they could be forced to set aside more cash to soak up losses.

Bad energy loans can also have an impact on financial markets in other ways.

“The problem is that while a small fall in the oil price might act like a tax cut for the global economy, a large fall means significant balance sheet stress for energy producers,” says Sebastian Raedler, equity strategist at Deutsche Bank.

He estimates that “significantly stressed” US energy companies account for 20 per cent of the high-yield bond market. This is important because the risk premium in the equity market has closely tracked high-yield spreads over the past decade. If oil prices remain low and spreads widen, equities could come under more pressure. (…)

The 13 countries of the Opec cartel, which control about 40 per cent of world production, are likely to see their economies contact this year.

But that impact is vastly overshadowed by the benefit of lower prices for the four largest net importers — China, US, Japan and India — which make up more than 50 per cent of the world’s $77tn GDP.

“The impact of lower oil prices on producer countries is very painful individually,” says Prof Mohaddes. “But they are a small part of the overall global economy, so the boost in spending for consumers should eventually win out.”

Kuwait Plans to Cut Spending Next Year as Oil Revenue Plummets

IMF, World Bank move to avert oil-led defaults Team flies to Azerbaijan over possible $4bn emergency loan

Officials from the International Monetary Fund and the World Bank are heading to Azerbaijan to discuss a possible $4bn emergency loan package in what risks becoming the first of a series of bailouts stemming from the tumbling oil price.

The Baku visit, which follows a currency crisis triggered by the collapse in crude, comes amid concern at the two global institutions over emerging market producers from central Asia to Latin America.

The fund and the bank have also been monitoring developments in other oil-producing countries such as Brazil, which is now mired in its worst recession in more than a century, and Ecuador. The oil-driven crisis in Venezuela has even raised the possibility of repaired relations between the fund and Caracas, a city IMF staff last visited more than a decade ago. (…)

“These are bad times for oil producers and their creditors,” Oxford Economics warned clients on Wednesday. “History provides reason for extreme pessimism on the likely fortunes of commodity producers; suggesting that [emerging markets] are prone to default and that commodity slumps are possibly the biggest cause of defaults.” (…)

‘Worst may not be over’: Canada’s injured economy in 6 charts

But David Rosenberg is more hopeful citing:

- Existing home sales which rose 10% YoY in December;

- Retail sales which surged 1.7% MoM (ex-autos +1.1%) in November and quietly have risen in 6 of the past 7 months;

- Manufacturing shipments which jumped 1% MoM in November

- Manufacturing employment which has expanded by 30k in the past 3 months’

Not just this, but we haven’t seen the impact of the federal budget hit home yet.

Canada has a competitively supercharged exchange ate, extremely low interest rates, oil trying to form a bottom, fiscal stimulus on deck, and a U.S. consumer confidence on an uptrend – which is music to the ears of a country that ships 20% of its GDP south of the border.

Oil rises toward $34 on chance of production cut

Oil rises toward $34 on chance of production cut

Russian officials have decided they should talk to Saudi Arabia and other OPEC countries about output curbs to bolster oil prices, the head of Russia’s pipeline monopoly said.

This was from Reuters today with essentially nothing else to support. However, I found this at Saudiarabianews:

The comments by Nikolai Tokarev, head of Transneft, gave the strongest indication to date of possible cooperation between the cartel and Russia, the top non-OPEC oil producer, and helped spur a sharp rise of more than 5 percent in world oil prices.

A vice president of Lukoil, Russia’s No.2 oil producer, said earlier this week that Moscow should start talking to OPEC,

Tokarev said oil executives and government officials met in Moscow on January 26 and reached the conclusion that talks with OPEC were needed to shore up oil prices.

“At the meeting there was discussion in particular about the oil price and what steps we should take collectively to change the situation for the better, including negotiations within the framework of OPEC as a whole, and bilaterally,” he said.

“The main initiative is being shown by, of course, our Saudi partners. They are the main negotiators. That means that they are the ones we need to discuss this with first of all.”

He said Russia is willing to discuss output cuts with OPEC, calling that “one of the levers or mechanisms that would allow us to in some way balance the oil price.”

The oil executives meeting in Moscow, moreover, discussed the technical feasibility of cutting production in Russia, he said, and agreed that because oil field activities are frozen in during the winter, production cuts would only be possible in the summer.

A Russian energy ministry representative confirmed to Reuters that possible coordination with OPEC had been discussed at the meeting, which the ministry hosted.

“The meeting participants discussed the possibility of coordination of actions with OPEC members amid unfavorable market conditions on the global oil market,” the official said.

(…) A Kremlin spokesman told Reuters on January 27 that while Russia holds regular discussions with other oil-producers on the situation in world markets, but there are no plans as of now for coordinated actions.

Thus it would be a major reversal for Russia if discussions with OPEC begin in earnest following this week’s apparent agreement among oil executives in Moscow. (…)

So far, within OPEC, only Algeria and Venezuela have clearly expressed support for a production cut.

However, Iraq, OPEC’s second biggest producer after Saudi Arabia, softened its stance this week, saying it is now willing toreduce its output if all major producers inside and outside of OPEC agree. (…)

But while Russia and Iraq now seem more willing to tighten the oil spigot, Iran remains bent on increasing production, leading many analysts to be skeptical that any agreement on output cuts is on the way.

Iranian President Hassan Rouhani said on Thursday that oil prices would not stay low for long as producers restore market balance.

“The price of oil is at a low level … I don’t think it will last in the long term … The pressure on oil-producing nations means balance will be restored in the short term,” Rouhani, whose country is the third-largest producer in OPEC, said at the French Institute of International Relations. (…)

But Iranian Oil Minister Bijan Zanganeh said Tehran had not been contacted by Moscow over oil output cuts.

“I have not received anything,” Zanganeh said at a Franco-Iranian summit in Paris.

FYI: Bloomberg reminds us:

There is a precedent for a surprise agreement to turn around a chronically oversupplied oil market. When oil plunged to $10 a barrel in 1998-1999, Saudi Arabia and other oil producers for months said they wouldn’t to production. But behind the scenes, their diplomats were meeting in secret in cities from Miami to Madrid to arrange a series of output curbs that ended the rout.

Remember El-Badr last Monday: “It is crucial that all major producers sit down to come up with a solution to this”

Meanwhile,

American Drivers Are Back on the Road in Record-Setting Fashion

U.S. vehicle-miles traveled surged 4.3% in November 2015 compared with November 2014, the largest increase since 1999, according to the Transportation Department. That put 2015 on pace to become the most heavily traveled year in history.

In the 12 months leading up to November, drivers covered 3.14 trillion miles, up 3.6% from the same period in 2014, the highest year-over-year increase since 1997, according to the department.

U.S. New-Home Sales Rise in December The market for newly built U.S. homes entered 2016 on a solid footing, after December’s sales capped their best year since 2007.

Purchases of new single-family homes increased by 10.8% to a seasonally adjusted annual rate of 544,000 in December, the Commerce Department said Wednesday, beating the 502,000 estimated by economists The Wall Street Journal surveyed.

New home sales in 2015 reached an estimated 501,000, not seasonally adjusted. That marks their highest annual level since 776,000 new homes sold in 2007, underscoring the long slog back from the housing bust. Nationwide, the pace of new-home sales growth in December was up 9.9% from a year earlier, the Commerce Department said.

Averaging Dec with Nov to account for new closing procedures which shifted sales out of November, we get 517k, slightly above the full yea average of 502k. Last 6-m avg:497k vs 507k in 1st 6m. Looks like sideways trend to me especially given the mild December.

The Northeast and the South were soft while the Midwest and particularly the West were strong although both regions only ended the year on the 2015 average.

EARNINGS WATCH

Gathering speed:

- 129 companies (38.3% of the S&P 500’s market cap) have reported. Earnings are beating by 4.6% while revenues have missed by 0.5%.

- Expectations are for a decline in revenue, earnings, and EPS of -3.5%, -4.6%, and -3.0% (-3.3% yesterday). EPS is on pace for -0.1% (-0.4%), assuming the current 4.6% beat rate for the remainder of the season. This would be +5.9% (+5.6%) excluding Energy.

- Today, 52 companies representing 12.9% of the S&P 500 will report results including, Microsoft, Amazon, Visa, Amgen, and Bristol-Myers. (RBC)

German Government Trims Economic Growth Forecast

The German government expects its gross domestic product to grow 1.7% this year, slightly less than the 1.8% growth it predicted in October. In 2015, Germany’s GDP expanded 1.7%, official statistics showed earlier this month.

Strong domestic consumption and record employment levels were the main drivers of Germany’s economy last year, making up for weakening orders from China, Russia and other developing economies. (…) For 2016, the government expects domestic consumption to grow 1.9%, in line with last year.

It expects exports to grow 3.2%, slowing from last year’s 5.4% rise, and imports to grow 4.8% compared with 5.7% in 2015.

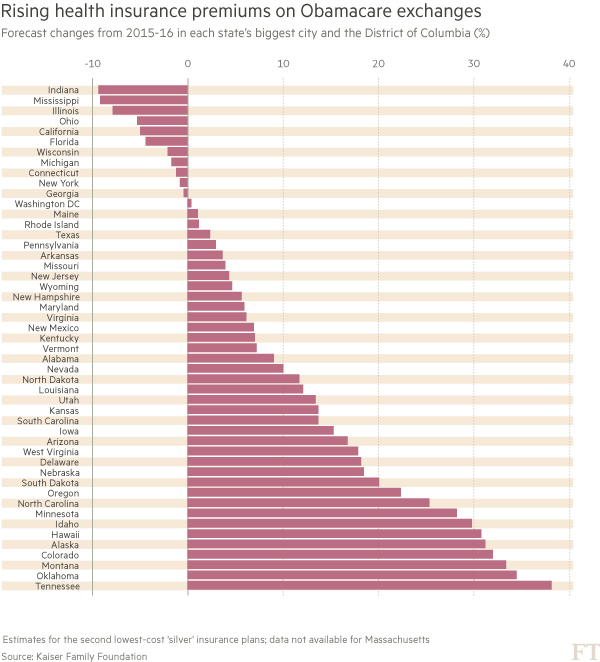

Obamacare markets face fresh troubles

(…) At issue is the balance that insurers need to make their businesses work between healthy customers and those making claims. The Obamacare formula was that first-time customers on the exchanges would draw in the insurers, and competition among insurers would push down premium rates for customers.

But the worry today is that Obamacare has a potentially unsustainable mix of too many sick people and too few affordable healthcare plans.

UnitedHealth, the US’s biggest private insurer, lost $720m on the government-backed exchanges last year and is debating whether to abandon them entirely. Other insurers have increased premiums while complaining clients are less healthy than expected. And in a blow to hopes for more competition, 11 of 23 new insurance start-ups fostered by the reform legislation have failed. (…)

On the exchanges, healthcare experts say two weaknesses in particular are beginning to show through. The first is size. They are divided up by state and some states have such small populations — less than 600,000 people, for example, live in Wyoming — that they are not necessarily attractive to insurers, says Mr Minarik.

The second weakness is a set of generous rules that let people sign up for insurance the moment they need treatment rather than in advance. This has wreaked havoc with insurers that find themselves with too many customers making claims.

Mr Williams supports the goal of broadening access to health insurance but says: “What we are seeing the federal government struggle with is finding the right balance between the solvency of insurers and protecting consumers.”

The Obama administration has acknowledged concerns about the viability of the exchanges. Andy Slavitt, who oversees them as acting head of the Centers for Medicaid & Medicare Services, said this month he was seeking to create more stable and balanced “risk pools” on them. He announced steps that included tightening enrolment rules and improving the redistribution of funds to insurers taking higher risks from those that were more cautious.

Some 32m Americans were still uninsured in 2015, according to the Kaiser Family Foundation, but Mr Slavitt said more healthy consumers under the age of 35 were being pushed into the market by the threat of a tax penalty. (…)

Alphabet and Apple spell global tax war

(…) We face a historic moment. The tax system formed under the League of Nations in 1928 relies on the idea that companies should be taxed largely where profits are created, not where they sell their products and services. It could soon fall apart and what happens then is anyone’s guess, although it will not be pretty and will probably resemble a global tax war.

Multinationals, especially US corporations subject to America’s dysfunctional tax laws, stretched rules to the point where the result appals taxpayers. They did so with the aquiescence of offshore havens and countries such as Ireland and Luxembourg.

The European taxpayer in the street might just credit the idea that Alphabet or Apple create, design and manage their products and services from California, and so the US should receive a larger share of its profits than Italy or the UK. This is the intended outcome of international tax treaties.

Why, though, should he or she accept that intellectual property can be shifted to any convenient spot, according to which jurisdiction levies the least tax? Google’s search engine was not invented in Bermuda and Apple did not develop the iPhone in a tax-advantaged entity sitting between Ireland and the US. Such structures obey the letter of the law but they are nonsensical.

They exist to hold what is in theory a US tax liability until Congress gets around to cutting the US corporate tax rate from 40 per cent (including federal and state taxes) and luring the cash back. (…)

Well, perhaps. Without attributing malice to Steve Jobs, both Apple, the company he co-founded, and Ireland were pretty ingenious about tax; they can hardly complain if Margrethe Vestager, EU competition commissioner, is ingenious in return. As to Apple’s complaint of retrospective legislation, the Supreme Court often strikes down US state laws long after they were passed, no matter how inconvenient it is for anyone who is affected.

The US Treasury is lining up on its companies’ side. It worries about taxpayers footing the bill in forgone tax receipts if more is taken by European countries. The Senate finance committee wants it to consider retaliating by double taxing European companies if billions are bitten from Apple.

The incentive to carry on co-operating is slim. The UK tax authorities tried to raise Google’s bill while still treating its British arm as a minor contributor to global profits — a plausible view under revised OECD guidelines. They are now in disgrace for not being tough enough while France and Italy, which have changed tack to enforce far higher local taxes, bask in approval.

It is clear where this ends. When the global tax consensus cannot hold, it is every nation for itself. This was what they tried to remedy in 1928 but the goodwill is fading fast.