![]() Did you miss THAT STINKY BULL

Did you miss THAT STINKY BULL

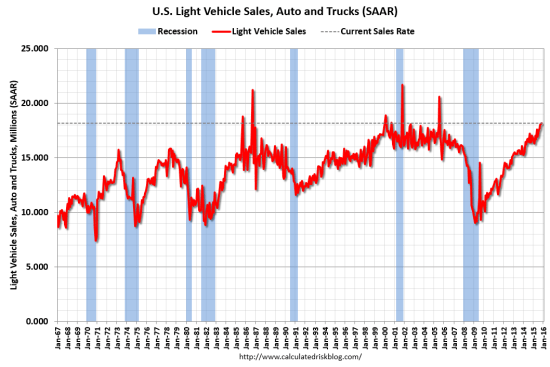

U.S. Light Vehicle Sales Remain Strong Despite Monthly Dip

Total sales of light vehicles eased 0.3% during November to 18.19 million units (SAAR) following a like increase in October. Sales have risen 6.2% since last November and were near the highest level since July 2005.

Passenger car sales led the way lower last month and fell 2.5% to 7.81 million after a 1.3% October rise. Sales were down by 4.0% versus one year earlier. Domestic car sales declined 3.0% to 5.71 million and were down 5.6% from the peak during August 2014. Sales of imported autos eased a lesser 0.9% to 2.10 and have been falling steadily since Q4’13.

Sales of light trucks increased 1.5% to 10.38 million after having been roughly unchanged m/m in October. Light truck sales share of the total new vehicle market rose to 57.1%, the highest level since a spike in July 2005. Purchases were up 15.5% versus a year earlier. Imported light truck sales rose 2.5% to 1.66 million, a record high. Sales of domestically made trucks gained 1.3% to 8.72 million.

(

(U.S. Construction Activity Continues to Strengthen

The value of construction put-in-place increased 1.0% during October following an unrevised 0.6% September increase. Three-month growth of 10.4% (AR) was steady with Q3 but down sharply from 29.2% during Q2. A 0.5% October rise had been expected in the Action Economics Forecast Survey.

Building activity in the private sector increased 0.8% following a 0.9% September gain. Activity increased at an 11.3% rate during the last three months. Residential building activity rose 1.0% (18.3% y/y), the seventh consecutive month of strong gain. The gain was led by a 1.6% increase in single-family building (11.3% y/y) which equaled the strongest rise of the year. Multi-family building rose 1.4% (27.2% y/y). Spending on improvements eased 0.3% (+21.5% y/y). Nonresidential building improved 0.6% (14.4% y/y) as factory sector construction rose 3.0% (37.6% y/y).

Public sector building increased 1.4% (5.6% y/y) following three months of little change. Water supply spending rose 2.5% (5.3% y/y) and office construction jumped 1.8% (7.2% y/y). Highway and street construction increased 1.1% (5.2% y/y) but power construction declined 5.2% (-8.7% y/y).

CHINESE GREEN SHOOTS

Markit added some color to yesterday’s PMI:

The survey signalled the largest monthly rise in new export orders since October of last year, the second consecutive monthly improvement. The data therefore suggest that the downturn in foreign trade seen throughout much of 2015 is starting to reverse, albeit only modestly.

Despite the upturn in export sales, total orders inflows fell at a slightly increased rate in November, highlighting a further deterioration in demand for manufactured goods from domestic customers.

Large firms are seeing a steeper drop in order books compared to small and medium sized firms, linked to an ongoing deterioration in export performance at these larger firms. Large firms have seen exports slump in recent months at a rate not seen since the first half of 2009, at the height of the global financial crisis.

Large firms suffer in global markets

New export orders seem to be mending in Asia:

Meanwhile, China continues to export deflation:

Average producer selling prices meanwhile fell at the steepest rate for 20 months, indicating that the deflationary trend intensified in November. Input prices also dropped at an increased rate, the steepest seen for nine months. With suppliers’ delivery times improving in November, pointing to a healthy supply of inputs, the survey suggests there is an ongoing lack of inflationary pressures in supply chains.

Deflationary pressures intensify as supply glut continues

In fact all Asia is exporting deflation:

Average selling prices across Asia continued to fall at a rate unchanged on that seen in October, which was in turn the highest for just over one-and-a-half years. Firms in China, Taiwan, South Korea and Vietnam once again cut prices in an effort to boost sales, but prices were hiked in India, Japan, Indonesia and Malaysia, the latter seeing the steepest rate of increase, with selling price inflation hitting a three-and-a-half year survey high.

Manufacturers’ selling prices

Eurozone Inflation Remains Weak

The European Union’s statistics agency Wednesday said its broadest measure of prices for goods and services was 0.1% higher than in November 2014, a rate of increase that was unchanged from October. Economists surveyed by The Wall Street Journal last week had expected to see a rise in the inflation rate to 0.2%.

The core rate slipped to 0.9% from 1.1% in October, as prices for services and manufactured goods rose at a slower pace, indicating a weakening of inflationary pressures coming from within the currency area.

Core CPI declined 0.2% in November after +0.2% in October, +0.5% in September and +0.3% in August. Annualized last 2 months: 0%, last 3 months +2.0%, last 4 months +2.4%.

-

ECB’s Preferred Inflation-Outlook Gauge Climbs to 5-Month High

The five-year, five-year forward break-even rate, which measures the outlook for inflation over the five-year period from 2020, rose to 1.83 percent Tuesday. That’s still below the average of 2.26 percent over the past decade. The measure fell to as low as 1.48 percent in January. ECB officials have said the rate is among key gauges they monitor. (…)

Watch for U.S. recession, zero interest rates in China next year, Citi says

Watch for U.S. recession, zero interest rates in China next year, Citi says

As the U.S. economy enters its seventh year of expansion following the 2008-09 crisis, the probability of recession will reach 65 percent, Citi’s rates strategists wrote in their 2016 outlook published late on Tuesday. A rapid flattening of the bond yield curve towards inversion would be an key warning sign.

“The cumulative probability of U.S. recession reaches 65 percent next year,” Citi’s rates strategists wrote in their 2016 outlook published late on Tuesday. “Curve inversion will likely come more quickly than the consensus thinks.” (…)

RBC Capital:

Zuckerbergs to Give 99% of Facebook Shares to Charity

Zuckerbergs to Give 99% of Facebook Shares to Charity

Facebook Inc. Chief Executive Mark Zuckerberg and his wife, Priscilla Chan, said Tuesday that over the course of their lives they would give away 99% of their Facebook shares, now valued at $45 billion, in what would be one of the world’s largest philanthropic gifts.

Mr. Zuckerberg and his wife, a pediatrician, revealed the donation pledge while announcing the birth of their first child, Maxima Chan Zuckerberg. In a 2,200-word letter to their daughter, Mr. Zuckerberg and Dr. Chan said they had created a new foundation that would initially focus on “personalized learning, curing disease, connecting people and building strong communities.” (…)

-

Zuckerberg offers new approach to giving LLC provides cash for political activism and for-profit investing

By creating a limited liability company to use the money for political activism and for-profit investing, as well as traditional giving, Mr Zuckerberg revealed how a new generation of Silicon Valley entrepreneurs may approach the philanthropic world. (…)

In contrast to traditional foundations, LLCs are able to engage in public policy advocacy and for-profit investments that can also advance their favoured causes. The structure will also allow the Zuckerbergs to keep direct control of the Facebook stock that is contributed to the company, to be called the Chan Zuckerberg Initiative. The couple say all investment profits will be ploughed back into additional philanthropic work.