U.S. SERVICES PMIs

![]() US Service Gauge Rises to Six-Month High, Topping All Forecasts ISM service-sector index rose to 54.5 in August, est. 52.5

US Service Gauge Rises to Six-Month High, Topping All Forecasts ISM service-sector index rose to 54.5 in August, est. 52.5

The Institute for Supply Management’s services index increased almost 2 points to 54.5, data showed Wednesday. Readings above 50 indicate expansion, and the figure topped all estimates in a Bloomberg survey of economists. (…)

Thirteen services industries reported growth in August, led by real estate, rental and leasing as well as accommodation and food services.

The ISM’s employment index rose last month to its highest level since November 2021, re-enforcing the broad-based hiring seen in last week’s jobs report. Additional hiring also allowed firms to make progress on backlogged orders.

Meanwhile, costs for materials and wages continued to accelerate in August, with the group’s prices-paid index rising to a four-month high. A sustained pickup in costs for service providers would risk keeping inflation elevated for longer.

ISM’s gauge of new orders rose to a six-month high and a measure of business activity edged higher. Exports expanded at the fastest pace in nearly a year. (…)

![]() Nobody mentions the other, much less buoyant, survey:

Nobody mentions the other, much less buoyant, survey:

![]() S&P Global: Service sector demand falters sparking weakest growth in activity for seven months

S&P Global: Service sector demand falters sparking weakest growth in activity for seven months

The seasonally adjusted final S&P Global US Services PMI Business Activity Index posted 50.5 in August, down sharply from 52.3 in July. The rate of output growth slowed for the third month running and was only marginal. Although some firms noted that activity growth was led by efforts to work through past orders, weak client demand and a return to contraction in new business weighed on the expansion.

Although only fractional, the fall in new orders was the first in six months and signalled a marked turnaround from the sharp upturn seen in the second quarter of 2023. Muted demand conditions reportedly stemmed from the impact of higher interest rates and inflation on customer spending.

Foreign client demand remained more supportive, with new export orders continuing to rise in August thanks to new client acquisition and sustained interest from existing customers.

Service providers largely noted that greater wage bills drove input price inflation during August, alongside reports of upward energy and fuel price pressures as well as some firming of materials prices. The rate of increase picked up from that seen in July and was marked overall. Although slower than the 2023 average to date, the pace of inflation was historically marked.

Subdued demand conditions led firms to be more hesitant regarding increases in selling prices in August. Although still sharp overall by pre-pandemic historical standards, the rate of output charge inflation was the slowest since February.

Service sector firms meanwhile recorded only a fractional rise in employment midway through the third quarter. Lower new order inflows were widely cited as encouraging a drawback in hiring activity. The rate of job creation weakened for the third successive month to the slowest since October 2022.

The softer uptick in workforce numbers reflected emerging evidence of spare capacity across the service sector, amid the renewed drop in new business. Backlogs of work fell for a second month running, declining at the steepest rate since November 2022.

Firms remained upbeat in their assessment of the outlook for output over the coming year, despite the current muted demand. The degree of confidence improved from that seen in July, yet remained below the series average. Although companies were often buoyed by hopes that initiatives such as marketing campaigns would drive growth in new orders, client hesitancy amid interest rate hikes subdued expectations.

History has shown that it’s generally better to put one’s chips on S&P Global’s surveys. But the ISM gets most of the coverage…

Which one does the Fed watch? Not a moot point given services’ relative importance.

Fed Set to Double Its Economic Growth Forecast After Strong US Data

Following a string of stronger-than-expected reports on everything from consumer spending to residential investment, economists have been boosting their forecasts for gross domestic product. One widely-followed, unofficial estimate produced by the Atlanta Fed even has it expanding 5.6% on an annualized basis in the third quarter.

That marks a sharp turnaround from three months ago — the last time policymakers updated their own numbers — when the consensus view was that the economy would stall in the current quarter. And it may be enough to prompt Fed officials to scale back their estimates for interest-rate cuts in 2024.

“Consumer spending was robust in June and July, so the third quarter is virtually baked in the cake at this point,” said Stephen Stanley, the chief economist at Santander Capital Markets US who is projecting 3.7% growth in the July-to-September period. “5% seems too high, but not impossible.” (…)

When Fed officials last updated their own projections for the US in mid-June, they showed the median policymaker thought GDP would expand just 1% in 2023. At the time, that marked an upgrade over the previous projection round in March, which implied a recession this year.

That number will probably go up to 1.8% or 2% in the new projections set to be released at the conclusion of the central bank’s Sept. 19-20 policy meeting, and the outlook for the unemployment rate could be revised lower, according to Omair Sharif, president of Inflation Insights LLC.

The growth upgrade may also lead Fed officials to scale back the easing they had projected for next year to 75 basis points of rate cuts instead of 100, Sharif said. (…)

Better-than-expected numbers in a monthly Institute for Supply Management report on the US services sector published Wednesday bolstered the theme. (…)

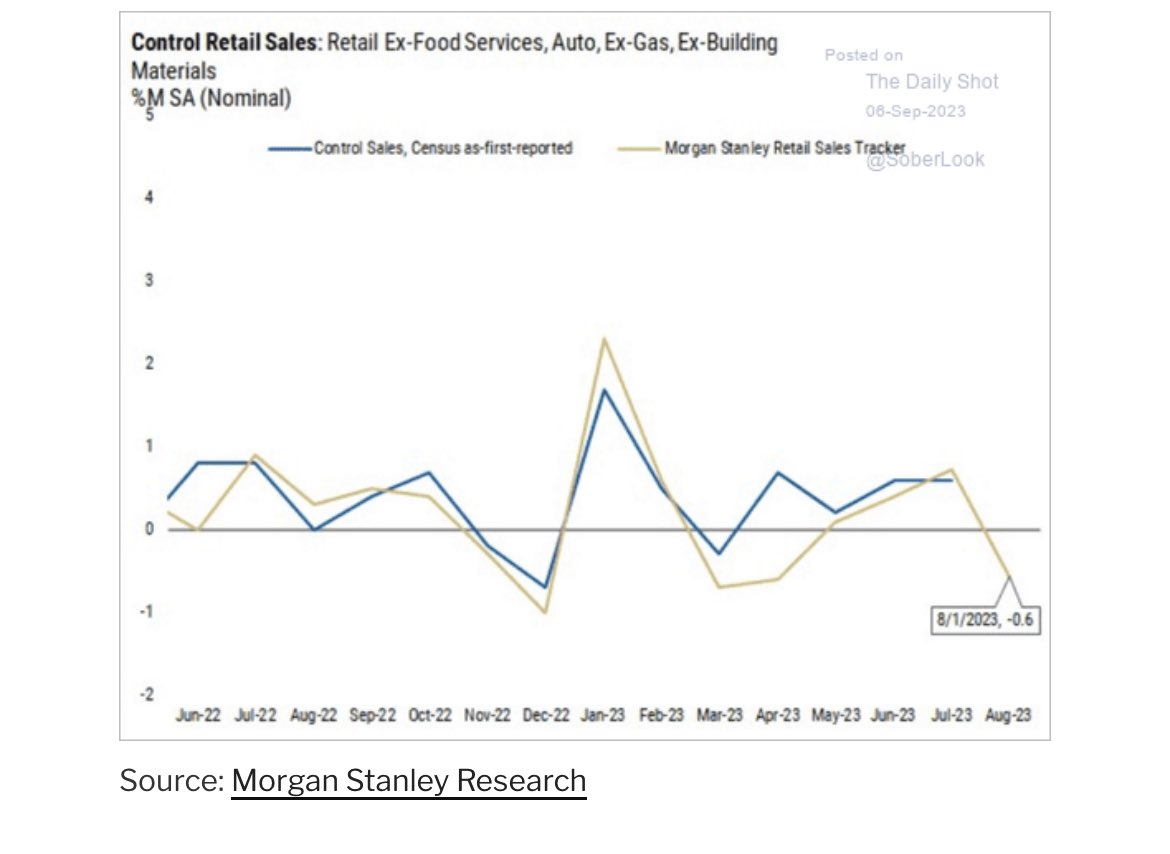

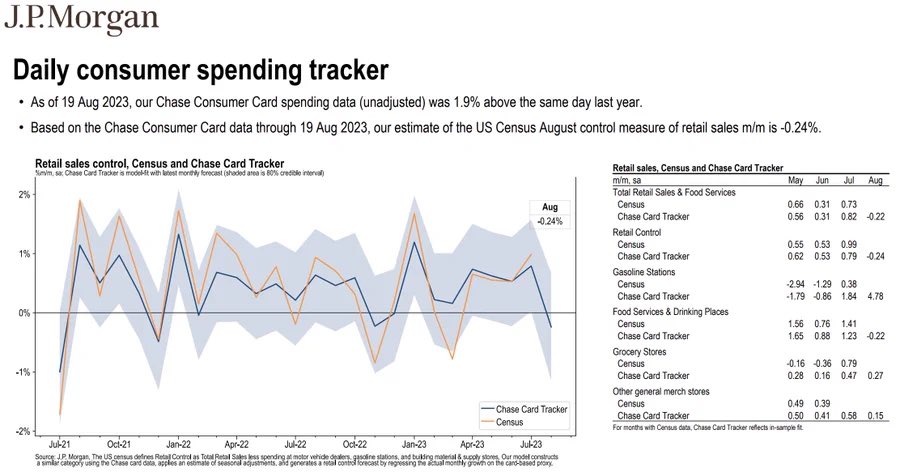

After the spectacular summer retail sales data, Morgan Stanley and J.P. Morgan warn of a very weak August (h/t @BobEUnlimited):

:

Recall that August autos sales of 15.0MM (saar) were down 4.5% from July and 3.8% from their Q2 average of 15.6MM even as incentives rose.

The Fed’s latest Beige Book suggests that growth in the US economy and jobs market slowed in July and August as “contacts from most districts indicated economic growth was modest. (…) Companies around the country are reporting increasing difficulty in passing higher costs along to customers.” Not a sign of strong demand.

Speaking of costs:

China’s Exports Fall for a Fourth Month as Once-Reliable Growth Engine Sputters A deep downturn in the property sector has also pushed imports to their 11th month of declines in the past year.

(…) China’s outbound shipments dropped 8.8% in August from a year earlier, contracting for a fourth consecutive month, China’s General Administration of Customs said Thursday. (…) They represented an improvement from the 14.5% year-over-year drop in exports in July, which marked the worst such result since February 2020.

Imports into China, including intermediate components, commodities and consumer products, fell 7.3% in August from a year earlier, a pace slower than July’s 12.4% drop as well as the 9.7% decline anticipated by economists. (…)

In the first half of the year, China accounted for 13.3% of U.S. goods imports, down from a high of 21.6% in 2017, which represented the lowest level since 2003.

Trade with the 10-nation Association of Southeast Asian Nations has grown over the past year to become China’s largest export market, ahead of the U.S. and European Union, according to a recent report by HSBC. (…)

Bloomberg views the same data more optimistically:

China’s trade slump eased in August, adding to early signals the worst may be over for some parts of the world’s second-largest economy as it tries to regain momentum.

Overseas shipments fell 8.8% in dollar terms from a year earlier while imports contracted 7.3%, both better than estimates and significantly less severe than July’s downturn. (…)

Other data has suggested global demand is beginning to pick up, providing some hope for China’s trade in the coming months. South Korea’s exports — a bellwether for world trade — also declined at a more moderate pace in August than the previous month.

Thursday’s data showed China’s shipments to Europe and Asean continuing to record double-digit declines, but there was a notable improvement in US trade: Exports dropped 9.5% in August, compared to a 23.1% slump in July. (…)

The milder decline in imports, meanwhile, provided a sign that the downturn in domestic demand may be bottoming out. (…)

But as we saw from yesterday’s PMIs, the Chinese economy continues to struggle.

The slowdown in business activity coincided with a weaker increase in overall new business. New orders increased modestly, and at a pace that was below the average seen for 2023 to date. Data suggested that this was partly due to weaker foreign demand for Chinese services.

New export business fell for the first time since December 2022, albeit marginally, amid reports of sluggish overseas market conditions.

- China Seeks to Broaden iPhone Ban to State Firms, Agencies It could deal blow to Apple and amplifies a self-reliance push.

![]() “Moving production to India, euh?”

“Moving production to India, euh?”

-

German Economy Faces Fresh Contraction Higher energy costs, Chinese competition and cooling global demand for goods are hobbling Europe’s industrial powerhouse

(…) Figures released Thursday by Germany’s statistics agency showed industrial production fell by 0.8% in July from June, and was 4% down from February 2022, the month of Russia’s invasion.

The German economy should contract by 0.3% in the current quarter, and by 0.5% in 2023 as a whole, the Kiel Institute for the World Economy said Wednesday, cutting its previous estimate. (…)

According to the statistics agency, sales in stores and their online equivalents fell in July and were 4% lower in the first seven months of this year than in the same period of 2022. In particular, households have been cutting back on food consumption as prices soar, buying 5.3% less than in the first seven months of last year.

Hobbled by falling demand at home, German manufacturers are also under pressure in overseas markets. In July, the country’s businesses sold goods valued at 130.4 billion euros—equivalent to $139.86 billion, to the rest of the world, a decline from June and a 1% drop from a year earlier.

The surprising resilience of the U.S. economy despite rising interest rates has helped, with exports to the world’s largest economy rising by 5.2% from the previous month. Sales to Chinese buyers were up a more modest 1.2%. Exports to the U.K., which has stagnated since the start of the war, were down 3.5%. (…)

There are few signs of a rebound beyond this quarter. Wages began to rise faster than consumer prices during the second quarter, and that should restore some lost spending power to households. But the outlook for factories is gloomy.

According to the statistics agency, new factory orders were almost 12% lower in July than in June, reversing a recent pickup that had been partly driven by demand for military equipment. It was the largest fall in a single month since April 2020. (…)

The world’s 4th largest economy continued to sink at the end of the third quarter per S&P Global:

Manufacturers scaled back output for a fourth consecutive month in August. Furthermore, the rate of contraction accelerated once again to the fastest seen since the initial COVID shutdowns in spring 2020. Production was down across all main industrial groupings, reflecting a broad-based reduction in demand.

New orders continued to fall sharply, with the rate of decline quickening slightly since July to the fastest for more than three years (and far outstripping the reduction in output). New export orders were down markedly, amid reports of reduced sales to China and across Europe, although the rate of decline eased from the previous month and was noticeably slower than that of total new business.

Germany’s service sector slipped back into contraction in August after having grown throughout the first seven months of the year, the latest HCOB PMI® survey compiled by S&P Global showed. Businesses reported a sustained weakening of demand amid a backdrop of economic uncertainty and strong inflationary pressures.

The survey showed that activity had finally succumbed to a sustained decline in demand, with inflows of new business across the service sector falling for a second straight month in August. Furthermore, the rate of decline accelerated to the quickest since last November, amid reports of growing reluctance amongst clients and persistently high inflation. Weaker foreign demand was also a factor behind the sector’s downturn, although the third successive monthly fall in new export business was softer than that seen in July.

Gross domestic product rose only 0.1% in the three months through June, compared with a prior increase measured at 0.3% — an outcome that had surprised to the upside when first published in late July. (…)

The remainder of the year looks similarly bleak, with PMI data signaling private-sector activity in contraction and surveys pointing to further anemic expansion of just 0.1% in the current quarter. (…)

The data confirm how China-led weakness in global demand is hurting exporters badly enough to be weighing down the region as a whole.

Both Germany, the euro area’s biggest economy, and Italy — its third-largest — are suffering likely recessions in manufacturing at present. The latter country even experienced an overall GDP contraction during the second quarter.

Bank of Canada Holds Rates Steady as Economy Shifts Into Weaker Period The Bank of Canada held its main interest rate steady at 5% after back-to-back rate rises in June and July, saying the economy has shifted into a weaker phase and labor-market pressures have eased.

Nevertheless, the central bank Wednesday said it remained concerned “about the persistence of underlying inflationary pressures,” and is prepared to raise rates again should conditions not improve. (…)

In a statement explaining its decision, the Bank of Canada said the Canadian economy “has entered a period of weaker growth, which is needed to relieve price pressures.” (…)

The Bank of Canada added that labor-market activity “has continued to ease gradually,” although noted that annual wage growth was elevated at between 4% and 5%. Canada’s unemployment rate rose by a half percentage point in the span of three months, and now sits at 5.5% as of July. Employment growth has slowed, and job vacancies have dropped about 25% from their peak last year and sit at their lowest level in more than two years. (…)

It said year-over-year and three-month measures of core inflation—which strips out volatile items like food and energy—were both running at 3.5%, “indicating there has been little recent downward momentum in underlying inflation. The longer high inflation persists, the greater the risk that elevated inflation becomes entrenched.” (…)

Of mounting concern for economists is Canada’s per capita gross domestic product, which has declined for four straight quarters—down 2% in the second quarter from a year ago. This reflects growth in Canada’s population fueled by an aggressive immigration plan.

Historical data indicates that the Bank of Canada was cutting rates in the four prior instances since 1980 when GDP per capita fell below the year-ago level, according to economists at National Bank Financial. This time, they add, the Bank of Canada has been raising rates to wrestle down inflation.

Real-Estate Doom Loop Threatens America’s Banks Regional banks loaded up on commercial real-estate loans and investments that are now a looming danger—and their exposure is more substantial than it appears.

(…) Banks roughly doubled their lending to landlords from 2015 to 2022, to $2.2 trillion. Small and medium-size banks originated many of those loans, and all that lending helped push up property prices. (…)

Over the past decade, banks also increased their exposure to commercial real estate in ways that aren’t usually counted in their tallies. They lent to financial companies that make loans to some of those same landlords, and they bought bonds backed by the same types of properties.

That indirect lending—along with foreclosed properties, trading portfolios and other assets linked to commercial properties—brings banks’ total exposure to commercial real estate to $3.6 trillion, according to a Wall Street Journal analysis. That’s equivalent to about 20% of their deposits.

The volume of commercial property sales in July was down 74% from a year earlier, and sales of downtown office buildings hit the lowest level in at least two decades, according to data provider MSCI Real Assets. When deals begin again, they will be at far lower prices, which will shock banks, said Michael Comparato, head of commercial real estate at Benefit Street Partners, a debt-focused asset manager. “It’s going to be really nasty,” he said. (…)

Depositors withdrew funds from many small and regional lenders earlier this year after the collapse of three midsize banks stoked fears of a systemwide crisis.

The doom-loop scenario is starting to play out in big cities where office vacancies have soared. Real-estate investors that are unable to refinance their debt, or can only do it at high rates, are defaulting. The lenders, no longer getting the debt payments, often have to write down the value of those mortgages. Sometimes the bank ends up owning the property.

“The plumbing is clogged right now,” said Scott Rechler, chief executive of real-estate investor RXR. “And that is going to create a backup that will eventually overflow on the commercial real-estate markets and on the banking system.” (…)

Besides banks, lenders such as private debt funds, mortgage REITs and bond investors can also provide funding—but many of them are financed by banks and can’t get loans. “We are seeing a serious credit crunch developing,” said Ran Eliasaf, managing partner of Northwind Group, a private real-estate lender. (…)

The first quarter of 2023 marked the first decline in banks’ commercial real-estate holdings since 2013, according to the Journal’s analysis. At that point, banks’ overall securities holdings had lost nearly $400 billion in value, largely due to higher interest rates. Banks don’t have to mark down the value of loans in most cases, so the real losses are likely greater.

Banks with less than $250 billion in assets held about three-quarters of all commercial real-estate loans as of the second quarter of 2023, the Journal’s analysis shows. They accounted for nearly $758 billion of commercial real-estate lending since 2015, or about 74% of the total increase during that period. (…)

Roughly $900 billion worth of real-estate loans and securities, most with rates far lower than today’s, need to be paid off or refinanced by the end of 2024. (…)

In early 2021, an affiliate of Brookfield Asset Management borrowed $465 million in CMBS and other debt against the Gas Company Tower, a 52-story office building in downtown Los Angeles.

At the time, appraisers valued the property at $632 million, according to Trepp, up from a valuation of $517 million when Brookfield bought the building in 2013. When the loans came due this February, the owner defaulted. An appraiser earlier this year cut the building’s estimated value to $270 million.

![]() Data through August 23rd show that deposits have stabilized since SVB…

Data through August 23rd show that deposits have stabilized since SVB…

…while lending kept rising, particularly at smaller banks… Actually, CRE loans at smaller banks are up 1.3% from their pre-SVB level.

-

WeWork Looks to Renegotiate Most of Its Leases as It Fights to Survive WeWork launched a renegotiation of its office leases globally, testing its leverage against landlords that stand to lose if the embattled co-working space provider goes out of business.

More Binance Executives Leave, Including Some Overseeing Russia Several Binance executives have left recently, including leaders overseeing its Russian business, extending a period of rapid senior turnover at the crypto giant.

Binance has faced intense regulatory scrutiny this year. The latest departures, including those of regional head Gleb Kostarev and Russia chief Vladimir Smerkis, follow exits by its general counsel, chief strategy officer and head of investigations in recent months. Binance has also laid off staff and curtailed benefits. (…)

Founded in 2017, Binance is by far the largest crypto exchange in the world. For years it operated without licenses and without an official home base, serving traders through its Binance.com platform. As regulators started cracking down on the industry, the company said it would change and become compliant, though it continued to take risks. (…)

China:

China: