Robust Hiring in April Shows U.S. Job Market Remains Hot in Cooling Economy Employers added 253,000 jobs last month and unemployment fell to 3.4%

Employers added 253,000 jobs in April, the best gain since January, the Labor Department said Friday. Job growth was revised lower in February and March. The unemployment rate fell to 3.4% last month, matching the lowest reading since 1969.

Low joblessness kept upward pressure on wages, which grew 4.4% in April from a year earlier, up slightly from a 4.3% annual increase in March. Average hourly wages rose 0.5% from a month earlier to $33.36. (…)

On Friday, investors saw just a 7% chance that the Fed would raise rates at its next meeting, and they see rising chances of a cut after that, according to CME Group. Interest-rate futures markets imply a 75% probability that the Fed will have cut rates below current levels by September.

April’s monthly payrolls increase was slightly below the average monthly gain of 290,000 over the prior six months. Employment in February and March was revised down by a total of 149,000. (…)

Friday’s report showed job gains in most industries, even ones such as construction that are particularly sensitive to interest-rate increases. (…)

In April, 83.3% of Americans in their prime working years, ages 25 to 54, were employed or seeking jobs, the highest share since 2008. The influx of job seekers is helping restaurants, bars and hotels snap up workers, after they struggled with acute labor shortages for much of the pandemic.

Pushed by renewed demand to travel and socialize, leisure and hospitality businesses added about 900,000 jobs over the past year, almost a quarter of all jobs gained. (…)

Interestingly, employment among prime-age workers is now exceeding its pre-pandemic level and at its highest level since 2001. Prime-age workers are also enjoying above average wage increases at +6.6% YoY in Q1.

April saw a reacceleration in all variables impacting labor income:

- employment rose 0.16% MoM (+2.0% annualized) following +0.16% and +0.11% in February and March respectively;

- weekly hours were unchanged in April after two months of declines;

- hourly wages jumped 0.5% after +0.3% in each of the previous 3 months; first 4 months: +4.0% a.r., last 2 months +4.5%, last month +6.1%.

Aggregate weekly payrolls thus rose 0.66% MoM (+7.8% a.r.), sharply higher than the +0.1% average gain of the previous 2 months. First 4 months: +8.1% a.r., last 3 months: +3.3%, last 2 months +4.4%.

On a YoY basis, payroll income is up 6.6% in April, higher than +6.2% in March and still positive in real terms with PCE inflation at 4.2% in March. Consumer expenditures should thus remain strong in Q2.

If so, real spending on services will remain buoyant, up 3.0% YoY in Q1, keeping the pressure on services prices, and services wages, which the Fed currently considers its main targets.

The “75% probability that the Fed will have cut rates below current levels by September” looks very high to me, and to Henry McVey, KKR CIO:

(…) the labor market is making it harder for the Fed to accomplish its mission of bringing inflation back to two percent. In the latest data, overall employment is about 3.3 million jobs higher than it was pre-COVID, while the labor force participation rate is still 80 basis points below its pre-pandemic peak.

The combination of limited supply and above trend demand following the pandemic has pushed the unemployment rate back down to 1960s levels, and put upward pressure on wages. So, while labor might not be the biggest driver of inflation on a historical basis, we think it will remain the biggest single driver of ‘sticky’ inflation this cycle.

We maintain our out of consensus view that the Fed will not go into cutting mode anytime soon. We have been highlighting this reality for some time, but the prospect of the Fed cutting 150-175 basis points during the next 12 months (which is what the futures are pricing) seems extremely low to us.

The reacceleration of the economy suggested by recent PMI surveys is supported by labor trends:

- true, the last 3 months has the average payroll gain at 222k vs the 6-month average of 278k. But

- employment growth at service-providers has stabilized above 200,000 per month;

- the long and widely expected goods recession looks more like a very soft landing. Demand for goods remains solid and inventories have been pared down.

Wages have also reaccelerated in both goods and services industries: positive for consumer spending, not so for inflation. As seen last week, productivity (-0.9% YoY) and unit labor costs (+5.8%) data are not encouraging.

Recall what April PMI surveys revealed:

- Service sector input costs rose at the steepest rate for three months, while the increase in selling prices quickened to the fastest since August 2022.

- The rate of manufacturing cost inflation quickened to the sharpest in three months, while the pace of increase in selling prices also accelerated above the series average.

This wage tracker chart (through Q1) from Goldman Sachs is not suggesting any retrenchment in wages across G7 countries:

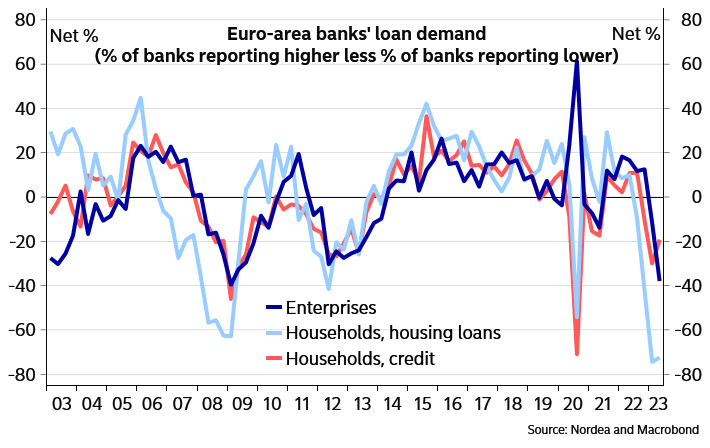

The new economic worry comes from a possible credit crunch as regional banks are seen tightening lending standards in the wake of SVB. Regional banks supply much of the credit needs of small and medium size businesses which in turn provide 70% of U.S. jobs.

Data: FDIC and FRED; Chart: Rahul Mukherjee/Axios

But 7 weeks after SVB, credit seems to be flowing smoothly, even at smaller banks as this chart of weekly credit flows through April 26 shows. Deposit movements (black and grey bars) also do not suggest a crisis; recent declines typically reflect large outflows from accounts as the annual tax filing season comes to a close:

Canada’s job market stays resilient despite signs of cooling economy Statistics Canada says the economy added 41,400 new jobs in April, more than the 20,000 positions analysts had been forecasting

Full-time employment was down for the first time in eight months, with five provinces reporting a decline – the worst diffusion in 7 months. As a result, hours worked grew at the slowest pace since December 2022.

Moreover, half of the employment gains in April were concentrated among the self‑employed. Excluding this category, the number of people employed increased by 23K in the month, the lowest level since November 2022.

While we have yet to see a contraction in payrolls, the dominance of the self-employed among job creation could signal a change in attitude from Canadian employers and a slower pace of payroll expansion in the months ahead.

In addition, just under a third of new jobs created since the start of 2023 have been in ‘high wage’ sectors, in sharp contrast to 2022. As a result, even with annual wage inflation in the 4-5% range, the impressive job gains seen since the beginning of 2023 are not providing the same boost to household finances than if they had been concentrated in high-paying industries.

All in all, despite a stronger headline number than consensus expectations, April’s employment report does not argue for a change in policy by the Bank of Canada.

EARNINGS WATCH

From Refinitiv/IBES:

Through May. 5, 419 companies in the S&P 500 Index have reported earnings for Q1 2023. Of these companies, 77.1% reported earnings above analyst expectations and 18.4% reported earnings below analyst expectations. In a typical quarter (since 1994), 66% of companies beat estimates and 20% miss estimates. Over the past four quarters, 74% of companies beat the estimates and 22% missed estimates.

In aggregate, companies are reporting earnings that are 7.2% above estimates, which compares to a long-term (since 1994) average surprise factor of 4.1% and the average surprise factor over the prior four quarters of 4.2%.

Of these companies, 74.5% reported revenue above analyst expectations and 25.5% reported revenue below analyst expectations. In a typical quarter (since 2002), 62% of companies beat estimates and 38% miss estimates. Over the past four quarters, 71% of companies beat the estimates and 29% missed estimates.

In aggregate, companies are reporting revenues that are 2.5% above estimates, which compares to a long-term (since 2002) average surprise factor of 1.3% and the average surprise factor over the prior four quarters of 2.3%.

The estimated earnings growth rate for the S&P 500 for 23Q1 is -0.7%. If the energy sector is excluded, the growth rate declines to -2.4%.

The estimated revenue growth rate for the S&P 500 for 23Q1 is 3.5%. If the energy sector is excluded, the growth rate improves to 4.4%.

The estimated earnings growth rate for the S&P 500 for 23Q2 is -4.7%. If the energy sector is excluded, the growth rate improves to 0.5%.

After a poor start, the Q1 earnings season got better when financials reported and went in overdrive when 91% of tech companies beat with a surprise factor of +8.2%. Even Industrials shone with a 84% beat rate and a +10.0% surprise factor.

Conf. calls were generally upbeat: 25 more companies than during the Q4 season provided guidance so far, 21 positive, leading analysts to pump up.

Trailing EPS are now $219.83. Full year: $220.47e and 12-m forward $226.28e.

This “earnings recession” could be over after a mere 2.1% decline in trailing earnings. Q3 and Q4 ex-E estimates are now incorporating rising margins even with revenue growth in the 4% range.

TECHNICALS WATCH

- S&P 500 Large Cap Index – 13/34–Week EMA Trend Chart

Here’s a longer term version of this indicator courtesy of Trade Signals:

Source: @Marlin_Capital

From The Market Ear

-

Buyback announcements have continued to boom…almost $200bn worth in the last 3 weeks.

Deutsche

- Goldman’s PB was net sold for the 3rd week in a row and saw the largest net selling in three months…note short selling was the main driver, not selling of longs…

GS

FYI:

From David Bahnsen (The Bahnsen Group)

- Our GDP per person was basically the same as Europe’s and Japan’s thirty years ago. Then, for 33 years, we have had booms and busts, good times and bad times, smart decisions and insane ones, and somehow our GDP per person is 33% better than Europe’s and nearly 60% better than Japan’s.

- Our economy has gone from 40% of the GDP of the G7 to 58% – a massive increase in the relative size and power of the economy compared to the rest of the developed world in just thirty years.

- Our income per person is 30% higher than the income per person in Western Europe

- While China has EXPLODED in size and contribution to the global economy over the last three decades, the U.S. was 25% of the global GDP thirty years ago and is still 25% of the global; GDP today.

- Adjusted for inflation, our millennials make 9k more per year than Gen X did when Gen X was the same age and 10k more than baby boomers did when they were the same age (again, adjusting for inflation!).

- American poverty is at an all-time low

Related?

Data from the OECD reveals that while Americans are working ~337 hours a year less than Mexican workers, they’re still notching an extra 75 hours a year compared to the OECD average of 1,716 hours per year. While that may not sound like a lot, at only an extra hour-and-a-half or so a week, it’s a big difference to the hours some other nations are clocking in.

Workers in Germany, for example, put in 1,349 hours on average over 2021 — 367 hours below the OECD average, 442 less than America, and a genuinely staggering 779 hours less than in Mexico.

Source: The Daily Shot

Source: The Daily Shot Source:

Source: